- Technology

- Interactive and Self-Service Kiosk Market

Interactive and Self-Service Kiosk Market Size, Share, and Growth Forecast 2026 - 2033

Interactive and Self-Service Kiosk Market by Component (Hardware, Software, Services), by Kiosk Type (Automated Teller Machines, Self-Checkout Kiosks, Ticketing Kiosks, Information Kiosks, Others), by Screen Size (Less than 15

Interactive and Self-Service Kiosk Market Size and Trend Analysis

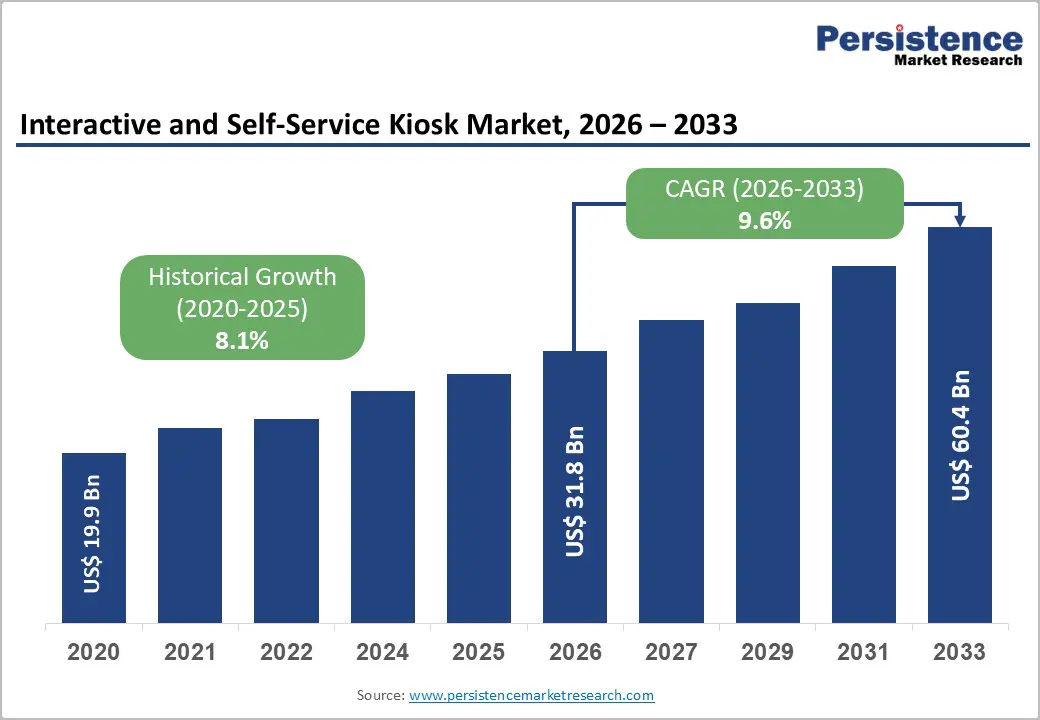

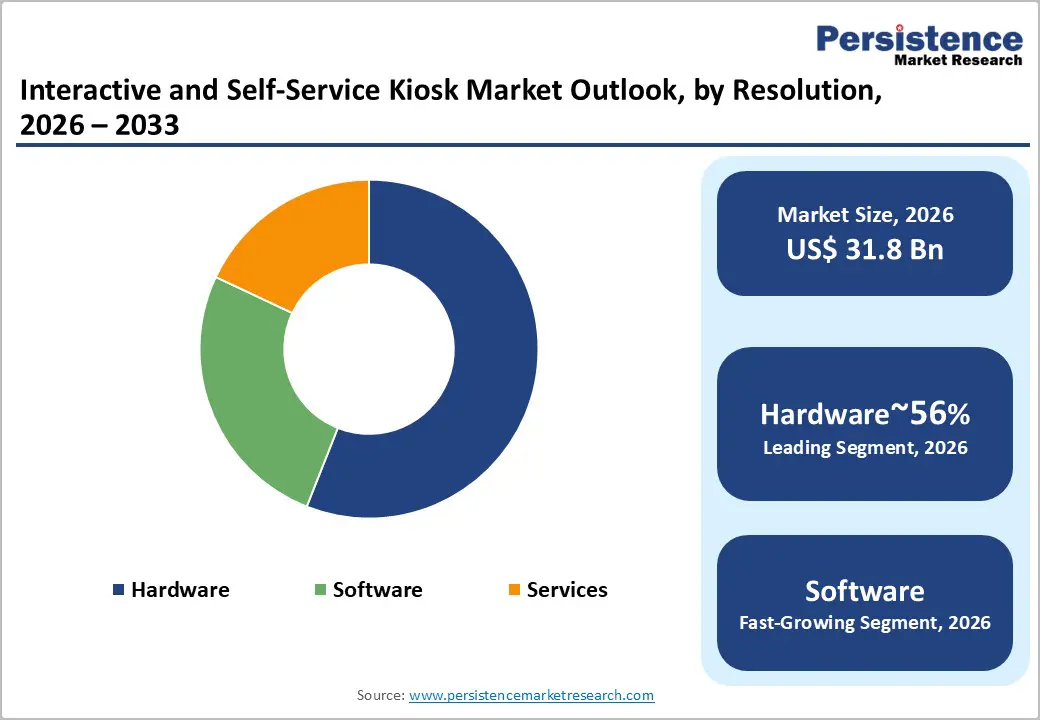

The global interactive and self-service kiosk market size is likely to be valued at US$ 31.8 billion in 2026 and is expected to reach US$ 60.4 billion by 2033, growing at a CAGR of 9.6% during the forecast period from 2026 and 2033. Market growth is driven by accelerating demand for contactless transactions and seamless self-service experiences across the retail, banking, healthcare, and hospitality sectors.

Key Market Highlights

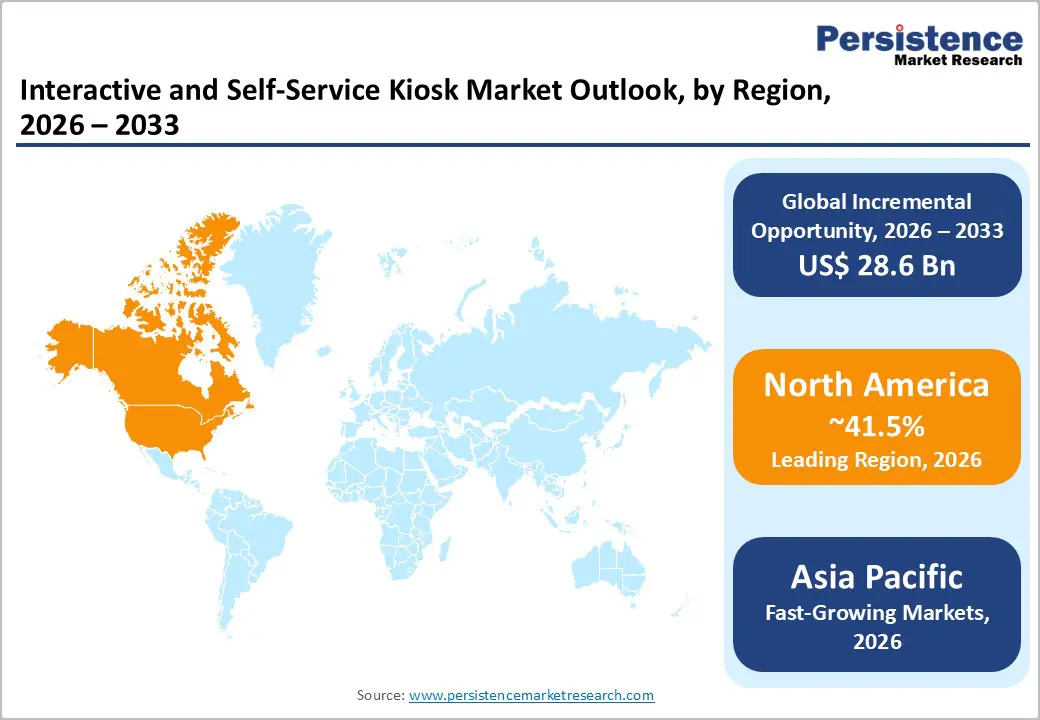

- North America Market Leadership: North America commands approximately 41.5% of global interactive and self-service kiosk market revenue, driven by mature technology adoption infrastructure, extensive retail networks, and banking sector modernization initiatives supporting sustained demand through 2033.

- Asia-Pacific Fastest Regional Growth: Asia-Pacific region is projected to register the highest CAGR of approximately 39% during the forecast period, driven by rapid urbanization, government smart city initiatives in China, Japan, and South Korea, and expanding digital payment adoption across emerging markets including India.

- Retail Sector Dominance with Expanding Healthcare Opportunity: Retail self-checkout kiosks represent the dominant segment capturing approximately 29.75% market share in 2024, while healthcare kiosks emerge as fastest-growing application vertical with CAGR of 15.2% through 2034, driven by labor shortages and patient engagement transformation.

- ATM Segment Leadership Sustained by Digital Banking Evolution: Automated Teller Machines maintain market dominance capturing substantial portion of Interactive and Self-Service Kiosk Market, supported by continuing bank investments in Interactive Teller Machines featuring video conferencing and digital transformation capabilities modernizing branch infrastructure.

- Contactless Payment and AI Integration as Critical Growth Drivers: The convergence of contactless payment adoption (affecting 70% of global transactions) and artificial intelligence integration creates substantial opportunities for advanced kiosk capabilities including personalized user experiences, biometric authentication, and predictive maintenance enabling sustained market expansion through 2033.

| Report Attribute | Details |

|---|---|

|

Interactive and Self-Service Kiosk Market Size (2026E) |

US$ 31.8 Billion |

|

Market Value Forecast (2033F) |

US$ 60.4 Billion |

|

Projected Growth CAGR(2026-2033) |

9.6% |

|

Historical Market Growth (2020-2025) |

8.1% |

Market Dynamics

Market Growth Drivers

Contactless Payment Adoption and Digital Wallet Integration

The integration of contactless payment technologies and digital wallets has become a critical growth driver for the interactive kiosk market. According to recent industry data, approximately 70% of all in-person transactions worldwide are now contactless, with over 80% of global consumers actively using contactless payment methods. NFC (Near Field Communication) technology powers over 95% of contactless transactions globally, making it the dominant standard.

The proliferation of Apple Pay, Google Pay, and regional digital wallets has created substantial demand for kiosks equipped with secure payment terminals. This trend is particularly prominent in North America, where the contactless payment market was valued at approximately US$ 15.98 Billion in 2024 and is projected to reach nearly US$ 71.85 Billion by 2034, representing a growth rate of approximately 16% annually. Retailers and financial institutions are rapidly deploying kiosks featuring modern payment infrastructure to accommodate consumer expectations for frictionless transactions.

Operational Efficiency and Labor Cost Reduction

Organizations across retail, BFSI, and hospitality sectors are deploying self-service kiosks to address mounting labor challenges and operational pressures. The quick-service restaurant (QSR) industry exemplifies this trend, with adoption of kiosks surging 43% globally over the past two years. Major restaurant chains report that 65% of QSR customers indicate they would visit more frequently if kiosks were available. Kiosks deployed in restaurants demonstrate order processing times reduced by up to 40%, with queue reductions of 25-40%.

Average ticket sizes increase by 15% when customers utilize kiosks compared to traditional counter orders, with 20% of customers adding extra items when prompted by digital menus. In retail environments, self-checkout lanes now comprise approximately 38% of checkout options in US grocery chains, reflecting the industry's commitment to automation. Retailers investing in self-service technology report improved customer retention, with shoppers utilizing hybrid checkout models (both self-service and staffed lanes) demonstrating the highest retention rates and customer lifetime value.

Market Restraints

High Initial Installation and Maintenance Costs

Despite strong growth momentum, significant upfront capital requirements remain a substantial barrier to widespread kiosk adoption, particularly among small and medium-sized enterprises. Comprehensive kiosk deployments require substantial investment in hardware components including high-resolution touchscreen displays, payment terminals, barcode scanners, and advanced processors. Additionally, organizations must budget for professional installation services, network infrastructure upgrades, and integration with existing enterprise systems such as point-of-sale and inventory management platforms.

Ongoing maintenance expenses including hardware repairs, software updates, cybersecurity patches, and technical support represent continuous operational costs. Financial institutions implementing ATM networks with advanced features like interactive teller machines and video-assisted advisory capabilities face particularly elevated capital expenditures. Smaller retail outlets and independent hospitality establishments frequently postpone kiosk adoption due to inadequate capital budgets, limiting total addressable market expansion in emerging economies where cost sensitivity remains pronounced.

Data Privacy, Security, and Cybersecurity Concerns

Self-service kiosks collect sensitive customer information including payment card details, personal identification data, and biometric information, creating substantial cybersecurity and regulatory compliance challenges. Kiosks must comply with stringent standards including PCI DSS (Payment Card Industry Data Security Standard), GDPR (General Data Protection Regulation) in Europe, and various national data protection regulations. High-profile security breaches at retail and financial institutions have heightened consumer anxiety regarding data protection at unattended terminals. Biometric authentication systems incorporating facial recognition and fingerprint scanning introduce additional privacy considerations, with regulatory bodies increasingly scrutinizing data collection, storage, and usage practices.

Organizations deploying kiosks must implement robust encryption protocols, secure authentication mechanisms, and comprehensive network security infrastructure. Non-compliance carries substantial financial penalties, operational disruptions, and reputational damage. These compliance requirements and associated security investments create barriers particularly for resource-constrained organizations, potentially slowing market expansion in heavily regulated industries.

Market Opportunities

Healthcare Sector Digital Transformation and Patient Engagement Enhancement

The healthcare industry represents one of the fastest-growing application areas for interactive kiosks, driven by acute labor shortages and the imperative to improve patient experiences. The medical kiosk market is projected to expand from US$1.7 billion in 2024 to approximately US$7.0 billion by 2034, representing a CAGR of 15.2%. Patient self-service kiosks specifically are forecast to grow from US$1.4 billion in 2025 to US$6.3 billion by 2035, advancing at a CAGR of 16.6%. Hospitals increasingly deploy kiosks for patient check-in, insurance verification, appointment scheduling, and consent form collection, with 52.9% of patient self-service kiosk revenue attributed to hospital deployments.

Integration with Electronic Health Records (EHR) systems enables seamless data flow while reducing administrative workload on clinical staff. According to the Health Resources and Services Administration, over 75 million people currently reside in primary care professional shortage areas, creating substantial demand for technology-enabled solutions extending healthcare access. Telemedicine-enabled kiosks facilitate remote patient consultations while supporting infection control protocols. The American Hospital Association has documented significant healthcare staffing crises, making kiosk investments attractive for operational efficiency.

Artificial Intelligence Integration and Personalized User Experiences

Advanced technologies including artificial intelligence, machine learning, and biometric authentication are creating unprecedented opportunities for kiosk functionality enhancement. AI-powered kiosks can analyze customer behavior patterns to deliver personalized product recommendations, targeted promotions, and customized user interfaces. In the QSR industry, AI-driven kiosks enable dynamic menu updates based on inventory availability and demand patterns, with personalized upsell suggestions increasing customer spending.

Facial recognition technology integrated with kiosks streamlines identity verification in banking applications, border control, and age-restricted retail scenarios. Biometric authentication utilizes fingerprint scanning, iris recognition, and facial features for secure, contactless transaction processing. Machine learning algorithms incorporated into kiosk software optimize system performance through predictive maintenance, reducing unexpected downtime. Voice-activated interfaces enhance accessibility for elderly and disabled users, expanding market addressable to previously underserved populations. Organizations implementing edge computing and IoT gateways enable remote monitoring, real-time diagnostics, and centralized management of geographically distributed kiosk networks. These technological innovations position kiosks as intelligent service delivery platforms rather than simple transaction terminals, unlocking new revenue streams and competitive advantages.

Category-wise Insights

Hardware Component Analysis

The hardware component segment maintains significant market importance, encompassing touchscreen displays, processors, payment terminals, barcode scanners, and peripheral devices. Modern kiosk hardware emphasizes durability, responsiveness, and advanced feature integration. Capacitive touchscreen technology dominates the market, providing responsive, multi-touch input capabilities with intuitive user interactions. High-resolution displays with anti-glare coatings and brightness optimization enhance usability in diverse lighting conditions.

Hardware manufacturers including Advantech Co., Ltd., Diebold Nixdorf, and Fuji Electric Co., Ltd. are integrating advanced processors enabling complex applications and real-time processing. The segment captures a substantial portion of total market revenue due to the continuous demand for hardware replacements and system upgrades. Modular hardware designs allow businesses to customize kiosk configurations for specific use cases, from compact models for retail checkout to robust units for banking applications. Advances in system-on-chip (SoC) integrated displays are reducing component complexity while improving reliability and reducing overall system costs.

Software and Services Analysis

The software component holds significant strategic importance, accounting for 72.4% of kiosk software market value specifically. Kiosk software platforms manage user interfaces, transaction processing, content display, and device control across networked installations. Cloud-based deployment models command approximately 61.7% market share, enabling centralized management, real-time updates, and scalable operations across multiple locations.

Windows-based platforms maintain the largest software market share due to broad enterprise compatibility, extensive application ecosystems, and integration with existing Active Directory infrastructure. Android platforms exhibit faster adoption growth, particularly in retail and hospitality applications. Modern kiosk software emphasizes security through user authentication, payment encryption, and compliance with regulatory standards. Remote management capabilities enable operators to deploy content updates, monitor device performance, and troubleshoot issues without on-site intervention. Mobile application integration allows seamless connectivity with customer smartphones, enabling features like mobile wallet payments and pre-registration. Organizations increasingly adopt cloud-based solutions for operational flexibility, reducing infrastructure maintenance and enabling rapid scaling of kiosk networks.

Kiosk Type Analysis - ATM Leadership

Automated Teller Machines (ATMs) represent the dominant kiosk type within the Interactive and Self-Service Kiosk Market, driven by sustained demand from banking and financial institutions modernizing their branch infrastructure. The global ATM market was valued at approximately US$ 63.29 Billion in 2024 and is projected to expand to US$ 134.31 Billion by 2030, advancing at a CAGR of 13.3% from 2025-2030. Banking and financial services kiosks captured approximately 28.58% market revenue in 2024, driven by sustained ATM replacement programs and branch downsizing initiatives. Interactive Teller Machines (ITMs) featuring video conferencing capabilities with remote bankers enable 24/7 service availability while reducing branch staffing requirements.

Modern ATM networks increasingly incorporate advanced security features including biometric authentication, card encryption, and real-time fraud monitoring. Cash recycling ATMs optimize liquidity management while reducing operational visits for cash replenishment. Banks are integrating ATMs with omnichannel strategies, positioning them as critical touchpoints in omnichannel banking ecosystems. The segment's dominance reflects the banking industry's sustained investment in self-service infrastructure and the critical role kiosks play in customer financial access.

End-User Segment Analysis - Retail Dominance

The retail sector represents the largest end-user vertical within the interactive kiosk market, commanding approximately 29.75% revenue share in 2024 and continuing to expand rapidly. Retail self-checkout kiosks are experiencing accelerated adoption, with the segment projected to reach 16.20% CAGR and potentially exceed US$9 billion in absolute expenditure within the forecast period. Major retail chains, including Walmart, Kroger, and Target, have extensively deployed self-checkout and self-ordering kiosks across store locations.

Kiosks function beyond simple checkout applications, enabling endless-aisle browsing for product discovery, price verification, and streamlined returns processing. Hospitality operators represent an increasingly significant vertical, advancing at an estimated 15.80% CAGR driven by staffing challenges and wage inflation. Hospitality establishments deploy counter-order kiosks and drive-through solutions enabling contactless ordering and payment. The hospitality vertical is projected to exceed 20% market share by 2030 if current momentum persists, reflecting the industry's commitment to automation-driven service efficiency.

Screen Size Distribution

The 15"–32" screen size category dominates the interactive kiosk market, balancing user visibility, installation flexibility, and cost considerations. This size range accommodates most applications, including retail checkout, ticketing, information dissemination, and service ordering. Larger displays exceeding 32" serve specialized applications requiring detailed content display or multiple simultaneous user interactions. Compact displays under 15" address space-constrained environments and specialized applications.

Digital signage markets indicate the 32 to 52-inch segment dominates among digital signage displays, driven by demand for interactive and self-service solutions. Organizations deploying kiosks in retail environments increasingly select larger displays to accommodate complex transactions and enhance visual engagement. Healthcare applications benefit from appropriate display sizing facilitating user comfort and accessibility compliance.

Regional Insights

North America Interactive and Self-Service Kiosk Trends

North America maintains market leadership with approximately 39-41.5% global revenue share, supported by mature technology adoption infrastructure, substantial retail and banking sectors, and comprehensive regulatory frameworks. The United States alone dominates regional demand, driven by large-scale kiosk deployments across quick-service restaurants, airports, retail chains, and financial institutions. QSR chains have extensively adopted self-ordering kiosks, with major brands including McDonald's, Wendy's, and Subway implementing systems across thousands of locations.

Airport terminals extensively deploy kiosks for ticketing, wayfinding, and immigration processing, creating substantial demand for ruggedized, high-traffic solutions. US market leadership reflects the region's early adoption of EMV payment standards, tap-to-pay technology, and ADA (Americans with Disabilities Act) compliance requirements shaping kiosk design standards globally. The region's mature retail ecosystem and robust financial services sector create sustained demand for advanced kiosk capabilities. Canada demonstrates elevated healthcare kiosk penetration as provincial healthcare systems seek triage automation and remote-care intake capabilities. Recent developments including Diebold Nixdorf's expansion of US-based manufacturing in North Canton, Ohio demonstrate company commitment to domestic production supporting reliability and localized delivery for major retail, quick-service restaurant, and fuel/convenience customers. The region benefits from strong supply chain infrastructure, advanced technology ecosystems, and sophisticated consumer expectations for self-service capabilities.

Europe Interactive and Self-Service Kiosk Trends

Europe represents a substantial market opportunity with revenue generation of approximately US$ 6,495.7 Million in 2024, projected to grow at a CAGR of 7.3% from 2025 to 2030, reaching approximately US$ 9,884.7 Million by 2030. European markets emphasize unattended kiosks at significantly higher ratios compared to North America, with restaurants and retailers deploying substantially more kiosks per location.

Germany, United Kingdom, France, and Spain represent primary markets driving regional expansion. European kiosk deployments prioritize sustainability initiatives and data protection compliance, particularly GDPR requirements governing personal data collection and biometric information processing. The region demonstrates strong adoption of cloud-based kiosk management systems and contactless payment technologies, with Europe reaching 85% contactless transaction penetration in retail environments. Smart city initiatives across major European metropolitan areas drive deployment of information kiosks supporting urban mobility, public services, and citizen engagement. Advanced regulatory harmonization through EU directives influences product design standards and operational requirements. Diebold Nixdorf and other major manufacturers maintain robust service and support infrastructure across the region, supporting large-scale deployments in retail, banking, and hospitality sectors.

Asia Pacific Interactive and Self-Service Kiosk Trends

Asia-Pacific emerges as the fastest-growing region, projected to register the highest CAGR of approximately 39% during the forecast period, with substantial growth driven by rapid digitalization and smart city development initiatives. The region's interactive kiosk market was valued at approximately US$ 7,115.6 Million in 2024 and is anticipated to grow at approximately 10% CAGR from 2025 to 2030. Self-service kiosk market values in the region reached approximately US$ 4.7 Billion in 2023 and are projected to expand to US$ 11.5 Billion by 2033, advancing at a CAGR of 9.4% from 2024 to 2033.

China, Japan, South Korea, and India represent primary growth markets with distinct development characteristics. China leads the regional market with expanding retail footprints combining smart shelving with kiosk-enabled checkout systems streamlining store operations for convenience retail chains. India leverages kiosks as digital grams, extending government services and banking access to rural residents through technology-enabled platforms. Japan and South Korea pioneer robotics-enabled kiosks performing complex tasks including food preparation and item dispensing, establishing performance benchmarks gradually globalizing. The region's 60% global population share and rising urbanization create substantial demand for contactless payment kiosks supporting swift transaction processing. Smartphone wallet adoption including regional digital payment solutions has established fertile ground for QR code-based interactions and mobile-integrated kiosks. Government smart city initiatives across major Asian metropolitan areas fund infrastructure including intelligent wayfinding kiosks and public service terminals. Cost-effective manufacturing capabilities in the region support rapid innovation cycles and competitive pricing, attracting both international and local market participants.

Competitive Landscape

Market Structure Analysis

The interactive and self-service kiosk market exhibits a fragmented competitive structure with a mix of global market leaders and regional specialists competing across diverse application segments. Global industry leaders including Diebold Nixdorf, Incorporated, Advantech Co., Ltd., KIOSK Information Systems, and GRGBanking command significant market shares through extensive product portfolios, comprehensive service networks, and established customer relationships across banking, retail, and hospitality sectors. These incumbents leverage integrated solutions combining hardware, software, and services, creating substantial switching costs and customer loyalty. Regional competitors and emerging specialists focus on specific market segments including healthcare kiosks, restaurant self-ordering systems, and smart city applications, often demonstrating superior customization capabilities and localized support. Company strategies emphasize technology innovation incorporating artificial intelligence, biometric authentication, and cloud-based management systems to differentiate offerings. Recent consolidation trends including Glory Global Solutions Ltd.'s acquisition of Acrelec and Flooid demonstrate companies' pursuit of complementary capabilities spanning cash handling, self-service checkout, and omnichannel commerce platforms. Emerging market participants and startups introduce disruptive business models including modular hardware designs and software-as-a-service pricing, challenging traditional capital-intensive deployment models. Market leaders invest substantially in research and development, expanding product lines to address emerging applications in healthcare, autonomous vehicles, and smart city infrastructure.

Key Market Developments

- May 2025: Diebold Nixdorf Expands U.S. Manufacturing - Diebold Nixdorf established a new retail technology production line at its North Canton, Ohio facility to manufacture self-service checkout systems and kiosks domestically, strengthening supply chain reliability and enabling rapid scaling for major QSR and retail customer deployments.

- July 2025: Glory Global Solutions Advances Integrated Kiosk Solutions - Glory Global Solutions Ltd. announced integrated platform combining cash handling expertise, Acrelec self-service checkout and kiosk capabilities, and Flooid omnichannel commerce technology, enabling seamless customer experiences across banking, retail, and food service verticals.

- December 2024: Smashburger Chain Deploys Diebold Nixdorf Self-Service Kiosks - Smashburger, an Italian smashburger chain, partnered with Diebold Nixdorf to implement self-service kiosks at its Udine, Italy restaurant location, reflecting accelerating QSR adoption of automated ordering solutions across European markets.

Companies Covered in Interactive and Self-Service Kiosk Market

- Advantech Co., Ltd.

- Diebold Nixdorf

- Incorporated

- DynaTouch Corporation

- Embross

- Frank Mayer and Associates, Inc.

- Glory Global Solutions Ltd.

- GRGBanking

- IER

- Aksor SAS

- Azkoyen SA

- Fuji Electric Co., Ltd.

- Thales Group

- Hitachi Payment Services Pvt. Ltd.

- KIOSK Information Systems

- NCR Corporation

- Olea Kiosks Inc.

- Posiflex Technology Corporation

Frequently Asked Questions

The Interactive and Self-Service Kiosk Market is projected to reach US$ 60.4 Billion by 2033, growing from US$ 31.8 Billion in 2026, representing a CAGR of 9.6% during the forecast period driven by accelerating demand for contactless transactions and operational automation.

Primary growth drivers include rising contactless payment adoption affecting 70% of global transactions, businesses' imperative to reduce labor costs amid acute staffing challenges, post-pandemic consumer preference for touchless interactions, and technological advancements in artificial intelligence and biometric authentication enhancing kiosk capabilities.

Automated Teller Machines (ATMs) represent the dominant kiosk type, capturing substantial market share driven by sustained banking sector investments in branch automation, Interactive Teller Machine deployments offering video conferencing and extended services, and continuous modernization of banking infrastructure to support omnichannel customer engagement strategies.

North America leads the market with approximately 41.5% global revenue share, supported by mature technology adoption infrastructure, extensive retail and banking sectors, comprehensive regulatory frameworks, and early adoption of advanced payment standards and accessibility requirements shaping global industry standards.

The medical kiosk market represents the fastest-growing application vertical, projected to expand from US$ 1.7 Billion in 2024 to US$ 7.0 Billion by 2034 at a CAGR of 15.2%, driven by acute healthcare labor shortages, need for patient engagement enhancement, and opportunities for operational efficiency through automated check-in and scheduling systems.

Key market participants include Diebold Nixdorf, Incorporated, Advantech Co., Ltd., KIOSK Information Systems, GRGBanking, Glory Global Solutions Ltd., Fuji Electric Co., Ltd., NCR Corporation, and Olea Kiosks Inc., competing through integrated solutions combining hardware, software, and services with strategic focus on innovation and customer experience enhancement.