- Medical Devices

- Fundus Camera Market

Fundus Camera Market Size, Share, and Growth Forecast 2026 - 2033

Fundus Camera Market by Product Type (Non-Mydriatic, Mydriatic, Hybrid, ROP), by Modality (Tabletop, Handheld), Application (Diabetic Retinopathy Diagnosis, Glaucoma & AMD Diagnosis, Others), End-user (Hospitals, Ophthalmology Clinics, Optometrist Offices, Others), and Regional Analysis, 2026-2033

Fundus Camera Market Size and Trend Analysis

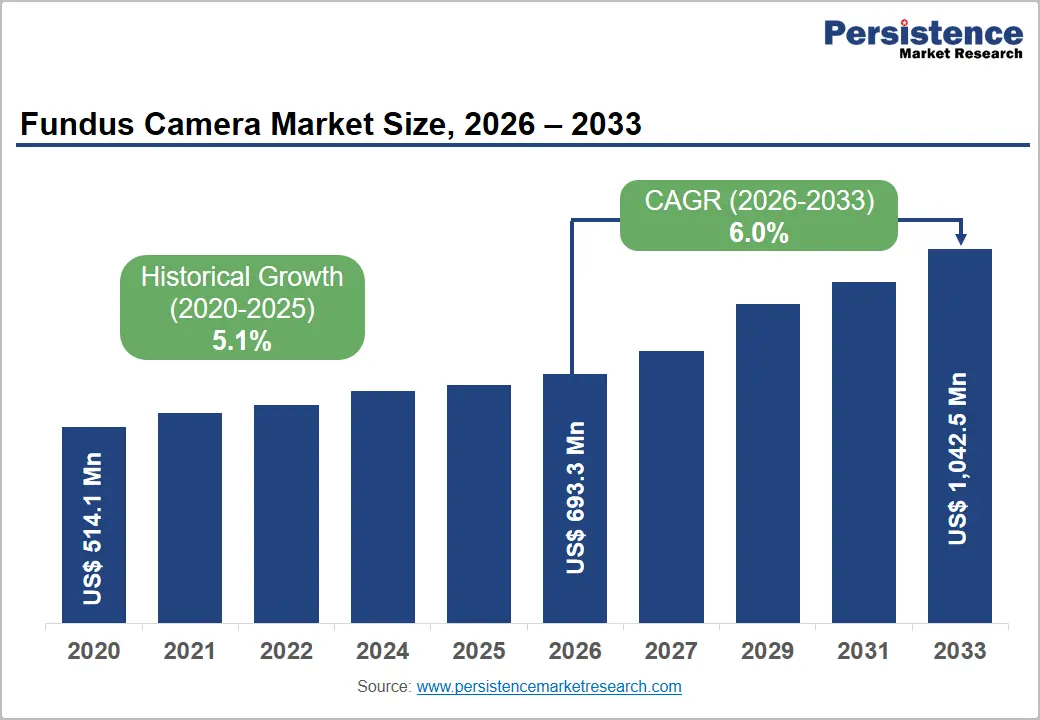

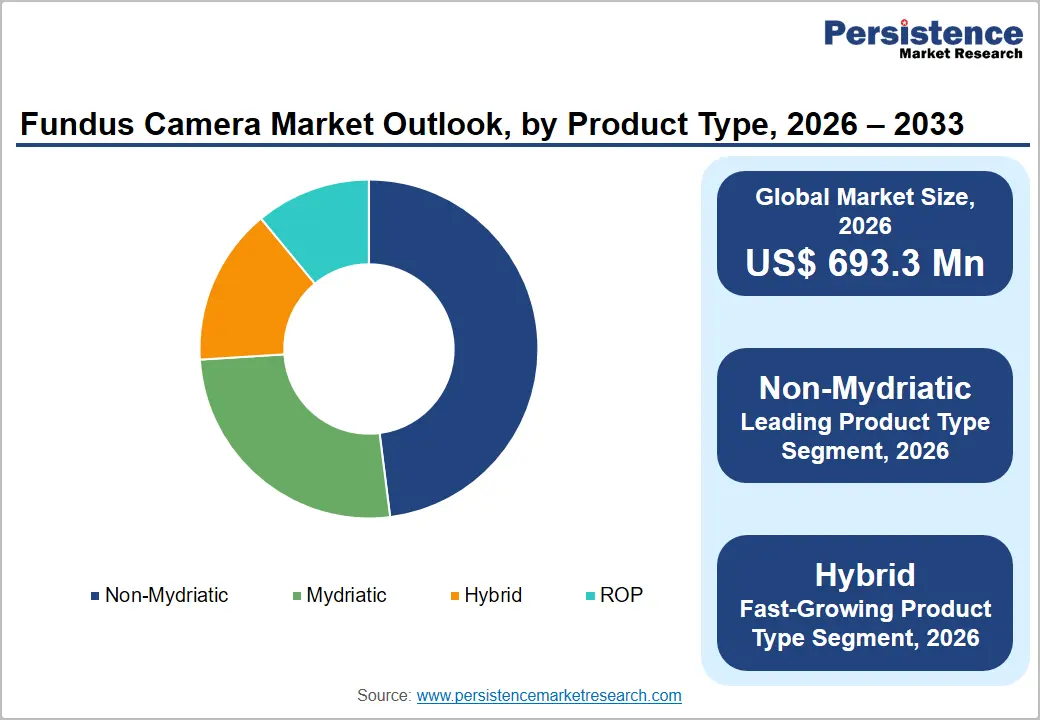

The global fundus camera market size is expected to be valued at US$ 693.3 million in 2026 and projected to reach US$ 1,042.5 million by 2033, growing at a CAGR of 6.0% between 2026 and 2033. The accelerating global burden of diabetes-related retinal diseases, rising prevalence of age-related macular degeneration (AMD) and glaucoma, and the transformative integration of artificial intelligence (AI) into fundus imaging for automated retinopathy screening fuel growth. The International Diabetes Federation (IDF) estimates that over 537 million adults globally have diabetes, with diabetic retinopathy (DR) affecting approximately one-third of all diabetic patients, creating an enormous and expanding base of patients requiring systematic retinal imaging. Simultaneous advances in non-mydriatic and handheld fundus camera technology are extending diagnostic access beyond specialty eye care settings into primary care, community screening, and teleophthalmology programs globally.

Key Industry Highlights:

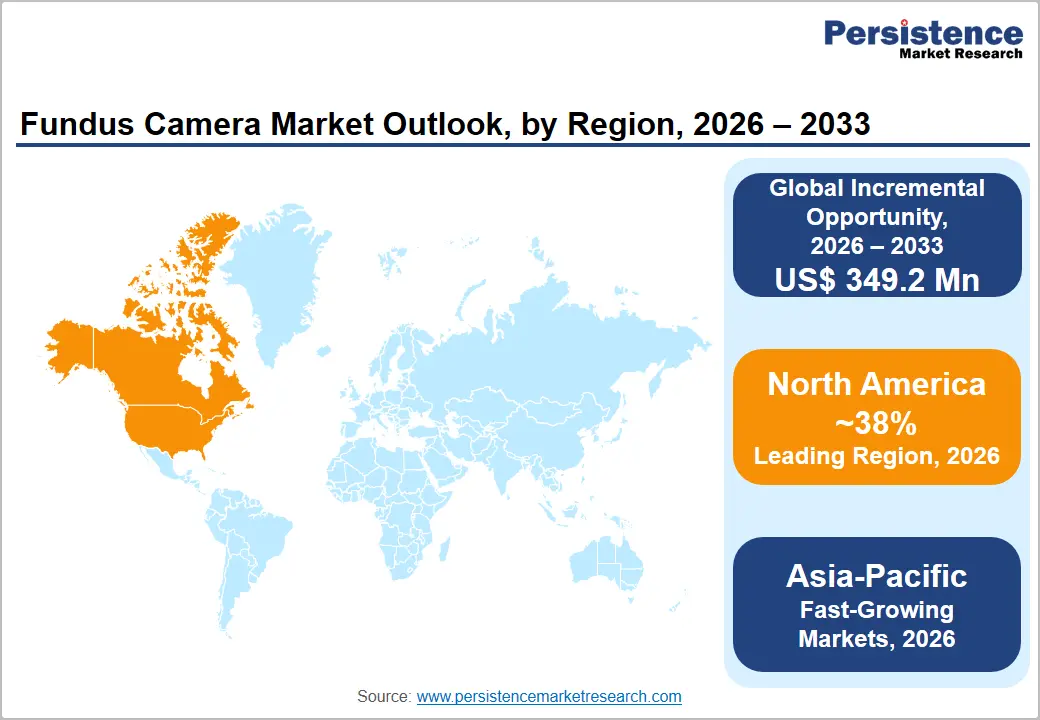

- Leading Region – North America: North America is likely to register approximately 38% of the global fundus camera market in 2026, anchored by over 37 million U.S. diabetic patients, FDA-cleared autonomous AI DR screening systems, CMS reimbursement coverage, and commercial leadership of Carl Zeiss Meditec and Topcon.

- Fastest Growing Region – Asia Pacific: Asia Pacific is the fastest-growing fundus camera market, driven by China's and India's combined 230+ million diabetic patients (IDF), national DR screening program expansion under Healthy China 2030 and NPCBVI, and domestic portable imaging innovators like Remidio.

- Dominant Segment – Non-Mydriatic Fundus Cameras: Non-mydriatic cameras lead the product type segment with approximately 48% share in 2026, driven by patient-friendly, dilation-free imaging that enables high-throughput DR screening adopted as the standard modality by the NHS Diabetic Eye Screening Programme and equivalent national programs globally.

- Fastest Growing Segment – Hybrid Fundus Cameras: Hybrid fundus cameras integrating mydriatic/non-mydriatic capability with AI grading software are the fastest-growing product type, endorsed by the ADA 2024 Standards of Care for teleretinal DR screening and increasingly deployed in primary care and endocrinology settings outside traditional ophthalmology clinics.

- Key Market Opportunity – Handheld and AI-Integrated Fundus Cameras in LMICs: Portable fundus cameras integrated with AI DR grading, exemplified by Optomed Aurora and Remidio's smartphone-based platforms, offer a transformative teleophthalmology opportunity across India, Southeast Asia, and Africa, where ophthalmologist shortages create a massive unserved retinal screening demand.

Market Dynamics

Drivers – Rise in Global Diabetic Retinopathy Burden Creating Mass Screening Imperative

Diabetic retinopathy is the world's leading cause of preventable blindness among working-age adults, and its rising global incidence is the single most powerful demand driver for fundus cameras. The IDF projects that global diabetes prevalence will reach 783 million by 2045, with diabetic retinopathy (DR) affecting approximately 103 million people globally as of 2020 per research published in The Lancet Diabetes & Endocrinology. The American Academy of Ophthalmology (AAO) recommends annual dilated fundus examination for all diabetic patients, creating a structural, policy-mandated screening volume that scales directly with the diabetic population. National DR screening programs including the NHS Diabetic Eye Screening Programme (DESP) in the U.K., covering over 2.8 million patients annually, exemplify the large-scale institutional demand that fundus cameras serve globally.

AI-Powered Fundus Imaging Transforming Screening Capacity and Diagnostic Accuracy

The integration of artificial intelligence with fundus cameras is fundamentally transforming the screening landscape, enabling automated, high-throughput diabetic retinopathy and AMD detection with clinician-level accuracy. The FDA approved IDx-DR (Digital Diagnostics) in 2018 as the first autonomous AI diagnostic system cleared for clinical use, requiring no specialist interpretation for DR screening decisions. Subsequently, Google Health's deep-learning retinal imaging algorithms and Topcon's Harmony AI platform have been validated in peer-reviewed studies published in Nature Medicine and JAMA Ophthalmology. AI integration increases fundus camera utilization rates in primary care settings by reducing the specialist interpretation bottleneck, dramatically expanding the addressable market for fundus imaging beyond traditional ophthalmology practice settings.

Restraints - High Equipment Cost and Reimbursement Limitations in Emerging Markets

Premium fundus cameras, particularly ultra-widefield and AI-integrated tabletop systems, carry price points ranging from US$ 15,000 to over US$ 60,000 per unit, limiting adoption in resource-constrained healthcare settings. In many low- and middle-income countries (LMICs) with the highest diabetic retinopathy burden, public hospital procurement budgets and limited health insurance reimbursement for retinal imaging create significant access barriers. The WHO Vision 2020 initiative has highlighted equipment cost as a primary barrier to retinal diagnostics scale-up in Sub-Saharan Africa and South Asia, constraining market penetration in high-burden geographies.

Shortage of Trained Ophthalmologists Limiting Image Interpretation Capacity

The global shortage of trained ophthalmologists and retinal specialists constrains the clinical utility of fundus imaging in many regions. The International Council of Ophthalmology (ICO) estimates a global deficit of over 100,000 ophthalmologists, with the most acute shortages in Sub-Saharan Africa and South Asia. In rural and peri-urban settings, fundus cameras may be acquired but remain underutilized due to insufficient locally available expertise for image grading, limiting the return on investment for healthcare facilities and dampening repeat purchasing rates for consumables and upgrades.

Opportunities - Handheld Fundus Cameras Enabling Teleophthalmology and Point-of-Care Retinal Screening

Handheld and portable fundus cameras represent one of the most transformative growth opportunities in the fundus camera market, enabling retinal imaging at the point of care in primary care clinics, diabetic care centers, neonatal intensive care units (for ROP screening), and community outreach settings. Optomed Oy's Aurora handheld fundus camera and Remidio Innovative Solutions' smartphone-based fundus imaging platforms are expanding retinal imaging into settings where tabletop systems are impractical.

The WHO has identified teleophthalmology as a priority strategy for closing the specialist access gap in LMICs, creating policy-level demand for portable imaging solutions. In the U.K., NHS-funded community retinal screening hubs operating with handheld cameras are demonstrating the model's scalability, with India's National Programme for Control of Blindness (NPCB) increasingly incorporating portable fundus imaging into district-level diabetic eye care.

AI-Integrated Hybrid Fundus Cameras: The Fastest-Growing Product Innovation

Hybrid fundus cameras combining mydriatic and non-mydriatic capabilities in a single platform integrated with AI-driven automated grading software represent the fastest-growing product innovation in the fundus camera market. These platforms eliminate the clinical choice between dilation-dependent image quality and patient convenience, capturing high-resolution fundus images with or without mydriasis. Carl Zeiss Meditec's CLARUS ultra-widefield fundus imaging system and Topcon's Maestro2 OCT-fundus camera hybrid exemplify this convergence. The American Diabetes Association (ADA) 2024 Standards of Care specifically endorse validated teleretinal screening programs utilizing non-mydriatic and hybrid imaging platforms.

Category-wise Analysis

Product Type Insights

Non-mydriatic fundus cameras hold the leading position in the fundus camera market by product type, commanding approximately 48% revenue share in 2026. Non-mydriatic cameras capture retinal images without requiring pharmacological pupil dilation, eliminating the 20-30 minute dilation wait time, associated patient discomfort, and temporary vision impairment that deters patient compliance in routine screening programs. This patient-friendly workflow has made non-mydriatic systems the preferred choice for high-throughput diabetic retinopathy screening programs, primary care integration, and community-based retinal imaging initiatives. The NHS Diabetic Eye Screening Programme exclusively uses non-mydriatic cameras as the standard imaging modality across its 200+ screening centers a procurement standard emulated by national DR programs in Australia, Canada, and Singapore, cementing this segment's commercial leadership.

Modality Insights

Tabletop fundus cameras represent the leading modality segment in the fundus camera market, accounting for approximately 72% share in 2026. Tabletop systems deliver superior image resolution, wider field of view options (including ultra-widefield imaging covering up to 200 degrees of the retina), and robust AI integration capabilities that are critical for clinical diagnostic accuracy in hospital and ophthalmology clinic settings. The American Academy of Ophthalmology (AAO) clinical guidelines specify high-resolution fundus imaging as the standard of care for diabetic retinopathy grading, glaucoma documentation, and AMD monitoring requirements best fulfilled by tabletop systems. Premium tabletop platforms from Carl Zeiss Meditec, Topcon, NIDEK, and Canon command premium pricing that further reinforces the modality's revenue leadership.

Regional Insights

North America Fundus Camera Market Trends and Insights

North America dominated the global fundus camera market in 2026 likely to account for the revenue contribution valued at US$ 693.3 Mn in 2026, due to advanced ophthalmic infrastructure, strong diabetic retinopathy screening programs, and high adoption of AI-enabled retinal imaging technologies. The region benefits from increasing prevalence of diabetes, age-related macular degeneration (AMD), and glaucoma, which require routine retinal examinations. According to the CDC, around 9.6 million Americans were living with diabetic retinopathy in 2021, significantly increasing demand for retinal imaging systems. The presence of major ophthalmic device manufacturers, favorable reimbursement systems, and strong hospital investments further supported market expansion.

U.S. Fundus Camera Market Trends and Insights

The United States dominated the North American fundus camera market and is likely to reach nearly US$180 million by 2026. Prevalence of high diabetes, expanding elderly population, and increasing adoption of retinal screening technologies in hospitals and eye clinics highlight the significance of the fundus camera in medical setting. According to the CDC, approximately 9.6 million people in the U.S. were affected by diabetic retinopathy in 2021, while over 1.8 million suffered from vision-threatening diabetic retinopathy. Rising demand for early diagnosis of glaucoma and AMD further accelerated fundus camera utilization. The country also witnessed the rapid adoption of AI-integrated retinal imaging platforms and teleophthalmology solutions across primary healthcare networks.

Canada Fundus Camera Market Trends and Insights

Canada is likely to account for a CAGR of around 6.8% during the forecast period. Rise in diabetic population, increasing awareness regarding retinal disorders, and government-supported vision care initiatives. Canada experienced a high adoption of portable and handheld fundus cameras, particularly in remote and underserved regions where access to ophthalmologists remained limited. Increasing investments in digital healthcare and telemedicine also accelerated demand for advanced retinal imaging systems. The country’s aging population contributed significantly to the growing burden of age-related eye diseases such as AMD and glaucoma, supporting the continuous expansion of ophthalmic diagnostic infrastructure across hospitals and specialty clinics.

Europe Fundus Camera Market Trends and Insights

Europe represented a significant region in the fundus camera market due to strong public healthcare systems, widespread ophthalmic screening programs, and rising prevalence of chronic eye diseases. The increasing elderly population across European countries has substantially increased retinal disease incidence, especially diabetic retinopathy and macular degeneration.

The region also benefited from advanced hospital infrastructure and strong adoption of digital ophthalmology technologies. According to European health studies, diabetic retinopathy prevalence among diabetic patients remained above 20% in several countries, supporting continued retinal imaging demand. Government-funded screening initiatives and growing awareness regarding preventable blindness further strengthened market growth. Europe remained the second-largest regional contributor to the global market in 2026.

Germany Fundus Camera Market Trends and Insights

Germany is projected to lead the fundus camera market in Europe and reach around US$70 Million by 2026. The country’s dominance was attributed to strong ophthalmology infrastructure, high healthcare expenditure, and increasing retinal disease screening rates. Germany recorded significant growth in diabetic retinopathy cases due to rising diabetes prevalence among aging adults. Hospitals and ophthalmology centers increasingly adopted ultra-widefield and non-mydriatic fundus cameras for early retinal disease diagnosis. The country also witnessed growing implementation of AI-assisted retinal imaging technologies in clinical practice. The presence of major ophthalmic device companies and strong reimbursement support further accelerated market penetration across healthcare facilities.

France Fundus Camera Market Trends and Insights

France fundus camera is likely to achieve a CAGR of approximately 6.5% during the forecast period. Rise in elderly population and rising government initiatives for diabetic eye screening are major contributors. France experienced an expanding demand for digital retinal imaging systems in both hospitals and outpatient ophthalmology clinics. Increasing adoption of teleophthalmology services and portable fundus cameras improved retinal screening accessibility in semi-urban and rural regions. The growing prevalence of diabetes-related vision impairment and AMD also accelerated demand for advanced ophthalmic diagnostics. Continuous technological advancements in retinal imaging and supportive healthcare policies further strengthened the country’s market outlook.

Asia Pacific Fundus Camera Market Trends and Insights

Asia Pacific is projected to register the fast growth in the fundus camera market due to the rapidly increasing diabetic population, expanding healthcare infrastructure, and improving access to ophthalmic care. Countries such as China, India, and Japan witnessed substantial increases in retinal disorders associated with diabetes and aging populations. Rising government initiatives for blindness prevention and diabetic retinopathy screening significantly boosted retinal imaging adoption. Increasing investments in teleophthalmology and portable fundus cameras also supported rural eye care expansion. The region benefited from growing medical tourism and rising healthcare expenditure, particularly across emerging economies. Asia-Pacific was expected to witness the highest CAGR among all regions through the forecast period.

China Fundus Camera Market Trends and Insights

China dominated the Asia-Pacific fundus camera market and was expected to reach approximately US$ 60 Mn in 2026, driven by the high prevalence of diabetes, increasing elderly population, and large-scale ophthalmic screening initiatives. Studies indicated that diabetic retinopathy prevalence among diabetic patients in China exceeded 23%, creating substantial demand for retinal imaging systems. The country witnessed the rapid adoption of AI-based ophthalmic diagnostics and ultra-widefield imaging technologies across hospitals and eye care centers. Government investments in healthcare modernization and expansion of telemedicine services also supported increasing deployment of portable fundus cameras in community healthcare settings.

India Fundus Camera Market Trends and Insights

India was expected to grow with a CAGR of nearly 7.5% during the forecast period. Rising diabetes burden, expanding eye screening programs, and improving access to ophthalmic care significantly supported market growth. India witnessed increasing demand for affordable handheld and non-mydriatic fundus cameras, especially in rural and semi-urban healthcare centers. Government initiatives for blindness prevention and diabetic retinopathy screening accelerated the adoption of portable retinal imaging systems. The country also emerged as a key hub for AI-enabled ophthalmic innovations and teleophthalmology deployment. Growing healthcare investments and rising awareness regarding early retinal disease diagnosis continued to strengthen long-term market opportunities.

Competitive Landscape

The fundus camera market is moderately consolidated, with Carl Zeiss Meditec AG, Topcon Corporation, NIDEK Co., Ltd., and Canon Inc. collectively commanding over 55% of global revenues. These leaders differentiate through ultra-widefield imaging capabilities, AI grading software integration, and comprehensive service networks. Emerging players Optomed Oy, Remidio, and Clarity Medical Systems compete in the high-growth handheld and portable segment, targeting LMICs and teleophthalmology programs. Key business model trends include AI software-as-a-service (SaaS) layers on top of hardware sales and cloud-based retinal image management platforms. Strategic M&A activity is consolidating specialty imaging capabilities into broader ophthalmic platform ecosystems.

Key Developments:

June 2025: Carl Zeiss Meditec AG announced that the ZEISS CLARUS 700 received approval from China’s National Medical Products Administration (NMPA). The approval expanded the company’s presence in the Chinese ophthalmic imaging market and strengthened access to advanced retinal imaging technologies.

June 2025: Optomed Oy launched the next-generation handheld fundus camera, Optomed Lumo, to strengthen its portable retinal imaging portfolio. The device was introduced to improve point-of-care eye screening and support early detection of retinal diseases such as diabetic retinopathy and glaucoma.

Global Fundus Camera Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 514.1 Million |

|

Projected Market Value (2026) |

US$ 693.3 Million |

|

Projected Market Value (2033) |

US$ 1,042.5 Million |

|

CAGR (2026-2033) |

6.0% |

|

Leading Region |

North America, 38% share |

|

Dominant Product Type |

Non-Mydriatic, 48% share |

|

Top-ranking Modality |

Tabletop, 60% share |

|

Incremental Opportunity |

US$ 349.2 Million |

Companies Covered in Fundus Camera Market

- Carl Zeiss Meditec AG

- Topcon Corporation

- NIDEK Co., Ltd.

- Canon Inc.

- Optomed Oy

- Kowa Optimed

- CenterVue S.p.A. (Revenio Group)

- Clarity Medical Systems

- Optovue Inc.

- Epipole Ltd.

- Visionix

- Remidio Innovative Solutions Pvt. Ltd.

- Others

Frequently Asked Questions

The global fundus camera market is projected to be valued at US$ 693.3 million in 2026.

Rising diabetic retinopathy prevalence, aging population, increasing eye screenings, teleophthalmology adoption, and technological advancements.

North America leads with approximately 38% market share in 2026.

Expansion in teleophthalmology, AI-based retinal diagnostics, portable imaging devices, and emerging healthcare infrastructure investments.

Carl Zeiss Meditec AG, Topcon Corporation, NIDEK Co., Ltd., Canon Inc., Optomed Oy, Remidio Innovative Solutions.