- Beauty & Personal Care

- Frizz Control Shampoo Market

Frizz Control Shampoo Market Size, Share, and Growth Forecast 2026 - 2033

Frizz Control Shampoo Market by Formulation (Herbal / Botanical, Silicone Based, Protein / Keratin Based, Paraben-Free / Sulfate-Free, Vegan / Cruelty-Free, Other), Price Segment (Economy / Mass Market, Mid-Range, Premium / Luxury), Packaging Type (Bottles, Sachets/Pouches, Tubes, Dispenser), Distribution Channel, and Regional Analysis, 2026 - 2033

Frizz Control Shampoo Market Size and Trend Analysis

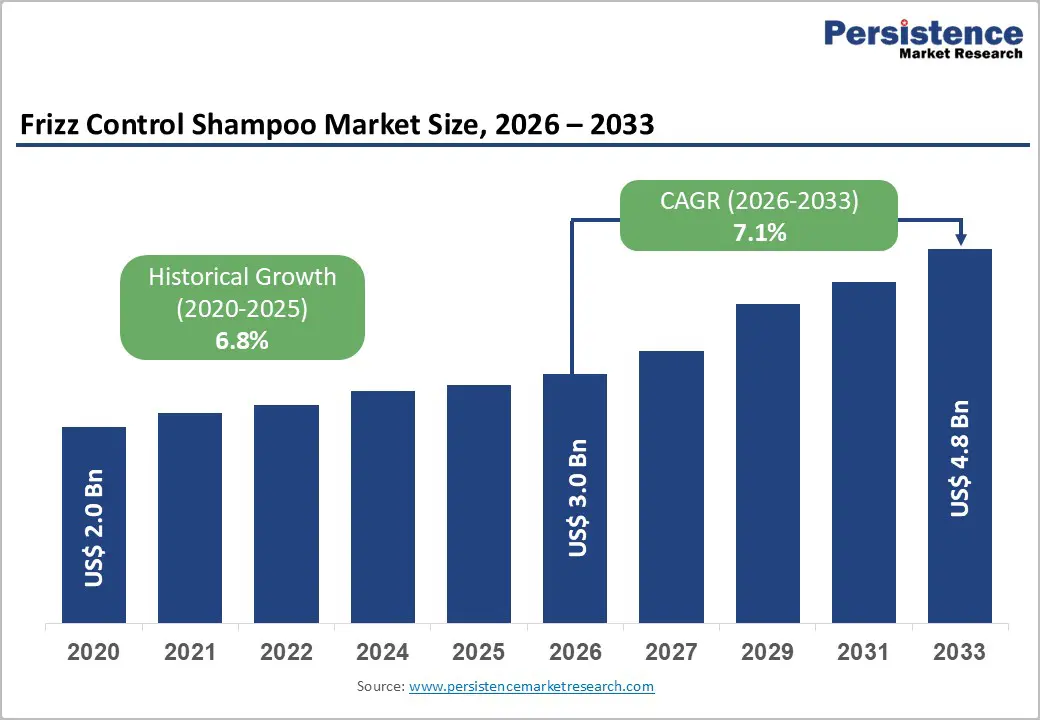

The global Frizz Control Shampoo market size is expected to be valued at US$ 3.0 billion in 2026 and projected to reach US$ 4.8 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033. The market expansion is fundamentally anchored in surging global consumer awareness around hair health, humidity-induced frizz management, and the progressive premiumization of personal hair care routines.

Rising demand for clean-label, sulfate-free, and protein-enriched formulations across North America, Europe, and Asia Pacific, coupled with the explosive growth of e-commerce as a primary beauty retail channel, is structurally broadening the addressable consumer base. Simultaneously, increasing consumer inclination toward vegan, cruelty-free, and botanically derived hair care products is accelerating formulation innovation across leading global brands, ensuring consistent market demand momentum through the forecast horizon.

Key Industry Highlights:

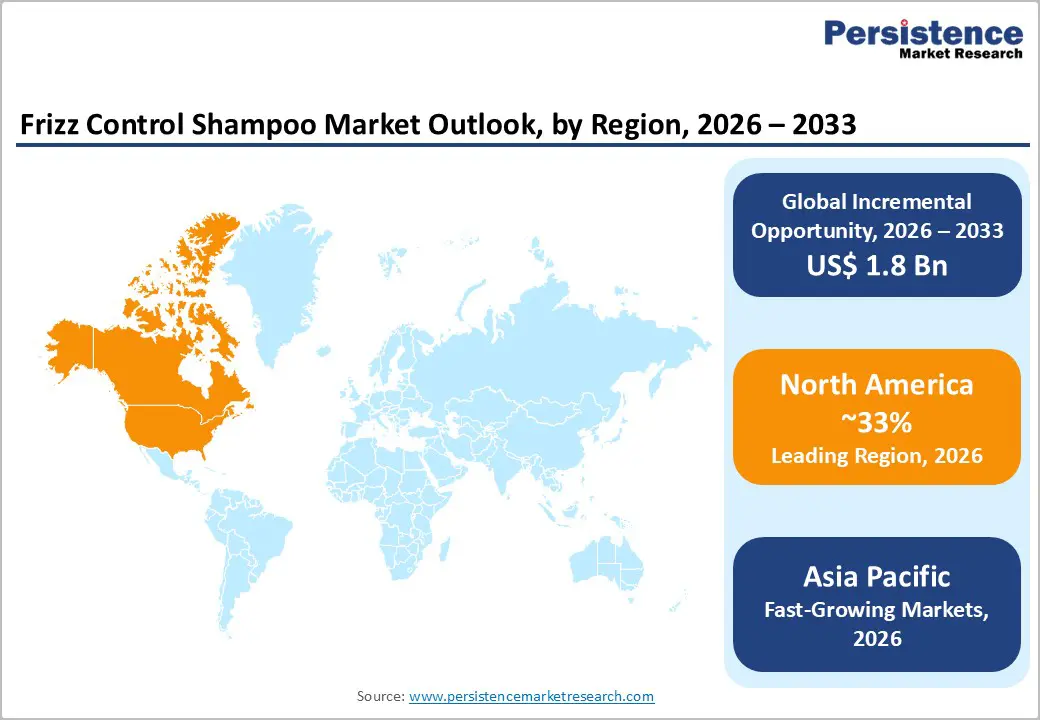

- Leading Region: North America leads the global Frizz Control Shampoo market with approximately 33% revenue share in 2025, driven by the United States’ mature hair care innovation ecosystem, robust clean-label consumer demand, and the comprehensive regulatory transformation introduced by the FDA’s MoCRA in 2022.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, projected at approximately 9.3% CAGR (2026–2033), powered by high-humidity climatic conditions across Southeast Asia, rising middle-class personal care spending in India and China, and accelerating e-commerce beauty retail penetration across ASEAN economies.

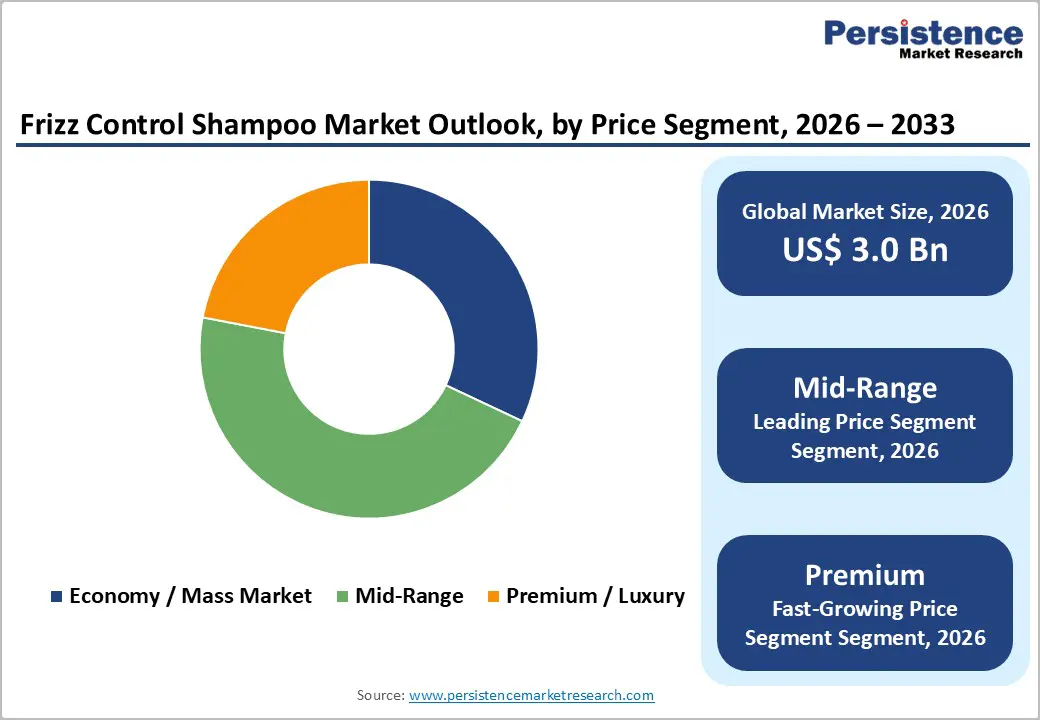

- Dominant Segment: The Mid-Range price segment dominates the Frizz Control Shampoo market with approximately 43% market share in 2025, reflecting its broad demographic accessibility and proven demand resilience across diverse economic cycles, anchored by major brands from Procter & Gamble, Unilever, and Henkel.

- Fastest Growing Segment: E-commerce Platforms represent the fastest-growing distribution channel, fueled by subscription-based hair care models, AI-personalized product recommendation engines, and rising D2C brand penetration across Amazon, Tmall, Nykaa, and regional beauty digital marketplaces.

- Key Opportunity: The most compelling market opportunity lies in the Vegan / Cruelty-Free and Herbal Botanical formulation segment, where brand investments in certified clean-label, ethically sourced frizz control formulations are positioned to capture significant consumer premiumization spending and expanded specialty retail distribution through 2033.

| Key Insights | Details |

|---|---|

|

Frizz Control Shampoo Market Size (2026E) |

US$ 3.0 Billion |

|

Market Value Forecast (2033F) |

US$ 4.8 Billion |

|

Projected Growth CAGR (2026–2033) |

7.1% |

|

Historical Market Growth (2020–2025) |

6.8% |

Market Dynamics

Drivers - Rise in Consumer Demand for Specialized and Clean-Label Hair Care Formulations

The global consumer shift toward specialized, ingredient-conscious personal care products represents a defining growth driver for the frizz control shampoo market. According to Cosmetics Europe, the European personal care market recorded retail sales exceeding €90 billion in 2023, with haircare among the most consistently expanding sub-categories. A growing proportion of consumers, particularly millennials and Generation Z, actively scrutinize ingredient labels, driving brands to reformulate legacy products to eliminate sulfates, parabens, and silicones. The U.S. Food and Drug Administration (FDA) has further reinforced this trend through regulatory reviews of certain cosmetic ingredient safety standards under the Modernization of Cosmetics Regulation Act of 2022 (MoCRA), compelling manufacturers to invest in transparent, compliant, and clinically substantiated formulations. This regulatory and consumer-behavioral convergence is generating measurable and durable demand for premium frizz control shampoos designed around clean, functional ingredient platforms.

Rising Prevalence of Hair Damage and Climate-Driven Frizz Concerns Expanding Product Adoption

Climate variability and increasing atmospheric humidity levels are materially expanding the addressable consumer base for frizz control shampoos globally. According to the National Oceanic and Atmospheric Administration (NOAA), average global surface temperatures have risen consistently over the past three decades, contributing to elevated ambient humidity in tropical, subtropical, and coastal regions, conditions that directly amplify hair porosity and frizz susceptibility in a majority of hair types. A 2022 consumer survey published in the International Journal of Cosmetic Science found that over 60% of respondents globally identified frizz and manageability as their primary hair care concern. This pervasive, cross-demographic need drives persistent and recurring purchases of anti-frizz shampoos across both mass-market and premium price tiers, creating a structurally resilient and volume-stable demand foundation for manufacturers and brands operating across the global hair care value chain.

Restraints - Intensifying Competition from Multi-Benefit Hair Care Alternatives and DIY Treatments

The frizz control shampoo market faces meaningful competitive pressure from the proliferation of multi-benefit combination hair care products, including conditioning shampoos, co-washing products, leave-in treatments, and hair serums, that consolidate frizz-control functionality with broader moisturization, color protection, or volumizing benefits within a single SKU. This trend, significantly amplified by influencer-driven social media content promoting DIY hair masking, oil treatments, and budget-conscious hair care routines, is diluting consumer category loyalty specifically toward single-benefit frizz control shampoos. The U.S. Bureau of Labor Statistics Consumer Expenditure Survey consistently records discretionary personal care spending adjustments during periods of economic pressure, further compressing unit purchase frequency in the value-sensitive mass market segment.

Regulatory Restrictions on Key Functional Ingredients Complicating Formulation Innovation

Mounting regulatory scrutiny across key markets over certain functional hair care ingredients is creating significant formulation and compliance challenges for frizz control shampoo manufacturers. The European Commission’s Scientific Committee on Consumer Safety (SCCS) has progressively tightened permissible concentration limits on formaldehyde-releasing agents and certain preservative systems widely used in keratin-based smoothing and frizz-control formulations. In the United States, the FDA’s MoCRA framework has introduced new mandatory adverse event reporting and substantiation requirements that increase compliance costs, particularly for smaller, independent brands. These intersecting regulatory developments are constraining formulation flexibility, extending product development timelines, and disproportionately impacting mid-tier manufacturers with limited regulatory and R&D infrastructure.

Opportunity - Accelerating Growth of Vegan, Cruelty-Free, and Herbal Botanical Frizz Control Formulations

The global acceleration of ethical consumerism presents a high-value, strategically differentiated opportunity for frizz control shampoo brands to invest in vegan, cruelty-free, and herbal botanical formulation platforms. According to the Vegan Society, the global market for vegan-certified personal care products has grown at a double-digit pace in recent years, with certification increasingly functioning as a baseline consumer expectation rather than a differentiating premium. The Leaping Bunny Program, administered by Cruelty Free International, has certified thousands of personal care product lines globally, reflecting both consumer demand and retailer listing requirements aligned with cruelty-free standards. Botanical extracts, including argan oil, shea butter, coconut-derived actives, aloe vera, and rice protein, are gaining prominent positioning in new frizz control launches, particularly among indie beauty brands and Tier-1 FMCG multinationals reformulating legacy product lines. Brands investing proactively in certified ethical formulation frameworks are strategically positioned to command premium price points and secure growing shelf placement in specialty and natural beauty retail channels globally.

E-Commerce and Direct-to-Consumer Channel Expansion Unlocking New Revenue Pockets

The structural shift toward e-commerce and branded direct-to-consumer (D2C) digital channels represents one of the most actionable and highest-return commercial opportunities for frizz control shampoo brands across both developed and emerging markets. The United Nations Conference on Trade and Development (UNCTAD) reported that global e-commerce sales exceeded US$ 26 trillion in 2022, with beauty and personal care among the fastest-growing product categories across digital platforms. Subscription-based shampoo services, personalized hair care quiz-driven product recommendations, and AI-powered skin and scalp diagnostic tools embedded within branded e-commerce ecosystems are enabling brands to build proprietary consumer data assets while simultaneously reducing dependence on traditional retail intermediaries. Amazon, Nykaa (India), Tmall (China), and Lazada (Southeast Asia) represent high-penetration regional platforms through which both global and emerging brands can cost-effectively access fragmented, geographically dispersed frizz-conscious consumer segments that conventional brick-and-mortar distribution cannot efficiently serve.

Category-wise Analysis

Formulation Insights

The Protein / Keratin Based formulation segment leads the frizz control shampoo market, accounting for approximately 28% of total market share in 2025. This dominance reflects the scientifically established efficacy of keratin and hydrolyzed protein actives in reinforcing the hair cuticle structure, reducing porosity, and delivering sustained frizz suppression across diverse hair types, particularly chemically treated, color-processed, and heat-damaged hair. Dermatological and cosmetic science literature consistently validates keratin’s role in restoring the hair’s natural protein matrix, lending clinical credibility that resonates strongly with increasingly ingredient-literate consumers. Leading brands including Pantene (a Procter & Gamble brand), Dove (Unilever), and Kerastase (L’Oréal) have each invested in proprietary keratin-complex technologies to reinforce their competitive positioning within this high-performing formulation tier. The segment’s leadership is further supported by salon channel endorsement, where keratin-based frizz control treatments command a premium positioning and professional credibility.

Price Segment Insights

The Mid-Range price segment leads the frizz control shampoo market by revenue, accounting for approximately 43% of total market share in 2025. This leadership reflects the mid-range segment’s broad demographic accessibility, appealing simultaneously to aspirational mass-market consumers trading up from economy-tier products and to value-conscious premium consumers seeking effective formulations without the full cost premium of salon-exclusive or luxury brands. Mid-range frizz control shampoo brands, including Herbal Essences (Procter & Gamble), TRESemmé (Unilever), and Schwarzkopf (Henkel), have effectively occupied this positioning through high retail distribution density, ongoing product renovation, and competitive on-shelf pricing. The Consumer Price Index data from the U.S. Bureau of Labor Statistics confirms that personal care products in this price band demonstrate greater demand resilience during inflationary cycles compared to the premium tier, further underpinning the segment’s robust market leadership through the forecast period.

Packaging Type Insights

The Bottles packaging segment leads the frizz control shampoo market, capturing approximately 68% of total market share in 2025. The dominance of bottles, particularly High-Density Polyethylene (HDPE) and Polyethylene Terephthalate (PET) formats, reflects their functional superiority in terms of product preservation, consumer convenience, dispensing control, and compatibility with retail shelf planograms across global grocery, pharmacy, and specialty beauty channels. Standard flip-cap and pump-top bottle formats are well-established across all price tiers and distribution channels, enabling brands to leverage economies of scale in both filling operations and secondary packaging logistics. Growing sustainability pressures from regulatory bodies including the European Commission are accelerating investment in post-consumer recycled (PCR) bottle formats and concentrated refill-compatible bottle systems, ensuring the segment’s continued leadership while evolving its material and design architecture in alignment with circular economy objectives.

Distribution Channel Insights

Supermarkets & Hypermarkets lead the distribution channel category, accounting for approximately 35% of total market share in 2025. The channel’s leadership is rooted in its broad geographic footprint, high consumer traffic density, integrated promotional ecosystem, and the central role that physical retail replenishment continues to play in FMCG personal care purchasing behavior. Major global retailers including Walmart, Carrefour, Tesco, and Target, command vast, dedicated personal care aisle space that grants disproportionate visibility and purchase consideration to stocked frizz control shampoo brands. Planogram-driven shelf adjacency strategies, loyalty card data utilization, and in-store promotional mechanics, including end-cap displays and multi-buy offers, allow brand owners to effectively drive trial and repeat purchase at scale. Despite the accelerating growth of e-commerce, the immediacy and tactile product engagement offered by supermarket and hypermarket retail formats continues to anchor their market leadership position across the majority of global regions in 2025.

Regional Insights

North America Frizz Control Shampoo Market Trends and Insights

North America holds the leading position in the global frizz control shampoo market, accounting for approximately 33% of total market revenue share in 2025. The United States is the primary regional growth engine, supported by a highly sophisticated and innovation-driven hair care industry, strong consumer familiarity with functional shampoo formulations, and elevated per-capita personal care spending. The FDA’s MoCRA, enacted in December 2022, has introduced the most comprehensive federal cosmetics regulatory reform in over 80 years, compelling manufacturers to ensure ingredient safety substantiation and robust adverse event reporting, ultimately driving investment in clinically validated, transparent frizz control formulations that resonate with the region’s increasingly ingredient-literate consumer base.

The U.S. Natural Products Association (NPA) reports consistent year-on-year growth in natural and certified-organic personal care product sales across the country, reflecting a structural consumer migration toward botanical and clean-label frizz control solutions. Canada’s multicultural consumer base, characterized by high representation of textured, curly, and coily hair types particularly susceptible to humidity-induced frizz, is also generating incremental demand for specialized anti-frizz shampoo formulations across both the mass-market and premium tiers, with particular growth observed in specialty beauty retail and D2C e-commerce channels.

Europe Frizz Control Shampoo Market Trends and Insights

Europe represents the second-largest regional market for frizz control shampoos, driven by a highly regulated cosmetic ingredient environment, a mature consumer base with strong preferences for efficacious and ethically sourced formulations, and progressive brand commitments to sustainable packaging and clean beauty standards. France, Germany, the United Kingdom, and Spain collectively dominate regional market consumption. The EU Cosmetics Regulation (EC) No 1223/2009 establishes one of the world’s most rigorous ingredient safety frameworks, directly shaping formulation strategy for both regional and globally operating frizz control shampoo brands that seek European market access.

France’s prominent position as the global headquarters of leading beauty multinationals, including L’Oréal, which has publicly committed to achieving 100% sustainably sourced bio-based ingredients for its hair care portfolio by 2030, positions the country as a key formulation and innovation hub for the frizz control category. Germany’s well-developed natural and organic beauty retail sector, anchored by chains such as dm-drogerie markt and Rossmann, is driving meaningful growth in herbal and botanical frizz control formulations, while the UK’s vibrant indie beauty ecosystem continues to introduce disruptive, direct-to-consumer frizz control brand propositions that are reshaping consumer expectations across the broader European market.

Asia Pacific Frizz Control Shampoo Market Trends and Insights

Asia Pacific is the fastest-growing regional market for frizz control shampoos, projected to expand at a CAGR of approximately 9.3% between 2026 and 2033. The region’s accelerated growth trajectory is underpinned by the high prevalence of humidity-prone climate conditions across Southeast Asia, South Asia, and coastal East Asia, geographies where frizz management represents an acute and near-universal hair care concern for a demographically vast and increasingly affluent consumer population. China’s National Bureau of Statistics has consistently documented robust year-on-year growth in cosmetics and personal care retail sales, with premium haircare registering above-average expansion rates regulated under the National Medical Products Administration (NMPA).

India represents a particularly high-potential growth market, where rising middle-class disposable incomes, accelerating smartphone penetration driving beauty e-commerce adoption, and the government’s Production Linked Incentive (PLI) scheme for cosmetics and toiletries manufacturing are collectively stimulating both domestic consumption and local production capacity. Japan remains a center of formulation innovation, with brands such as Kao Corporation and Shiseido Co., Ltd. consistently investing in advanced hair-care biotechnology platforms. Across ASEAN markets including Indonesia, Vietnam, and the Philippines, rapid modern trade retail infrastructure development is significantly expanding frizz control shampoo accessibility, driving strong volume growth across both mass-market and mid-range price segments.

Competitive Landscape

The global frizz control shampoo market demonstrates a moderately consolidated structure, where large multinational personal care manufacturers command a significant share through diversified brand portfolios, global distribution networks, and strong retail shelf presence. Competition is primarily driven by formulation innovation, particularly the use of keratin complexes, botanical extracts, sulfate-free systems, and climate-responsive technologies designed to address humidity-induced frizz.

Strategic focus areas include premiumization, clean-label positioning, and sustainable packaging to capture environmentally conscious consumers. Companies are increasingly investing in digital marketing, influencer collaborations, and data-driven consumer insights to strengthen brand loyalty and accelerate product differentiation. At the same time, agile independent brands are intensifying competition by leveraging direct-to-consumer channels, rapid product innovation cycles, and transparent ingredient storytelling. E-commerce expansion and subscription-based haircare models further reshape competitive dynamics, compelling established players to enhance personalization capabilities and omnichannel strategies. Overall, market participants compete on technology, branding, sustainability credentials, and distribution efficiency to secure long-term share gains.

Key Developments

- September, 2025: Wella Professionals launches its Ultimate Smooth Range in India, offering advanced frizz-control haircare featuring patented technology with Squalane and Omega-9 for smoother, shinier, and frizz-free hair.

- February, 2026: ZXX enters India’s beauty market with a simplified, salon-grade haircare system designed for everyday use, expanding its global footprint and addressing growing consumer demand for accessible premium hair solutions.

- February, 2026: Not Your Mother’s launches a new scent-driven hair care collection, combining engaging fragrances with targeted formulas to enhance daily hair care routines and appeal to lifestyle-focused.

Companies Covered in Frizz Control Shampoo Market

- L’Oréal S.A.

- Procter & Gamble

- Unilever

- Henkel AG & Co. KGaA

- Kao Corporation

- Johnson & Johnson

- Estée Lauder Companies

- Coty, Inc.

- Beiersdorf AG

- Shiseido Co., Ltd.

- Revlon, Inc.

- Amika (Dynamic Blending Specialists LLC)

- OGX (Vogue International LLC)

- Moroccanoil Israel Ltd.

- Cantu Beauty (PDC Brands)

- Briogeo Hair Care

- Aveda Corporation

- Wella Professionals

- ZXX

Frequently Asked Questions

The frizz control shampoo market is projected to reach US$ 3.0 billion in 2026.

Demand is driven by clean-label preferences and rising humidity-related frizz concerns.

North America leads the market with around 33% revenue share.

Opportunities include vegan botanical formulations and expanding e-commerce and D2C channels.

Key players include L’Oréal, Procter & Gamble, Unilever, Henkel, Kao, and Shiseido.