- Advanced Materials

- Flexible Glass Market

Flexible Glass Market Trends, Size, Share, Growth, and Forecasts for 2025 - 2032

Flexible Glass Market by Product Type (Thin Flexible Glass, Ultra-thin Flexible Glass), By Thickness (<0.1 mm, 0.1–0.3 mm, >0.3 mm), By Application (Displays, Wearable Devices, Solar Panels, Automotive Displays, Electronic Paper, Photovoltaic Cells), By Industry, and Regional Analysis for 2025 - 2032

Flexible Glass Market Share and Trends Analysis

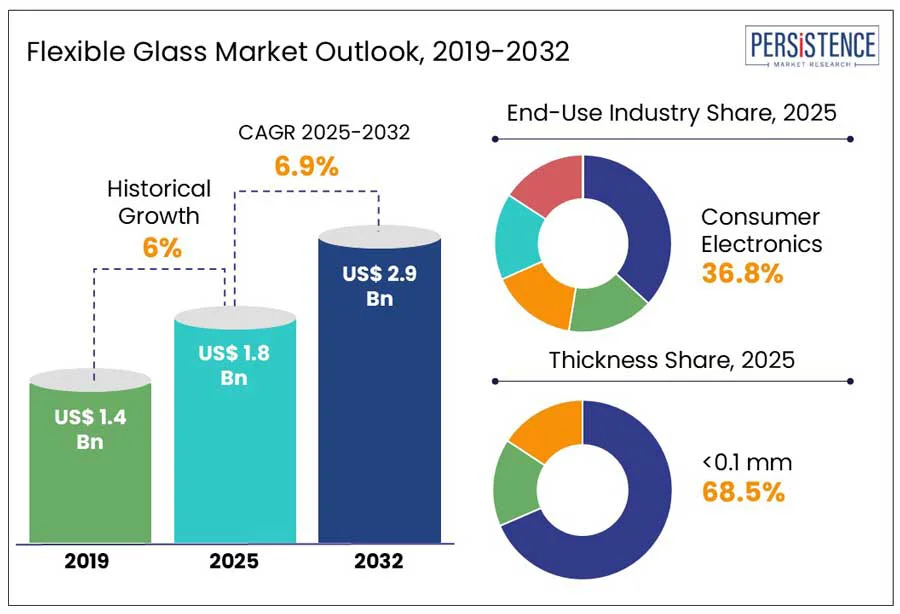

The global flexible glass market size is expected to increase from US$ 1.8 billion in 2025 to US$ 2.9 billion, with a CAGR of 6.9% by 2032. According to the Persistence Market Research report, the industry is experiencing significant growth, fueled by increasing demand in the consumer electronics, energy, and automotive industries. Flexible glass is known for its ultra-thin, lightweight, and bendable properties, making it an ideal material for foldable displays, wearable devices, and next-generation photovoltaic panels. Its unique combination of durability, optical clarity, and flexibility positions it as a preferred alternative to traditional rigid glass and plastic substrates.

Technological advancements in ultra-thin glass manufacturing and improved lamination techniques have further enhanced its commercial viability. The rise of foldable smartphones, rollable tablets, and curved displays is accelerating the adoption of flexible glass among electronics manufacturers. Additionally, the material’s compatibility with high-temperature processing and its barrier properties are expanding its applications in the solar energy and automotive sectors. As trends in sustainability, miniaturization, and innovation continue to shape global industries, flexible glass is set to become a crucial enabler of future-ready designs and technologies.

Key Industry Highlights:

- Flexible glass is increasingly being adopted in foldable smartphones, tablets, and wearable devices due to its durability and optical clarity.

- Its integration into flexible solar panels is also gaining momentum as global demand for clean energy rises.

- Innovations in manufacturing techniques have enabled the production of glass sheets thinner than 0.1 mm, which enhances flexibility and allows for better integration into various designs.

- Strategic partnerships, such as those between Corning and Samsung Display, are accelerating the commercial deployment and optimization of these products.

- Flexible glass is being used in curved and adaptive automotive infotainment systems and dashboards, contributing to the modern aesthetic of vehicle interiors.

- The demand for sleeker and thinner consumer devices is driving the adoption of ultra-thin flexible glass over traditional plastics.

- Companies are also developing chemically strengthened and coated flexible glass to enhance scratch resistance and mechanical reliability.

- Flexible glass is entering the field of biomedical wearables and sensors, playing a vital role in the digital healthcare revolution.

|

Global Market Attribute |

Details |

|

Flexible Glass Market Size (2025E) |

US$ 1.8 Bn |

|

Market Value Forecast (2032F) |

US$ 2.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.0% |

Market Dynamics

Driver - Growing adoption of foldable and rollable electronic devices is fueling global flexible glass demand

The flexible glass market has been significantly driven by the growing demand for foldable and rollable electronic devices. Flexible glass is increasingly being adopted due to its ability to bend without breaking while maintaining the durability and optical clarity of traditional glass. Its use is being prioritized in next-generation smartphones, tablets, and wearable devices, where lighter, thinner, and more resilient materials are essential. As advancements in display technology progress, the need for substrates capable of enduring repeated bending without performance degradation is being emphasized. Consequently, flexible glass is being positioned as a critical material in the development of future electronic devices.

In 2025, Samsung announced that its upcoming Galaxy S25 Edge smartphone would feature Corning® Gorilla® Glass Ceramic 2, a newly developed glass ceramic designed for superior protection in ultra-thin formats. The collaboration between Samsung and Corning underscores the accelerating integration of flexible glass into modern, sleek, and durable electronic products.

Restraint - Technical challenges in achieving consistent flexibility without compromising durability hinder market scalability

The growth of the flexible glass market is being hindered by unresolved technical challenges related to balancing flexibility with long-term durability. While ultra-thin glass materials are being developed to bend and curve, maintaining structural integrity under repeated mechanical stress has not been consistently achieved. Cracking, delamination, and performance degradation are being observed when flexible glass is subjected to extreme bending or environmental fluctuations.

As a result, hesitation is being shown by manufacturers when integrating such materials into high-performance applications. Additionally, uniform quality across large-scale production is proving difficult, leading to reliability concerns. Until these technical limitations are effectively addressed through improved fabrication methods and material innovations, widespread adoption of flexible glass across various industries is expected to remain constrained.

Opportunity - Integration of flexible glass in next-generation solar panels presents a major growth avenue

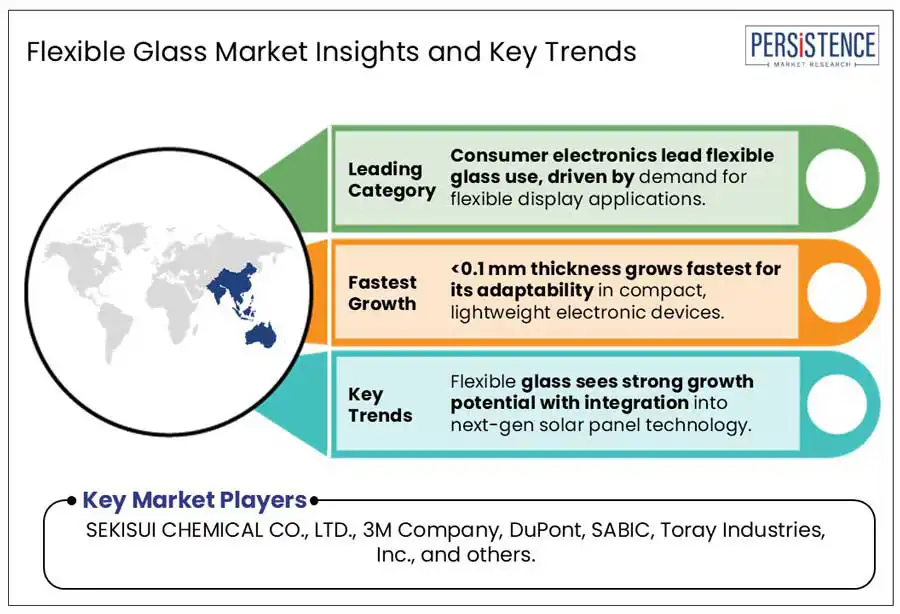

The flexible glass market stands to benefit significantly from the potential integration into next-generation solar panels, presenting a promising opportunity for growth and innovation in this sector. Flexible glass is being explored as a lightweight, durable, and bendable alternative to traditional rigid covers, allowing the development of ultra-thin and portable solar modules. Its high optical clarity and excellent barrier properties are being leveraged to enhance solar panel efficiency and longevity. Additionally, its suitability for applications requiring flexibility and aesthetics, such as building-integrated photovoltaics (BIPV) and solar wearables, is being increasingly recognized. As renewable energy technologies experience growing demand, flexible glass is being positioned as a key material enabling innovation in the solar energy sector.

In 2025, Corning announced a US$1.5 billion investment to expand its solar wafer manufacturing operations in Saginaw County, Michigan. The initiative aims to support the rising need for domestically produced solar components and builds upon Corning's expertise in hyper-pure polysilicon production through Hemlock Semiconductor.

Category Wise Insights

Industry Insights

Consumer electronics have been identified as the leading in the flexible glass market, driven by its widespread application in flexible displays. Devices such as foldable smartphones, tablets, wearable gadgets, and curved televisions are increasingly being designed with flexible glass to enhance durability, portability, and design flexibility. This material is being preferred over traditional glass and plastics due to its superior scratch resistance, high transparency, and ability to bend without breaking. As product designs evolve toward slimmer and more resilient formats, flexible glass is being relied upon to ensure consistent performance in advanced electronic applications.

At DesignCon 2025, DuPont showcased its advanced materials, including Pyralux® flex circuit laminates and Kapton® polyimide films. These materials were engineered to enhance signal integrity and thermal performance in high-speed consumer electronics. DuPont’s innovations reflected the critical role of flexible materials in meeting the growing demands of next-generation consumer electronic devices.

Thickness Insights

The <0.1 mm thickness segment has been identified as the fastest-growing product category due to its exceptional adaptability in compact and lightweight devices. Ultra-thin glass is being increasingly favored for foldable smartphones, wearable technology, and other portable electronics, where flexibility and space efficiency are essential. Its ability to retain strength and optical clarity while withstanding significant bending is being leveraged to meet evolving product design requirements. Manufacturing advancements are enabling the consistent production of high-quality ultra-thin glass, accelerating its adoption across various industries.

In 2025, this trend was exemplified by Toray Industries’ development of the PICASUS™ nano-laminated film, composed of approximately 1,000 ultra-thin layers within a total thickness of just 0.1 mm. Offering high transparency and electromagnetic wave permeability, the film is designed for compact devices such as smartphones, wearables, and automotive electronics. This innovation underscored the growing demand for ultra-thin, flexible materials in the expanding consumer electronics sector.

Regional Insights and Trends

North America Flexible Glass Market Trends

Increasing investment in wearable technology innovation has accelerated the integration of flexible glass into advanced devices across North America. At CES 2025, Vuzix Corporation’s unveiling of its AI-powered smart glasses Ultralite Pro and Ultralite Audio OEM platforms developed in collaboration with Quanta Computer, highlighted this trend. These next-generation smart glasses have been designed with advanced waveguide technology, which depends on transparent glass to project visual content directly to the eyes, enabling cutting-edge applications such as augmented reality and real-time translation.

Flexible glass has been incorporated into these devices to enhance durability and support sleek, lightweight designs. Its ability to bend without compromising optical clarity or structural integrity has made it an ideal choice for wearables that require both functionality and aesthetic appeal. As consumer expectations shift toward unobtrusive, high-performance wearable devices, flexible glass is being increasingly adopted as a key enabling material in North America’s rapidly evolving wearable technology landscape.

Europe Flexible Glass Market Trends

In Europe, the growing focus on sustainable energy has been driving the adoption of flexible glass in photovoltaic (PV) applications. A notable example is AGC Glass Europe’s implementation of one of the largest rooftop PV self-consumption plants in Spain, located at its Port of Sagunto facility. This 4.6 MW installation, spanning 48,400 m², has been designed to produce 7 GWh of energy annually, significantly cutting CO? emissions.

The project aligns with AGC’s broader objective of achieving carbon neutrality by 2050 and exemplifies the strategic use of flexible glass in large-scale PV systems. The integration of flexible glass in such renewable energy projects underscores its contribution to enhancing energy efficiency, durability, and adaptability in solar infrastructure. As Europe intensifies its efforts toward decarbonization, the use of advanced materials such as flexible glass is being positioned as a key enabler of innovation and performance improvements in next-generation solar energy solutions.

Asia Pacific Flexible Glass Market Trends

The rapid expansion of advanced display manufacturing hubs in China and South Korea has been recognized as a major factor driving the demand for flexible glass in the Asia Pacific region. In South Korea, Corning established a fully integrated supply chain for ultra-thin bendable glass at its Asan facility, with an investment of $1.5 billion over five years. Mass production of foldable substrates began at this facility, supplying components for devices such as Samsung’s Galaxy Z Flip 5.

Corning’s CEO highlighted South Korea’s emergence as a global hub for bendable glass manufacturing. Simultaneously, China has solidified its dominance in the display glass market, accounting for over 70% of global market share in 2023. This position has been reinforced by major investments, including BOE’s $9 billion OLED plant in Chengdu and Tunghsu Group’s $2.2 billion ultra-thin flexible glass project in Quzhou.

Competitive Landscape

The competitive landscape of the global flexible glass market is shaped by the presence of several prominent players focusing on innovation, strategic collaborations, and geographic expansion. Companies such as Corning Incorporated, Asahi Glass Co., Ltd., and Schott AG are heavily investing in R&D to enhance product performance for applications in foldable smartphones, tablets, wearables, and solar panels. Partnerships between flexible glass producers and electronics manufacturers, such as Corning’s collaboration with Samsung Display, have accelerated commercial adoption. Asian manufacturers including LG Chem, Toray Industries, and Mitsubishi Chemical Corporation are leveraging regional manufacturing advantages and proximity to major OEMs in China and South Korea.

Firms such as 3M Company and DuPont are offering specialized coatings and materials to complement flexible glass solutions. Growing demand across the consumer electronics and energy sectors is intensifying competition, prompting firms to expand production capacity and customize product portfolios to meet evolving end-user requirements globally. Innovation and integration remain key differentiators.

Key Industry Developments

- In April 2024, LG Chem has announced its entry into the automotive smart glass sector with the development of Switchable Glazing Film (SGF). This film, which alters its transparency based on electrical signals, will be supplied to Webasto for integration into sunroof systems for European OEMs.

- In September 2024, Corning has introduced EXTREME ULE® Glass, which is designed to meet the stringent requirements of next-generation semiconductor manufacturing. This ultra-low expansion glass provides exceptional thermal stability and uniformity, which are critical for extreme ultraviolet (EUV) lithography processes in advanced chip production.

Companies Covered in Flexible Glass Market

- Asahi Glass Co., Ltd.

- Dow Chemical Company

- LG Chem

- SCHOTT

- Corning Incorporated

- Corning Incorporated

- Mitsubishi Chemical Corporation

- SEKISUI CHEMICAL CO.,LTD.

- 3M Company

- DuPont

- SABIC

- Toray Industries, Inc.

- Central Glass Co., Ltd. Polytronix, Inc.

- Oike & Co., Ltd.

- Saint-Gobain India Pvt. Ltd.

Frequently Asked Questions

The global industry is projected to be valued at 1.8 Bn in 2025.

The industry is driven by the growing adoption of foldable and rollable electronic devices is fueling global flexible glass demand.

The global industry growth is poised at a CAGR of 6.9% from 2025 to 2032.

Integration of flexible glass in next-generation solar panels presents a major growth avenue is the key market opportunity.

Major players are SEKISUI CHEMICAL CO., LTD., 3M Company, DuPont, SABIC, Toray Industries, Inc., and others.