- Electric Mobility

- E-Bike Market

E-Bike Market Size, Share, and Growth Forecast 2025 - 2032

E-bike Market by Propulsion Type (Pedal-assisted E-bikes, Throttle-assisted E-bikes), by Motor Type (Hub Motors, Mid-Drive Motors, Others), by E-bike Type (City/Urban E-bikes, Mountain E-bikes, Trekking/Touring E-bikes, Cargo E-bikes, Cruiser), by Distribution Channel (Online Retailers, Direct-to-Consumer Brands, Department Stores, Independent Bike Shops), by Regional Analysis, 2025 - 2032

E-Bike Market Size and Trend Analysis

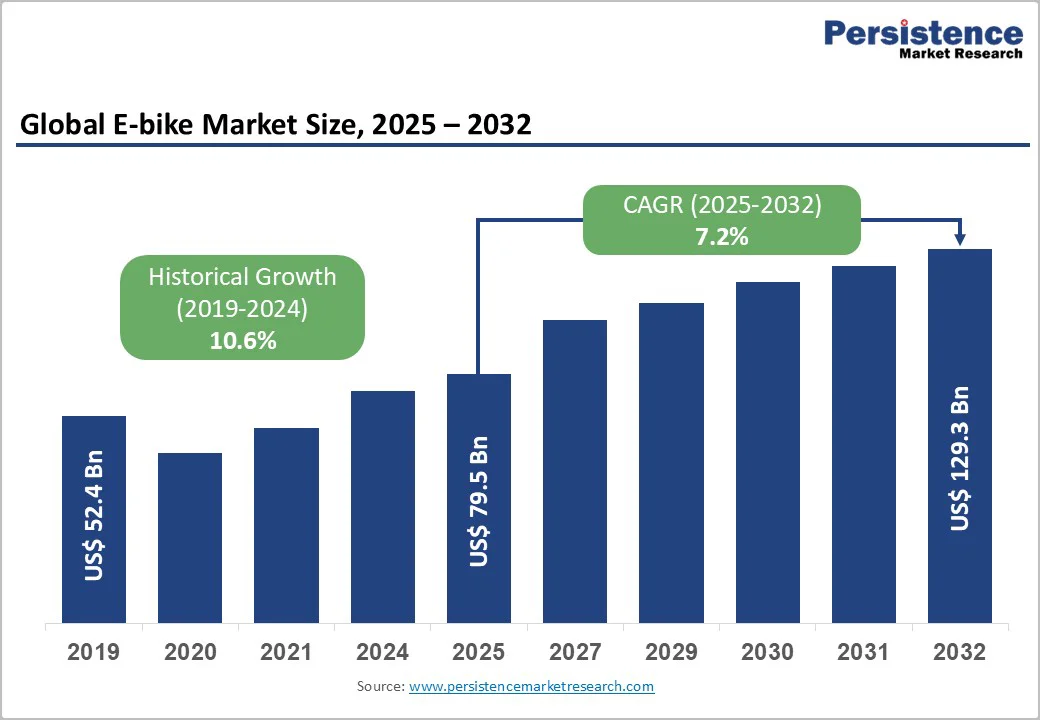

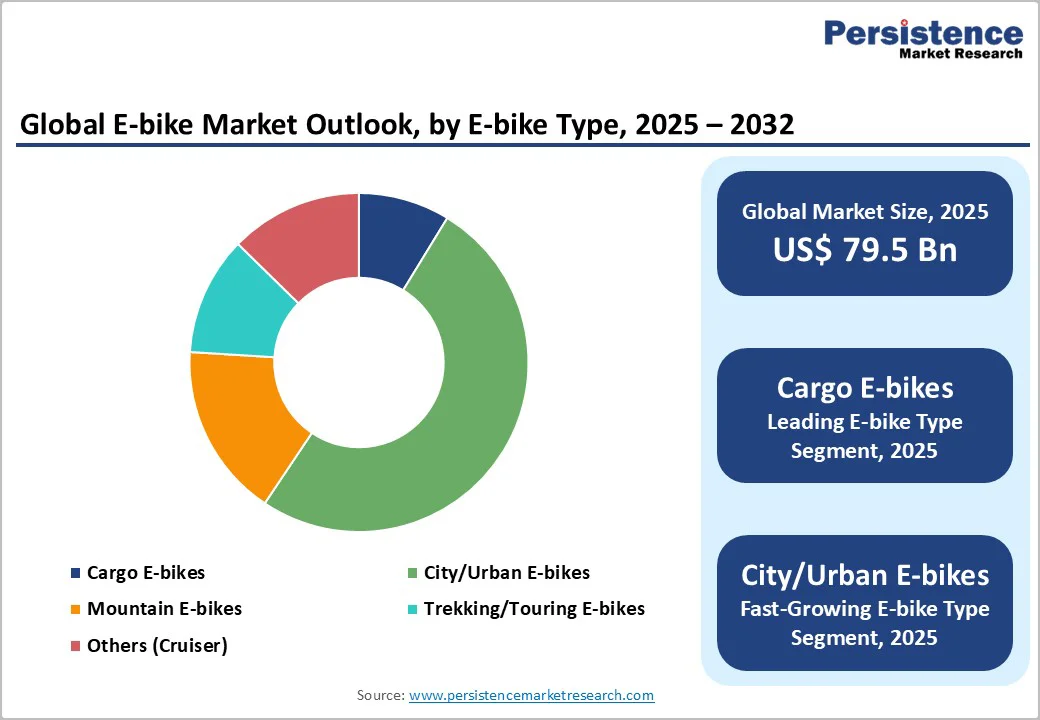

The global E-bike market size was valued at US$ 79.5 billion in 2025 and is projected to reach US$ 129.3 billion by 2032, growing at a CAGR of 7.2% between 2025 and 2032. The market expansion is primarily driven by accelerating urbanization, stringent government policies promoting zero-emission transportation, and remarkable advancements in lithium-ion battery technology.

Consumer preference for sustainable mobility solutions is intensifying as cities implement low-emission zones and cycling infrastructure improvements. Additionally, rising fuel costs and environmental awareness are compelling commuters to shift toward eco-friendly alternatives, while innovations in motor efficiency and battery density are making e-bikes more accessible and attractive across diverse demographic segments.

Key Market Highlights

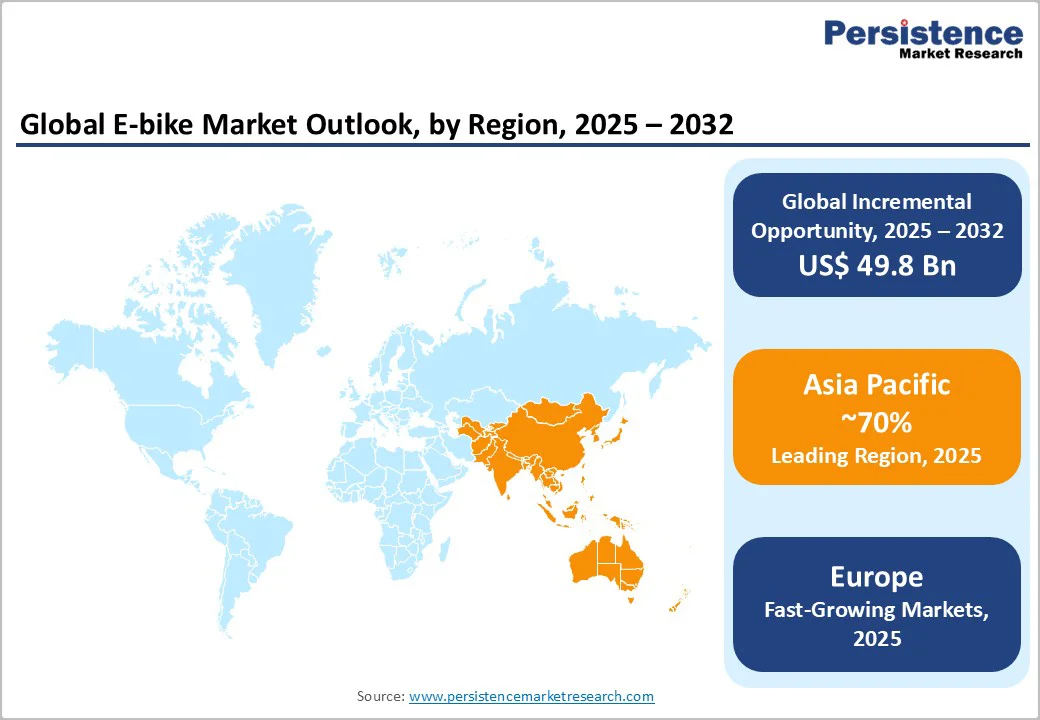

- Leading Region: Asia Pacific dominates the global e-bike market with approximately 72.9% share, driven by China’s 84% regional market dominance and production exceeding 30 million units annually.

- Fastest-Growing Region: North America demonstrates the accelerated regional growth with a projected 11.6% CAGR through 2032, supported by expanding cycling infrastructure, government incentives, and strong adoption of Class 3 e-bikes.

- Leading Category: Pedal-assisted e-bikes lead globally with approximately 79% market share, driven by energy efficiency, extended battery range, regulatory advantages, and consumer preference for health benefits.

- Fastest-Growing Segment: Cargo e-bikes represent the fastest-expanding category with 9.6% projected CAGR through 2034, fueled by e-commerce growth, municipal emission mandates, and logistics fleet deployment by Amazon, UPS, and DHL.

- Key Market Opportunity: E-bike subscription and smart connectivity solutions integrating advanced battery management, GPS tracking, anti-theft systems, and smartphone enabled e-bikes are expected to provide key growth opportunities.

| Key Insights | Details |

|---|---|

|

E-bike Market Size (2025E) |

US$ 79.5 Billion |

|

Market Value Forecast (2032F) |

US$ 129.3 Billion |

|

Projected Growth CAGR(2025-2032) |

7.2% |

|

Historical Market Growth (2019-2024) |

10.6% |

Market Dynamics

Drivers - Urbanization and Traffic Congestion are Driving E-Bike Adoption

Rapid urbanization in both developed and emerging economies is fueling unprecedented traffic congestion in major cities, creating a pressing need for efficient short-distance transportation solutions. E-bikes have emerged as a highly practical alternative, offering faster commuting times, lower operational costs, and reduced environmental impact compared to personal automobiles or public transit. Cities such as Amsterdam, Copenhagen, and Shanghai have invested heavily in cycling infrastructure, including protected lanes and dedicated facilities, fostering widespread adoption. According to the International Transport Forum, e-bikes could reduce urban traffic congestion by up to 10% if they capture just 15% of short-distance trips. This potential creates strong incentives for governments worldwide to continue supporting infrastructure development and policies that encourage e-bike adoption.

Battery Technology Advancements and Cost Reduction is Enabling Wider Adoption

Advancements in lithium-ion battery technology have significantly enhanced the affordability and practicality of e-bikes. Since 2020, energy density has increased by 15–20% annually, while costs per kilowatt-hour (kWh) have declined from approximately US$ 150/kWh in 2015 to around US$ 80–90/kWh in 2025. These improvements make e-bikes more accessible to consumers and reduce total cost-of-ownership compared to traditional bicycles. Modern battery management systems (BMS) also provide enhanced safety features, faster charging capabilities, and longer lifespans exceeding 1,000 charge cycles.

Premium manufacturers are increasingly integrating Lithium Iron Phosphate (LFP) chemistry, which offers superior thermal stability and durability. These advancements directly address consumer concerns over range anxiety and battery longevity. As a result, e-bikes are becoming economically competitive and more attractive for daily commuting, recreational use, and longer-distance travel, supporting sustained market growth globally.

Restraints - High Initial Purchase Cost and Infrastructure Limitations

Although battery prices have fallen steadily, the average cost of premium e-bikes remains between US$ 2,000 and US$ 4,000, limiting affordability in price-sensitive markets. While e-bikes offer long-term savings, the high upfront expense discourages adoption, especially in developing economies where purchasing power is lower. Limited financing options and the higher price gap compared to traditional bicycles further deter first-time buyers.

Infrastructure limitations also impede growth, as inadequate cycling lanes and restricted charging networks create range concerns, particularly in rural and semi-urban areas. Many Asia-Pacific and Latin American countries lack standardized charging protocols, which affects consumer confidence and interoperability. Additional costs related to battery replacement and specialized servicing raise the total cost of ownership, making e-bikes less accessible to lower-income consumers who could benefit most from affordable mobility.

Regulatory Fragmentation and Supply Chain Volatility

E-bike regulations differ widely across global markets, creating complexity for manufacturers and importers. The European Union restricts pedal-assist e-bikes to 250 W motors and 25 km/h assistance, while U.S. Class 3 models allow up to 750 W and speeds of 28 mph. These differing rules raise design and certification costs for global manufacturers. Additionally, California’s SB 1271 will require UL 2849 safety certification for e-bikes sold in the state from January 2026, further increasing compliance expenses.

Simultaneously, supply chain volatility continues to challenge production stability. Price fluctuations in lithium, cobalt, and nickel, coupled with geopolitical tensions and trade restrictions, have increased manufacturing costs. Logistics disruptions and tariff uncertainties compound these issues, leading to inconsistent supply and delayed product availability. Manufacturers often transfer these costs to consumers, constraining demand growth in cost-sensitive and emerging regional markets.

Opportunities - Cargo and Utility E-Bikes for Last-Mile Delivery

The explosive growth of e-commerce and same-day delivery services has created unprecedented demand for sustainable last-mile logistics solutions. Electric cargo bikes can carry payloads of 50 to 250 kilograms, making them ideal for urban parcel delivery and food distribution. Major logistics providers including Amazon, DHL, and UPS have deployed pilot fleets of e-cargo bikes, with Amazon reportedly operating over 10,000 electric cargo bikes across European cities. The global electric cargo bike market size is likely to be valued at US$ 3.2 Billion in 2025 and is estimated to reach US$ 5.4 Billion in 2032, growing at a CAGR of 7.8% during the forecast period 2025 - 2032.

This growth is driven by the surging emphasis on reducing carbon emissions and promoting sustainable transportation. Cities implementing congestion pricing and emission bans, such as London and Paris, are actively incentivizing e-cargo bike adoption, creating significant market opportunities for manufacturers and establishing a compelling segment within the broader e-bike motor market ecosystem.

Subscription-Based Models and Micro-Mobility Integration

Emerging subscription and bike-as-a-service models are fundamentally reshaping e-bike ownership patterns, particularly in urban markets. The e-bike subscription platform market was valued at US$ 2.5 billion in 2024 and is anticipated to reach US$ 9 billion by 2032, representing a 17.4% CAGR. Companies such as Cowboy, Dance, and Zoomo offer all-inclusive subscription packages encompassing bike maintenance, theft insurance, and battery management, reducing consumer barriers to adoption.

These platforms integrate seamlessly with micro-mobility ecosystems, connecting e-bikes with public transportation systems and enabling multi-modal journey planning. Employers are increasingly subsidizing e-bike subscriptions as employee wellness benefits, while municipalities are partnering with operators to provide affordable mobility access in underserved communities. This business model innovation addresses affordability concerns while generating predictable revenue streams, positioning subscription services as a critical growth driver for the e-bike market through 2032.

Category-wise Analysis

Propulsion Type Insights

Pedal-assisted e-bikes command approximately 79% of global e-bike sales due to superior battery efficiency and favorable regulatory classification. These systems require continuous rider engagement while providing proportional motor assistance, extending range compared to throttle-only alternatives. In the European Union, pedal-assist bikes are classified as traditional bicycles, allowing use on protected lanes and exempting riders from licensing.

Investment in torque sensors and cadence-based algorithms continues, reinforcing pedal-assisted systems as the market standard. This dominant propulsion type drives innovation across urban, trekking, and cargo e-bike segments, supporting sustained adoption and shaping the broader global e-bike market landscape.

Motor Type Insights

Hub motors command approximately 68% of the e-bike market because they offer cost-effective performance, mechanical simplicity, and broad compatibility with diverse bicycle designs. Manufacturers integrate these motors directly into the wheel hub, requiring minimal frame adjustments and enabling effortless installation, including in aftermarket retrofit applications.

In contrast, mid-drive motors, growing at an estimated 8.5% CAGR, attract performance-focused riders with higher torque outputs of 70–95 Nm, compared with 40–60 Nm for hub systems. By positioning the motor at the crankset, mid-drive designs improve weight distribution, climbing efficiency, and overall handling. Premium suppliers such as Bosch, Shimano, and Yamaha price these systems 30–50% higher, reinforcing their adoption in mountain biking, trekking, and other demanding segments, and solidifying mid-drive technology as a key area of market growth.

E-Bike Type Insights

City/urban e-bikes account for approximately 58% of the market, favored for commuting in congested areas. They offer upright positions, lighting systems, cargo racks, and weigh 25–30 kg, ensuring accessibility for diverse riders. Bike-sharing systems in San Francisco, Berlin, and Singapore have accelerated awareness and trials.

Mountain e-bikes (e-MTBs) and cargo e-bikes are growing fastest. E-MTBs expand at 8.1% CAGR due to recreational and tourism demand. Cargo models, priced US$ 3,500–6,000, address logistics needs with reinforced frames and high load capacity. This segment drives expansion beyond recreational users, becoming crucial for urban delivery and commercial applications globally.

Distribution Channel Insights

Offline channels, including independent bike shops and specialty retailers, remain the leading distribution method, maintaining roughly 73% market share globally. These channels leverage experiential advantages such as test rides, personalized guidance, and expert after-sales support, which are critical for building consumer confidence in complex e-bike systems. Their hands-on approach is particularly valued in mature markets such as Europe and North America, where established retail networks and cycling cultures reinforce trust and brand loyalty.

While offline channels dominate, online and direct-to-consumer (DTC) platforms are rapidly expanding, benefiting from the rise of digitally native consumers and e-commerce infrastructure. Click-and-collect models and integrated service offerings further enhance convenience. Despite rapid online growth, offline retail remains the primary sales channel globally.

Regional Insights

North America E-bike Market Trends

North America is witnessing strong e-bike adoption, with a projected CAGR of 11.6% from 2025 to 2032, significantly above the global average. The United States leads this growth, supported by federal tax credits, state rebates, and municipal incentives. Cities such as Denver, Portland, and San Francisco have expanded protected bike lanes over 1,000 kilometers, reinforcing infrastructure for safe cycling. The pandemic accelerated adoption, with approximately 1.2 million units expected to be sold in 2025.

Class 3 e-bikes, capable of 28 mph assistance, are rapidly gaining traction, particularly for urban commuting and cargo applications. Companies like Amazon and Cargo Bike Co-op are expanding electric cargo operations. Regulatory inconsistencies across states and rising tariffs on imported components create challenges, while California’s UL 2849 battery certification effective January 2026 establishes safety standards, balancing compliance costs with enhanced market confidence.

Europe E-bike Market Trends

Europe holds approximately 20% of the global e-bike market, making it the most mature region with deep cycling traditions and supportive regulations. Sales reached roughly 4.5 million units in 2024, fueled by subsidies in Germany, Netherlands, and France. Germany, the European leader, offers purchase incentives of US$ 1,500–2,500 per model, driving annual sales of about 2.1 million e-bikes.

Regulatory harmonization around EN 15194 (250W motors, 25 km/h assistance) provides clarity for manufacturers. Speed pedelecs and high-performance models are gaining traction, while smart connectivity features like GPS tracking and smartphone integration differentiate premium brands. Despite strong demand, battery supply chain challenges and rising raw material costs pressure margins. The Netherlands leads in e-bike penetration, with e-bikes representing roughly 15% of all bicycle sales, supported by extensive cycling infrastructure investments.

Asia Pacific E-bike Trends

Asia Pacific dominates the global e-bike market with approximately 70% share, driven by China’s manufacturing and consumption. China accounts for 84% of the regional market, producing roughly 45 million units annually, meeting both domestic demand and export needs. The region benefits from established battery supply chains, large urban population, and manufacturing expertise, reinforcing its global leadership in e-bike production.

India is the fastest-growing market, with rapid urbanization in cities like Bangalore, Delhi, and Mumbai boosting demand for affordable mobility. Government incentives, such as the PM E-Drive scheme with US$ 481 million in subsidies, support adoption among price-conscious consumers. Southeast Asian markets including Vietnam, Thailand, and Indonesia are implementing supportive policies. Expanding bike-sharing platforms and subscription services further accelerate micro-mobility adoption, positioning Asia Pacific as the primary engine of global e-bike growth through 2032.

Competitive Landscape

The global e-bike market is moderately fragmented, with established players and emerging direct-to-consumer (DTC) brands competing for market share. Traditional manufacturers like Giant Manufacturing (Taiwan), Accell Group (Netherlands), Trek Bicycle (USA), and Specialized maintain leadership through strong distribution networks and brand recognition. DTC brands such as Rad Power Bikes, Aventon, and Blix are disrupting the market with innovative business models, competitive pricing, and direct consumer engagement, reshaping the competitive dynamics.

Component suppliers including Bosch, Shimano, Yamaha, and Panasonic exert influence over product innovation through proprietary technology and supply chain control. Regional Chinese manufacturers, including Yadea, Aima Technology, and Jiangsu Xinri, are expanding globally by leveraging cost advantages. Market consolidation continues, with strategic acquisitions by Accell and Giant expanding OEM and brand portfolios.

Key Market Developments:

- In March 2024, Trek Bicycle announces lightweight aero road e-bikes. Trek Bicycle Corporation introduced its advanced road e-bike lineup featuring integrated battery systems, lightweight carbon frames, and app-based connectivity features, targeting performance-oriented cyclists and addressing the underserved premium segment.

- In October 2024, ZADD Bikes launches 'Utility Hauler' electric cargo bicycle in India. ZADD Bikes unveiled the Utility Hauler specifically designed for last-mile delivery applications in India, featuring 25 to 30 kilogram rear load capacity and extended range supporting 160 kilometers with dual battery configuration, addressing rapid e-commerce expansion in emerging markets.

- In March 2025, Tern launches third-generation GSD electric cargo bike with enhanced specifications. Tern released its advanced GSD cargo e-bike incorporating reinforced frames, increased load capacity reaching 210 kilograms, Bosch Smart System integration with GPS tracking and ABS braking, and modular accessories, establishing new standards for premium cargo e-bike functionality and safety.

Companies Covered in E-Bike Market

- Giant

- Trek

- Specialized

- Rad Power Bikes

- Yamaha

- Accell Group

- Haibike

- Merida

- Riese & Müller

- Moustache Bikes

- A2B

- Pedego

- Bosch eBike Systems

- Shimano STEPS

- Gazelle

- Orbea

- Aventon

- Velotric

- MOD Bikes

- Hero Lectro

Frequently Asked Questions

The global e-bike market is valued at US$ 79.5 billion in 2025 and projected to reach US$ 129.3 billion by 2032, growing at a 7.2% CAGR.

E-bike demand is driven by urban congestion, battery technology advances, rising fuel costs, government incentives, and growing health consciousness.

Pedal-assisted e-bikes dominate with 79% market share due to superior efficiency, longer range, and favorable regulatory classification.

North America is the fastest-growing region with an 11.6% CAGR between 2025-2032, while Asia Pacific holds the largest 70% share globally.

Cargo and utility e-bikes offer the strongest opportunity, expanding at a 9.6% CAGR through 2034, alongside subscription-based ownership models.