- Specialty & Fine Chemicals

- Dioctyl Phthalate (DOP) Market

Dioctyl Phthalate (DOP) Market Size, Share, and Growth Forecast, 2026 - 2033

Dioctyl Phthalate (DOP) Market by Product Type (General Grade, Electrical Grade, Food Grade, Medical Grade), Application (Flooring & Wall, Wire & Cable, Film & Sheet, Consumer Goods), End-user (Construction, Automotive, Healthcare), and Regional Analysis for 2026-2033

Dioctyl Phthalate (DOP) Market Share and Trends Analysis

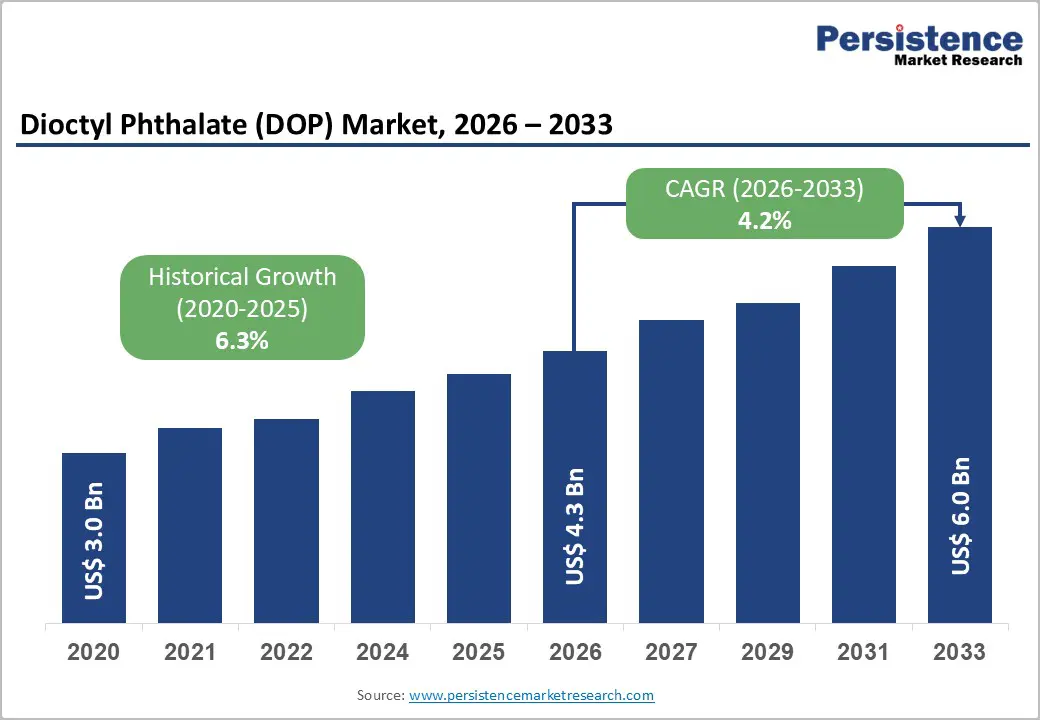

The global dioctyl phthalate (DOP) market size is likely to be valued at US$ 4.3 billion in 2026, and is projected to reach US$ 6.0 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026−2033.

Flexible polyvinyl chloride (PVC) continues to serve critical roles in construction materials, wire and cable insulation, and automotive interior components. Urbanization and infrastructure modernization programs are increasing the need for durable flooring, protective coatings, and lightweight vehicle parts that enhance energy efficiency. Emerging economies are accelerating industrial recovery and capital expenditure, which is reinforcing baseline demand for plasticizers that improve flexibility, processability, and product longevity. Regulatory scrutiny surrounding phthalate usage is shaping product strategy and formulation development.

Environmental and safety standards in sectors such as toys and medical devices are prompting manufacturers to reassess compliance frameworks and innovate lower risk blends. Producers are strengthening supply chain resilience and investing in process optimization to meet evolving standards without disrupting downstream industries. Infrastructure resilience initiatives in developing regions are continuing to prioritize long life construction materials, which is sustaining adoption despite sustainability driven transitions.

Key Industry Highlights

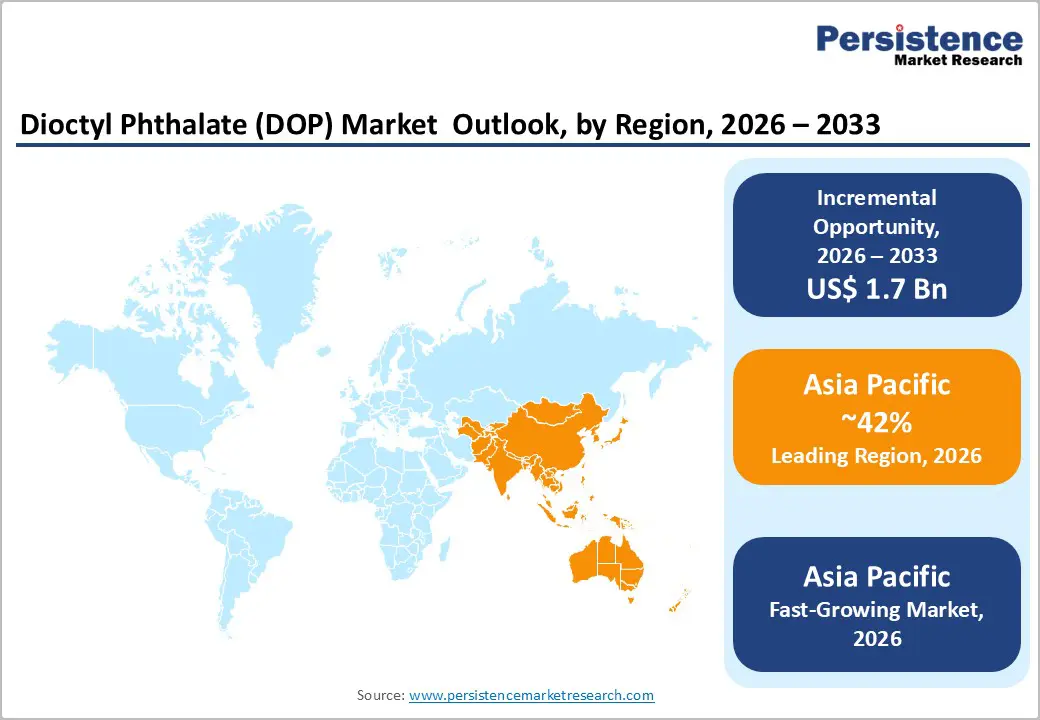

- Regional Leadership: Asia Pacific is likely to lead as well as emerge as fastest-growing market through 2033, accounting for approximately 42% market share, supported by robust construction output and automotive production.

- Product Type Dominance: General-purpose grade DOP is set to secure around 62% market revenue share in 2026, and medical-grade DOP is poised to be the fastest-growing segment during the 2026-2033 forecast period.

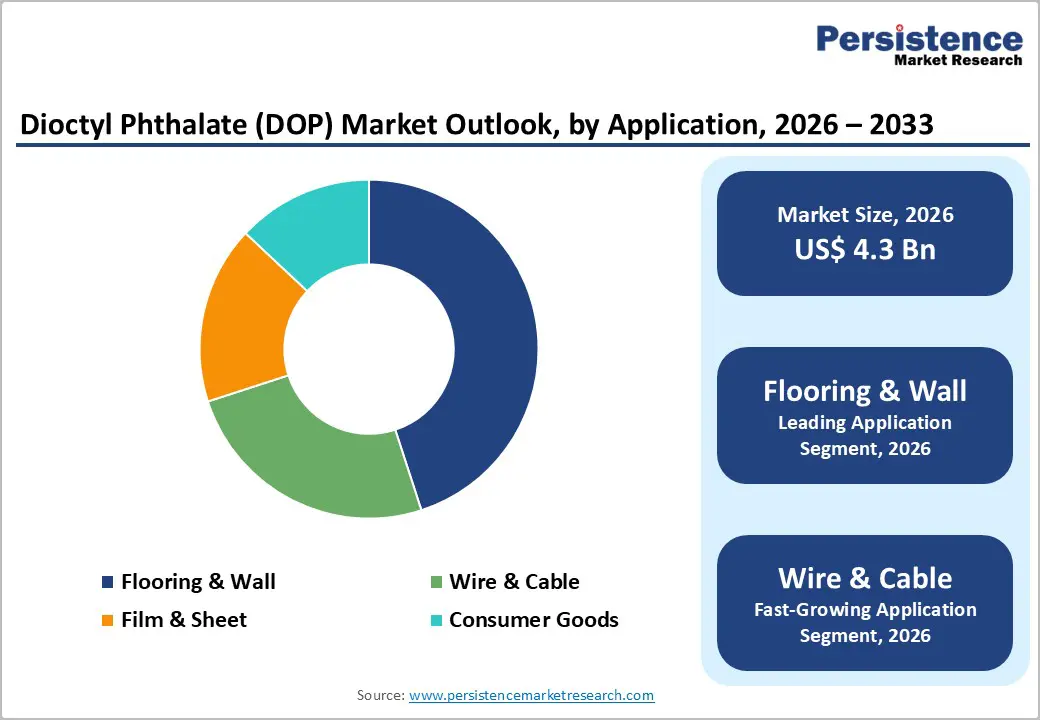

- Leading & Fastest-growing Applications: Flooring & wall coverings are expected to lead with an estimated 35% revenue share in 2026, while wire & cable applications are expected to register the highest growth between 2026 and 2033.

- Prime Driver: The central position of DOP as the primary plasticizer in flexible PVC products such as flooring, wall coverings, roofing membranes, and window profiles mainly drives the market.

- Prominent Opportunity: Heavy investments in R&D efforts to formulate advanced DOP offerings while tackling environmental issues is a high-value market opportunity.

| Key Insights | Details |

|---|---|

| Dioctyl Phthalate (DOP) Market Size (2026E) | US$ 4.3 Bn |

| Market Value Forecast (2033F) | US$ 6.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Construction and Infrastructure Development Activities

Rising construction activity is directly increasing dioctyl phthalate consumption since it functions as a core plasticizer in flexible PVC products such as flooring systems, wall coverings, roofing membranes, and window profiles. Developers are selecting these materials for their durability, elasticity, and cost efficiency in both new builds and renovation projects. Architects and contractors are incorporating DOP plasticized PVC to deliver weather resistant and long lasting building solutions that extend asset life cycles. In the United States, the Infrastructure Investment and Jobs Act is accelerating infrastructure renewal, which is strengthening demand for PVC based cabling insulation, sealing systems, and protective structural coatings across public works projects.

Construction companies are relying heavily on plasticized materials to meet performance specifications at scale, reinforcing steady plasticizer offtake. Residential development is recovering in line with urbanization trends and housing demand, which is supporting consistent material procurement. Suppliers are aligning manufacturing output and distribution planning with expanding project pipelines to ensure supply continuity. At the same time, producers are adapting formulations to comply with tightening environmental standards governing phthalate usage. Procurement teams are securing long term partnerships with compliant and quality focused DOP manufacturers to mitigate regulatory risk and safeguard supply reliability. As infrastructure modernization continues globally, construction will remain a foundational driver of DOP demand, linking performance requirements with evolving sustainability expectations.

Competitive Pressure from Alternative Plasticizer Technologies

The dioctyl phthalate market growth is facing intensifying competition from advanced plasticizer technologies that are offering enhanced performance profiles and improved environmental positioning. Non phthalate alternatives such as 1,2 cyclohexane dicarboxylic acid diisononyl ester (DINCH) and citrate based plasticizers are gaining traction in flexible PVC applications, particularly where regulatory scrutiny is high. These substitutes are delivering lower migration characteristics and stronger compliance alignment in sensitive end uses. Bio based plasticizers derived from renewable feedstock sources such as vegetable oils are also expanding their footprint as manufacturers with sustainability mandates are prioritizing greener material inputs. Large PVC compounders are increasingly adopting dual portfolio strategies by supplying both phthalate based and phthalate free product lines to address diverse customer requirements.

Volatility in petrochemical feedstock pricing, including fluctuations in 2 oxo alcohol costs, is narrowing the traditional price advantage associated with DOP. Alternative plasticizer producers are scaling capacity and optimizing manufacturing efficiency, which is intensifying pricing competition. Buyers are fragmenting procurement strategies as regulatory compliance and sustainability metrics become key decision variables. In response, DOP suppliers are developing hybrid formulations that combine cost efficiency with improved migration resistance and environmental attributes. Procurement leaders are strengthening evaluation frameworks by considering total cost of ownership, lifecycle impact, and regulatory exposure. Strategic collaboration with technology innovators is accelerating product transitions and supporting circular economy initiatives, in a bid to diversify the market.

Technological Innovation in High-Performance DOP Formulations

Research & development (R&D) initiatives are strengthening dioctyl phthalate performance while addressing environmental and safety concerns. Advanced purification technologies are reducing impurity levels, which is enabling application in higher specification segments including medical grade and food contact materials under stricter compliance frameworks. Hybrid plasticizer systems are blending DOP with stabilizing agents such as epoxidized soybean oil and polymeric plasticizers to enhance heat stability and reduce migration. These engineered combinations are preserving core flexibility and processing advantages while improving durability and emission profiles. Manufacturers are also introducing specialized grades with lower volatile organic compound output to support indoor air quality standards in building applications.

Parallel innovation is emerging through circular economy models that are exploring chemical recycling of DOP containing PVC waste streams. Closed loop approaches are supporting resource recovery and reducing lifecycle environmental impact. Customers are increasingly prioritizing formulations that align with regulatory mandates without compromising cost efficiency or mechanical performance. Market stakeholder can gain strategic advantage by partnering with suppliers that integrate sustainability metrics into product development. Collaborative engagement with research focused organizations is accelerating adoption of next generation solutions. Through proactive innovation and compliance alignment, enhanced DOP formulations are enabling entry into premium applications while reinforcing resilience in a shifting plasticizer landscape.

Category-wise Analysis

Product Type Insights

General grade is slated to be the leading the product type in 2026, likely to account for an estimated 62% of the dioctyl phthalate market revenue share, as it is known for delivering balanced performance and cost efficiency across a wide range of industrial applications. This grade is functioning as a standard plasticizer in PVC products, where it is enhancing flexibility, processability, and long term durability. Construction and automotive manufacturers are driving demand as they require dependable materials for flooring systems, wire and cable insulation, and vehicle interior components. Producers are favoring this variant due to its consistent compatibility with PVC resins and stable processing characteristics. End users are benefiting from a combination of mechanical strength and economic viability, which is sustaining its dominant market position despite evolving regulatory and sustainability pressures.

Medical grade DOP is expected to grow the fastest during the 2026-2033 forecast period, since it meets stringent healthcare compliance requirements. This specialized variant is being utilized in applications such as intravenous (IV) bags, medical tubing, and surgical equipment where purity and safety standards are critical. Rising healthcare expenditure and increasing demand for medical devices driven by aging populations and chronic disease prevalence are reinforcing segment growth. Manufacturers are investing in advanced purification and quality control systems to align with international regulatory benchmarks. Healthcare providers are prioritizing consistent material performance and validated safety profiles, which is strengthening confidence in certified medical grade plasticizers for sensitive clinical environments.

Application Insights

Flooring & wall coverings are poised to represent the dominant application area, capturing approximately 35% of the DOP market revenue share in 2026. Flexible PVC flooring systems such as luxury vinyl tiles, sheet vinyl, and composition tiles are relying on dioctyl phthalate to achieve the flexibility and wear resistance required in high traffic environments. Commercial construction projects including retail outlets, healthcare facilities, and educational institutions are selecting vinyl solutions because they are offering cost efficiency and durable surface performance. Residential renovation activity is also sustaining baseline demand as homeowners are prioritizing aesthetic upgrades and long lasting materials. Although parts of Europe are transitioning toward phthalate free options in residential settings due to regulatory pressure, commercial and industrial segments continue to depend on DOP plasticized formulations where performance consistency and economic viability remain decisive factors.

Wire and cable applications are anticipated to showcase the highest growth trajectory between 2026 and 2033, fueled by electrical infrastructure upgrades and accelerating energy transition initiatives globally. Grid expansion, renewable energy deployment, and automotive electrification are increasing the need for insulation materials with strong dielectric properties, thermal resistance, and flame retardant performance. Specialized DOP-based formulations are enabling cable flexibility in applications that involve continuous bending and mechanical stress. Power transmission and telecommunications investments are strengthening demand, particularly in countries such as China and India, as well as across the Middle East. Growth in electric vehicle production is further driving requirements for advanced wiring harness systems that must withstand elevated temperatures while maintaining structural integrity across diverse climate conditions.

End-User Insights

The construction segment is expected to lead with an approximate 48% of the dioctyl phthalate market share in 2026, driven by the extensive incorporation of DOP by manufacturers into building materials such as pipes, cables, and flooring systems. These applications are requiring flexibility, impact resistance, and long service life under continuous mechanical and environmental stress. Rapid urbanization and infrastructure expansion across developing economies are reinforcing consumption of DOP plasticized PVC products. Project developers are prioritizing resilient materials that withstand temperature variation, moisture exposure, and long term wear. At the same time, sustainability driven construction practices are encouraging adoption of durable solutions that extend asset lifespan and reduce replacement cycles. Builders are seeking compliant formulations that align with green building benchmarks while preserving structural integrity and cost effectiveness.

The automotive sector is predicted to grow the fastest through 2033. Manufacturers are leveraging DOP to enhance flexibility and mechanical performance in interior trims, exterior components, and under hood applications. Lightweight material strategies aimed at improving fuel efficiency and lowering emissions are increasing reliance on advanced plasticized systems. Growth in electric vehicle production is creating additional opportunities, as engineers are specifying high performance insulation, sealing systems, and vibration resistant components that must tolerate thermal stress and continuous movement. Suppliers are refining formulations to support electrification requirements and evolving design standards. Companies that are developing durable and adaptable DOP grades aligned with next generation vehicle architectures will have strengthened their positioning as automotive priorities continue to shift toward efficiency and reliability.

Regional Insights

Asia Pacific Dioctyl Phthalate (DOP) Market Trends

Asia Pacific is poised to be both the leading and the fastest-growing regional market for DOP in 2026, accounting for approximately 42% of global market value. Regional DOP consumption is led by China, followed by Japan, India, South Korea, and the ASEAN bloc. Strong construction activity and automotive manufacturing are positioning the region as both a production base and a major demand center. Urban migration is increasing housing requirements, while large infrastructure programs such as the Belt and Road Initiative (BRI) are stimulating cross border development of transport corridors and utilities. India is advancing highway expansion, smart city programs, and affordable housing schemes, all of which are reinforcing demand for plasticized PVC in pipes, cables, and flooring systems. Industrial growth across Southeast Asia is also attracting foreign direct investment into manufacturing clusters, further strengthening material consumption.

Regulatory approaches across the region remain comparatively flexible in industrial applications, which is sustaining DOP usage in construction and infrastructure. China is gradually restricting certain consumer applications while permitting continued use in building and heavy industrial sectors. India is emphasizing industrial safety standards without imposing broad phthalate limitations on construction materials, and Southeast Asian markets are maintaining foundational chemical safety frameworks. Proximity to feedstock sources such as 2 ethylhexanol and phthalic anhydride is supporting cost efficient production, particularly in China where integrated capacity strengthens supply chain reliability. Regional producers including Aekyung Petrochemical, LG Chem, Nan Ya Plastics, and Sinopec are competing alongside multinational firms through localized operations. Companies that are aligning sourcing strategies with regional policy trends and infrastructure pipelines will have strengthened long term positioning within this high volume market.

Europe Dioctyl Phthalate (DOP) Market Trends

Europe is anticipated to secure a considerable portion of the DOP market share in 2026 and beyond, with Germany leading regional consumption, followed by France, the U.K., and Spain. Demand is anchored in construction activity and automotive manufacturing, even as regulatory oversight remains stringent. Eastern European markets such as Poland, Romania, and Czech Republic are experiencing elevated building development and industrial expansion. Renovation programs are prioritizing energy efficiency upgrades through PVC materials used in flooring, window profiles, and roofing systems. Policy initiatives under the European Green Deal and the Renovation Wave are channeling funding toward sustainable infrastructure and grid modernization, which is supporting continued PVC demand in structural and energy related applications.

Regulatory compliance remains a defining factor in market strategy. Under the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework, DOP is classified as a substance of very high concern (SVHC), which restricts its use in consumer contact products and requires authorization for certain applications. The European Chemicals Agency (ECHA) is continuously reviewing phthalate restrictions, prompting substitution in sensitive segments. Alternatives such as diisononyl phthalate (DINP), diisodecyl phthalate (DIDP), 1,2 cyclohexane dicarboxylic acid diisononyl ester (DINCH), and dioctyl terephthalate (DOTP) are gaining adoption in consumer focused PVC goods. Regional producers including Grupa Azoty, BASF, and Perstorp are competing with imports from Asian suppliers by emphasizing specialty grades for automotive, medical, and export markets.

North America Dioctyl Phthalate (DOP) Market Trends

North America is set to maintain a stable presence in the global market for dioctyl phthalate, with the United States accounting for the majority of regional consumption. Construction recovery, consistent automotive production, and large scale infrastructure upgrades are reinforcing demand for plasticized PVC products. The Infrastructure Investment and Jobs Act is channeling funding into transport corridors, water infrastructure, and broadband expansion, which is increasing usage of PVC pipes, insulated cables, and structural components. Residential development is strengthening gradually, while commercial expansion in data centers and logistics facilities is supporting additional material uptake. Mexico continues to operate as a major automotive manufacturing hub serving export markets, and Canada is investing in transit systems, green infrastructure, and trade connectivity projects that further sustain industrial demand.

Regulatory oversight remains rigorous across consumer applications. The U.S. Environmental Protection Agency (EPA) enforces restrictions under the Toxic Substances Control Act (TSCA), while the Consumer Product Safety Commission (CPSC) limits phthalate usage in children’s products. State level requirements such as California Proposition 65 are also mandating disclosure obligations. These frameworks are steering DOP usage toward industrial and construction segments rather than consumer goods. Producers including ExxonMobil Chemical, Eastman Chemical, and BASF are emphasizing high purity and specialty grades while investing in feedstock integration and efficiency improvements. Buyers are prioritizing compliant supply channels and collaborative sustainability initiatives to manage regulatory exposure while capturing growth in essential infrastructure driven sectors.

Competitive Landscape

The global dioctyl phthalate market structure is moderately concentrated, with a group of multinational producers shaping pricing dynamics and supply stability. Prominent participants include ExxonMobil Chemical Company, LG Chem Ltd., BASF SE, Eastman Chemical Company, and Nan Ya Plastics Corporation. These firms account for a substantial portion of global output and are leveraging scale advantages, integrated feedstock access, and global distribution networks to maintain competitive positioning. Market leaders are strengthening their foothold through mergers and acquisitions, geographic expansion into high growth regions, and portfolio diversification across industrial and specialty grades.

Competitive intensity remains elevated as suppliers are focusing on performance optimization, regulatory alignment, and cost efficiency. Companies are investing in research and development to refine plasticizer properties, improve migration resistance, and explore advanced application areas within construction, automotive, and medical segments. Innovation efforts are also targeting process efficiency and emission reduction to respond to evolving environmental standards. Strategic entry into emerging markets is enabling firms to capture incremental demand driven by infrastructure expansion and industrialization. Organizations that are aligning capital investment, compliance readiness, and customer collaboration strategies will have reinforced their long term resilience within this evolving plasticizer landscape.

Key Industry Developments

- In February 2026, Fujian Chunda reduced DOP offering prices in China, reflecting a supplier adjustment to local market conditions and pricing dynamics in the region. This move signals short-term cost relief for buyers while market participants monitor broader demand and feedstock cost trends.

- In February 2026, DOP prices in Asia showed a mixed trend, with regional assessments in the Far East indicating variability in offer levels due to fluctuating demand sentiment and supply conditions. This uneven pricing underscores short-term market adjustments rather than a clear directional movement.

- In October 2025, Bhageria Industries launched a new range of plasticizers and ethoxylates, expanding its product portfolio to serve industries such as coatings, adhesives, and polymers. The offerings aim to provide performance flexibility, competitive pricing, and enhanced service support for customers across key application segments.

Companies Covered in Dioctyl Phthalate (DOP) Market

- ExxonMobil Chemical Company

- LG Chem Ltd.

- BASF SE

- Eastman Chemical Company

- Grupa Azoty

- Nan Ya Plastics Corporation

- Aekyung Petrochemical Co., Ltd.

- Sinopec Group

- Bluesail Chemical Group Co., Ltd.

- KLJ Group

- Mitsubishi Chemical Corporation

- Perstorp Group

- Henan Qing'an Chemical Hi-Tech Co., Ltd.

- UPC Technology Corporation

- Jiangsu Zhengdan Chemical Industry Co., Ltd.

Frequently Asked Questions

The global dioctyl phthalate (DOP) market is projected to reach US$ 6.3 billion in 2026.

The market is driven by a sustained demand for flexible PVC in construction, automotive, and packaging, fueling growth amid infrastructure booms and urbanization.

The market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Major opportunities lie in developing bio-based DOP variants, expansion avenues in emerging economies, and formulations that target regulatory compliance.

ExxonMobil Chemical Company, LG Chem Ltd., BASF SE, Eastman Chemical Company, and Nan Ya Plastics Corporation are some of the key players in the market.