- Specialty & Fine Chemicals

- 2-Ethylhexanol Market

2-Ethylhexanol Market Size, Share, and Growth Forecast 2026 - 2033

2-Ethylhexanol Market by Application (Plasticizers, 2-EH Acrylate, 2-EH Nitrate, Other), and Regional Analysis for 2026 - 2033

2-Ethylhexanol Market Size and Trend Analysis

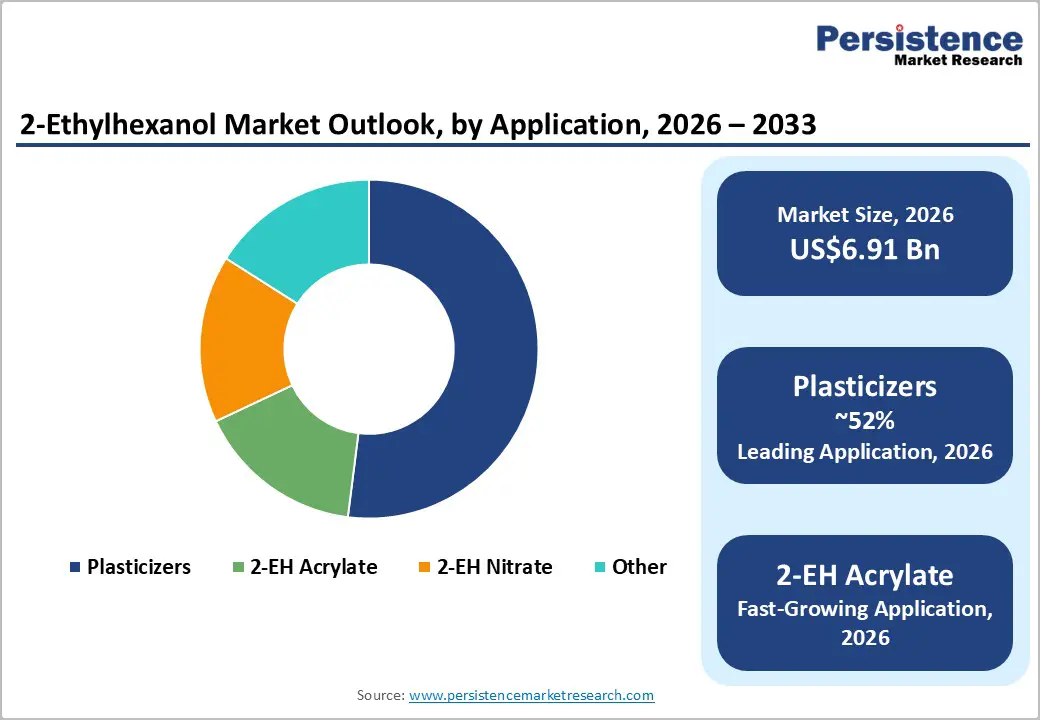

The global 2-Ethylhexanol market size is supposed to be valued at US$ 6.9 billion in 2026 and is projected to reach US$ 8.4 billion by 2033, growing at a CAGR of 2.8% between 2026 and 2033.

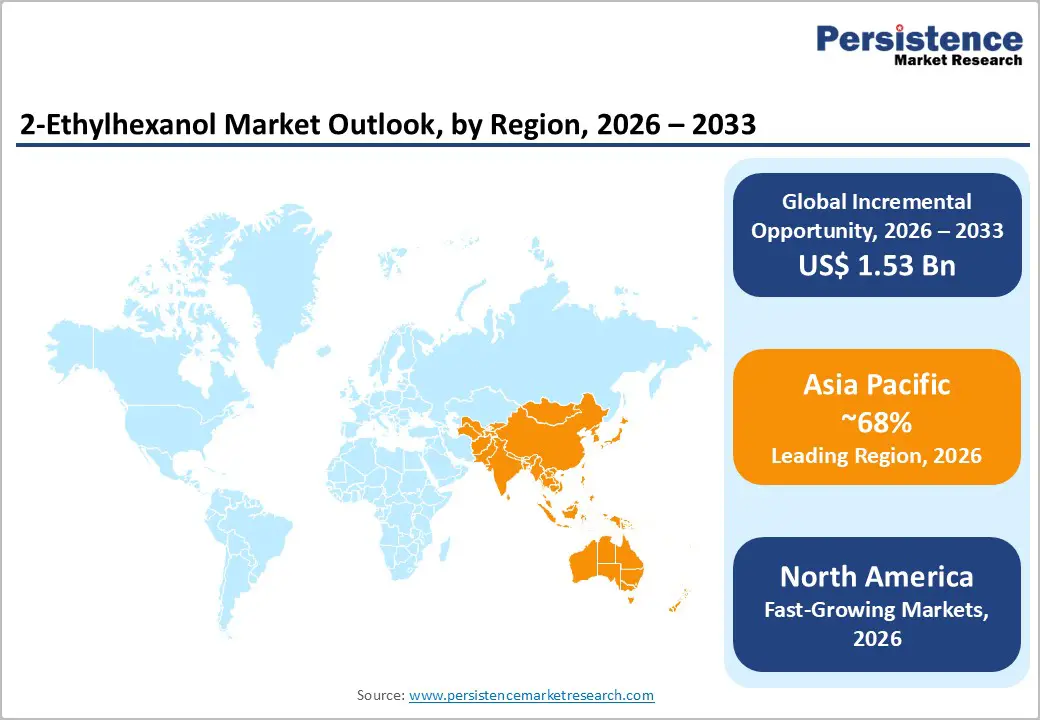

This moderate growth trajectory is primarily driven by the increasing consumption of plasticizers in flexible polyvinyl chloride (PVC) applications across construction, automotive, and consumer goods sectors. The Asia-Pacific region, particularly China, which accounts for approximately 50% of global production capacity, translating to around 2,800 kilotons, continues to dominate both production and consumption.

Key Market Highlights

- Leading Region: Asia Pacific dominates the global 2-ethylhexanol market, accounting for approximately 68% of production capacity, with China alone holding around 50% of global capacity due to robust industrial infrastructure, manufacturing advantages, and substantial construction sector growth.

- Fastest-Growing Region: North America is emerging as the fastest-growing region in the market, supported by rising end-use demand for plasticizers, emerging applications in fuel additives, and robust expansion in automotive and construction sectors.

- Dominant Segment: The plasticizers application segment accounts for approximately 52% of the market, driven by the essential role of 2-ethylhexanol in producing DOP and DOTP plasticizers for flexible PVC manufacturing in cables, flooring, automotive interiors, and construction materials.

- Fastest Growing Segment: The 2-ethylhexyl acrylate application segment exhibits robust growth potential, propelled by expanding demand in paints, coatings, adhesives, and packaging industries, supported by the construction boom and e-commerce sector expansion requiring durable coating and adhesive solutions.

- Key Market Opportunity: Development and commercialization of bio-based and non-phthalate plasticizers represents a significant opportunity, as demonstrated by LG Chem's December 2024 launch of eco-friendly 2-EH derivatives, addressing regulatory pressures and sustainability demands in Europe and North America.

| Key Insights | Details |

|---|---|

|

2-Ethylhexanol Market Size (2026E) |

US$ 6.9 Bn |

|

Market Value Forecast (2033F) |

US$ 8.4 Bn |

|

Projected Growth CAGR (2026-2033) |

2.8% |

|

Historical Market Growth (2020-2025) |

2.2% |

Market Dynamics

Drivers - Robust Infrastructure Development and Construction Activities in the Asia Pacific

Sustained infrastructure investments across the Asia-Pacific region continue to be a key driver of 2-ethylhexanol demand. China’s 14th Five-Year Plan allocates approximately US$4.2 trillion to transportation, energy, and urban development initiatives, whereas India’s National Infrastructure Pipeline allocates US$1.4 trillion to projects spanning renewable energy, road networks, and urban infrastructure.

These substantial capital commitments significantly increase the consumption of flexible PVC products, including cables, flooring, pipes, and wall coverings, which depend heavily on 2-EH-based plasticizers such as dioctyl phthalate (DOP) and dioctyl terephthalate (DOTP). Furthermore, the global construction sector, valued at US$5.69 trillion in 2024 and projected to reach US$8.64 trillion by 2030, reinforces robust and sustained demand for 2-ethylhexanol derivatives.

Increasing Demand for 2-Ethylhexyl Acrylate in Paints and Coatings Industry

The rising consumption of 2-ethylhexyl acrylate, a key derivative of 2-ethylhexanol, is driving significant growth in applications in paints, coatings, and adhesives. This monomer is integral to acrylic polymer production, offering superior flexibility, UV resistance, and durability in coating formulations. Rapid construction activity in emerging economies, coupled with renovation trends in developed markets, has boosted demand for emulsion paints and surface coatings.

Furthermore, the automotive industry increasingly requires high-performance coatings for interior and exterior applications, where 2-EH acrylate-based formulations provide enhanced weather resistance and aesthetic appeal. The expansion of e-commerce further increases demand for adhesives in secure packaging solutions, while industrial sectors adopt advanced coating technologies that use 2-EH acrylate to improve product longevity and performance.

Restraints - Stringent Regulatory Framework on Phthalate Plasticizers in Europe and North America

The enforcement of stringent regulations under the European REACH framework has significantly constrained market growth in developed regions. The European Chemicals Agency (ECHA) has listed 14 phthalates on the REACH Authorisation List (Annex XIV), imposing strict authorization requirements for specific applications. These measures arise from concerns over endocrine disruption and reproductive toxicity linked to traditional phthalate plasticizers.

Furthermore, the European Commission’s Restrictions Roadmap under the Chemicals Strategy for Sustainability, published in 2022, has intensified scrutiny on PVC-based plasticizers. As a result, demand for 2-EH-based phthalate plasticizers is declining in consumer goods sectors, particularly in children’s products. This regulatory environment compels manufacturers to reformulate and adopt non-phthalate alternatives, potentially limiting 2-ethylhexanol consumption in conventional applications.

Volatility in Raw Material Prices and Feedstock Availability

The production of 2-ethylhexanol relies heavily on propylene as a key feedstock through the oxo-synthesis process, making market dynamics susceptible to fluctuations in petrochemical raw material prices. Approximately half of China's 2-EH production capacity, totaling around 2.45 million tonnes, depends on feedstock purchased from spot markets, creating vulnerability to supply chain disruptions and price volatility. While propylene capacity expansions can potentially reduce production costs, competing downstream applications for oxo-alcohols create additional complexity.

Manufacturers often face decisions between producing n-butanol (NBA) versus 2-ethylhexanol based on prevailing margin differentials, which can impact 2-EH supply availability. Force majeure circumstances affecting major production facilities, as experienced during natural disasters impacting North American plants, demonstrate the market's susceptibility to supply disruptions. These factors collectively introduce uncertainty in pricing structures and supply reliability, potentially hindering consistent market growth and affecting downstream industries' procurement strategies.

Opportunities - Development and Commercialization of Bio-Based and Non-Phthalate Plasticizers

The shift toward sustainable chemistry offers significant growth prospects for 2-ethylhexanol manufacturers investing in eco-friendly derivatives. In December 2024, LG Chem launched an innovative phthalate-free 2-EH derivative, aligning with global sustainability goals and strengthening its position in environmentally conscious markets. This development addresses increasing regulatory pressures and consumer demand for safer alternatives that maintain performance while minimizing environmental and health risks.

Bio-based plasticizers derived from renewable feedstocks present additional opportunities, offering superior biodegradability and reduced carbon footprints compared to conventional petroleum-based products. Green chemistry principles, emphasizing renewable resources, safer solvents, and environmentally benign processes, are shaping product strategies. Producers delivering 2-EH derivatives that meet stringent environmental standards while ensuring flexibility, durability, and thermal stability will gain traction in premium markets, particularly in Europe and North America.

Expansion in Electric Vehicle Production and Advanced Automotive Applications

The global shift toward electric vehicles (EVs) is creating substantial growth opportunities for 2-ethylhexanol derivatives in advanced automotive applications. Rising EV production in Europe is driving increased use of PVC components, particularly in cable insulation and interior systems, where 2-EH-based plasticizers deliver essential properties such as flexibility, heat resistance, and electrical performance. These attributes are critical for battery wiring harnesses and insulation materials.

Additionally, the lightweight and readily processable nature of plasticized PVC supports vehicle weight optimization, thereby enhancing energy efficiency. Interior elements such as dashboards, seating, and trim increasingly incorporate PVC formulations containing 2-EH plasticizers to enhance durability, ease of maintenance, and design versatility. As EV adoption accelerates globally, manufacturers that develop application-specific formulations and forge partnerships with automotive OEMs will capture significant value from this transformative trend.

Category-wise Analysis

Application Insights

The plasticizers segment holds a dominant position in the 2-ethylhexanol market, accounting for approximately 52% of total applications. This leadership is attributed to 2-EH’s essential role as a feedstock in producing both phthalate and non-phthalate plasticizers, notably dioctyl phthalate (DOP) and dioctyl terephthalate (DOTP), which are critical for manufacturing flexible polyvinyl chloride (PVC). These plasticizers are widely utilized in high-demand sectors such as cables, flooring, wall coverings, automotive interiors, and synthetic leather. The versatility and cost-efficiency of flexible PVC make it indispensable across diverse industries.

In China, production capacity for DOP and DOTP stands at 2.75 million tonnes and 2 million tonnes annually, respectively, underscoring the scale of manufacturing. Continued growth in construction, particularly in emerging economies, sustains demand for PVC products incorporating 2-EH-based plasticizers, owing to their thermal insulation, weather resistance, and mechanical flexibility.

Regional Insights

North America 2-Ethylhexanol Market Trends

The North American 2-ethylhexanol market is experiencing significant growth, supported by rising end-use demand for plasticizers, emerging applications in fuel additives, and robust expansion in the automotive and construction sectors. Leading U.S. chemical companies manufacture or consume significant volumes of 2-EH for plasticizers used in construction materials, automotive components, and consumer goods. The thriving construction industry, driven by extensive residential and commercial projects, continues to boost demand for flexible PVC products reliant on 2-EH-based plasticizers.

Regional supply dynamics are evolving through capacity expansion initiatives. In March 2025, Oxea GmbH announced plans to increase production at its Bay City, Texas facility to meet growing demand for plasticizers and acrylate esters. Companies such as ExxonMobil, Eastman Chemical, and OQ Chemicals are also expanding output. Regulatory emphasis on product safety and environmental compliance is accelerating innovation in non-phthalate formulations. However, despite established infrastructure, North America remains behind Asia in absolute production capacity.

Europe 2-Ethylhexanol Market Trends

Europe represents a mature market distinguished by stringent regulatory frameworks and a strong commitment to sustainable chemical solutions. The European Union’s REACH regulation significantly shapes market dynamics, with 14 phthalates listed on the Authorisation List, requiring specific approvals for continued use. The European Chemicals Agency (ECHA) further reinforced this through its November 2023 investigation on PVC plasticizers under the Restrictions Roadmap of the Chemicals Strategy for Sustainability. These developments are accelerating the shift toward non-phthalate and bio-based alternatives.

Major markets such as Germany, the U.K., France, and Spain exhibit varying performance, influenced by construction activity and automotive production. Europe maintains notable 2-EH capacity, exemplified by Oxea Group’s Oberhausen plant. Rising EV demand is driving PVC usage in cable insulation and interiors, creating new opportunities for 2-EH derivatives. The market is transitioning toward premium, environmentally compliant products, supported by innovation that meets regulatory and performance standards.

Asia Pacific 2-Ethylhexanol Market Trends

Asia Pacific remains the leading region in the global 2-ethylhexanol market, accounting for approximately 68% of global production capacity. China alone accounts for nearly 50% of this capacity, equivalent to about 2,800 kilotons, and is the primary revenue contributor due to strong industrial growth. China’s total 2-EH output stands at 2.45 million tonnes, supported by major producers such as Daqing Petrochemical, Qilu Petrochemical, Tianjin Bohai Chemical, and Sichuan Petrochemical.

Significant government investments, including India’s Make in India initiative and large-scale infrastructure programs, are further stimulating consumption. Additionally, China’s anticipated 21% increase in propylene capacity and new facilities employing advanced LP Oxo technology reinforce Asia-Pacific’s position as the epicenter of global market growth.

Competitive Landscape

The global 2-ethylhexanol market is moderately consolidated, with a few multinational chemical companies holding significant shares alongside regional producers, particularly in Asia. Leading players such as BASF SE, Eastman Chemical Company, and Dow Chemical Company leverage integrated production systems, extensive distribution networks, and strong customer relationships across diverse end-use sectors. Competitive strategies focus on capacity expansion, technological advancements in oxo-synthesis, vertical integration, and the development of environmentally compliant derivatives. Companies increasingly pursue strategic partnerships and supply agreements to secure feedstock and strengthen their presence in high-growth regions.

Key Market Developments

- March 2025: Oxea GmbH, a prominent producer of oxo intermediates, announced plans to enhance production capacity at its 2-ethylhexanol facility in Bay City, Texas, to meet rising demand in the North American market for plasticizers and acrylate esters.

- December 2024: LG Chem unveiled a new eco-friendly derivative of 2-EH designed for phthalate-free plasticizers, aligning with the company's sustainability objectives and providing competitive advantages in markets with stringent environmental regulations.

- August 2024: BASF signed a Memorandum of Understanding with UPC Technology Corporation to supply 2-Ethylhexanol and N-Butanol from its upcoming Oxo plant at the Zhanjiang Verbund site, set to commence operations in 2025.

Top Companies in the 2-Ethylhexanol Market

BASF SE (Ludwigshafen, Germany) stands as one of the world's largest chemical producers with comprehensive 2-ethylhexanol production capabilities integrated within its global Verbund manufacturing network. The company's strategic expansion in Asia, particularly the upcoming Oxo plant at the Zhanjiang Verbund site through partnership with UPC Technology Corporation, positions it to capture growing demand in the region's construction and automotive sectors. BASF's technological expertise in oxo-synthesis processes, combined with its extensive customer base across plasticizers, coatings, and specialty chemicals applications, provides significant competitive advantages in technical service and product innovation.

Eastman Chemical Company (Kingsport, U.S.) operates a significant 2-ethylhexanol production capacity, including its major facility in Longview, Texas, serving North American and global markets. The company's integrated business model, spanning from feedstock procurement through derivative production, enables cost-effective operations and strong customer relationships across multiple end-use segments. Eastman's focus on specialty applications and technical customer support, combined with its commitment to sustainable chemistry practices, strengthens its market position in premium segments requiring high-purity 2-EH and specialized derivatives.

Dow Inc. (Midland, U.S.) maintains a strong presence in the 2-ethylhexanol market through its advanced oxo-technology platform and integrated petrochemical operations. The company's LP Oxo technology, licensed to producers such as Anqing Shuguang Petrochemical Oxo Co. for new capacity installations, demonstrates its technological leadership in efficient and environmentally responsible production processes. Dow's global manufacturing footprint, technical innovation capabilities, and strong relationships with downstream plasticizer and acrylate producers position it as a key influencer in market development and application innovation across construction, automotive, and industrial segments.

Companies Covered in 2-Ethylhexanol Market

- Dow Inc.

- BASF SE

- Eastman Chemical Company

- SABIC

- Sinopec

- Mitsubishi Chemical Corporation

- LG Chem, Ltd.

- INEOS Holdings Ltd.

- Formosa Plastic Group

- China National Petroleum Corporation

- Oxea GmbH

- ExxonMobil Chemical

- OQ Chemicals

- Grupa Azoty S.A.

- KH Neochem Co., Ltd.

- Tianjin Bohua Yongli Chemical Industry Co., Ltd.

- Luxi Chemical

- Anqing Shuguang Petrochemical Oxo Co.

- Henan GP Chemicals Co.

Frequently Asked Questions

The global 2-ethylhexanol market is projected to reach US$ 8.4 Bn by 2033, growing from US$ 6.9 Bn in 2026 at a CAGR of 2.8% during the forecast period, driven by increasing demand from plasticizers and acrylate applications.

The market is primarily driven by substantial infrastructure investments in the Asia Pacific, including China's US$ 4.2 trillion 14th Five-Year Plan and India's US$ 1.4 trillion National Infrastructure Pipeline, which fuel demand for flexible PVC products incorporating 2-EH-based plasticizers across construction, automotive, and consumer goods sectors.

The plasticizers segment dominates the market with approximately 52% share, as 2-ethylhexanol serves as a critical feedstock for producing DOP and DOTP plasticizers essential for flexible PVC manufacturing in cables, flooring, automotive interiors, and construction materials.

Asia Pacific leads the global market, accounting for approximately 68% of production capacity, with China alone holding around 50% of global capacity, translating to approximately 2,800 kilotons, driven by robust industrial infrastructure and substantial construction sector growth.

Significant opportunities lie in developing bio-based and non-phthalate plasticizers, as demonstrated by LG Chem's December 2024 launch of eco-friendly 2-EH derivatives, and in the expanding electric vehicle sector where 2-EH-based plasticizers are essential for cable insulation and interior components.

Key players include BASF SE, Eastman Chemical Company, Dow Inc., SABIC, Sinopec, Mitsubishi Chemical Corporation, LG Chem, INEOS Holdings, Oxea GmbH, and China National Petroleum Corporation, who leverage integrated operations and technological expertise to maintain competitive positions.