- Specialty & Fine Chemicals

- Dioctyl Fumarate Market

Dioctyl Fumarate Market Size, Share, and Growth Forecast, 2025- 2032

Dioctyl Fumarate Market by Grade (More than 99%, Less than 99%), Application (Chemical Manufacturing, Paints & Coatings, Adhesives, Lubricants, Cosmetics, Others), and Regional Analysis for 2025 - 2032

Dioctyl Fumarate Market Share and Trends Analysis

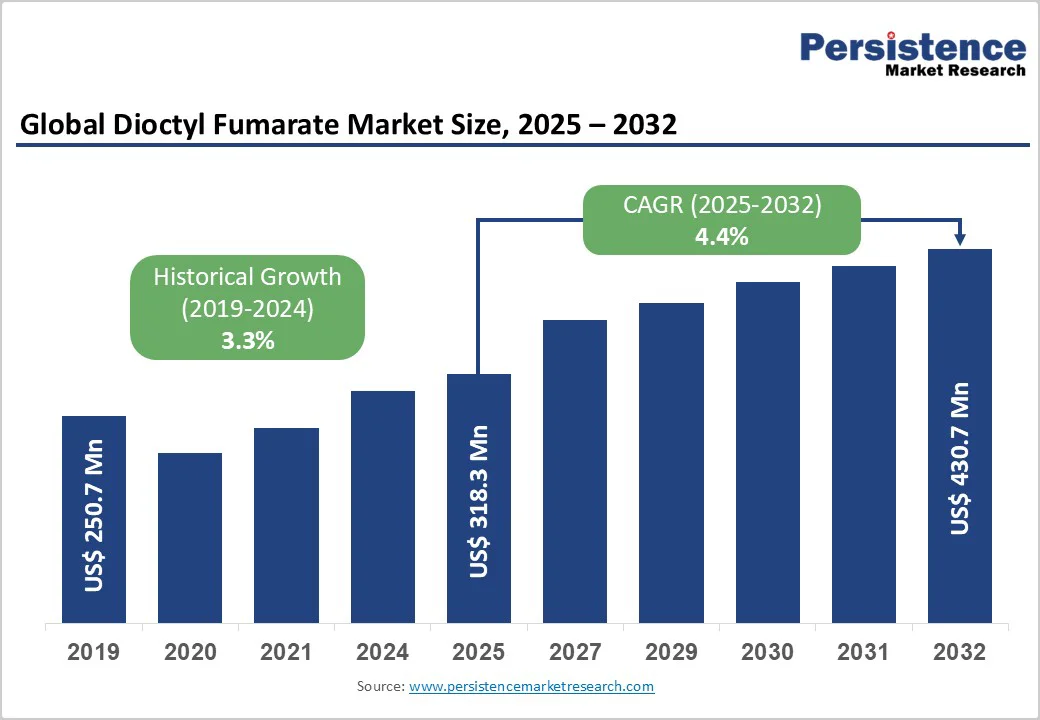

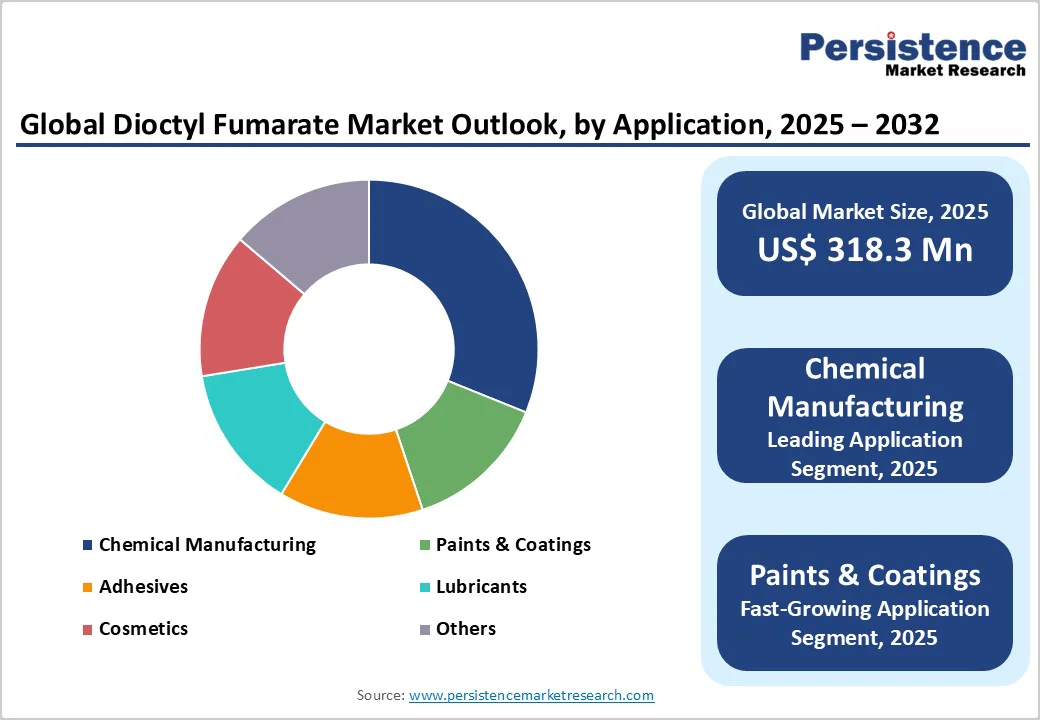

The global dioctyl fumarate market size is likely to be valued at US$ 318.3 million in 2025, and is projected to reach US$ 430.6 million by 2032, growing at a CAGR of 4.4% during the forecast period 2025 - 2032.

The consistent expansion of the market reflects the critical role of the compound as a chemical intermediate and plasticizer across multiple industrial applications. Dioctyl fumarate (DOF), with molecular formula C20H36O4, serves as an essential building block material in chemical manufacturing, demonstrating superior oxidative stability and enhanced lubricating properties.

The market's growth trajectory is further underpinned by a rising demand from the paints & coatings, adhesives, lubricants, and cosmetics industries, coupled with increasing adoption of non-phthalate plasticizer alternatives driven by stringent environmental regulations.

Key Industry-Highlights

- Dominant Grade: The >99% purity grade is expected to dominate with an estimated 60% market share in 2025, while the <99% grade represents the fastest growing segment through 2032, driven by cost-sensitive applications.

- Leading Application: Chemical manufacturing leads the application category, projected to hold approximately 40% share in 2025, while paints & coatings emerge as the fastest growing application during 2025 - 2032, fueled by infrastructure development and urbanization.

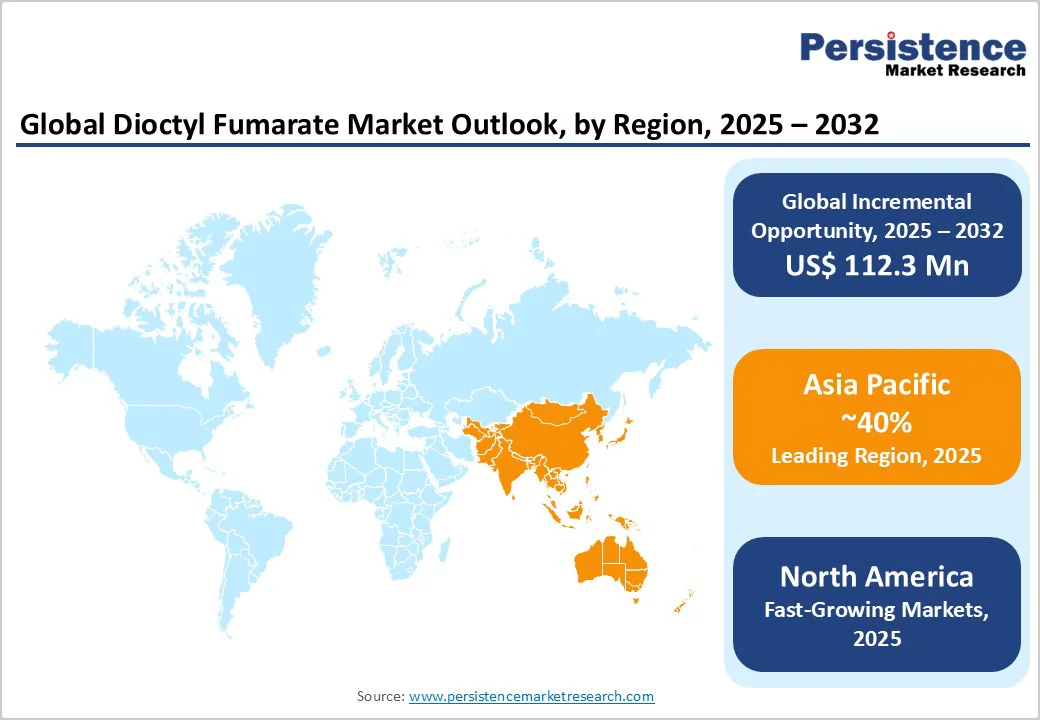

- Dominant Region: Asia Pacific is anticipated to dominate with a market share of about 40% share in 2025, led by China's chemical production growth and India's unprecedented industrial development.

- Fastest-growing Regional Market: North America is poised to be the fastest-growing regional market between 2025 and 2032, driven by stringent phthalate regulations and robust demand from construction, automotive, and adhesives sectors.

- Market Opportunities: Rising adoption of non-phthalate plasticizers due to regulatory pressure can create substantial growth opportunities, with eco-friendly plasticizers gaining promising traction over the 2025 - 2032 forecast period.

- Competitive Trends: Market consolidation has been accelerated through strategic acquisitions and expansion of high-purity production capabilities by Asian manufacturers.

| Key Insights | Details |

|---|---|

| Dioctyl Fumarate Market Size (2025E) | US$ 318.3 Mn |

| Market Value Forecast (2032F) | US$ 430.7 Mn |

| Projected Growth (CAGR 2025 to 2032) | 4.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Robust Growth in Paints & Coatings Industry Driving Demand

The paints and coatings sector represents the most significant demand driver for dioctyl fumarate, fueled by rapid urbanization and infrastructure development globally. According to Oxford Economics, global construction work done will reach a value of nearly US$ 14 trillion by 2037, powered by construction activities in China, the U.S., and India.

This favors the paints & coatings market, which in turn, can promote the dioctyl fumarate market growth. The role of DOF in manufacturing coatings, printing inks, and cosmetics positions it strategically within this expanding ecosystem, particularly as demand from new construction and automotive refinish segments accelerates across emerging markets.

The Asia Pacific chemical industry's expansion serves as another growth catalyst, with the region dominating both production and consumption of dioctyl fumarate. China's chemical production grew 6.8% in 2024, accounting for 86% of global chemical growth, while India's chemical sector, valued at US$ 220 billion in 2024, is projected to reach US$ 300 billion by 2028.

The chemical intermediates market in China and India benefits from abundant raw materials, affordable labor, and comprehensive supply chains, supporting leadership in specialty chemicals production. This regional industrial expansion directly correlates with a widening dioctyl fumarate demand, as manufacturers capitalize on competitive production economics and proximity to high-growth end markets.

Raw Material Volatility and Rising Competition from Alternative Plasticizers

The DOF market growth is restrained by raw material price volatility, supply chain disruptions, and intensifying competition from alternative plasticizers. Heavy dependence on petroleum-based feedstock exposes producers to crude oil price fluctuations, affecting production costs and profitability.

Recent logistics challenges and geopolitical tensions, including disruptions in key trade routes and fluctuating chemical output in major economies, have further strained global supply networks. The market’s moderate fragmentation limits pricing flexibility and increases vulnerability to input cost variations, particularly in export-driven regions such as Asia Pacific.

Adding to the above is the rising competition from non-phthalate and bio-based plasticizers that poses a long-term challenge. The growing adoption of sustainable materials, including itaconic acid derivatives and bio-esters, reflects industry preference for safer, low-migration alternatives.

However, the higher cost of bio-based additives compared to conventional phthalates restricts their use in price-sensitive applications such as construction and packaging. This dual challenge of cost pressure and competitive substitution continues to limit DOF market expansion and shrink profit margins globally.

Strengthening Sustainability Trends and Industrial Expansion to Create Lucrative Opportunities

The dioctyl fumarate market is poised to experience substantial growth opportunities as industries increasingly prioritize sustainable, low-toxicity, and high-performance chemical solutions.

The accelerating global transition toward eco-friendly manufacturing and green chemistry practices is reshaping demand dynamics across specialty chemicals, construction, automotive, lubricants, and adhesives sectors. End-users are seeking safer, customizable, and high-purity alternatives to conventional plasticizers, positioning DOF as a valuable additive for flexible PVC, coatings, and polymer formulations.

Emerging markets across Asia Pacific, particularly China, India, and Southeast Asia, are witnessing rapid infrastructure expansion and automotive production growth, fueling demand for advanced plasticizers and performance chemicals.

Simultaneously, the lubricants and adhesives industries are embracing materials with superior thermal stability, low volatility, and oxidative resistance characteristics well aligned with dioctyl fumarate’s functional properties.

As manufacturers intensify R&D investments in renewable feedstock sources and bio-based synthesis, DOF suppliers adopting sustainable production and product diversification strategies stand to capture significant long-term growth potential globally.

Category-wise Analysis

Supply Mode Insights

The DOF market is set to be led by the more than 99% purity grade segment, which accounts for an estimated 60% of the total demand. This dominance stems from the stringent quality and performance requirements in end-use industries such as construction, pharmaceuticals, and specialty chemicals.

High-purity DOF is essential for achieving superior adhesion, lubrication, and material compatibility, particularly in applications where product integrity directly affects long-term stability and safety. The trend toward high-performance, customized chemical solutions continues to reinforce the preference for premium-grade DOF across coatings, adhesives, and polymer formulations.

On the other hand, less than 99% purity grade represents the fastest-growing segment from 2025 to 2032. It caters to cost-sensitive applications such as plasticizers, industrial lubricants, and general-purpose adhesives. Rapid industrialization in developing regions, particularly across the Asia Pacific, is driving the adoption of lower-cost grades that deliver reliable performance without premium pricing, strengthening their market foothold.

Application Insights

Chemical manufacturing remains the dominant application, likely to account for more than 40% of the dioctyl fumarate market revenue share in 2025. The key role of DOF as a chemical intermediate and plasticizer in polyvinyl chloride (PVC) and related polymers enhances flexibility and durability across sectors such as construction, electrical, and medical products.

DOF’s strong solubility, thermal stability, and compatibility with multiple solvents make it indispensable in adhesive and polymer synthesis. The compound’s low toxicity and minimal environmental impact further strengthen its appeal for manufacturers aiming to meet global safety and sustainability standards.

Continuous innovations in polymer formulations and the growing demand for eco-friendly materials reinforce its leading position within the chemical manufacturing value chain.

In contrast, the paints and coatings segment is set to be the fastest-growing application through 2032, supported by rapid urbanization, infrastructure expansion, and the global shift toward sustainable coatings. Increasing adoption of water-borne, low-VOC formulations and stricter environmental regulations are boosting DOF demand as a non-phthalate additive that improves texture, adhesion, and durability.

Regional Insights

Asia Pacific Dioctyl Fumarate (DOF) Market Trends

Asia Pacific accounts for over 40% market share in the global dioctyl fumarate market, establishing itself as the fastest-growing region. This dominance is primarily driven by China and India, which serve as the key growth engines of the regional chemical sector. According to Cefic (2023), chemical sales highlight Asia Pacific’s industrial strength, with China (€2,238 billion) leading globally, followed by Japan (€146 billion), India (€134 billion), and South Korea (€135 billion).

China’s chemical production grew by 6.8% in 2024, solidifying its position as the world’s largest chemical market supported by abundant raw materials, cost-effective labor, and advanced manufacturing infrastructure. India’s chemical industry is also expanding rapidly, projected to reach USD 383 billion by 2030 at an 8% CAGR, supported by pro-industrial government policies and growing foreign investments.

The Asia Pacific Dioctyl Fumarate market is forecasted to grow at a CAGR of 7.2% through 2033, driven by accelerating industrialization, infrastructure development, rising disposable incomes, and a cost-competitive production base attracting strong domestic and international participation.

North America Dioctyl Fumarate (DOF) Market Trends

North America holds a significant position in the dioctyl fumarate market, supported by a mature chemical manufacturing infrastructure, stringent environmental regulations favoring non-phthalate alternatives, and strong presence of end-use industries. The United States DOF market benefits from shale gas advantages, providing cost-effective feedstock for chemical production, enhancing competitive positioning in specialty chemicals manufacturing.

Regulatory frameworks including the U.S. Environmental Protection Agency (EPA)'s TSCA Action Plan targeting phthalates are driving the adoption of safer plasticizer alternatives, creating market opportunities for compliant products. Innovation ecosystem and high R&D investment characterize the region, with manufacturers focusing on bio-based and sustainable chemical solutions aligned with corporate sustainability goals.

Europe Dioctyl Fumarate (DOF) Market Trends

Europe is rapidly emerging as one of the fastest-growing regional markets for dioctyl fumarate, propelled by strong regulatory reforms, sustainability initiatives, and expanding demand for eco-friendly chemical intermediates. The region’s strict bans on phthalates in consumer and industrial applications have accelerated the adoption of compliant alternatives such as DOF across construction, automotive, and packaging sectors.

With chemical production rebounding in 2024, led by Germany’s industrial recovery and renewed investment in specialty chemicals, the Europe DOF market’s growth momentum is supported by its transition toward green chemistry and circular economy principles.

European Union (EU) policies promoting energy-efficient buildings and low-carbon materials further enhance the market outlook, creating substantial opportunities for sustainable plasticizers and additives.

Major companies such as BASF, Evonik Industries, and Polynt S.p.A. are leveraging their technological expertise and R&D capabilities to meet evolving environmental standards. While high energy costs and competitive pressures persist, Europe’s strong regulatory framework and innovation-driven industry position it as a key growth hub for the DOF market.

Competitive Landscape

The global dioctyl fumarate market structure is characterized by moderate fragmentation, with key players accounting for more than one-fourth of total market share. The competitive landscape features a cluster of major manufacturers based in East Asia, particularly China, alongside global chemical companies with diversified product portfolios.

Leading players include ESIM Chemicals GmbH (Germany), Kawasaki Kasei Chemicals Ltd (Japan), Korea PTG Co. Ltd (South Korea), Polynt SpA (Italy), TNJ Chemical Industry Co. Ltd (China), Tokyo Chemical Industry Co. Ltd (Japan), and Penta Manufacturing Company (United States).

The market structure reflects regional specialization, with Chinese manufacturers leveraging production scale and cost advantages, while established global players compete on quality, innovation, and regulatory compliance. Moderate concentration enables competitive pricing dynamics while supporting product differentiation strategies based on purity levels, application-specific formulations, and technical service capabilities.

Key Industry Developments:

- In October 2025, ESIM Chemicals in Austria filed for bankruptcy due to projected liquidity shortfalls in 2026, rising fixed costs, and losing key customer projects amid intense competition from Asian suppliers. The company, which employs 289 people and has assets of €144 million against liabilities of up to €147 million, aims to restructure and maintain production in most facilities. ESIM specializes in custom chemical manufacturing and was formed from DSM Pharmaceutical Products and Patheon, but its recent focus on specialty chemicals has faced market and cost pressures.

- In May 2025, Private equity firm Keystone Capital acquired a stake in Penta Fine Ingredients, a specialty ingredient supplier for the fragrance, flavors, and personal care industries. Headquartered in New Jersey, Penta serves multiple sectors with a focus on fragrances and personal care, supplying intermediates and specialty materials globally. The investment aims to support Penta’s expansion through strategic acquisitions and scaling operations amid rising demand for complex and clean label ingredients in beauty and personal care.

Companies Covered in Dioctyl Fumarate Market

- Polynt S.p.A.

- ESIM Chemicals GmbH

- Kawasaki Kasei Chemicals Ltd.

- TNJ Chemical Industry Co., Ltd.

- Tokyo Chemical Industry Co., Ltd. (TCI)

- Penta Manufacturing Company

- Korea PTG Co., Ltd.

- Hebei Yanxi Chemical Co., Ltd.

- Dayang Chem (Hangzhou) Co., Ltd.

- Chemwill Asia Co., Ltd.

- Other Market Players

Frequently Asked Questions

The global dioctyl fumarate market is estimated to reach US$ 318.3 million in 2025.

The key market driver is the rising adoption of non-phthalate and environmentally friendly plasticizers across various end-use industries such as construction, automotive, packaging, and consumer goods.

The dioctyle fumarate market is poised to witness a CAGR of 4.4% from 2025 to 2032.

Increasing prioritization of sustainable, low-toxicity, and high-performance chemical solutions across industries and growing adoption of non-phthalate plasticizer alternatives driven by stringent environmental regulations are key market opportunities.

Polynt S.p.A., ESIM Chemicals GmbH, Kawasaki Kasei Chemicals Ltd., and TNJ Chemical are a few leading players in the market.