- Specialty & Fine Chemicals

- Diethyl Oxalate Market

Diethyl Oxalate Market Size, Share, and Growth Forecast 2026 - 2033

Diethyl Oxalate Market by Product Form (Liquid Diethyl Oxalate and Powder Diethyl Oxalate), Application (Flavors & Fragrances, Dyestuffs, Solvents, Intermediates, Plasticizers, and Others), Industry (Pharmaceuticals, Agricultural, Plastics & Polymers, Cosmetics & Personal Care, Pigments & Dyes, Electronics, Chemicals, and Others), and Regional Analysis, 2026 - 2033

Diethyl Oxalate Market Size and Share Analysis

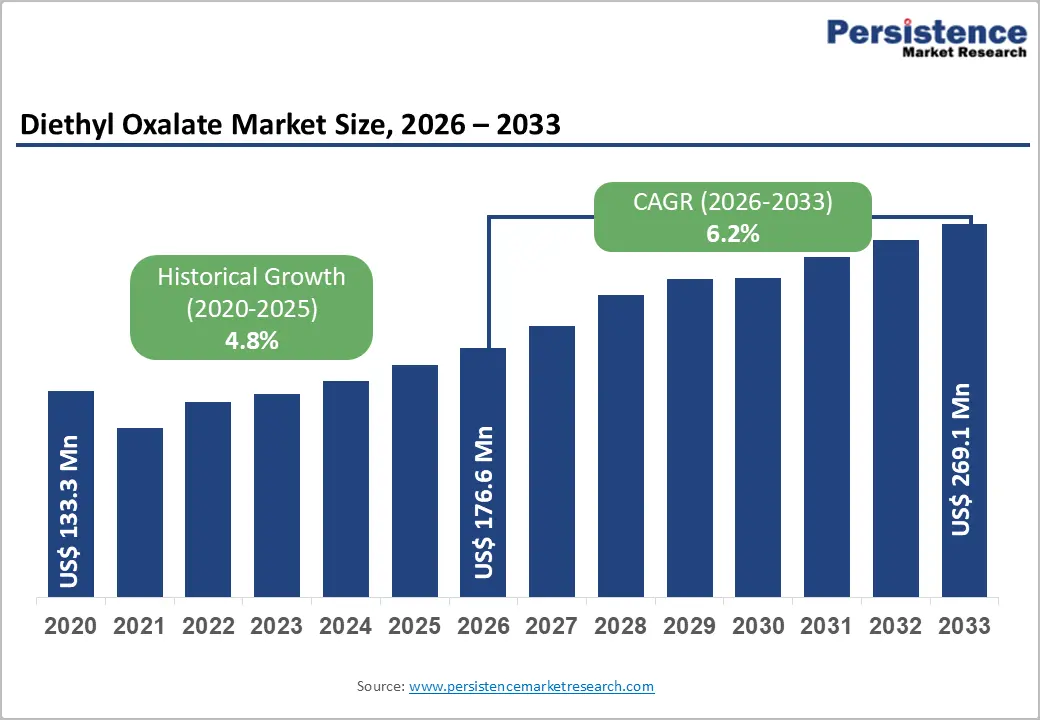

The global diethyl oxalate market size is likely to be valued at US$ 176.6 million in 2026 and is projected to reach US$ 269.1 million by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The diethyl oxalate market is experiencing robust expansion driven primarily by a rise in demand from the global pharmaceutical industry, where the compound serves as a critical intermediate in the synthesis of high-value active pharmaceutical ingredients (APIs), including steroids, barbiturates, and macrolide antibiotics.

Key Industry Highlights:

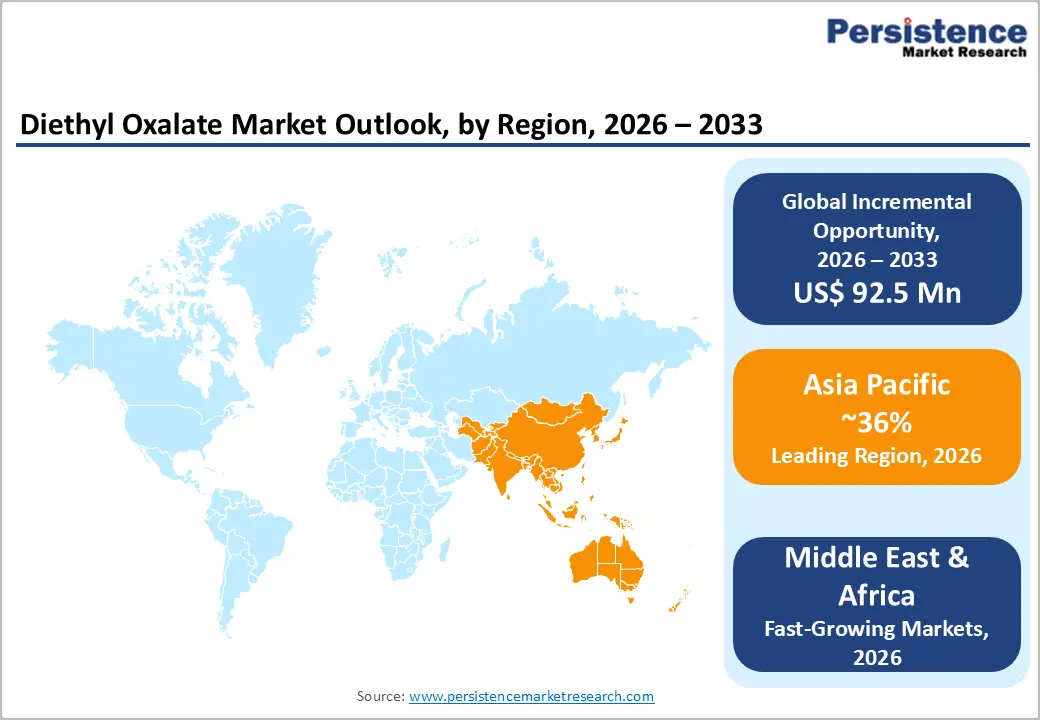

- Leading Region: Asia-Pacific dominates the global diethyl oxalate market, with a 36.5% market share (2026), driven by China's dominance in pharmaceutical API production and India's expanding pharmaceutical manufacturing sector, which accounts for 35%-40% of global pharmaceutical output.

- Fastest Growing Country: India exhibits the highest growth trajectory, expanding at a regional pace of 7.2% CAGR through 2033, fueled by pharmaceutical capacity expansion, establishing manufacturing hubs.

- Dominant Product Form: Liquid Diethyl Oxalate captures 59% market share within product category, driven by versatility as a solvent and chemical intermediate across pharmaceutical, cosmetics, and industrial applications requiring precise dosing and superior dispersion characteristics.

- Growing Segment: Pharmaceutical supported by global pharmaceutical market expansion and increased API production in the Asia Pacific, driving demand for pharmaceutical-grade diethyl oxalate intermediates.

- Key Market Opportunity: Renewable Energy Application in Dye-Sensitized Solar Cells (DSSCs) represents an emerging, high-growth opportunity, in which diethyl oxalate increases photocurrent density by up to 26%, creating incremental demand beyond traditional pharmaceutical applications.

| Key Insights | Details |

|---|---|

| Diethyl Oxalate Market Size (2026E) | US$ 176.6 Mn |

| Market Value Forecast (2033F) | US$ 269.1 Mn |

| Projected Growth CAGR (2026 - 2033) | 6.2% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Increasing Demand from the Pharmaceutical Industry for Active Pharmaceutical Ingredient Production

The accelerating demand from the pharmaceutical industry for Active Pharmaceutical Ingredient (API) production is a critical driver shaping the growth trajectory of several upstream chemical and materials markets. This surge is primarily driven by the expanding global burden of chronic and infectious diseases, an aging population, and increasing access to healthcare across emerging economies. Pharmaceutical manufacturers are scaling up API production to support higher volumes of generic drugs, branded formulations, and specialty therapies, including oncology, cardiovascular, and metabolic treatments. The rising emphasis on supply chain resilience has prompted many countries and pharmaceutical companies to localize or diversify API manufacturing, reducing dependence on single-source suppliers. Regulatory agencies are also enforcing stricter quality, purity, and traceability standards, which increases the consumption of high-grade intermediates, solvents, reagents, and processing aids used in API synthesis.

The growing pipeline of complex APIs, such as high-potency APIs, peptides, and biologically derived compounds, requires advanced chemical inputs and sophisticated production processes, further amplifying material demand. Contract Development and Manufacturing Organizations (CDMOs) play a pivotal role by expanding capacity and investing in new facilities to meet sponsor requirements, which in turn boosts the consumption of pharmaceutical-grade raw materials. The post-pandemic focus on vaccine development, antiviral drugs, and essential medicines has reinforced long-term investments in API infrastructure worldwide.

Rising use in Cosmetics, Personal Care, and Emerging Renewable Energy Applications

Rising utilization across cosmetics, personal care, and emerging renewable energy applications represents a diversified and increasingly influential demand driver. In the cosmetics and personal care industry, consumer preferences are shifting toward high-performance, multifunctional, and premium formulations that offer enhanced sensory appeal, longer shelf life, and proven efficacy. This trend is driving increased usage of specialty chemicals, functional additives, and high-purity ingredients in skincare, haircare, and color cosmetics. Growing awareness of personal grooming, rapid urbanization, and the influence of digital marketing and e-commerce platforms are further expanding consumption, particularly in developing regions.

Manufacturers are reformulating products to meet clean-label, sustainable, and regulatory-compliant standards, which often require higher volumes of specialized inputs. Beyond personal care, renewable energy applications are emerging as a significant growth avenue. Materials and chemicals are increasingly used in biofuels, energy storage systems, hydrogen production, and advanced battery technologies, where performance reliability and efficiency are critical. The global push toward decarbonization, energy security, and climate commitments is accelerating investments in renewable infrastructure, indirectly boosting demand for supporting materials.

Restraints - Toxicity Concerns and Stringent Regulatory Compliance Requirements

Diethyl oxalate exhibits mild toxicity characteristics classified under Acute Toxicity Category 4 (H302) according to EU Regulation (EC) No 1272/2008, capable of causing skin corrosion, eye irritation, and serious respiratory tract injuries upon prolonged exposure. Industrial epidemiological studies have documented associations between chronic exposure to diethyl oxalate and elevated incidence of leukemia, kidney and liver damage, and reproductive complications among manufacturing workforce populations.

These documented health risks necessitate rigorous occupational safety protocols, including specialized personal protective equipment, ventilation systems, and worker monitoring programs that substantially increase production costs. The EU REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) Regulation imposes Annex XVII restrictions on the use of diethyl oxalate, requiring hazard assessment documentation and alternative evaluation studies, thereby lengthening regulatory approval timelines and delaying market entry for new applications.

Supply Chain Volatility and Limited Availability of High-Purity Raw Materials

Diethyl oxalate production via esterification of oxalic acid with ethanol requires precise process control, specialized catalytic equipment, and stringent azeotropic distillation procedures that create operational barriers to entry for new manufacturers. Feedstock availability, particularly anhydrous oxalic acid and high-purity ethanol vary geographically, creating supply vulnerabilities in regions lacking integrated chemical production infrastructure.

Transportation of diethyl oxalate, a hazardous chemical subject to the European Agreement concerning the International Carriage of Dangerous Goods by Road (ADR) regulations, increases logistics costs by 15%-25% relative to non-hazardous chemicals, thereby compressing profit margins for smaller market participants lacking scale economies.

Opportunities - Renewable Energy Technologies and Dye-Sensitized Solar Cell Commercialization

Renewable energy technologies present a compelling market opportunity, particularly with the gradual commercialization of Dye-Sensitized Solar Cells (DSSCs) as a complementary alternative to conventional silicon-based photovoltaics. DSSCs offer unique advantages such as low-cost production, lightweight structure, flexibility, and strong performance under low-light and indoor conditions, making them suitable for applications in building-integrated photovoltaics, consumer electronics, smart windows, and Internet of Things (IoT) devices. As global governments and private stakeholders intensify investments to achieve decarbonization targets and energy transition goals, interest in next-generation solar technologies is increasing. Ongoing advances in dyes, electrolytes, nanomaterials, and encapsulation techniques are improving the efficiency, stability, and lifespan of DSSCs, thereby narrowing the performance gap with traditional solar cells.

The ability to manufacture DSSCs using simpler processes and lower energy input aligns well with sustainability and circular economic objectives. Emerging economies are also exploring decentralized and off-grid energy solutions, where DSSCs can play a role due to their adaptability and cost advantages. As pilot projects progress toward commercial-scale deployment, demand for high-performance materials, specialty chemicals, and precision-manufacturing inputs used in DSSC production is expected to increase. In parallel, supportive policy frameworks, research funding, and industry-academia collaborations are accelerating innovation and reducing commercialization risks.

Expansion of Pharmaceutical Manufacturing Capacity in Asia Pacific and Emerging Markets

The expansion of pharmaceutical manufacturing capacity in Asia Pacific and other emerging markets represents a significant long-term market opportunity driven by structural shifts in global healthcare supply chains. Countries across Asia Pacific are rapidly scaling up drug formulation and Active Pharmaceutical Ingredient production to meet rising domestic healthcare demand and to strengthen their position as global manufacturing hubs. Factors such as large patient populations, the increasing prevalence of chronic diseases, improved healthcare access, and supportive government policies are encouraging investment in new facilities and capacity expansion. Cost competitiveness, availability of skilled technical labor, and growing expertise in regulatory-compliant manufacturing further enhance the region’s attractiveness.

Multinational pharmaceutical companies are increasingly adopting “China+1” or diversified sourcing strategies, channeling investments into Southeast Asia, South Asia, and parts of Latin America and the Middle East to reduce supply chain risks. This capacity expansion is driving sustained demand for pharmaceutical-grade raw materials, intermediates, solvents, and advanced processing inputs. Contract manufacturing and outsourcing models are also gaining momentum, with local manufacturers upgrading infrastructure to meet international quality standards. As emerging markets move beyond volume-based generic production toward complex formulations, high-potency APIs, and specialty drugs, the requirement for high-purity and performance-driven materials will intensify.

Category-wise Analysis

Product Form Insighst

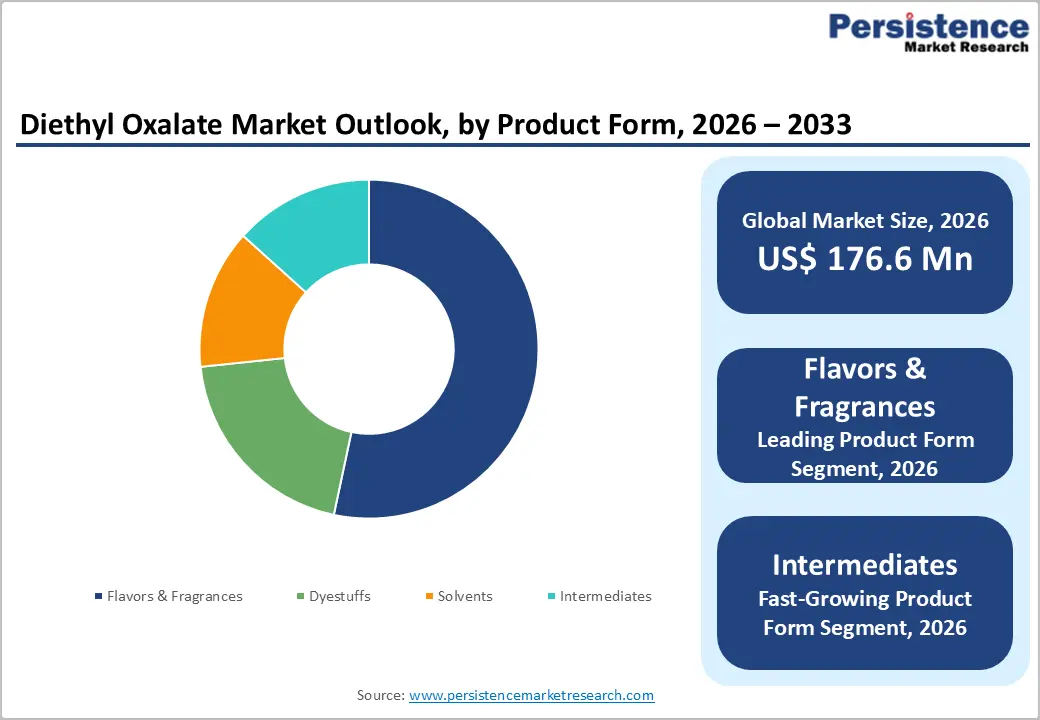

Liquid diethyl oxalate dominates the market with an estimated 59% market share in 2026, driven by its versatility as a solvent and chemical intermediate across pharmaceutical, cosmetics, and industrial applications. Liquid form enables easier integration into manufacturing processes, permits precise dosing in formulations, and facilitates superior dispersion in complex chemical reactions. The colorless liquid exhibits high purity specifications with boiling point at 18°C and melting point of 41°C, making it suitable for diverse processing temperatures required in pharmaceutical synthesis of barbiturates, steroids, and macrolide antibiotics.

Powder diethyl oxalate is an emerging segment, growing at a 7.1% CAGR from 2026 to 2033, driven by applications in solid-dose pharmaceutical formulations and in fine chemical synthesis that require controlled-release mechanisms. Powder form offers advantages including improved handling characteristics, enhanced stability in certain formulations, and potential for automation in manufacturing processes. The dual-form market structure reflects the specialized requirements of different end-user industries, with liquid form dominating pharmaceutical and cosmetics applications, while powder form captures niche applications in specialty chemicals and pharmaceutical adjuvants.

Application Insights

Flavors & fragrances are the leading application segment within product form categories, accounting for approximately 38% of the market based on application data and the pharmaceutical industry's preponderance. The pharmaceutical application encompasses the synthesis of phenobarbital and related barbiturates via Claisen condensations, steroid production for anti-inflammatory and hormonal therapies, and macrolide antibiotic synthesis for the treatment of bacterial infections. Diethyl oxalate's role as a chemical precursor for generating disubstituted malonic ester intermediates positions as an essential reagent in established pharmaceutical synthesis pathways with decades of validated chemistry.

Dyestuffs applications account for approximately 25% market share, where diethyl oxalate functions as a high-performance solvent for organic pigments and synthetic dyes utilized in textile manufacturing, industrial coatings, and specialized ink formulations. Solvents represent a significant share of the market, serving applications including cellulose ester dissolution, lacquer formulation, paint stripping, and polymeric residue cleaning in electronics manufacturing. Intermediates and Plasticizers collectively constitute 17% of market demand, supporting diverse industrial applications, including polyurethane synthesis, polymer additives, and specialty chemical production.

Industry Insights

Pharmaceuticals are the dominant Industry, accounting for approximately 38% of global diethyl oxalate consumption, reflecting their critical role as intermediates in complex drug synthesis. The pharmaceutical sector’s reliance on diethyl oxalate spans multiple therapeutic categories, most notably barbiturates used in neurological indications such as epilepsy and insomnia, corticosteroids for the treatment of inflammatory and autoimmune conditions, and macrolide antibiotics widely prescribed for bacterial infections. Diethyl oxalate is valued in pharmaceutical manufacturing for its high reactivity, controlled esterification behavior, and suitability for producing high-purity intermediates required under stringent regulatory standards.

Cosmetics & personal care account for approximately 13% of global diethyl oxalate consumption, owing to its functional versatility in high-value formulations. In this sector, diethyl oxalate is primarily used for fragrance enhancement, skin conditioning, and as a plasticizer that improves texture, stability, and sensory performance in premium cosmetic products. Its ability to enhance fragrance longevity and contribute to smooth, uniform application makes it particularly attractive for fine fragrances, skincare creams, and specialized personal care products. Rising consumer spending on beauty and grooming, increasing preference for premium and performance-oriented formulations, and rapid product innovation are key factors driving demand.

Regional Insights

North America Diethyl Oxalate Market Trends

North America represents a mature market, commanding approximately 32% of global diethyl oxalate market share, driven by established pharmaceutical manufacturing infrastructure and stringent regulatory standards that ensure product quality and supply chain reliability. The United States dominates regional consumption through its robust specialty chemicals and pharmaceutical sectors, where companies synthesize advanced therapeutics including long-acting barbiturates for neurological indications and complex steroid derivatives for endocrine treatments.

Regulatory compliance under FDA pharmaceutical manufacturing standards and EPA chemical safety protocols creates high barriers to entry for generic producers, enabling established suppliers to maintain pricing power and market share through superior product quality and traceability.

Regional market growth is projected at approximately 3.3% CAGR from 2026 to 2033, reflecting market maturity and saturation in traditional pharmaceutical applications. However, emerging opportunities in cosmetics and personal care formulations, particularly in premium skincare products marketed to affluent consumer demographics, provide incremental demand growth. Investment in renewable energy technologies, including dye-sensitized solar cell (DSSC) commercialization supported by federal tax incentives and state renewable portfolio standards, is generating new demand channels outside traditional pharmaceutical and cosmetics applications.

Europe Diethyl Oxalate Market Trends

Europe commands approximately 26% of the global diethyl oxalate market share, underpinned by a highly regulated operating environment shaped by EU REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) administered by the European Union, alongside the EC Cosmetics Regulation Annex III, which strictly governs ingredient safety, concentration limits, and permitted applications in finished products. These frameworks raise compliance thresholds but also reinforce demand for consistently high-purity, pharmaceutical- and cosmetics-grade diethyl oxalate.

Europe’s cosmetics and personal care industry, particularly its premium and dermocosmetic segments, represents a significant demand source for pharmaceutical-grade diethyl oxalate formulations. Manufacturers in the region emphasize product safety, regulatory compliance, and formulation performance to meet discerning consumer expectations and strict oversight. This focus supports steady uptake of high-specification inputs that deliver fragrance enhancement, formulation stability, and controlled functional performance. While regulatory scrutiny can lengthen approval timelines and elevate costs, it also creates barriers to entry that favor established suppliers with proven compliance records.

Asia Pacific Diethyl Oxalate Market Trends

Asia-Pacific is the dominant and fastest-growing regional market, accounting for 36.5% of the global diethyl oxalate market in 2026 and recording the highest regional growth rate. China leads regional consumption, supported by its position as the world’s largest pharmaceutical API manufacturer and exporter, with high-volume production of barbiturates, macrolide antibiotics, and steroid intermediates supplying global pharmaceutical value chains.

India is a rapidly expanding secondary market, with Indian Oxalate Limited supporting domestic demand and exports. India’s pharmaceutical sector, responsible for 35-40% of global manufacturing by volume, is expanding capacity at a 7.2% CAGR through 2033. Japan sustains niche demand via suppliers such as TCI Chemicals for ultra-pure grades used in advanced synthesis and research. Overall, cost-competitive manufacturing, ample feedstock availability, and accelerating pharmaceutical capacity position the Asia Pacific for continued dominance through 2032.

Competitive Landscape

The global diethyl oxalate market exhibits a moderately fragmented structure, with 15-20 established manufacturers controlling approximately 75-80% of total supply volume, alongside a multitude of regional and specialty producers that compete primarily on price sensitivity and local market familiarity. In the Asia Pacific region, Zibo Xusheng Chemical Co., Ltd. and Nanjing Chengyi Chemical Co., Ltd. exert dominant influence through high-volume production capacity, technical expertise in oxalate ester chemistry, and long-standing relationships with pharmaceutical manufacturers across China, India, Japan, and export markets.

Market leaders typically pursue expansion strategies focusing on capacity augmentation, geographic diversification into emerging pharmaceutical markets, and vertical integration upstream into oxalic acid and other key intermediates to secure raw material supply and cost efficiency. Smaller regional players remain relevant in niche segments, supplying local pharmaceutical and specialty chemical manufacturers, but face challenges in scaling due to regulatory barriers, high capital requirements, and the need for advanced production capabilities. Overall, the market structure balances consolidation among a few global leaders with opportunities for regional players who can deliver specialty products and localized support, creating a competitive but quality-driven landscape.

Key Developments:

- In January 2025, Zibo Xusheng Chemical announced capacity expansion initiative targeting 15,000 metric tons annual production by Q3 2025, targeting pharmaceutical manufacturers in India and Southeast Asia, anticipating pharmaceutical API production growth in the region.

- In September 2024, Indian Oxalate Limited completed facility modernization targeting pharmaceutical-grade product certifications and EU GMP (Good Manufacturing Practice) compliance to expand export market participation in European pharmaceutical supply chains.

- In May 2024, TCI Chemicals introduced ultra-pure diethyl oxalate formulations, achieving 99.99% chemical purity for advanced pharmaceutical research and specialized laboratory applications, supporting premium market segment positioning in developed markets.

Companies Covered in Diethyl Oxalate Market

- TCI Chemicals

- BorsodChem MCHZ, s.r.o

- Zibo Xusheng Chemical Co., Ltd

- ACETO GmbH

- Connect Chemical GmbH

- Chemtura Corporation

- Nanjing Chengyi Chemical Co., Ltd.

- RX Chemicals

- Alpha Chemika

- Hefei TNJ Chemical Industry Co., Ltd.

- Indian Oxalate Limited

- Mudanjiang Fengda Chemicals Corporation

- Kraton Corporation

- Gohil Dyechem

- CDH Fine Chemical

Frequently Asked Questions

The global diethyl oxalate market was valued at US$ 176.6 Mn in 2026 and is projected to reach US$ 269.1 Mn by 2033, representing a CAGR of 6.2% driven by escalating pharmaceutical demand, cosmetics applications, and emerging renewable energy technology adoption.

Primary demand drivers include pharmaceutical industry expansion for API production including steroids and barbiturates, cosmetics and personal care sector growth for fragrance enhancement and plasticizer applications, and emerging renewable energy applications in dye-sensitized solar cells (DSSCs) with photocurrent density improvements of up to 26%.

Liquid Diethyl Oxalate dominates market with 59% market share, driven by versatility as a chemical solvent and intermediate across pharmaceutical synthesis of barbiturates and steroids, cosmetics fragrance enhancement, and industrial applications requiring precise dosing and superior dispersion characteristics.

Asia Pacific commands the largest market share at 36.5% in 2026, driven by China's pharmaceutical API dominance and India's position accounting for 35% to 40% of global pharmaceutical manufacturing, with Zibo Xusheng Chemical operating 10,000 metric tons annual production capacity.

Renewable Energy Application in Dye-Sensitized Solar Cells (DSSCs) represents the most significant emerging opportunity, where diethyl oxalate functions as a cost-effective electrolyte additive improving photocurrent density by up to 26%, with global DSSC market projected to expand at 12.1% CAGR through 2033.

Major market participants include Zibo Xusheng Chemical Co., Ltd. (China, 10,000 tons/year capacity), Indian Oxalate Limited (India, leading domestic producer), Nanjing Chengyi Chemical Co., Ltd. (China, established 1993), BorsodChem MCHZ, s.r.o. (Czech Republic), TCI Chemicals (Japan), and regional suppliers including ACETO GmbH and Connect Chemical GmbH in Europe.