- Bulk Chemicals

- Diethylene Glycol (DEG) Market

Diethylene Glycol (DEG) Market Size, Share, and Growth Forecast, 2025 - 2032

Diethylene Glycol Market by Application (Antifreeze and Coolant, Solvents, Humectants, Polyester Resins and Plasticizers, Emulsifiers and Lubricants, Others), End-use (Agrochemical, Automotive, Cosmetic and Personal Care, Paints and Coatings, Oil and Gas, Textiles, Plastics, Others), and Regional Analysis for 2025 - 2032

Diethylene Glycol Market Size and Trend Analysis

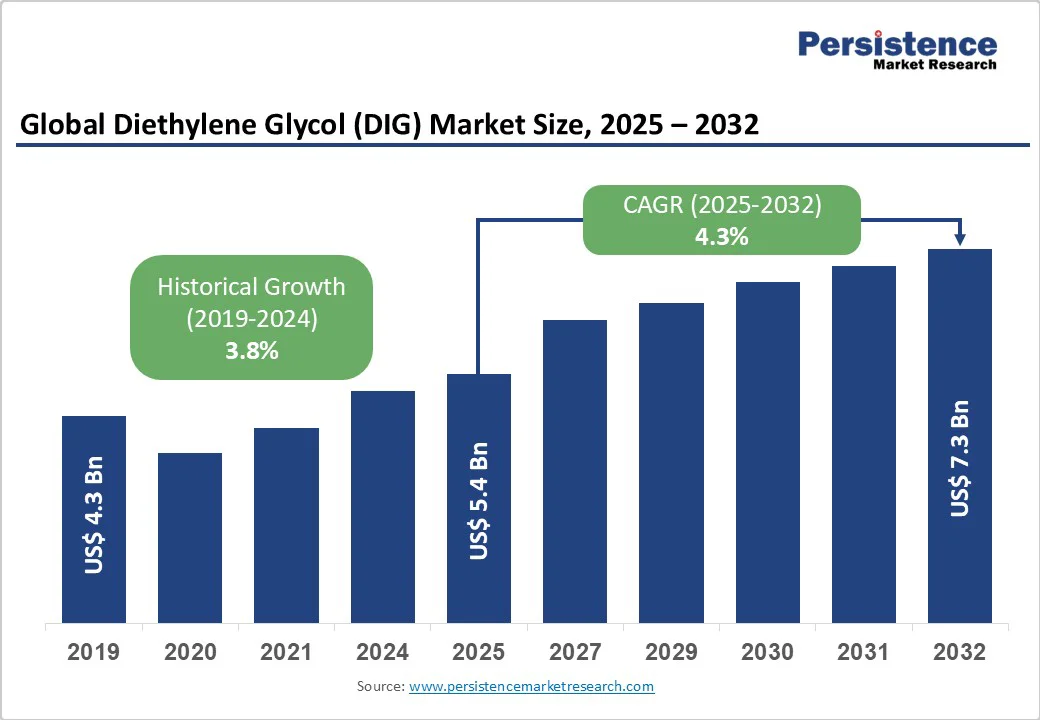

The global diethylene glycol market is likely to be value at US$5.4 Bn in 2025 and reach US$3.5 Bn by 2032, growing at a CAGR of 4.3% during the forecast period from 2025 to 2032.

The DEG market is experiencing robust growth, driven by its versatile applications across industries such as automotive, textiles, and plastics, where its properties as a solvent, humectant, and chemical intermediate are highly valued.

Key Industry Highlights:

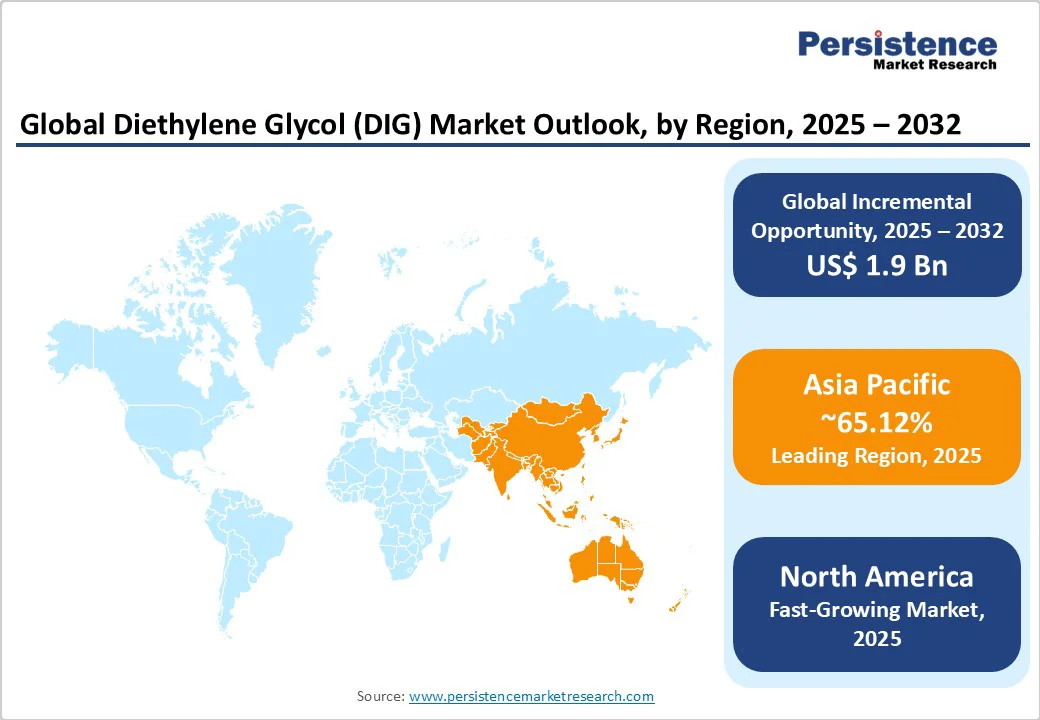

- Leading Region: Asia Pacific holds a 65.12% share in 2025, driven by rapid industrialization, high chemical production, and expanding automotive and textile industries in countries such as China and India.

- Fastest-growing Region: North America is the fastest-growing region, fueled by strong demand from the automotive and paints, and coatings sectors, supported by advanced manufacturing infrastructure in the U.S. and Canada.

- Investment Plans: China’s 14th Five-Year Plan (2021-2025) emphasizes chemical manufacturing and infrastructure development, boosting DEG demand for polyester resins and antifreeze applications.

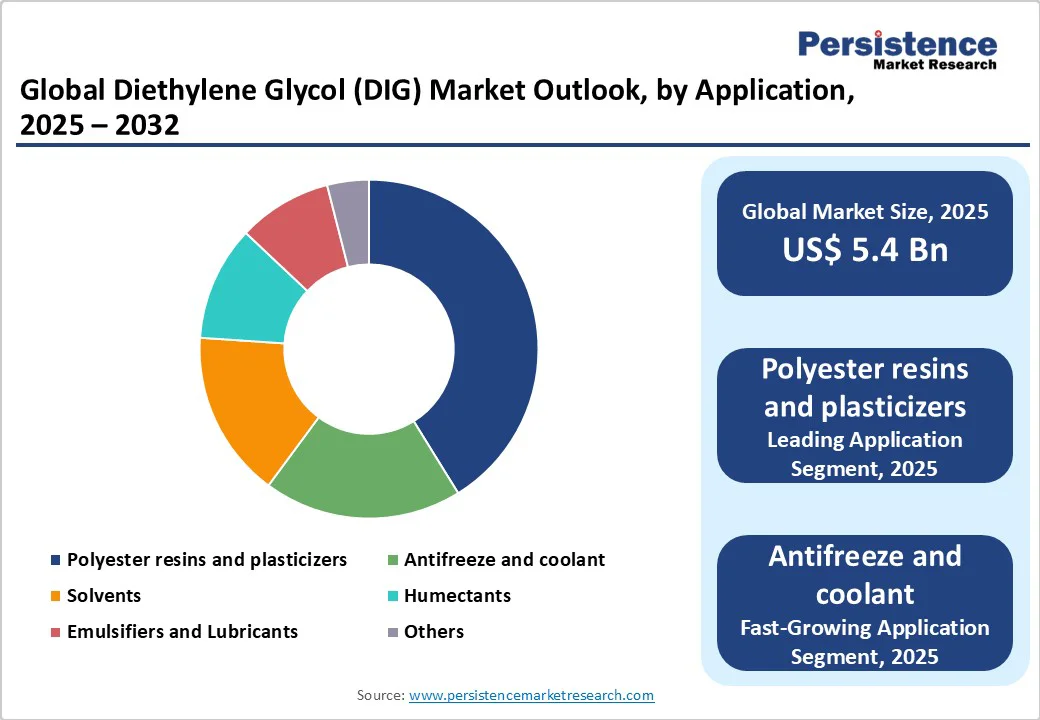

- Dominant Application: Polyester resins and plasticizers account for 41.3% share driven by their widespread use in plastics and packaging industries.

- Leading End-use: The plastics industry contributes over 21.8% of market revenue, propelled by global demand for flexible packaging and consumer goods.

| Key Insights | Details |

|---|---|

| Diethylene Glycol Market Size (2025E) | US$ 5.4Bn |

| Market Value Forecast (2032F) | US$7.3Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.8% |

Market Dynamics

Driver: Surging Demand in Polyester Resins and Automotive Sectors Fuels Market Growth

The global diethylene glycol market is witnessing significant growth due to the increasing demand for polyester resins and automotive applications. DEG is a critical raw material in producing polyester resins, widely used in packaging, textiles, and construction materials.

According to the International Trade Organization, global plastic production reached 436 million metric tons in 2023, with polyester resins accounting for a significant share, driving DEG consumption. In the automotive sector, DEG is essential for antifreeze and coolant formulations, ensuring engine efficiency in extreme conditions.

The global automotive industry relies on DEG for high-performance coolants, particularly in electric vehicles (EVs). Companies such as BASF SE reported sales increases in DEG-based products in 2024, driven by automotive and plastics demand. Government initiatives, such as India’s Production-Linked Incentive (PLI) scheme for chemicals, further boost DEG consumption, positioning these sectors as key drivers for market expansion through 2032.

Restraint: Fluctuating Raw Material Prices and Environmental Regulations

The diethylene glycol market encounters significant headwinds from both raw material volatility and tightening environmental regulations. As DEG is synthesized from ethylene—a derivative of crude oil and natural gas, its production costs are highly sensitive to fluctuations in global energy markets. This unpredictability places smaller manufacturers at a disadvantage, reducing their pricing flexibility and market competitiveness.

Additionally, regulatory frameworks such as the EU’s REACH impose strict environmental and safety requirements, raising operational and compliance costs. The rise of bio-based alternatives, such as bio-ethylene glycols, is further intensifying competition, especially in sustainability-focused regions. Moreover, concerns over DEG’s toxicity in sensitive applications, including cosmetics and personal care, and inconsistent regulatory standards across regions, further constrain growth and limit broader market adoption.

Opportunity: Rising Applications in Renewable Energy and Sustainable Packaging

The increasing focus on renewable energy and sustainable packaging presents significant opportunities for the diethylene glycol market. DEG is used in manufacturing polyester resins for recyclable plastics, aligning with global sustainability trends.

In renewable energy, DEG is used in lubricants and coolants for wind turbines and solar panel manufacturing. The International Energy Agency estimates global renewable energy capacity to increase by 2.5 times by 2030, boosting DEG demand. Companies such as Shell plc and Mitsubishi Chemical Corporation are innovating with eco-friendly DEG formulations for green applications.

Government policies, such as the EU’s Circular Economy Action Plan, encourage sustainable packaging, creating opportunities for manufacturers to develop high-performance, environmentally friendly DEG-based products to meet industry demands through 2032.

Category-wise Insights

By Application

- Polyester resins and plasticizers segment dominates the diethylene glycol market, contributing 41.35% of revenue in 2025, driven by its extensive use in plastics, packaging, and textiles. DEG’s role as a chemical intermediate ensures high demand in producing flexible and durable polyester-based products, with companies such as Reliance Industries Limited and Indorama Ventures leading in supplying DEG for packaging solutions across the Asia Pacific and North America.

- Antifreeze and coolant is the fastest-growing application, propelled by rising automotive production and the shift toward electric vehicles. DEG’s hygroscopic properties make it ideal for high-performance coolants, with major players such as BASF SE and LyondellBasell expanding offerings to meet demand in automotive hubs such as the U.S., Germany, and China.

By End-use

- The plastics sector leads with 21.8% of market share of the diethylene glycol market in 2025, driven by global demand for flexible packaging and consumer goods. DEG’s use in polyester resins supports applications in food packaging and industrial plastics, with companies such as Saudi Aramco and Nippon Shokubai Co. Ltd. catering to high-demand regions such as the Asia Pacific and Europe.

- Automotive industry is the fastest-growing end-use segment, fueled by increasing vehicle production and demand for antifreeze and coolants. The rise of electric vehicles and advanced manufacturing in the U.S. and China drives DEG consumption, with players such as Shell plc and Mitsubishi Chemical Corporation innovating for automotive applications.

Regional Insights

Asia Pacific Diethylene Glycol Market Trends

The Asia Pacific region is set to dominate the diethylene glycol market in 2025, capturing an estimated 65.12% share. This leadership is fueled by rapid industrialization, robust chemical manufacturing, and expanding automotive and textile sectors-particularly in China and India.

China, as the world’s largest chemical producer, accounting for 44% of global chemical output according to ITIF, ensures a reliable supply of raw materials essential for DEG production. Meanwhile, India’s growing textile and packaging industries, supported by the government’s Make in India initiative, are driving strong demand for DEG, especially in polyester resin manufacturing.

Major players such as Reliance Industries Limited and India Glycols Limited are strategically expanding their operations to serve increasing needs in marine, industrial, and consumer goods applications. Additionally, government-backed infrastructure development projects across the region further bolster industrial growth. These combined factors solidify Asia Pacific’s dominant position in the DEG market, a trend expected to continue through 2032, supported by ongoing urbanization and rising consumption.

North America Diethylene Glycol Market Trends

North America is emerging as the fastest-growing region in the diethylene glycol market, propelled primarily by strong demand from the automotive and paints & coatings industries across the U.S. and Canada. In the U.S., the automotive sector heavily depends on DEG for manufacturing antifreeze and coolant formulations, essential for vehicle performance and safety. Meanwhile, Canada’s robust chemical manufacturing landscape supports DEG’s application in various industrial uses, as highlighted by the Chemistry Industry Association of Canada.

Leading companies such as LyondellBasell and BASF SE hold significant market shares, leveraging their extensive distribution networks to supply DEG for major infrastructure and automotive projects. Additionally, growing consumer awareness and preference for high-performance, environmentally friendly chemicals are encouraging manufacturers to innovate and adopt greener DEG formulations. This shift toward sustainability, coupled with ongoing industrial growth, underpins North America’s rapid market expansion, positioning the region as a critical hub for DEG demand and innovation over the coming years.

Europe Diethylene Glycol Market Trends

Europe stands as the second fastest-growing region in the diethylene glycol (DEG) market, fueled by stringent environmental regulations, rising demand from the automotive and cosmetics sectors, and significant infrastructure investments in countries such as Germany and France.

Valued at €655 billion in 2023 according to CEFIC, the European chemical industry plays a crucial role in supporting DEG consumption, particularly in paints, coatings, and polyester resin production. Germany’s robust automotive industry, a major user of DEG-based antifreeze and coolants, benefits from the presence of leading chemical companies such as Merck KGaA and BASF SE.

Furthermore, the European Union’s Green Deal drives the adoption of sustainable packaging solutions and renewable energy initiatives, which are increasingly reliant on eco-friendly chemical products such as bio-based DEG. This strong regulatory focus on sustainability and compliance acts as a catalyst for market growth, positioning Europe for steady expansion in the DEG sector through 2032.

Competitive Landscape

The global diethylene glycol market is highly competitive, characterized by a fragmented landscape with numerous domestic and international players. Leading companies such as BASF SE, Reliance Industries Limited, and Indorama Ventures dominate through extensive product portfolios and global distribution networks.

Regional players, such as India Glycols Limited, focus on localized offerings in the Asia Pacific. Companies are investing in sustainable production technologies and bio-based DEG formulations to enhance market share, driven by demand for eco-friendly chemicals in the automotive and plastics sectors.

Key Industry Developments

- February 2023: Nippon Shokubai Co., Ltd. successfully received ISCC PLUS certification for 19 products, including monoethylene glycol, diethylene glycol, triethylene glycol, acrylic acid, and acrylic ester, allowing the company to produce and market low-environmental-impact products derived from biomass raw materials via the mass balance method. This certification supports the company's efforts to establish a global supply system, reduce environmental impact, and promote a circular economy.

- October 2024: Clariant launched its new line of high-performance pharmaceutical excipients at the CPHI Milan tradeshow in Milan, Italy. The products are designed to support the pharmaceutical development, particularly for injectables, and include new VitiPure and Polyglycol excipients. These excipients, such as diethylene glycol derivatives, meet stringent microbial control standards and surpass pharmacopoeia requirements for parenteral applications.

Companies Covered in Diethylene Glycol (DEG) Market

- BASF SE

- India Glycols Limited

- Indorama Ventures Public Company Limited

- LyondellBasell Industries Holdings B.V.

- Merck KGaA

- Mitsubishi Chemical Corporation

- Nippon Shokubai Co. Ltd.

- Pon Pure Chemicals Group

- Reliance Industries Limited

- Saudi Basic Industries Corporation (Saudi Aramco)

- Shell plc

- TCI Chemicals (India) Pvt. Ltd.

- Others

Frequently Asked Questions

The diethylene glycol market is projected to reach US$5.4 billion in 2025.

Growing demand in polyester resins and automotive applications, along with expanding use in sustainable packaging, are key market drivers.

The diethylene glycol market is poised to witness a CAGR of 4.3% from 2025 to 2032.

Rising applications in renewable energy and sustainable packaging are key market opportunities.

BASF SE, Reliance Industries Limited, Indorama Ventures, and Mitsubishi Chemical Corporation are key market players.