- Metals & Minerals

- Diamond Market

Diamond Market Size, Share, and Growth Forecast, 2026 - 2033

Diamond Market by Product Type (Synthetic, Natural, Rough, Polished), Application (Jewelry, Industrial), and Regional Analysis for 2026 – 2033

Diamond Market Size and Trends Analysis

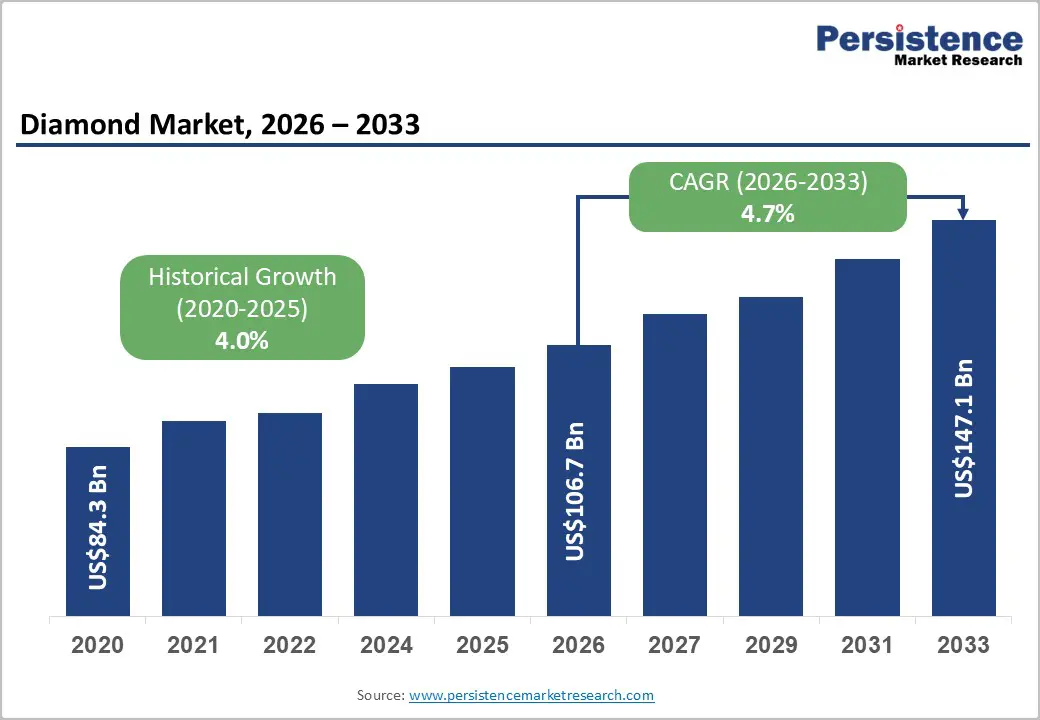

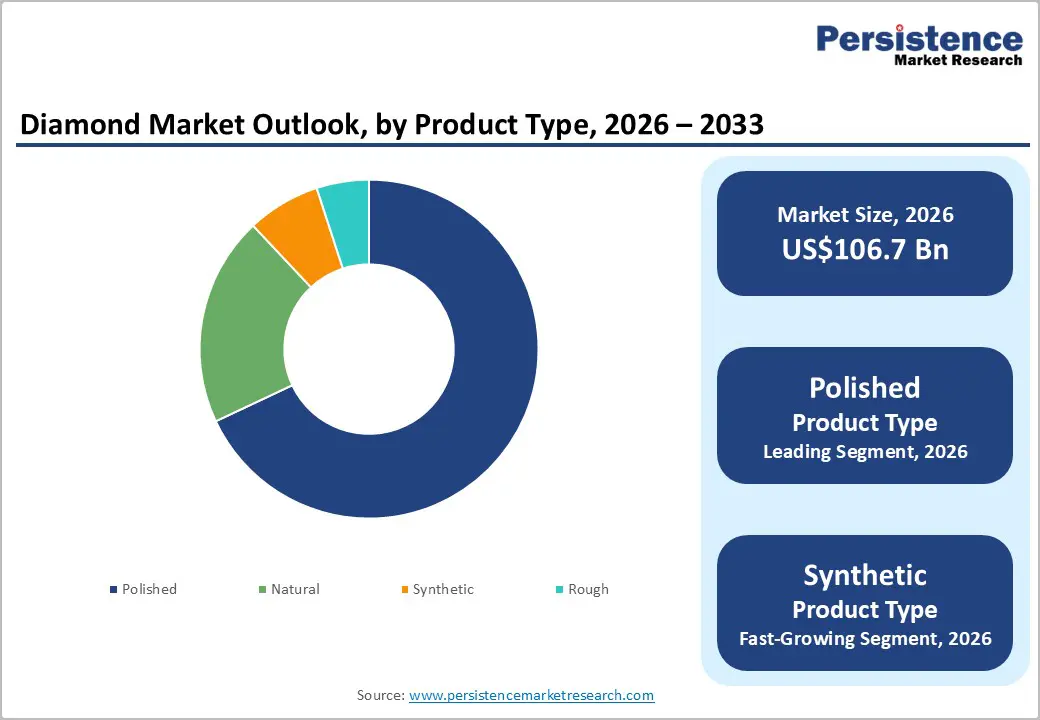

The global diamond market size is likely to be valued at US$106.7 billion in 2026, and is expected to reach US$147.1 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by sustained demand for natural and lab-grown diamonds in luxury jewelry, increasing consumer preference for ethically sourced and affordable synthetics, growing industrial applications in cutting tools, electronics, and quantum technologies, and rising disposable incomes in emerging luxury markets.

Increasing recognition of diamonds as both emotional luxury assets and high-performance industrial materials in emerging bridal, investment, and advanced manufacturing markets remains a major driver of market growth.

Key Industry Highlights:

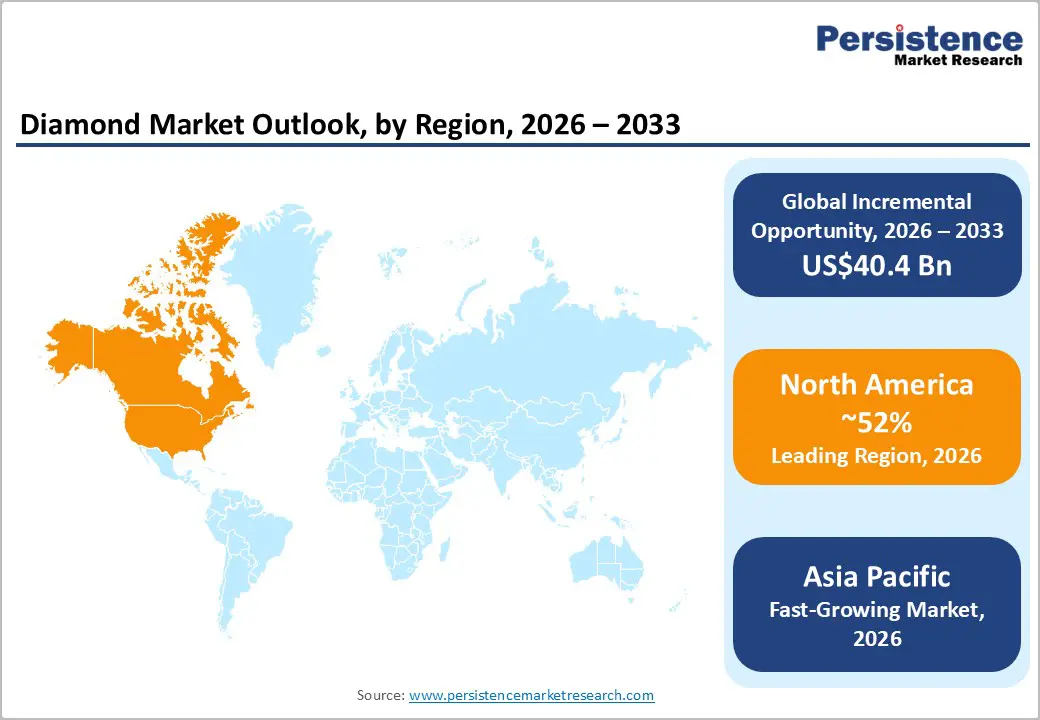

- Leading Region: North America, anticipated to account for a 52% market share in 2026, driven by high demand for engagement rings and wedding jewelry, along with diamonds symbolizing commitment and status, continued to support steady sales.

- Fastest-growing Region: Asia Pacific, fueled by rising middle-class luxury spending, e-commerce penetration, and industrial diamond growth.

- Dominant Product Type: Polished, to hold approximately 68% of the market share, as it remains the primary form for jewelry consumption.

- Leading Application: Jewelry, to contribute nearly 82% of the market revenue, due to dominant bridal and fashion demand.

| Key Insights | Details |

|---|---|

|

Diamond Market Size (2026E) |

US$106.7 Bn |

|

Market Value Forecast (2033F) |

US$147.1 Bn |

|

Projected Growth CAGR (2026-2033) |

4.7% |

|

Historical Market Growth (2020-2025) |

4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Lab-Grown Diamond Acceptance and Jewelry Demand Surge

Rising consumer awareness and shifting preferences toward ethical and sustainable luxury have significantly boosted demand for lab-grown diamonds. Unlike mined diamonds, these stones are produced in controlled environments using advanced technologies such as High Pressure High Temperature (HPHT) and Chemical Vapor Deposition (CVD), ensuring minimal environmental disruption and traceable sourcing. This transparency appeals strongly to younger consumers, particularly millennials and Gen Z, who prioritize sustainability and value-driven purchases.

Affordability has played a crucial role in expanding adoption. Lab-grown diamonds typically cost 30–50% less than natural diamonds of similar quality, enabling consumers to purchase larger or higher-grade stones within the same budget. This price advantage has increased their presence in engagement rings, fashion jewelry, and customized pieces. Retailers and jewelry brands have also accelerated this trend by expanding product lines and promoting lab-grown options alongside natural diamonds. E-commerce platforms and digital marketing have further enhanced visibility and accessibility, allowing consumers to compare quality, certifications, and pricing with ease.

Industrial Diamond Expansion in Electronics & Superabrasives

Growing demand for high-performance materials in advanced manufacturing and electronics has accelerated the use of industrial diamonds. Known for their exceptional hardness, thermal conductivity, and wear resistance, synthetic diamonds are increasingly utilized in cutting, grinding, drilling, and polishing applications. These properties make them essential in producing precision components for industries such as automotive, aerospace, and heavy machinery, where durability and efficiency are critical. In the electronics sector, industrial diamonds are gaining importance due to their superior heat dissipation capabilities. As electronic devices become smaller and more powerful, managing heat effectively has become a key challenge. Diamond-based substrates and heat spreaders help improve device reliability and performance, particularly in semiconductors, power electronics, and high-frequency devices.

The rise of superabrasives has further strengthened demand. Industrial diamonds are widely used in tools designed for machining hard materials such as ceramics, composites, and hardened metals. Their ability to maintain sharpness and reduce tool wear enhances productivity and lowers operational costs in manufacturing processes. Advancements in synthetic diamond production technologies have enabled consistent quality and scalability, making these materials more accessible across industries.

Barrier Analysis – High Production Costs (Natural Diamonds)

Extracting natural diamonds involves complex and capital-intensive processes that significantly raise overall costs. Companies must invest heavily in geological surveys, exploration activities, and the development of mining infrastructure, often in remote or difficult-to-access regions. Establishing and operating a mine requires advanced machinery, skilled labor, and continuous maintenance, all of which add to operational expenses.

Compliance with environmental regulations and responsible mining practices increases financial burdens. Companies are required to manage land rehabilitation, water usage, and emissions, which further elevates costs. Transportation and security also contribute, as diamonds must be safely moved through tightly controlled supply chains. Another challenge lies in the declining availability of high-quality deposits, forcing companies to dig deeper and process larger volumes of ore to extract fewer diamonds.

Environmental and Ethical Concerns

Concerns around sustainability and responsible sourcing have become increasingly influential in shaping consumer attitudes toward diamonds. Traditional mining activities can lead to land degradation, deforestation, and disruption of local ecosystems, raising questions about long-term environmental impact. Water consumption and carbon emissions associated with extraction and processing further contribute to the industry’s environmental footprint.

Ethical issues also play a significant role, particularly those related to labor practices and the historical association with conflict diamonds. Consumers are becoming more conscious about the origins of their purchases and expect transparency across the supply chain. Certifications and traceability initiatives have been introduced to address these concerns, but skepticism still exists among buyers.

Opportunity Analysis – Rising Demand for Customized Jewelry

Technological progress has significantly transformed how diamonds are produced and tracked, improving both accessibility and transparency across the industry. In the lab-grown segment, innovations in High Pressure High Temperature (HPHT) and Chemical Vapor Deposition (CVD) methods have enabled the production of high-quality diamonds with consistent purity, color, and size. These improvements have reduced manufacturing time and costs, making lab-grown diamonds more competitive and widely accepted in both jewelry and industrial applications.

Advancements in traceability solutions have strengthened trust in natural diamonds. Blockchain technology and digital certification systems are being used to record a diamond’s journey from mine to market, ensuring authenticity and ethical sourcing. This level of transparency helps address concerns related to origin, labor practices, and environmental impact. Mining companies and retailers are increasingly adopting these technologies to differentiate their offerings and meet evolving consumer expectations. By combining innovation in production with enhanced traceability, the industry is creating a more accountable and flexible ecosystem.

Traceability and Blockchain Adoption

Improving transparency across the diamond value chain has become a major focus, driving the adoption of advanced tracking technologies. Blockchain systems enable the creation of secure, tamper-proof digital records that document each stage of a diamond’s journey from mining and cutting to polishing and final sale. This ensures that every transaction and ownership change is recorded, making it easier to verify authenticity and origin.

Such traceability helps address long-standing concerns related to unethical sourcing, including the circulation of conflict diamonds. By providing verifiable proof of origin, companies can strengthen consumer trust and meet growing expectations for responsible sourcing. Buyers are increasingly interested in knowing where and how their diamonds were produced, and digital certification tools offer instant access to this information. Blockchain integration streamlines supply chain operations by reducing paperwork, minimizing fraud, and improving coordination among stakeholders.

Category-wise Analysis

Product Type Insights

The polished segment is anticipated to dominate the market, accounting for 68% of the market share in 2026. Strong demand for finished and ready-to-set diamonds continues to drive the dominance of the polished segment. These diamonds are directly used in jewelry manufacturing, making them more commercially valuable than rough stones. Jewelers and retailers prefer polished diamonds due to their immediate usability, consistent grading, and standardized pricing, which simplifies transactions and inventory management.

De Beers entered the polished diamond retail space and invested in grading and assaying facilities in Surat, which is the world’s largest diamond cutting and polishing hub. This move was aimed at capturing more value from finished diamonds rather than relying solely on rough diamond sales.

The synthetic segment represents the fastest-growing product type, and rapid advancements in production technologies have significantly accelerated the growth of synthetic diamonds. Methods such as High Pressure High Temperature (HPHT) and Chemical Vapor Deposition (CVD) enable large-scale manufacturing with consistent quality and faster turnaround times. These diamonds offer similar physical and chemical properties to natural diamonds while being more affordable, making them attractive to a broader consumer base.

Scio Diamond Technology Corporation is a U.S.-based manufacturer that focuses on producing high-quality synthetic diamonds using Chemical Vapor Deposition (CVD) technology. The company specializes in creating near-flawless, gem-quality diamonds as well as materials for industrial applications, demonstrating the versatility and scalability of lab-grown production.

Application Insights

The jewelry is expected to dominate the market, contributing nearly 82% of revenue in 2026. Diamonds are primarily associated with emotional and cultural significance, especially on occasions such as engagements, weddings, and celebrations, which consistently generate high demand. The perception of diamonds as symbols of luxury, status, and long-term value further strengthens their appeal. Continuous innovation in jewelry design, branding, and customization attracts a wider range of consumers across different income groups.

Titan Company Limited, which operates the well-known jewelry brand Tanishq. The company derives a significant portion of its revenue from diamond and gold jewelry, with strong demand driven by weddings, festive occasions, and daily wear collections in India.

The industrial sector represents the fastest-growing application, driven by the rising demand for high-performance materials in manufacturing and technology sectors, which is driving rapid growth in industrial applications of diamonds. Their exceptional hardness, thermal conductivity, and wear resistance make them essential for cutting, grinding, drilling, and polishing tools used in precision industries. As manufacturing processes become more advanced, the need for durable and efficient tooling continues to increase.

Expanding use in electronics, semiconductors, and heat management systems is accelerating adoption. Element Six, which develops industrial-grade synthetic diamonds for advanced manufacturing and electronics applications. The company produces diamond materials used in cutting, grinding, drilling, and polishing tools across industries such as automotive, aerospace, and mining.

Regional Insights

North America Diamond Market Trends

North America is projected to dominate with over 52% share in 2026, driven by strong consumer spending on luxury goods, particularly in the U.S., which remains the largest contributor in the region. Demand is heavily influenced by cultural factors, with engagement rings and wedding jewelry forming a significant portion of total sales. Consumers in the region increasingly view diamonds as symbols of commitment and status, sustaining steady demand for both classic and contemporary designs.

The growing acceptance of lab-grown diamonds, especially among younger buyers who prioritize affordability and sustainability. Retailers are responding by offering both natural and lab-grown options, allowing consumers to choose based on budget and values. Customization and branded jewelry collections are gaining popularity, supported by digital platforms that enable personalized design and seamless online purchasing. Sustainability and ethical sourcing have also become key considerations, pushing companies to adopt transparent supply chains and certification practices.

Europe Diamond Market Trends

Market growth in Europe is shaped by a strong heritage of luxury craftsmanship, evolving consumer preferences, and increasing emphasis on sustainability. Countries such as the U.K., France, and Italy play a significant role due to their well-established jewelry industries and high demand for premium products. Consumers in the region often prioritize quality, design, and brand reputation, supporting steady demand for diamond jewelry.

Growing interest in ethically sourced and traceable diamonds. European buyers are highly conscious of environmental and social impacts, prompting retailers to emphasize transparency, certifications, and responsible sourcing practices. Lab-grown diamonds are also gaining traction, particularly among younger consumers seeking sustainable and cost-effective alternatives. Demand for customized and designer jewelry is rising, driven by fashion trends and the influence of luxury brands. Digital transformation is further reshaping the market, with online platforms and omnichannel strategies improving accessibility and customer engagement.

Asia Pacific Diamond Market Trends

Asia Pacific is likely to be the fastest-growing market for diamonds, driven by rising disposable incomes, urbanization, and increasing affinity for luxury goods. Countries such as India and China are key contributors, supported by large populations and growing middle-class segments. In India, diamonds hold cultural significance, especially during weddings and festive occasions, while in China, changing lifestyles and gifting trends are boosting jewelry demand.

The expanding presence of organized retail and branded jewelry chains is improving consumer trust and product accessibility. Digital platforms and e-commerce are gaining momentum, allowing consumers to explore designs, compare prices, and make informed purchasing decisions. The region also plays a critical role in the global diamond supply chain, particularly in cutting and polishing activities, with India being a major hub. Additionally, lab-grown diamonds are gaining traction due to their affordability and increasing awareness of sustainable options.

Competitive Landscape

The global diamond market is increasingly defined by competition between established mining companies and rapidly growing lab-grown producers. In regions such as Europe and North America, major players like De Beers, ALROSA, and Petra Diamonds maintain strong positions through control over rough diamond supply, established brand heritage, and investments in traceability initiatives. These companies also strengthen their presence in polished diamonds to capture higher margins and align with consumer demand for finished jewelry.

In Asia Pacific, lab-grown diamond manufacturers are expanding rapidly by offering cost-effective and scalable alternatives, making diamonds more accessible to a broader consumer base. The increasing availability of polished diamonds further enhances luxury appeal while reducing ethical concerns associated with sourcing. To stay competitive, companies are adopting strategies such as blockchain-based traceability partnerships, expanding lab-grown portfolios, and repositioning natural diamonds through premium branding.

Key Industry Developments:

- In January 2026, De Beers Group announced a collaboration between its GemFair programme and luxury jewellery brand De Beers London to bring ethically sourced artisanal diamonds to consumers. The initiative aimed to formalize the artisanal and small-scale diamond mining (ASM) sector while showcasing the origin and craftsmanship behind these diamonds.

- In December 2025, Titan Company Limited entered the lab-grown diamond segment with the launch of its new brand, beYon from the House of Titan, and opened its first exclusive store in Mumbai. The company introduced a curated range of lab-grown diamond jewelry, marking its strategic expansion into the emerging category. It is also planned to expand the brand with additional stores in Mumbai and Delhi soon.

Companies Covered in Diamond Market

- Alrosa

- Dominion Diamond Mines

- Petra Diamonds

- De Beers Group

- Debswana

- KIRA DIAM TECH PRIVATE LIMITED

- Henan Huanghe Whirlwind CO., Ltd.

- Sumitomo Electric Industries, Ltd.

- Zhengzhou Sino-Crystal Diamond Co., Ltd.

Frequently Asked Questions

The global diamond market is projected to reach US$106.7 billion in 2026.

The diamond market is primarily driven by the growing acceptance of lab-grown diamonds and increasing demand for jewelry.

The diamond market is poised to witness a CAGR of 4.7% from 2026 to 2033.

Key market opportunities include the rising adoption of lab-grown and traceable natural diamonds, along with expansion in Asia Pacific and growing demand across industrial applications.

De Beers Group, Alrosa, Petra Diamonds, Sumitomo Electric Industries, and Henan Huanghe Whirlwind are the key players.