- Metals & Minerals

- Diamond Powder Market

Diamond Powder Market Size, Share, and Growth Forecast 2026 - 2033

Diamond Powder Market by Product Type (Natural, Synthetic, Monocrystalline Diamond (MDP), Resin Bond Monocrystalline Diamond (RDP), Polycrystalline Diamond (PDP)), Application (Grinding, Lapping and Polishing, Cutting and Sawing, Drilling/Mining, Miscellaneous), Industry, and Regional Analysis, 2026 - 2033

Diamond Powder Market Size and Trend Analysis

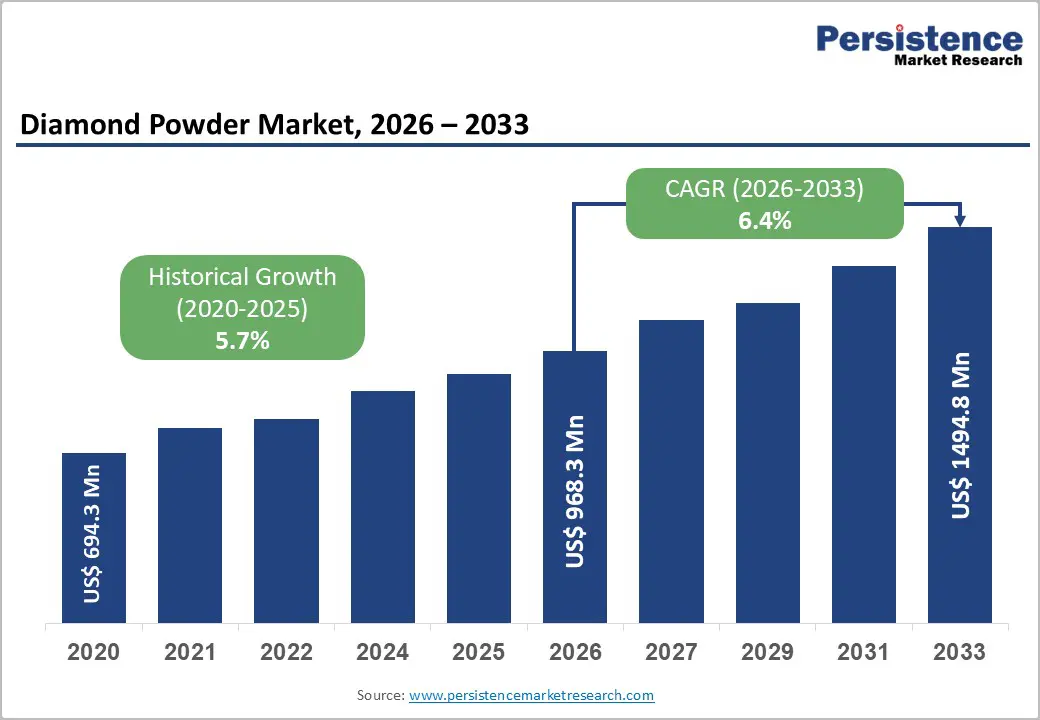

The global diamond powder market size is likely to be valued at US$ 968.3 million in 2026 and is expected to reach US$ 1,494.9 million by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033.

The market is primarily driven by the rise in demand for high-precision finishing materials in the semiconductor and electronics sectors, where diamond powder is critical for wafer polishing and heat dissipation.

Key Industry Highlights:

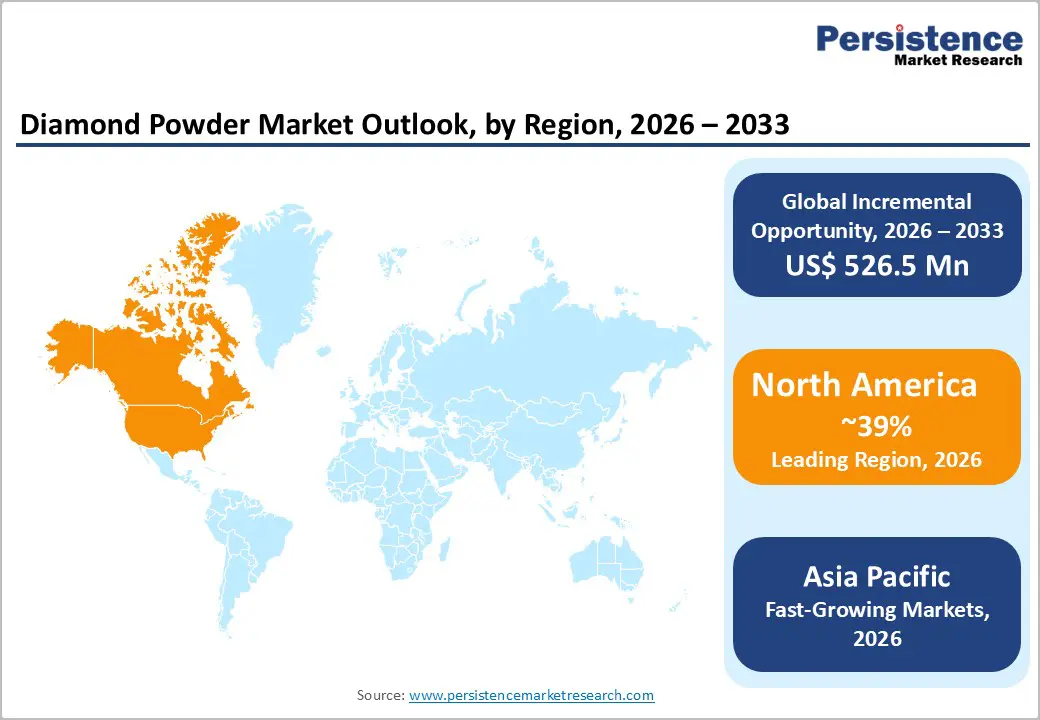

- Leading Region: North America dominates the diamond powder market accounting for 39% share, due to its massive electronics manufacturing base and leadership in synthetic diamond production volume.

- Fastest Growing Region: Asia Pacific is expected to witness the highest growth rate of about 8.5%, fueled by India's industrialization and China's semiconductor self-sufficiency drive.

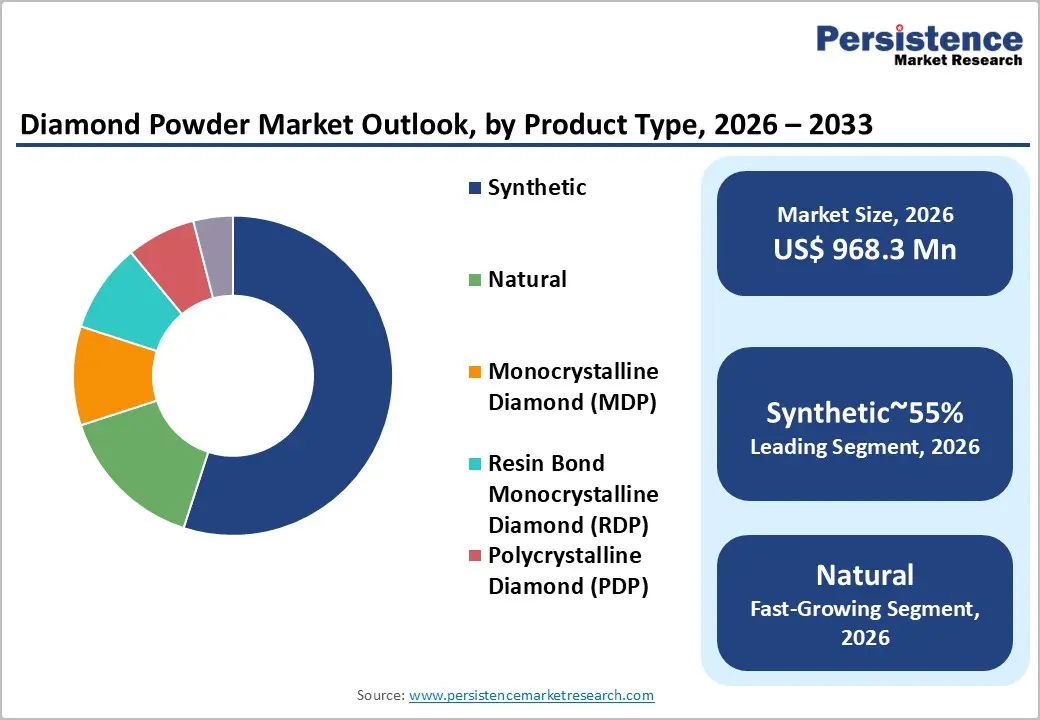

- Dominant Segment: Synthetic Diamond Powder retains the largest market share of approx. 55% share, offering superior consistency and availability for industrial applications compared to natural variants.

- Fastest Growing Segment: Lapping and Polishing applications are projected to grow fastest, driven by the atomic-level finishing requirements of next-gen semiconductors.

- Key Market Opportunity: Thermal Management in high-power electronics presents a critical revenue pocket, leveraging diamond's exceptional thermal conductivity for heat sinks.

| Key Insights | Details |

|---|---|

|

Diamond Powder Market Size (2026E) |

US$ 968.3 Million |

|

Market Value Forecast (2033F) |

US$ 1,494.9 Million |

|

Projected Growth CAGR (2026-2033) |

6.4% |

|

Historical Market Growth (2020-2025) |

5.7% |

Market Dynamics

Drivers - Rising Adoption of 5G, AI, and EV Technologies Drives Strong Demand for Diamond Powders in Advanced Semiconductor Polishing

The rapid expansion of 5G networks, artificial intelligence (AI), and electric vehicles (EVs) has significantly increased the need for advanced semiconductor chips, making this a major growth driver for the diamond powder market. Diamond powder plays a critical role in chemical mechanical planarization (CMP), a process used to polish hard semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN) to extremely smooth, atomic-level surfaces. These materials are essential for high-performance and power-efficient electronic devices.

According to the Semiconductor Industry Association, global semiconductor sales have reached record levels in recent years, directly boosting demand for superabrasive slurries. Diamond particles are preferred because they provide excellent dimensional accuracy, high material removal rates, and effective heat dissipation during polishing. As major semiconductor manufacturing hubs in Taiwan, South Korea, and the United States continue expanding fabrication capacity, sustained demand for high-quality diamond powder is expected to remain strong.

Automotive Shift Toward High-Performance Engines and Electric Vehicles Accelerates Use of Diamond Powders in Precision Machining

The automotive industry’s transition toward high-performance engines and electric powertrains is driving increased use of diamond powder in precision machining applications. Automotive manufacturers rely on Resin Bond Monocrystalline Diamond (RDP) and Polycrystalline Diamond (PDP) abrasives for honing and superfinishing critical engine and transmission components, including camshafts, crankshafts, and gears. These processes help reduce friction, enhance durability, and improve overall energy efficiency.

In electric vehicles, diamond powder is especially important for machining advanced ceramics and composite materials used in motors, batteries, and lightweight structural parts. These materials require highly controlled and aggressive cutting action that conventional abrasives cannot deliver. As automotive OEMs focus on extending component life, improving performance, and meeting stricter emission regulations, the demand for diamond abrasives capable of producing mirror-like surface finishes continues to grow, supporting steady global market expansion.

Restraints - Energy-Intensive Synthetic Diamond Manufacturing Processes Increase Costs and Limit Adoption Across Price-Sensitive End-Use Industries

High production costs and complex manufacturing processes remain a key restraint for the diamond powder market. Producing high-quality synthetic diamond powder requires advanced technologies such as High-Pressure High-Temperature (HPHT) and Chemical Vapor Deposition (CVD), both of which involve substantial capital investment and high energy consumption. These processes are necessary to produce Monocrystalline Diamond Powder (MDP) with consistent quality and performance, but they significantly increase final product prices.

As a result, price-sensitive industries such as basic construction and stone processing often continue using lower-cost alternatives like silicon carbide or aluminum oxide. In addition, fluctuations in raw material prices, particularly graphite, add further uncertainty to production costs and pricing strategies. This combination of high upfront investment, operating expenses, and raw material volatility limits market scalability and discourages smaller manufacturers from expanding production capacity.

Strict Environmental Compliance and Chemical Waste Disposal Regulations Add Operational Costs and Restrict Market Expansion

Environmental regulations pose another major challenge for diamond powder manufacturers, particularly during purification and processing stages. The production of diamond powder often involves chemical treatments using strong acids to remove impurities and achieve high purity levels. Regulatory authorities such as the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) enforce strict rules governing the handling, treatment, and disposal of chemical waste generated during these processes.

To comply, manufacturers must invest heavily in advanced waste treatment systems and environmental management infrastructure, increasing overall operational costs. These regulatory requirements are especially burdensome for small and mid-sized producers, limiting their ability to scale operations or enter highly regulated markets. In regions with strict environmental enforcement, compliance costs can slow capacity expansion and reduce competitiveness, acting as a significant barrier to market growth.

Opportunity - Growing Use of Biocompatible Nanodiamonds in Drug Delivery and Medical Imaging Creates High-Value Market Opportunities

The growing use of diamond nanoparticles in biomedical applications presents a high-value growth opportunity for the market. Nanodiamonds are increasingly used in drug delivery, bio-imaging, and tissue engineering due to their excellent biocompatibility, chemical stability, and non-toxic nature. Surface-modified diamond particles can be engineered to carry therapeutic drugs directly to targeted cells, such as cancer tumors, improving treatment effectiveness while minimizing side effects. Recent scientific studies have also demonstrated the potential of fluorescent nanodiamonds as long-lasting and stable markers for cellular imaging and tracking.

As healthcare and pharmaceutical industries increase investment in nanotechnology-driven therapies, demand for ultra-fine, high-purity diamond powders is expected to rise. Manufacturers that focus on innovation, surface functionalization, and medical-grade diamond formulations can access premium pricing and expand beyond traditional abrasive-based revenue streams.

Rising Heat Challenges in Electronics Boost Demand for Diamond-Based Thermal Management and Cooling Solutions

Rising heat generation in modern electronic devices is creating a strong demand for advanced thermal management solutions, opening new opportunities for diamond powder applications. Diamond has the highest thermal conductivity of any known material, making it an ideal filler for thermal interface materials (TIMs), heat spreaders, and diamond-polymer composites. These materials are increasingly used in high-power electronics, data centers, AI processors, and LED lighting systems, where efficient heat dissipation is critical for performance and reliability.

As computing workloads grow more intensive, especially in AI and cloud infrastructure, traditional cooling materials are reaching their limits. Diamond-enhanced thermal solutions offer superior performance, longer device lifespans, and improved energy efficiency. Manufacturers that develop specialized diamond powder grades optimized for thermal conductivity rather than cutting performance can tap into this fast-growing segment and build partnerships with electronics and thermal solution providers.

Category-wise Analysis

Product Type Insights

Synthetic Diamond Powder dominates the market, accounting for approximately 55% of total demand. Its leadership is driven by consistent availability, controlled quality, and the ability to customize properties such as particle size, shape, and friability. Unlike natural diamond powder, synthetic variants offer uniform performance, which is critical for precision-driven industries. Production methods such as HPHT allow manufacturers to tailor crystal structures for specific applications, including grinding, polishing, and lapping.

This level of control ensures predictable results, higher efficiency, and reduced process variability. Industries such as electronics, aerospace, and optics depend heavily on this consistency, as even minor performance deviations can lead to costly defects. Additionally, synthetic diamonds generally have a more stable cost structure compared to natural diamonds, further supporting their widespread adoption. As demand for precision manufacturing continues to rise, synthetic diamond powder is expected to remain the preferred choice.

Application Insights

Lapping and polishing represent the largest application segment, accounting for an estimated 38% of total market share. This dominance is driven by the growing need for ultra-precision surface finishing in industries such as semiconductors, electronics, and optics. Diamond slurries and pastes are widely used to polish silicon wafers, sapphire substrates, optical lenses, and display glass, where surface smoothness must be controlled at the angstrom level.

No other abrasive material can match diamond’s combination of hardness, cutting efficiency, and surface finish quality on extremely hard materials. The rapid growth of consumer electronics, smartphones, and optoelectronic devices has significantly increased demand for high-performance polishing solutions. As device designs become thinner and more complex, the importance of precise lapping and polishing continues to grow, reinforcing diamond powder’s critical role in advanced manufacturing processes.

Industry Insights

Construction and mining account for approximately 32% of total market volume, making this one of the largest end-use segments. This sector primarily uses coarser diamond powder grades for manufacturing cutting tools such as saw blades, drill bits, and wire saws used in stone, concrete, asphalt, and mineral processing. Rapid urbanization, infrastructure development, and rising demand for natural stone in residential and commercial construction are key factors driving consumption.

Emerging economies, in particular, are investing heavily in roads, buildings, and industrial projects, supporting steady demand for diamond-based tools. While electronics and semiconductors generate higher value per unit, the construction and mining sector consumes significantly larger volumes of diamond powder. This ensures that, despite lower margins, the segment remains a major contributor to overall market demand and production volumes.

Regional Insights

North America Diamond Powder Market Trends

The North American diamond powder market is driven by strong demand from high-tech manufacturing, aerospace, and defense industries. The United States leads the region due to its advanced semiconductor ecosystem and growing investment in domestic chip production. Government initiatives such as the CHIPS and Science Act have accelerated the construction of new wafer fabrication facilities, increasing demand for ultra-fine diamond slurries used in CMP processes.

The aerospace and defense sectors require advanced diamond materials for optical components, sensors, and thermal management systems. The region is also home to leading medical device manufacturers that use biocompatible diamond coatings. Overall, North America focuses more on high-value, specialized diamond powders rather than bulk industrial grades, with innovation, performance, and reliability being key competitive factors.

Europe Diamond Powder Market Trends

Europe’s diamond powder market is strongly influenced by automotive precision engineering and luxury manufacturing. Countries such as Germany and Switzerland are key contributors, driven by the demand for high-performance honing and finishing tools used in automotive engines and transmissions. Germany’s automotive industry, known for strict quality standards, relies heavily on diamond abrasives to improve efficiency and durability.

Switzerland and France also support market growth through luxury watchmaking and jewelry manufacturing, where diamond powders are used to polish sapphire glass and precious metals. A major trend in Europe is the push for sustainable and environmentally friendly manufacturing processes. Regulatory pressure is encouraging producers to adopt cleaner production technologies, while collaborations between research institutions and industry players are fostering innovation, including emerging applications in quantum computing and advanced electronics.

Asia Pacific Diamond Powder Market Trends

Asia Pacific is the largest and fastest-growing regional market for diamond powder, driven by strong manufacturing activity in China and India. China dominates global synthetic diamond production, supplying a significant share of HPHT diamond powder at competitive prices due to large-scale production capabilities. The region’s leadership in consumer electronics manufacturing generates massive demand for diamond powders used in glass, wafer, and component polishing.

India is also expanding its role in diamond processing and industrial manufacturing, supported by government initiatives and skilled labor availability. Additionally, rapid infrastructure development across Southeast Asia is driving demand for construction-grade diamond tools. Favorable factors such as access to raw materials, lower labor costs, and expanding industrial bases position Asia Pacific as both a major production hub and a key consumption center for diamond powder.

Competitive Landscape

The global diamond powder market is moderately fragmented, with a mix of large, vertically integrated players and numerous smaller regional manufacturers. Leading companies such as Hyperion Materials & Technologies and Element Six maintain a strong competitive edge through proprietary high-pressure synthesis technologies that enable precise control over particle size, shape, and consistency. These companies focus on innovation, product differentiation, and close collaboration with end-users.

A key competitive strategy involves developing customized diamond surface treatments to improve dispersion and performance in slurries and composites. Many top players are shifting from selling commodity powders to offering complete abrasive solutions, including tailored slurry formulations and technical support. Meanwhile, Chinese manufacturers compete aggressively on price and scale, rapidly expanding production capacity to dominate standard industrial-grade segments.

Key Market Developments:

- In August 2025, Henan Huanghe Whirlwind and its joint venture introduced four new diamond products, notably ultra-thin diamond heat sinks engineered for advanced 5G/6G and AI chip heat dissipation, reflecting a strategic move into high-end thermal solutions.

- At IMTEX 2025, Engis Corporation showcased its new ElectroMill Diamond Milling Tool, highlighting superior machining of difficult-to-cut materials and reinforcing its leadership in precision superabrasive finishing systems for advanced industrial applications.

- In December 2024, Hyperion Materials & Technologies advanced its investment in the Worthington, Ohio diamond and CBN manufacturing center, expanding the Micron production facility with state-of-the-art cleanrooms, expected to boost electronics market capacity by Q1 2025.

Companies Covered in Diamond Powder Market

- Engis Corporation

- Advanced Abrasives Corporation

- Applied Diamond Inc.

- Henan Huanghe Whirlwind

- Soham Industrial Diamond

- Hyperion Materials & Technologies

- ILJIN Diamond Co., Ltd.

- Zhengzhou Sino-Crystal Diamond Co., Ltd.

- SPEEDFAM

- Logitech Ltd

- PACE Technologies

- GNPGraystar

- Adámas Nanotechnologies

- Zhongnan Diamond Co., Ltd.

- Element Six

- Microdiamant

Frequently Asked Questions

The global market is projected to reach US$ 1,494.9 million by 2033, growing from US$ 968.3 million in 2026.

The surging demand for high-performance semiconductors and the need for precision lapping and polishing in the electronics industry are the primary growth drivers.

Synthetic Diamond Powder is the dominant segment, accounting for the majority of the market share due to its cost-effectiveness and consistent industrial properties.

North America leads the Diamond Powder market with a 39% share, fueled by its extensive electronics manufacturing base and dominance in synthetic diamond production.

The use of diamond powder in thermal management solutions for 5G and AI processors represents a significant high-growth opportunity for market participants.