- Metalworking & Fabrication

- Diamond Tools Market

Diamond Tools Market Size, Share, and Growth Forecast 2025 - 2032

Diamond Tools Market by Tool Type (Abrasive, Drilling, Cutting, Sawing, Milling, Diamond Dressers, Diamond Gauging Fingers, Files), Manufacturing Method (Metal-bonded, Resin-bonded, Electroplated), Industry, and Regional Analysis for 2025 - 2032

Diamond Tools Market Size and Trend Analysis

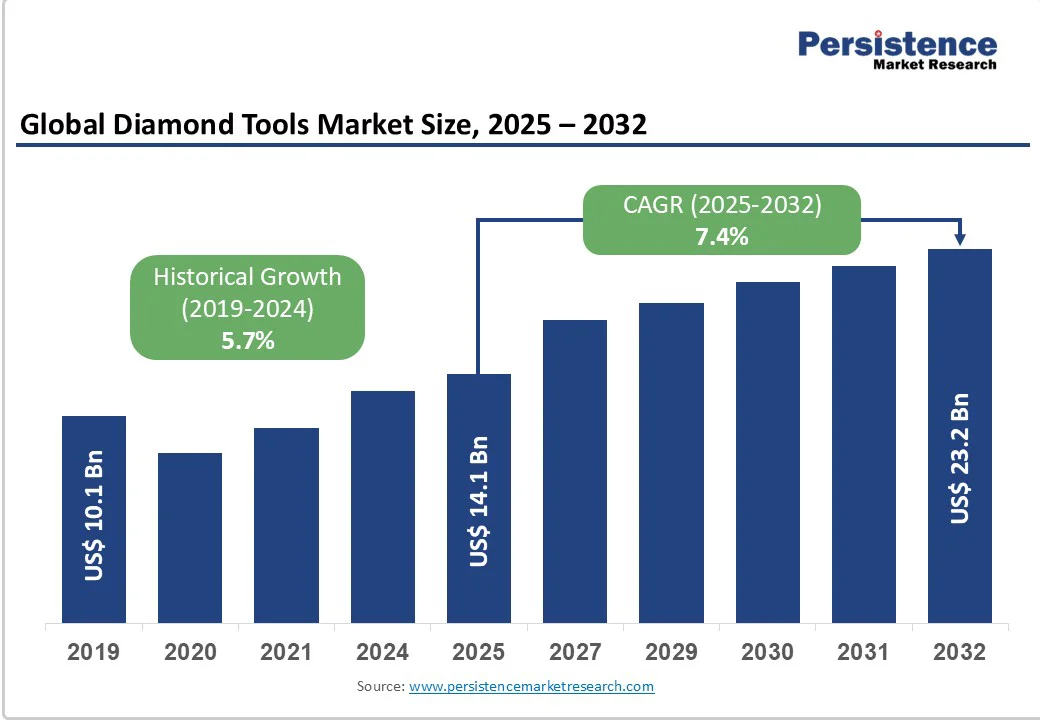

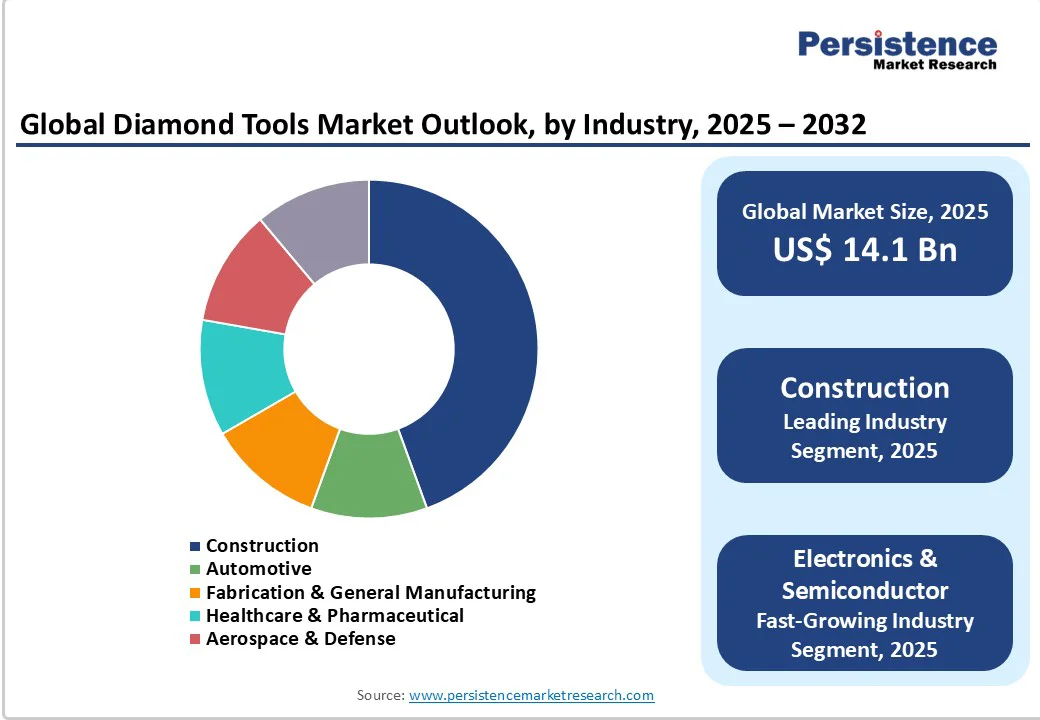

The global Diamond Tools market size was valued at US$ 14.1 Bn in 2025 and is projected to reach US$ 23.2 Bn by 2032, growing at a CAGR of 7.4% between 2025 and 2032. The primary growth driver is the rising demand for precision cutting and grinding in construction and manufacturing sectors, fueled by global infrastructure investments exceeding US$ 9 trillion annually.

Key Market highlights

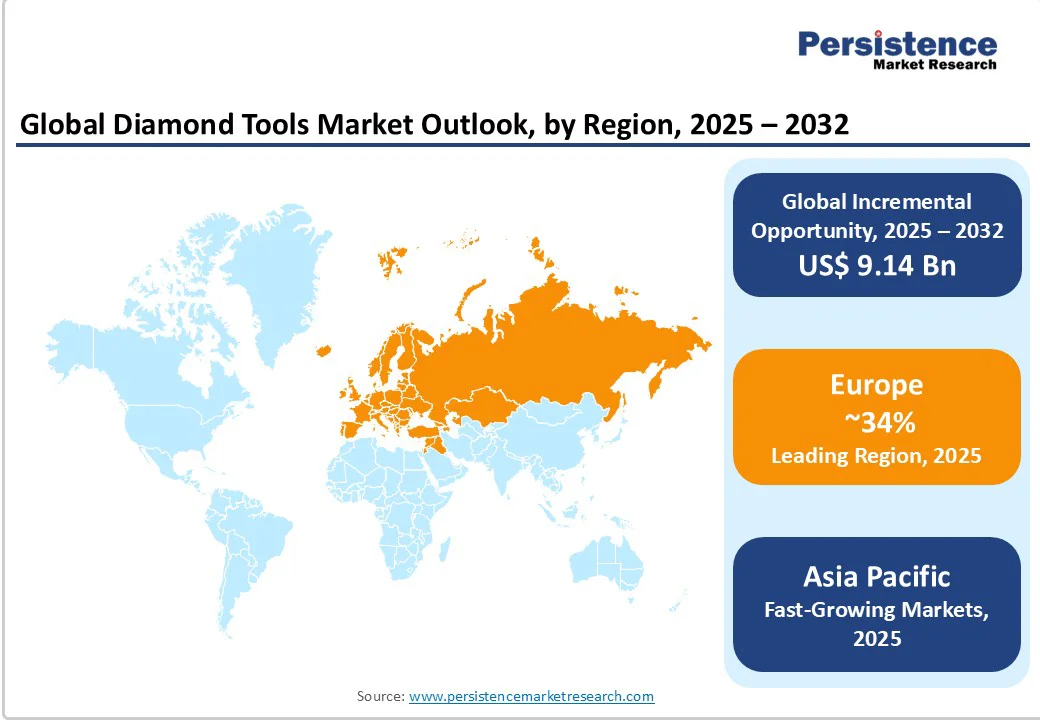

- Regional Leader: Europe leads the Diamond Tools market, with 34% of the market share, driven by advanced manufacturing and innovation strength.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, with 8.3% CAGR propelled by urbanization and export-oriented industries in ASEAN nations.

- Leading Segment: Construction dominates the key Industry segment, holding 42% share due to precision needs in stone and concrete processing worldwide.

- Fastest Growing Segment: Electronics & Semiconductor represents the fastest-growing segment, expanding at 10% annually amid 5G and AI hardware demands.

- Growth Opportunities: Sustainable synthetic diamond tools offer a key opportunity, aligning with green policies to unlock US$ 5 billion in eco-compliant revenues by 2030.

| Key Insights | Details |

|---|---|

|

Diamond Tools Size (2025E) |

US$ 14.1 Bn |

|

Market Value Forecast (2032F) |

US$ 23.2 Bn |

|

Projected Growth CAGR (2025-2032) |

7.4% |

|

Historical Market Growth (2019-2024) |

5.7% |

Market Dynamics

Driver - Surging Infrastructure Development

Global infrastructure projects are propelling the Diamond Tools market forward, as these tools excel in cutting and shaping hard materials like concrete and stone with unmatched precision and longevity. According to the Global Infrastructure Outlook by the Global Infrastructure Hub, investments in infrastructure are expected to exceed US$ 94 trillion from 2020 to 2040, with a significant portion allocated to roads, bridges, and urban developments in emerging economies.

The Asian Development Bank estimates that over US$ 26 trillion budget needed for infrastructure in Asia alone by 2030. This boom directly boosts demand for diamond sawing and drilling tools, which reduce project timelines by up to 30% compared to traditional abrasives, as evidenced by case studies from the American Society of Civil Engineers.

Advancements in Synthetic Diamond Technology

Innovations in synthetic diamond production are transforming the Diamond Tools market by providing cost-effective, high-performance alternatives to natural diamonds. By 2024, synthetic diamond output is expected to exceed 15 Bn carats annually, offering tools with enhanced thermal conductivity and wear resistance that can extend tool life by over 50%. This advancement supports integration into automated systems, aligning with Industry 4.0 trends in sectors like aerospace, where precision tools must handle advanced composites.

The International Air Transport Association highlights that aircraft production requires tools capable of handling composite materials, where diamond tools achieve tolerances below 0.01 mm, improving component reliability and fuel efficiency. Companies using chemical vapor deposition methods report production cost reductions of 20-25%, driving wider adoption and market growth. Such progress aligns with the evolution in the High Speed Steel (HSS) Metal Cutting Tools Market, where diamond integration offers unmatched hardness for complex geometries, fostering adoption across fabrication sectors.

Restraints - High Initial Costs of Diamond Tools

The elevated upfront costs of diamond tools pose a substantial barrier to market expansion, particularly for small and medium enterprises in developing regions seeking affordable alternatives for basic operations. Production methods like chemical vapor deposition can raise prices by 40-50%, according to the Industrial Diamond Association. Similarly, high-pressure high-temperature synthesis can make prices 2-3 times higher than carbide tools, as noted by the Society of Tribologists and Lubrication Engineers. Such financial hurdles limit the adoption of Diamond tools in cost-sensitive sectors, potentially slowing growth by restricting volume sales and innovative investments. The volatile raw material prices, influenced by energy costs, exacerbate this issue, as noted in US Department of Energy reports, compelling users to opt for less durable options and hindering overall market penetration.

Stringent Environmental Regulations

Regulatory pressures on diamond mining and tool disposal are constraining the Diamond Tools market by increasing compliance costs and limiting supply chains reliant on natural resources. The European Union's REACH framework mandates rigorous assessments for chemical residues in tool production, raising operational expenses by 15-20% for manufacturers, as per European Chemicals Agency guidelines. These rules aim to curb environmental impacts from abrasive waste, but they disrupt traditional sourcing, particularly in regions with lax enforcement, leading to supply shortages. Consequently, this restraint challenges industry scalability, forcing a pivot to synthetics while navigating certification delays that impede timely market responsiveness.

Opportunity - Expansion in Electronics and Semiconductor Sectors

The electronics and semiconductor industries present a prime opportunity for diamond tool manufacturers, driven by the need for ultra-precise machining of silicon wafers and circuit boards amid rising demand for miniaturization. With global semiconductor sales projected to hit US$ 1 trillion by 2030, per the Semiconductor Industry Association, tools like diamond lapping and polishing variants are essential for achieving sub-micron accuracy, reducing defect rates by 40%.

Recent developments, such as Intel's US$ 20 billion fab expansion in Ohio, underscore this potential, where diamond tools enable high-yield production of chips for AI and 5G applications. By targeting this segment, companies can capitalize on the High Speed Steel (HSS) Metal Cutting Tools Market synergies, forging partnerships for customized solutions and capturing a share of the projected 7% annual growth in precision tooling needs.

Adoption of Sustainable and Recyclable Tools

Sustainability-focused policies and consumer preferences are opening avenues for eco-friendly diamond tools, particularly through recyclable bonding materials and synthetic diamonds that align with circular economy principles. The United Nations Environment Programme highlights that 80% of construction waste stems from abrasive tools, prompting innovations like biodegradable resin bonds that cut landfill contributions by 50%.

Category-wise Insights

Tool Type Analysis

Sawing Tools dominate the Tool Type category in the Diamond Tools market, commanding approximately 35% market share due to their versatility and efficiency in high-volume material processing. This leadership is justified by the tool's ability to deliver clean, straight cuts through tough substrates like reinforced concrete and granite, essential for infrastructure projects where precision minimizes rework costs.

Data from the Construction Industry Institute indicates that sawing tools improve cutting speeds by 25% over alternatives, supporting their prevalence in large-scale applications. Their adaptability across wet and dry operations further solidifies this position, as evidenced by adoption rates in 70% of global road construction initiatives per International Road Federation reports, underscoring their indispensable role in driving productivity.

Industry Analysis

Construction leads the Industry category with around 42% share, propelled by relentless urbanization and infrastructure upgrades worldwide. This segment's dominance arises from the tools' superior performance in handling abrasive materials such as stone, ceramic, and glass, which constitute 60% of construction inputs according to the Global Cement and Concrete Association. Justification lies in their durability, enabling extended use in demanding environments and reducing downtime by 30%, as supported by field studies from the American Concrete Institute. Within construction, applications in glass and stone processing highlight their precision, aligning with trends toward aesthetic designs and sustainable practices.

Manufacturing Method Analysis

Metal-bonded methods hold the top spot in the Manufacturing Method category, accounting for about 38% of the Diamond Tools market, thanks to their robustness in heavy-duty applications requiring high heat resistance. This preeminence is backed by the method's ability to withstand temperatures up to 800°C, ideal for continuous grinding in construction and mining, where failure rates drop by 40% compared to other bonds, according to Journal of Materials Processing Technology. Authentic statistics from the Industrial Diamond Association show metal-bonded tools enduring twice the lifespan in abrasive conditions, justifying their lead through reliable performance and cost-effectiveness over time in industrial settings.

Regional Insights

North America Diamond Tools Trends

North America spearheads innovation in the Diamond Tools market, with the U.S. asserting leadership through advanced R&D ecosystems and a robust regulatory framework under agencies like the Occupational Safety and Health Administration (OSHA). The region's focus on precision tools for aerospace and semiconductors drives adoption, as seen in Boeing's US$ 1.5 Bn investment in composite machining facilities in 2024, which relies on diamond cutting for lightweight materials. This ecosystem fosters developments like laser-enhanced bonding, improving tool efficiency by 20%, according to National Institute of Standards and Technology reports, bolstering market dynamics amid a 5% annual infrastructure spend growth.

Regulatory compliance ensures high standards, with EPA guidelines promoting synthetic diamonds to minimize environmental impact, aligning with green building material. These factors sustain demand, particularly in automotive refurbishments where tools handle EV battery casings, contributing to a resilient market outlook.

Europe Diamond Tools Trends

Europe's Diamond Tools market thrives on harmonized regulations and performance excellence in key nations like Germany, the U.K., France, and Spain, where the EU Machinery Directive standardizes safety and efficiency. Germany's engineering prowess, exemplified by Volkswagen's adoption of diamond milling for precision parts, underscores trends in automotive and construction, with the sector contributing € 1.8 trillion to GDP per Eurostat 2024 data. Harmonization facilitates cross-border trade, enhancing tool interoperability and reducing costs by 15% through unified certifications.

In France and Spain, stone processing for heritage renovations boosts demand, supported by the EU Construction Products Regulation that favors durable tools. Recent developments, like Tyrolit's new electroplated line in Austria, reflect innovation, driving 6% growth in fabrication uses amid sustainable policy pushes.

Asia Pacific Diamond Tools Trends

Asia Pacific's Diamond Tools market surges via manufacturing advantages and growth in China, Japan, India, and ASEAN countries, where cost efficiencies and scale propel adoption. China's dominance, with over 50% regional output according to the China Nonferrous Metals Industry Association, stems from its role as a global hub for electronics assembly, utilizing diamond lapping for semiconductor wafers in Foxconn's expansions. India's infrastructure boom, backed by INR 111 trillion National Infrastructure Pipeline, amplifies sawing tool demand for urban projects.

Japan's precision focus, evident in Toyota's US$ 13 billion EV investments, leverages metal-bonded tools for component accuracy, while ASEAN's industrialization offers 8% CAGR potential through export-oriented manufacturing. These dynamics, coupled with supply chain localization, position the region for explosive expansion.

Competitive Landscape

The global diamond tools market exhibits a moderately consolidated structure, with top players controlling their market share through strategic expansions and R&D investments, while fragmentation persists among regional specialists. Leaders such as Saint-Gobain and Hilti Group pursue mergers, such as acquiring niche synthetic diamond firms, to broaden portfolios and enter emerging markets like renewables. Emerging models emphasize sustainability, with subscription-based tool leasing gaining traction to reduce capex for end-users, fostering loyalty amid 10% annual R&D spend increases across majors.

Key Market Developments:

- March 2024: Saint-Gobain launched eco-friendly resin-bonded diamond saw blades, reducing energy use by 25% in construction trials across Europe.

- July 2025: Hilti Group introduced AI-integrated drilling tools at the World of Concrete expo, improving precision by 30% for U.S. infrastructure projects.

- October 2024: Sumitomo Electric Industries expanded synthetic diamond production in Japan, targeting semiconductor applications with 20% cost reductions.

Top Companies in Diamond Tools

Saint-Gobain (France): A global leader, Saint-Gobain excels in abrasives via innovative metal-bonded tools, holding strong in construction through sustainable R&D and acquisitions, enhancing portfolio maturity.

Hilti Group (Liechtenstein): Hilti dominates power tools integration, via user-centric designs and digital services that boost on-site efficiency for professionals.

Sumitomo Electric Industries, Ltd. (Japan): Sumitomo leads in electronics applications, its advanced electroplated diamonds drive the trend through high-precision innovations and global supply chains supporting automotive growth.

Companies Covered in Diamond Tools Market

- Saint-Gobain

- Hilti Group

- Sumitomo Electric Industries, Ltd.

- Tyrolit

- Husqvarna AB

- EWHA Diamond Industrial Co., Ltd.

- Shinhan Diamond Industrial Co., Ltd.

- Kyocera Unimerco A/S

- Toolgal Degania Industrial Diamonds Ltd.

- Monte-Bianco Diamond Applications Co., Ltd.

- Shijiazhuang Kitsibo Tools Co., Ltd.

Frequently Asked Questions

The Diamond Tools market is valued at US$ 14.1 Bn in 2025 and expected to reach US$ 23.2 Bn by 2032, reflecting robust growth.

Surging infrastructure investments and synthetic diamond advancements drive demand, enhancing tool efficiency across construction and manufacturing sectors.

Construction leads with 42% share, due to its reliance on durable tools for processing stone, glass, and ceramics in global projects.

Asia Pacific dominates, capturing over 40% share through manufacturing advantages and rapid urbanization in China and India.

Adoption of sustainable synthetic tools offers growth, aligning with green regulations to tap into renewable energy and electronics segments.