- Pharmaceuticals

- Cutaneous Fibrosis Treatment Market

Cutaneous Fibrosis Treatment Market Size, Share and Growth Forecast, 2026 - 2033

Cutaneous Fibrosis Treatment Market by Drug Class (Corticosteroids, Anti-fibrotic Drugs, Immunotherapy), Route of Administration (Oral, Injectable, Topical), Indication (Keloid, Scleroderma, Others), and Regional Analysis for 2026 - 2033

Cutaneous Fibrosis Treatment Market Share and Trends Analysis

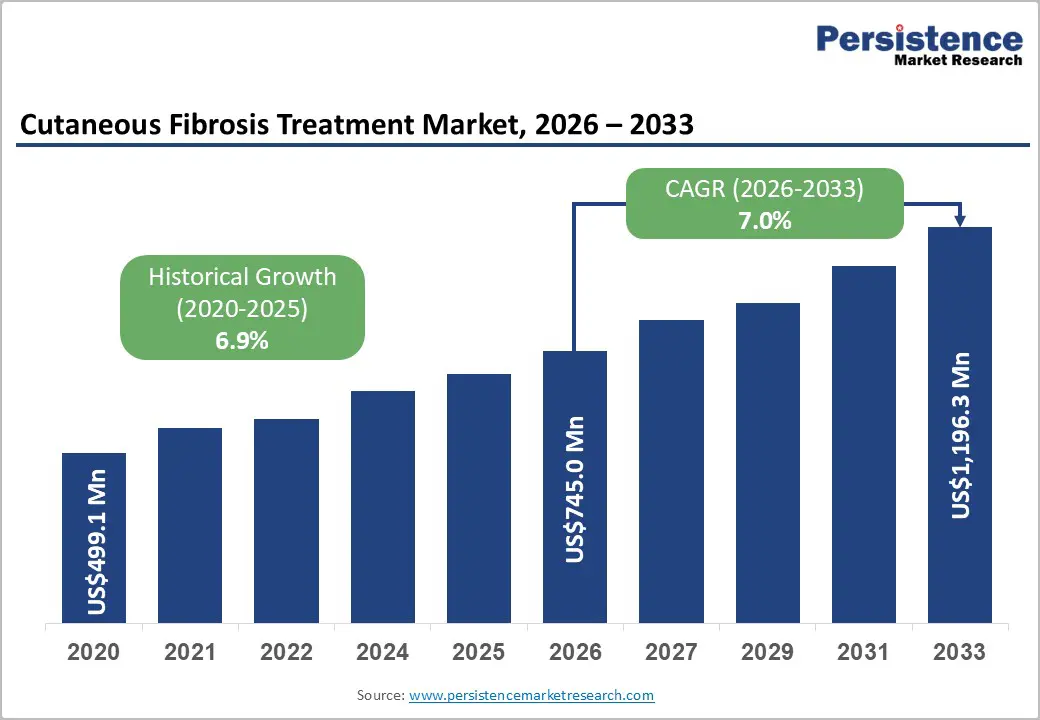

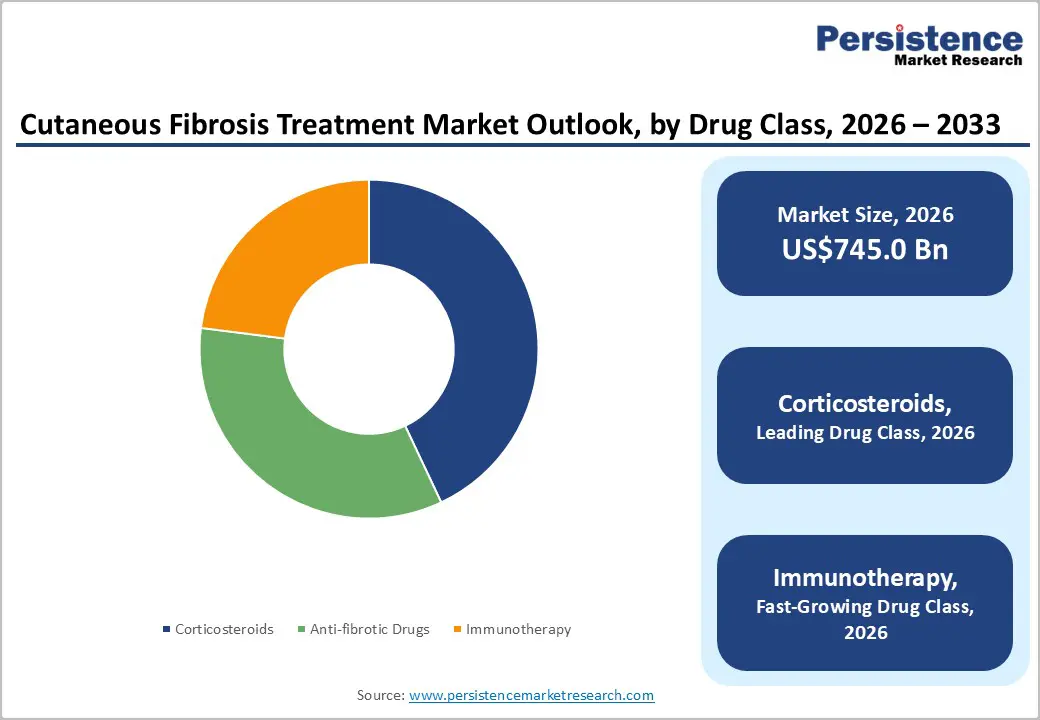

The global cutaneous fibrosis treatment market size is likely to be valued at US$745.0 million in 2026 and is projected to reach US$1,196.3 million by 2033, growing at a CAGR of 7.0% during the forecast period from 2026 to 2033, driven by the increasing incidence of autoimmune skin disorders, rising cancer survivorship linked with radiation-induced fibrosis, and broader adoption of biologic therapies.

Regulatory encouragement for orphan drug development and advances in anti-fibrotic drug development are accelerating clinical innovation. Expanding dermatology infrastructure in Asia Pacific and growing awareness regarding early intervention in fibrotic skin disease treatment are further contributing to market expansion.

Key Industry Highlights:

- Dominant Drug Class: Corticosteroids are set to command nearly 43% of the revenue share in 2026, while immunotherapy is projected to register the fastest growth at an estimated 7.4% CAGR through 2033, driven by increasing biologics adoption and targeted fibrosis therapies.

- Leading Route of Administration: Injectable therapies are anticipated to lead with approximately 46% share in 2026, while topical therapies are likely to be the fastest-growing segment at around 7.8% CAGR during 2026 - 2033, supported by rising demand for non-invasive treatment options.

- Key Indication Segment: Keloid treatment is expected to dominate with nearly 38% share in 2026, while chronic GvHD-associated cutaneous fibrosis is projected to witness the fastest growth at approximately 7.6% CAGR through 2033 due to increasing stem cell transplantation procedures.

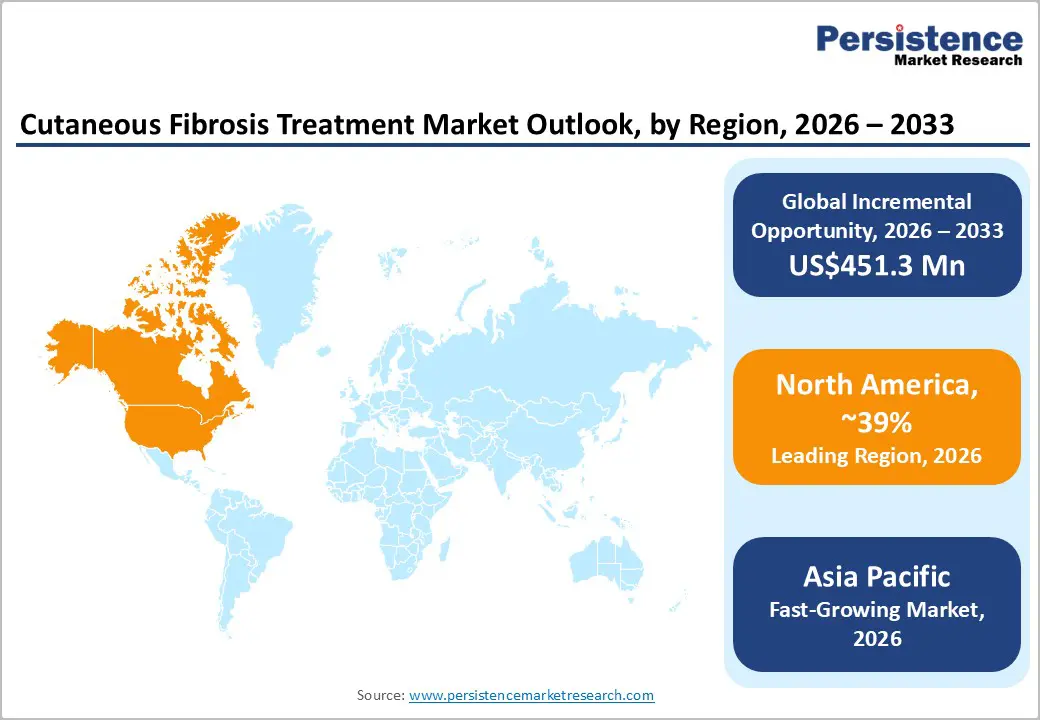

- Regional Leadership: North America is poised to dominate with nearly 39% share in 2026, while Asia Pacific is projected to register the fastest regional growth at an estimated 7.3% CAGR through 2033, supported by expanding biologics manufacturing and healthcare investments.

- Competitive Environment: Competitive dynamics include investments in biologics manufacturing, precision medicine expansion, orphan drug development, and targeted immunotherapy partnerships across emerging and developed markets within the skin fibrosis therapy market.

DRO Analysis

Driver - Rising Prevalence of Autoimmune and Fibrotic Skin Disorders

The increasing burden of scleroderma, keloids, chronic graft-versus-host disease, and radiation-induced fibrosis is driving demand across the dermal fibrosis therapeutics landscape. According to the U.S. National Institutes of Health (NIH), systemic sclerosis affects nearly 75,000 to 100,000 individuals in the U.S., while the European Commission estimates rare connective tissue diseases continue to rise due to improved diagnostic rates. The World Health Organization (WHO) has also reported increasing global cancer survivorship, contributing to a larger patient population vulnerable to post-radiation fibrosis complications.

This expanding disease burden is encouraging pharmaceutical companies to accelerate advanced skin fibrosis drugs research programs and expand biologic therapy pipelines. Hospitals and specialty dermatology clinics are increasingly adopting combination therapies involving corticosteroids, immunotherapy, and anti-fibrotic agents. As treatment awareness improves, particularly in developed healthcare systems, long-term therapeutic demand is expected to strengthen market revenue generation.

Restraint - High Clinical Development Costs and Limited Approved Therapies

The fibrosis biologics market faces significant challenges due to lengthy clinical development timelines, limited regulatory approvals, and high research costs. Fibrosis therapies often require long-term efficacy and safety studies because disease progression is gradual and clinical endpoints are difficult to standardize.

In addition, low patient availability for rare cutaneous fibrosis conditions complicates clinical trial recruitment. High costs associated with injectable biologics and specialty immunotherapies, combined with inconsistent reimbursement policies across Europe and Asia, continue to restrict treatment accessibility and slow the commercialization of emerging therapies.

Opportunity - Expansion of Precision Medicine and Biologic-Based Therapeutics

Growing investment in targeted immunology and biologic therapies is creating significant opportunities across the scleroderma treatment market. The U.S. National Institute of Arthritis and Musculoskeletal and Skin Diseases (NIAMS) has increased funding toward fibrosis-focused translational research programs, while the European Medicines Agency (EMA) continues to support orphan designation pathways for rare dermatologic disorders. Precision medicine approaches focusing on cytokine modulation and fibroblast inhibition are generating new treatment pathways.

Biopharmaceutical companies are increasingly developing monoclonal antibodies, cell-based therapies, and personalized immunotherapies targeting fibrosis signaling mechanisms. These innovations are expected to improve therapeutic outcomes while reducing recurrence rates in chronic fibrosis patients. Emerging economies, particularly China and India, are also expanding biologics manufacturing capacity, creating commercial opportunities for cost-efficient production and wider accessibility within the localized scleroderma treatment segment.

Category-wise Analysis

Drug Class Insights

Corticosteroids are projected to account for nearly 43% of the global revenue share in 2026, driven by strong clinical acceptance, rapid anti-inflammatory action, and cost-effective availability. Intralesional corticosteroid injections remain widely used for keloid and localized fibrosis treatment across dermatology settings. Their leadership is further supported by the growing use of combination therapies with laser-assisted procedures and biologics. In 2026, a Frontiers in Medicine study reaffirmed the long-term effectiveness of glucocorticoid-based fibrosis therapies.

Immunotherapy is anticipated to witness the fastest growth at an estimated 7.4% CAGR during 2026 - 2033, supported by rising investment in biologics and targeted immune-modulating therapies. Pharmaceutical companies are increasingly advancing cytokine inhibitors and fibroblast-targeting treatments to improve long-term fibrosis management. Growth accelerated in 2025 following expanded clinical evaluation of belumosudil for diffuse cutaneous systemic sclerosis. Advancements in CAR-T and monoclonal antibody research are also strengthening the advanced skin fibrosis drugs pipeline.

Route of Administration Insights

Injectable therapies are expected to hold approximately 46% market share in 2026, supported by superior localized drug delivery and faster therapeutic response in fibrosis treatment. Intralesional injections continue to dominate keloid and hypertrophic scar management due to effective suppression of fibroblast activity and collagen production. The segment is also benefiting from the rising adoption of combination injectable protocols across specialty dermatology clinics. In 2025, clinical studies highlighted improved scar reduction outcomes using corticosteroid combinations with 5-fluorouracil.

Topical therapies are projected to register the fastest growth at an estimated 7.8% CAGR through 2033, driven by increasing demand for non-invasive and home-based fibrosis treatment solutions. Expanding use of silicone gels, anti-fibrotic creams, and transdermal formulations is improving patient compliance while reducing systemic side effects. Pharmaceutical companies are increasingly investing in advanced transdermal delivery technologies for localized scar management. In 2025, researchers reported promising results from nanogel-based topical anti-fibrotic formulations targeting fibroblast proliferation pathways.

Indication Insights

Keloid treatment is projected to account for nearly 38% of market revenue in 2026, making it the leading indication segment within the dermal fibrosis therapeutics industry. Rising cosmetic dermatology awareness, increasing scar revision procedures, and high recurrence rates continue to support treatment demand globally. Healthcare providers are increasingly adopting multimodal approaches involving corticosteroids, cryotherapy, and laser-assisted procedures to improve outcomes. In 2025, researchers introduced machine learning-based predictive models for intralesional corticosteroid response in keloid patients.

Chronic GvHD-associated cutaneous fibrosis is expected to witness the fastest growth at an estimated 7.6% CAGR during 2026 - 2033, supported by increasing stem cell transplantation procedures and rising cancer survivorship globally. Growing adoption of biologics and immunosuppressive therapies is improving post-transplant fibrosis management across oncology centers. The segment is also benefiting from stronger collaboration between dermatology and hematology specialists for earlier diagnosis and intervention. In 2025, several North American transplant institutes expanded fibrosis-focused survivorship programs to accelerate targeted therapy adoption.

Regional Insights

North America Cutaneous Fibrosis Treatment Market Trends

North America is projected to account for nearly 39% of the global market share in 2026, supported by strong biologics research, favorable reimbursement systems, and the rising prevalence of autoimmune skin disorders. The region leads in anti-fibrotic drug development due to advanced clinical trial infrastructure and growing adoption of immunotherapy-based fibrosis treatments. FDA support for orphan drug and fast-track approvals continues to strengthen innovation across the market.

U.S. Cutaneous Fibrosis Treatment Market Trends

The U.S. is expected to contribute approximately 71% of the North American market in 2026, driven by high healthcare spending, advanced biotechnology research, and strong specialty dermatology infrastructure. Rising systemic sclerosis and radiation-induced fibrosis cases continue to support demand for advanced skin fibrosis drugs. In 2025, several fibrosis-focused biologic therapies received expanded FDA fast-track review status, reinforcing the country’s leadership in fibrosis treatment innovation.

Canada Cutaneous Fibrosis Treatment Market Trends

Canada is projected to account for nearly 11% of the regional market share in 2026, supported by expanding rare disease funding programs and improved biologics accessibility. The country is witnessing increasing adoption of immunotherapy and corticosteroid combination therapies across hospital-based dermatology care. Growing government investment in precision medicine and autoimmune disease research is further strengthening fibrosis-focused treatment development.

Europe Cutaneous Fibrosis Treatment Market Trends

Europe continues to hold a significant position in the cutaneous fibrosis treatment market, supported by harmonized regulatory policies, strong orphan drug support, and advanced dermatology infrastructure. Rising biologics adoption and expanding research focused on systemic sclerosis and chronic fibrosis conditions are driving regional growth. Increasing collaboration between healthcare systems and specialty dermatology centers is also improving treatment accessibility across the region.

Germany Cutaneous Fibrosis Treatment Market Trends

Germany is expected to account for approximately 26% of the European market in 2026, supported by strong clinical research capabilities and high biologics utilization. The country continues to invest in immunotherapy and precision medicine programs targeting fibrosis-related autoimmune disorders. In 2025, leading German hospitals expanded fibrosis-focused translational research partnerships to accelerate targeted biologic therapy development.

U.K. Cutaneous Fibrosis Treatment Market Trends

The U.K. is projected to hold nearly 18% of the regional market share in 2026, driven by National Health Service support for rare autoimmune disease management and growing biologics adoption. Increasing diagnosis rates and expanding dermatology referral networks continue to strengthen treatment demand. In 2025, several NHS-affiliated hospitals expanded multidisciplinary fibrosis care programs integrating dermatology and immunology expertise.

Asia Pacific Cutaneous Fibrosis Treatment Market Trends

Asia Pacific is projected to register the fastest regional growth through 2033, supported by rising healthcare investments, expanding dermatology awareness, and increasing biologics manufacturing capacity. The region is benefiting from improved healthcare access, growing medical tourism, and stronger adoption of minimally invasive fibrosis therapies. Government support for biotechnology expansion is further accelerating growth across the skin fibrosis therapy market.

China Cutaneous Fibrosis Treatment Market Trends

China is expected to account for nearly 34% of the Asia Pacific market in 2026, driven by expanding domestic biologics production, regulatory reforms, and rising investment in autoimmune disease research. Growing dermatology clinic networks and higher healthcare expenditure are improving fibrosis treatment accessibility. In 2025, Chinese regulators accelerated approval pathways for several locally developed biologic therapies targeting inflammatory skin disorders.

India Cutaneous Fibrosis Treatment Market Trends

India is projected to contribute approximately 16% of the regional market share in 2026, supported by cost-efficient pharmaceutical manufacturing and expanding specialty dermatology infrastructure. Rising medical tourism and increasing awareness regarding scar management are driving demand for injectable corticosteroids and topical fibrosis therapies. In 2025, several Indian pharmaceutical companies expanded biologics production capacity to support growing domestic and export demand for fibrosis treatments.

Competitive Landscape

The global cutaneous fibrosis treatment market is moderately consolidated, with leading companies such as F. Hoffmann-La Roche Ltd., Pfizer Inc., Sanofi S.A., and Novartis AG accounting for a significant share of global revenue. These players are strengthening their market position through biologics development, immunotherapy expansion, and fibrosis-focused clinical research. Strong regulatory expertise and investment in precision medicine remain key competitive advantages.

Meanwhile, emerging biotechnology firms are focusing on niche fibrosis indications such as systemic sclerosis and chronic GvHD-associated cutaneous fibrosis. High clinical development costs, strict regulatory pathways, and biologics manufacturing complexity continue to limit new entrants. However, growing innovation in monoclonal antibodies and fibroblast-targeting therapies is increasing partnership and licensing activity across the skin fibrosis therapy market.

Key Industry Developments:

- In September 2025, Krystal Biotech, Inc. received FDA approval for an expanded VYJUVEK label, improving access and home-based treatment flexibility for dystrophic epidermolysis bullosa patients.

- In January 2025, Boehringer Ingelheim International GmbH expanded its fibrosis research pipeline with additional investment in PDE4B inhibitor programs targeting progressive fibrotic diseases and autoimmune fibrosis conditions.

Companies Covered in Cutaneous Fibrosis Treatment Market

- F. Hoffmann-La Roche Ltd.

- Pfizer Inc.

- Sanofi S.A.

- Novartis AG

- Bristol-Myers Squibb Company

- AbbVie Inc.

- Amgen Inc.

- Johnson & Johnson

- Boehringer Ingelheim International GmbH

- Eli Lilly and Company

- Merck & Co., Inc.

- AstraZeneca plc

- Regeneron Pharmaceuticals, Inc.

- LEO Pharma A/S

Frequently Asked Questions

The global cutaneous fibrosis treatment market is projected to reach US$745.0 million in 2026.

Rising autoimmune skin disorders, increasing cancer survivorship, and growing biologics adoption drive market growth.

The market is expected to grow at a CAGR of 7.0% from 2026 to 2033.

Precision immunotherapy, biologics innovation, and expanding fibrosis care in emerging markets create major growth opportunities.

Key players include F. Hoffmann-La Roche Ltd., Pfizer Inc., Sanofi S.A., and Novartis AG.