- Pharmaceuticals

- Cutaneous and Systemic Leishmaniasis Market

Cutaneous and Systemic Leishmaniasis Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Cutaneous and Systemic Leishmaniasis Market by Drug Class (Pentavalent Antimonials, Antifungal Drugs, Antimicrobial Drugs, and Others), by Route of Administration (Oral, Injectable, and Topical), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Drug Stores, Online Pharmacies), and Regional Analysis from 2025 - 2032

Cutaneous and Systemic Leishmaniasis Market Share and Trends Analysis

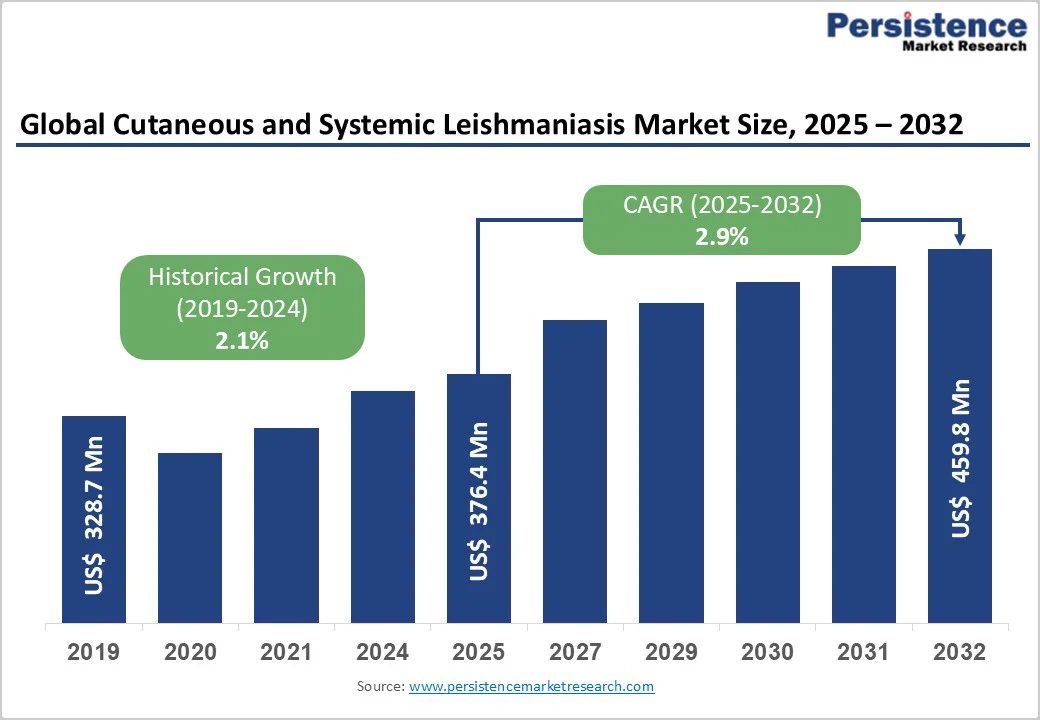

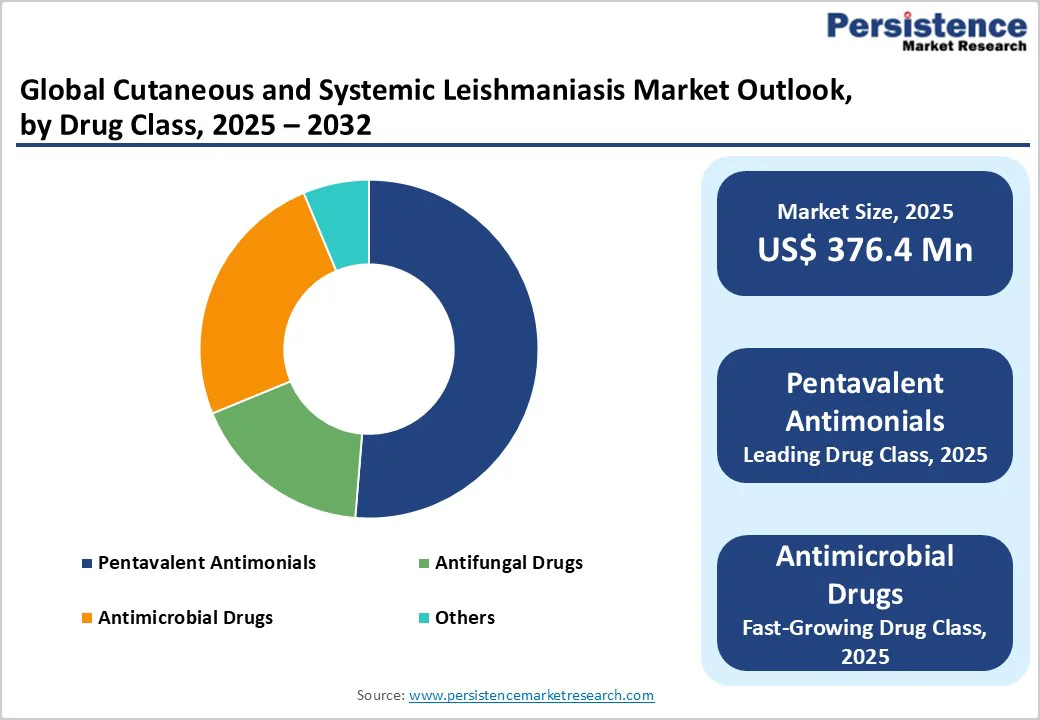

The global cutaneous and systemic leishmaniasis market size is valued at US$376.4 million in 2025 and projected to reach US$459.8 million at a CAGR of 2.9% during the forecast period from 2025 to 2032.

Global demand for treatments for cutaneous and systemic leishmaniasis is rising as endemic countries expand surveillance, early diagnosis, and access to WHO-recommended therapies through hospitals, public health programs, and NGO-supported clinics. Growing focus on patient-friendly, safer, and shorter-course treatment options is accelerating the shift toward oral drugs, combination regimens, and topical formulations.

In addition, increasing R&D investments in novel molecules, vaccine candidates, and parasite-targeted immunotherapies, along with strengthened elimination initiatives, donor funding, and improved drug procurement systems in low- and middle-income regions, are boosting treatment availability and driving market growth.

Key Industry Highlights

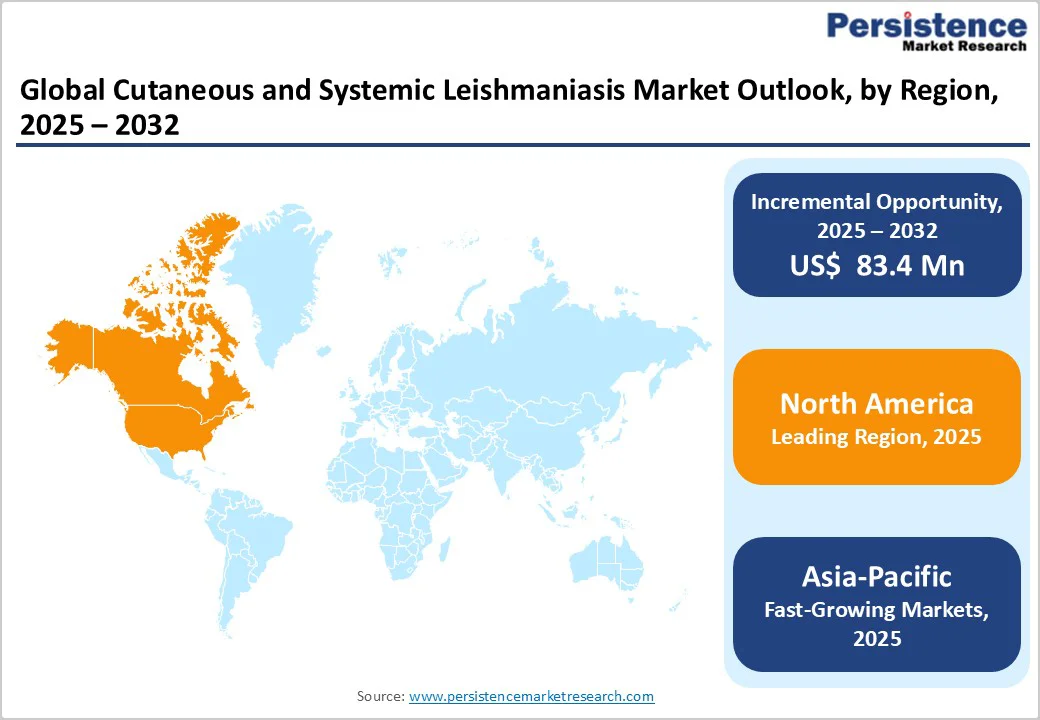

- Leading Region: North America leads globally with 39.4% share, supported by high treatment expenditure, strong R&D funding for neglected tropical diseases, and availability of advanced therapies such as liposomal amphotericin B.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by high disease burden in India, Bangladesh, and Nepal, expanding VL elimination programs, and increasing access to oral and combination therapies.

- Leading Drug Class Category: Pentavalent antimonial dominates with 51.3% share in 2025, due to their long-standing clinical use, wide availability in endemic countries, and inclusion in national treatment guidelines.

- Fastest-Growing Drug Class Category: Oral therapies are gaining rapid traction as safer, more convenient alternatives to injectable regimens, supported by expanding pipeline molecules and increasing adoption of miltefosine.

- Leading Distribution Channel: Hospital pharmacies account for the largest share, as most current treatments and drugs, such as amphotericin B and pentavalent antimonials, require inpatient supervision, cold-chain storage, and specialist monitoring, making hospitals the primary point of access in endemic regions.

- Fastest-Growing Distribution Channel: These channels are expanding rapidly due to mass drug distribution, donor-funded treatment campaigns, and centralized supply systems operated by WHO, MSF, DNDi, and national disease control programs, improving drug reach in rural and low-resource settings.

| Key Insights | Details |

|---|---|

|

Market Size (2025E) |

US$ 376.4 Mn |

|

Market Value Forecast (2032F) |

US$ 459.8 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

2.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.1% |

Market Dynamics

Driver - High Clinical Cure Rate with Combinational Drug Therapy and Increased Investments for Research and Development

A combination of several cutaneous and systemic leishmaniasis drugs has resulted in higher effectiveness rates among several cutaneous and systemic trial groups treated with the combination. Some combinations have also resulted in complete cure of cutaneous and systemic leishmaniasis. In February 2025, an article published in the National Library of Medicine reported 100% lesion resolution in three patients with Cutaneous Leishmaniasis treated with a novel 30-day topical combination (ciprofloxacin + ketoconazole + metronidazole), demonstrating a potential non-systemic, low-toxicity alternative to antimonial injections. Hence, this factor is likely to drive the growth of the cutaneous and systemic leishmaniasis market throughout the forecast period.

Several players in the cutaneous and systemic leishmaniasis markets are substantially investing in research activities to develop novel treatment alternatives. Furthermore, a wide range of drugs and therapies for the treatment of cutaneous and systemic leishmaniasis are currently in clinical trials, with almost all expected outcomes to be favorable. These initiatives are expected to create new opportunities for the treatment of cutaneous and systemic leishmaniasis.

Restraints - High Cost of Treatment and Chances of Side Effects

The treatment of Cutaneous & Systemic Leishmaniasis is very high due to the drugs being very expensive, making them unaffordable for a large share of patients, especially in low-resource and highly endemic countries. The high cost is further driven by limited drug availability, import dependency, and the need for prolonged treatment cycles, resulting in a heavy financial burden on both patients and public health programs. This economic barrier directly affects early diagnosis, timely intervention, and overall disease control efforts.

Moreover, the drugs used for the treatment can also cause serious adverse effects, including organ toxicity, injection site reactions, and long-term complications that require continuous medical supervision. These safety risks often lead to treatment discontinuation, prolonged hospitalization, and reduced patient adherence. As a result, the overall effectiveness of available therapies is compromised, creating a major clinical challenge in managing Cutaneous & Systemic Leishmaniasis.

Opportunity - Favorable Reimbursement Policies and Development of Next-Generation Therapies

Several governments around the globe are investing heavily in healthcare infrastructure, and this is likely to drive the market for cutaneous and systemic leishmaniasis. Apart from this, several private health insurance providers offer reimbursement policies to support the seamless and successful treatment of cutaneous and systemic leishmaniasis. Furthermore, people now have the freedom to choose the reimbursement policy that is most likely to offer the greatest benefits.

The development of next-generation therapies, including oral drugs with fewer side effects and vaccine candidates that eliminate the need for long, toxic, hospital-based injectable treatments, is creating significant market opportunities. Companies introducing shorter, safer, and more tolerable regimens can significantly transform the treatment landscape, especially in endemic regions with limited healthcare access. For example, in April 2024, the WHO reported that LXE408, an oral molecule co-developed by Novartis and DNDi, entered Phase II trials in Ethiopia, where it is being tested in 52 adults alongside standard sodium stibogluconate-paromomycin therapy, aiming to replace painful injections with a more accessible, patient-friendly oral alternative.

Category-wise Analysis

By Drug Class Insights

The pentavalent antimonials segment is projected to lead the global cutaneous and systemic leishmaniasis market, accounting for 51.3% in 2025. The segment’s strong performance is driven by long-established clinical use, broad availability across endemic regions, inclusion in multiple national treatment guidelines, and comparatively lower cost versus newer therapies. Despite increasing interest in liposomal amphotericin B, miltefosine, and emerging oral drugs, pentavalent antimonials continue to dominate due to entrenched procurement systems, widespread physician familiarity, and sustained use in first-line regimens for both cutaneous and visceral forms in low- and middle-income countries.

By Route of Administration Insights

The oral segment is expected to dominate the global cutaneous and systemic leishmaniasis market in 2025, with a 66.7% revenue share. This is due to its superior patient convenience, non-invasive administration, reduced need for hospitalisation, and growing pipeline of next-generation oral candidates aimed at replacing painful injectable regimens. Increasing adoption of drugs like miltefosine, along with the clinical advancement of new oral molecules such as LXE408 and controlled-release combinations, is accelerating the shift toward outpatient, home-based therapy, particularly in resource-limited endemic regions where injectable infrastructure and trained personnel remain scarce.

By Distribution Channel Insights

The hospital pharmacies segment is projected to hold 54.7% of the global cutaneous and systemic leishmaniasis market in 2025 due to their central role in dispensing injectable and inpatient-administered therapies, access to government-funded procurement channels, and ability to manage cold-chain and controlled-drug storage requirements. Since a large share of current treatments, such as pentavalent antimonials and liposomal amphotericin B, require supervised administration, monitoring for toxicity, and specialist consultation, hospitals remain the primary point of care, especially in high-burden countries where community-level distribution of leishmaniasis drugs is still limited.

Regional Insights

North America Cutaneous and Systemic Leishmaniasis Market Trends

The North American market is expected to dominate globally with a value share of 39.4% in 2025, with the U.S. leading the region. This dominance is due to high per-patient treatment expenditure, strong institutional funding from bodies such as the NIH, BARDA, and the Department of Defense, and the wide availability of premium therapies such as liposomal amphotericin B (AmBisome) used for both visceral and cutaneous leishmaniasis cases. The region also benefits from an active clinical research ecosystem, with multiple universities, military research centers, and biotech firms involved in the development of drugs, vaccines, and diagnostics. Supportive regulatory incentives, including orphan drug designation, fast-track approvals, and priority review vouchers, encourage continued industry investment, which drives the regional growth.

Europe Cutaneous and Systemic Leishmaniasis Market Trends

The European market is projected to experience steady growth, due to the increasing incidence of autochthonous cases in Mediterranean countries such as Spain, Italy, and Greece, the strong presence of WHO collaborating centers and DNDi partners, and sustained government funding for neglected disease research. Widespread availability of liposomal amphotericin B through national health systems, combined with rising awareness among clinicians treating refugee, migrant, and immunocompromised populations, supports market expansion. In addition, Europe hosts several ongoing clinical trials for oral and vaccine-based therapies, backed by EU Horizon grants and public–private collaborations, further strengthening long-term market visibility.

Asia and Pacific Cutaneous and Systemic Leishmaniasis Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR between 2025 and 2032, driven by the high disease burden in India, Bangladesh, and Nepal, ongoing WHO elimination programs for visceral leishmaniasis, and expanding access to miltefosine, liposomal amphotericin B, and combination regimens through government-subsidised schemes. Rising R&D collaborations involving Indian pharma, nonprofit organisations, and academic institutes are accelerating the development of affordable oral and vaccine candidates. For instance, in April 2025, researchers from the Indian Institute of Technology BHU (IIT BHU), in collaboration with the Indian Institute of Technology Guwahati, announced the development of dual-target liposomal drugs against Visceral Leishmaniasis (kala-azar), designed to inhibit two key parasite enzymes simultaneously and reduce the risk of drug resistance. Additionally, improved diagnostic penetration, increased vector-control funding, and strengthening of rural healthcare infrastructure are expected to fuel treatment uptake, particularly in endemic pockets of South Asia and emerging hotspots in China and Southeast Asia.

Competitive Landscape

The global cutaneous & systemic leishmaniasis market is highly competitive and consists of significant players. Several market players such as Gilead Sciences, Inc., Profounda Pharmaceuticals, Knight Therapeutics Inc., Janssen Global Services, LLC, Albert David Ltd., Jubilant Life Sciences Ltd., and Novartis AG are implementing new and differentiating strategies to meet product demand and dominate the regional market.

Key Industry Developments:

- In October 2024, Appili Therapeutics announced that it had achieved alignment with the U.S. Food and Drug Administration (FDA) on the development requirements for its lead asset, ATI-1801, a topical antiparasitic formulation targeting cutaneous leishmaniasis, marking a pivotal step toward a potential New Drug Application (NDA) submission.

- In February 2024, Zydus Lifesciences received WHO pre-qualification for the active pharmaceutical ingredient (API) of miltefosine, the only available oral drug for visceral leishmaniasis (kala-azar). This certification is a significant milestone because WHO pre-qualification is a global quality benchmark that allows international procurement agencies, NGOs, and endemic-country health ministries to source the API for large-scale public health programs.

Companies Covered in Cutaneous and Systemic Leishmaniasis Market

- Gilead Sciences, Inc.

- Profounda Pharmaceuticals

- Knight Therapeutics Inc.

- Janssen Global Services, LLC

- Albert David Ltd.

- Jubilant Life Sciences Ltd.

- Novartis AG

- Endo Pharmaceuticals Inc

- Lifecare Innovations Pvt Ltd

- Bristol-Myers Squibb Company

- United Biotech Pvt. Ltd.

- Taj Pharmaceuticals

- Centurion Healthcare Pvt Ltd

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 376.4 Mn in 2025.

Rising disease burden across endemic regions, coupled with ongoing WHO elimination programs, is driving demand for effective leishmaniasis treatments. Additionally, increasing R&D investment in oral drugs, combination therapies, and vaccines are driving cutaneous and systemic leishmaniasis market growth.

The global market is poised to witness a CAGR of 2.9% between 2025 and 2032.

The development of safer, shorter-course oral therapies and first-in-class vaccines that can replace toxic injectable regimens. Growing WHO and nonprofit funding, along with regulatory incentives for neglected disease drugs, also opens doors for new entrants and innovative treatment platforms are creating significant opportunities in the cutaneous and systemic leishmaniasis market.

Gilead Sciences, Inc., Profounda Pharmaceuticals, Knight Therapeutics Inc., Janssen Global Services, LLC, Albert David Ltd., Jubilant Life Sciences Ltd., and Novartis AG are the key players in the cutaneous and systemic leishmaniasis market.