- Automation & Robotics

- Control Flow Choke Market

Control Flow Choke Market Size, Share, and Growth Forecast 2026 - 2033

Control Flow Choke Market by Material Type (Carbon Steel, Stainless Steel, Corrosion-Resistant Alloy, Others), Product Type (Plugs & Cages, Positive Chokes, External Sleeves, Multistage Trims), Operation (Manual, Automatic), Design (In-line Type Body, Y Type Body, Angle Body), Industry (Oil & Gas, Chemical Processing, Power Generation, Paper & Pulp, Food & Beverages, Pharmaceuticals, Others), and Regional Analysis, 2026 - 2033

Control Flow Choke Market Size and Trend Analysis

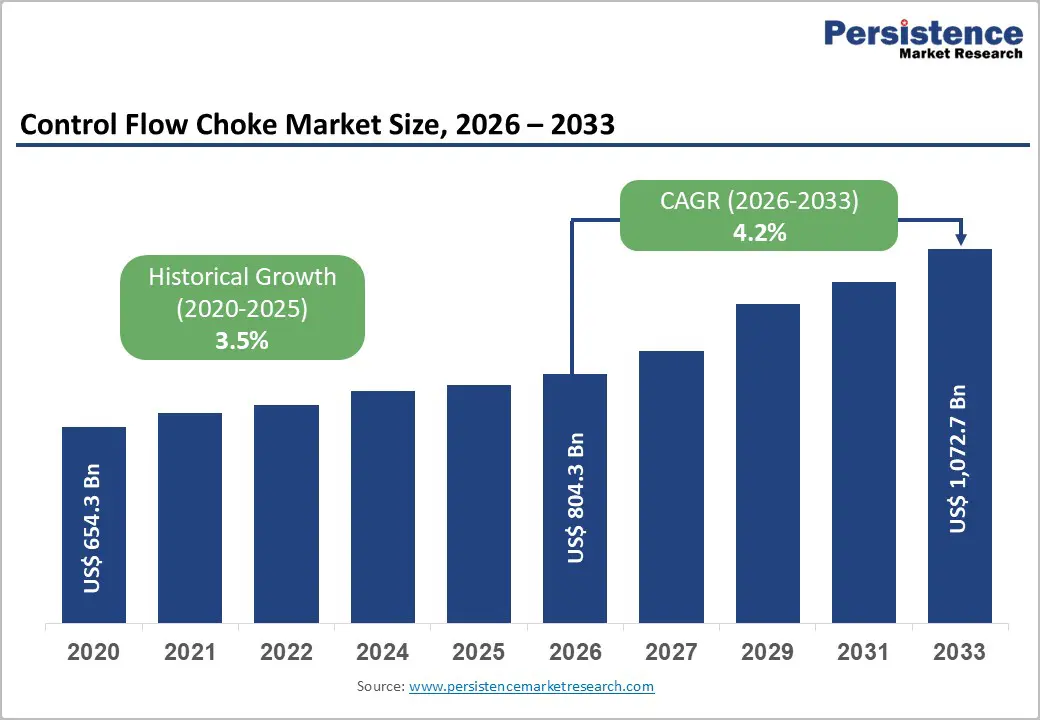

The global control flow choke market size is expected to be valued at US$ 804.3 million in 2026 and projected to reach US$ 1,072.7 million by 2033, growing at a CAGR of 4.2% between 2026 and 2033. From an energy-systems perspective, rising upstream investment and high global production levels create a durable installed base of wells, flowlines, and subsea systems that all require reliable choke and control flow devices.

Global upstream oil & gas investment rose by about 39% in 2022 to roughly US$ 499 billion and is expected to reach around US$ 570 billion in 2024, an increase of about 7% year on year, according to the International Energy Forum (IEF) and International Energy Agency (IEA). At the same time, world crude and condensate production averaged about 81.8 million barrels per day in 2023, with OPEC supplying roughly 35–37% of global crude output, underscoring the continuous need for wellhead and subsea choke valves to manage flow and pressure safely.

Key Industry Highlights

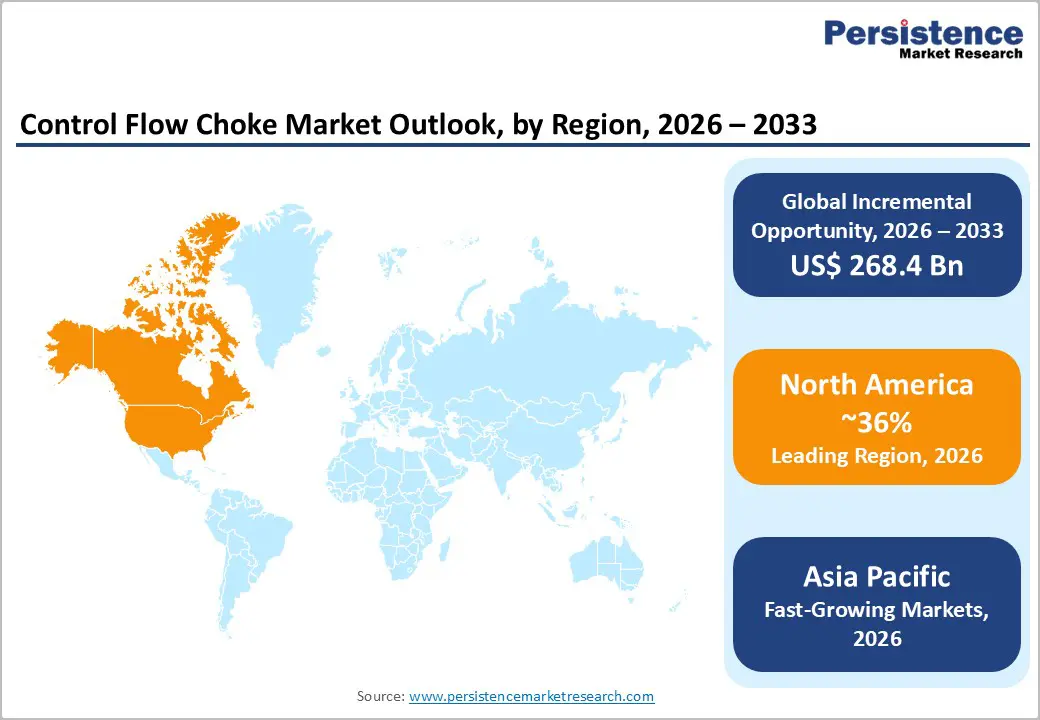

- Leading Region: North America, led by the United States, is expected to remain the largest control-flow choke market, with a 36% market share, supported by record U.S. oil output above 13 million barrels per day, intensive shale and deepwater activity, and strong adoption of digital valve technologies.

- Fastest-Growing Region: Asia Pacific is projected to record the fastest growth through 2033, driven by its roughly one-third share of global refining capacity, the rapid expansion of integrated refinery-petrochemical complexes, and significant investments in LNG and gas infrastructure, which require advanced choke solutions.

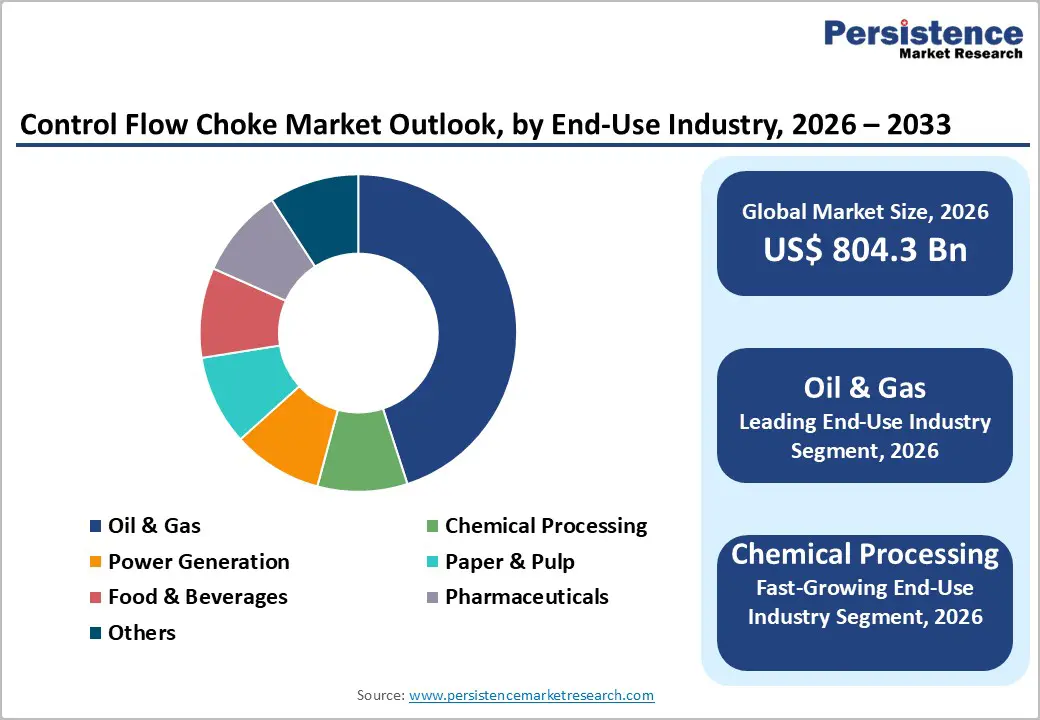

- Dominant Segment: The Oil & Gas segment will continue to dominate demand with 45% market share, as choke valves remain central to production wellheads, subsea manifolds, injection systems, and high-pressure flowlines across conventional, deepwater, and unconventional fields worldwide.

- Fastest-Growing Segment: Automatic chokes and Multistage Trims are poised for the highest growth, supported by the spread of smart valve controllers, remote operations, subsea developments, and high-pressure/sour service applications that demand finely controlled pressure drops and extended service life.

- Key Market Opportunity: Significant opportunity lies in combining corrosion-resistant alloys, duplex stainless steels, and nickel-based CRAs with digital diagnostics and predictive maintenance to reduce downtime and lifecycle costs in severe-service applications such as sour-gas, subsea, CO injection, and petrochemical units.

| Key Insights | Details |

|---|---|

|

Control Flow Choke Market Size (2026E) |

US$ 804.3 million |

|

Market Value Forecast (2033F) |

US$ 1,072.7 million |

|

Projected Growth CAGR (2026–2033) |

4.2% |

|

Historical Market Growth (2020–2025) |

3.5% |

Market Dynamics

Drivers - Heavy Upstream Oil & Gas Activity and Ongoing Service Requirements

The foremost factor driving the control-flow choke market is the sustained need to manage extreme pressures, erosive multiphase flows, and sour service conditions in upstream oil & gas operations. Choke valves are essential at the wellhead for regulating flow and creating controlled pressure drops, enabling safe operation of downstream pipelines, separators, and surface facilities.

Technical literature indicates that choke valves in production wells routinely handle pressure drops up to around 500 bar, operating in environments with sand, corrosive gases such as H-S and CO, and wide flow-rate variability. As global upstream oil & gas capital expenditure climbed to roughly US$ 499 billion in 2022 and is projected to be near US$ 570 billion in 2024, with a substantial share directed to new and existing fields, demand for high-performance production, injection, and subsea chokes is reinforced across all major producing basins.

Digitalization and Remote Operations in Harsh and Remote Assets

The rapid shift toward digitalized, automated, and remotely operated production assets, particularly in offshore and unmanned onshore fields. Modern choke systems increasingly integrate digital valve controllers and smart positioners that provide real-time diagnostics, enabling predictive maintenance and remote tuning of flow conditions. Emerson Electric Co. reports that its Fisher FIELDVUE digital valve controllers have been installed in more than 3 million units and have logged approximately 10 billion hours of operation, underscoring strong adoption of smart valve technologies in severe-service applications, including choke and control valves.

Such devices support higher uptime, tighter process control, and reduced manual intervention in high-risk environments. In subsea fields, Baker Hughes’ subsea choke and integrated process modules combine the choke and flowmeter in a compact assembly that reduces subsea system weight by over 40% and footprint by about 50%, simplifying intervention and lowering life-of-field costs. This convergence of automation, diagnostics, and modular subsea architecture directly stimulates demand for advanced automatic and multistage choke designs.

Restraints - Volatile Hydrocarbon Prices and Capital Discipline

Control-flow choke demand remains closely tied to upstream spending cycles, making the market vulnerable to commodity price volatility and to capital discipline among oil & gas operators. Even as upstream investment rebounded sharply in 2022, the IEF and IEA highlight that annual investment must increase further to about US$ 640 billion by 2030 to align with supply needs, a target that many companies approach cautiously in light of energy-transition uncertainties. Episodes of price weakness or macroeconomic slowdown can quickly defer drilling and completion programs, particularly in high-cost offshore or unconventional plays where severe-service chokes are most heavily specified. This cyclicality can delay choke upgrades and limit near-term replacement orders.

Corrosion, Erosion, and Maintenance Burden in Aggressive Service

Another key restraint is the high maintenance burden associated with choke valves exposed to sand-laden, corrosive, and high-velocity flows. Technical guidance from engineering sources notes that choke valves must often withstand conditions including multiphase flow, high pressure drops, and high solid content, which drive accelerated erosion, vibration, and noise, as well as corrosion from H-S, CO, and chlorides. Without careful material selection and advanced trim designs, operators face frequent shutdowns to rotate or replace chokes, increasing downtime and lifecycle costs. While severe-service solutions exist, such as tungsten-carbide trims and weld-overlayed Inconel internals, they significantly increase initial capital cost, which can deter smaller operators in marginal fields or mature assets.

Opportunity - Advanced Multistage Trims and Corrosion-Resistant Alloys for Harsh Fields

A major opportunity lies in multistage and multipath choke designs that address both erosion and noise while enabling large pressure drops. Severe-service specialists such as IMI Plc (through IMI CCI) have developed production choke valves with multi-stage DRAG trim technology and solid tungsten carbide components, engineered to control kinetic energy and mitigate erosion, vibration, and noise in high-pressure wells. A recent case study on water injection choke valves showed that upgrading to advanced DRAG-based chokes reduced lifecycle costs by up to 40% and extended service life by up to 50%, demonstrating the economic value of premium trims in long-life fields. Parallel advances in corrosion-resistant alloys (CRAs)—such as duplex stainless steels and nickel-based alloys highlighted by the Nickel Institute—support deployment in sour-gas, subsea, and CO-rich environments where failure risk is unacceptable. Together, these technologies position multistage trims and CRA-based chokes as high-growth niches within the broader market.

Asia Pacific Petrochemical, Refining, and Gas Infrastructure Expansion

The Asia-Pacific region presents substantial upside in demand for control-flow chokes as it continues to expand refining, petrochemical, and gas infrastructure. According to refinery capacity assessments from industry and regional agencies, the Asia Pacific accounts for roughly one-third of global oil refining capacity, with global refining capacity at an all-time high of about 103.5 million barrels per day in 2023, and new capacity additions heavily concentrated in Asian economies. The U.S. Energy Information Administration (EIA) reports that crude oil processing in China averaged around 14.8 million barrels per day in 2023, a record level that reflects both domestic fuel demand and petrochemical feedstock needs. Large integrated refinery-petrochemical complexes, as well as growing gas-fired power and LNG infrastructure across China, India, and ASEAN, require robust choke solutions for high-pressure letdown, gas injection, and multiphase flow control. This positions Asia Pacific as the fastest-growing regional market for sophisticated choke and severe-service control solutions over the coming decade.

Category-wise Analysis

Material Type Insights

Within the Material Type segment, Carbon Steel is expected to remain the leading material in 2025, driven by its cost-performance balance and broad applicability in wellhead piping and standard production environments. Industry analyses of oil and gas pipelines and fittings show that carbon steel pipes are widely used due to high tensile strength, pressure resistance, and ease of welding, while typically costing only about 20–40% of equivalent stainless or high-alloy solutions. This makes carbon steel the default choice for conventional onshore wells and many midstream applications where corrosive species are moderate and coatings or inhibitors can manage corrosion risk. Corrosion-resistant alloys and stainless steels, however, are gaining share in sour-gas fields, subsea systems, and aggressive chemical processing where lifecycle cost and reliability outweigh initial price premiums.

Product Type Insights

In the Product Type segment, Plugs & Cages are expected to hold the largest share of the control flow choke market in 2025, reflecting their widespread deployment in production wellheads and choke manifolds. Engineering sources describing choke trim technologies emphasize plug-and-cage designs for high-capacity, controllable throttling, especially in wells with varying drawdown requirements and multiphase flow. These designs enable relatively precise flow regulation via plug travel within a cage, distributing pressure drop and reducing localized wear. Their flexibility across tubing sizes and pressure classes makes them a natural choice for many operators as the “workhorse” adjustable choke. In contrast, Multistage Trims—which split pressure drop across multiple stages or paths—are emerging as the fastest-growing subsegment, as they are increasingly specified in deepwater, high-pressure gas, and high-sand applications where erosion, cavitation, and noise must be tightly controlled to maintain asset integrity over long field lives.

Operation Insights

Under Operation, Manual chokes currently dominate the installed base, given their lower cost, mechanical simplicity, and long history in conventional onshore and early offshore developments. Technical primers on choke valves distinguish non-regulating (manual or on/off) chokes from regulating (automatic) variants, noting that fixed-bean or manually adjustable chokes are widely used on wellhead Christmas trees where operating conditions change slowly or where operators accept periodic manual adjustment. This extensive installed base ensures that manual chokes still account for the largest share of global deployments as of 2025.

However, the Automatic segment—encompassing actuated and digitally controlled chokes integrated with SCADA and distributed control systems—is expanding at a much faster rate. The proliferation of intelligent valve controllers and positioners, such as Emerson’s Fisher FIELDVUE DVC series, which provide continuous diagnostics and remote configuration, is accelerating the shift toward automatic chokes in offshore, subsea, and unmanned onshore fields where remote and precise control is mandatory.

Design Insights

In terms of Design, Angle Body chokes are expected to account for a leading share of the market in 2025, especially in high-pressure production and kill/choke manifold service. Angle-body configurations are favored in many upstream applications because the change in flow direction enables designers to manage velocities, erosion zones, and outlet orientation more effectively, as reflected in common production choke and kill manifold layouts detailed in subsea and surface choke product catalogs. The geometry allows for robust wear-resistant trim packages and facilitates maintenance access while handling solids-laden, multiphase flow.

Are in-line Type Body designs likely to be the fastest-growing design segment- Inline chokes integrate more easily into compact modular skids and subsea process modules where footprint and envelope are constrained, and they align well with integrated flow-management concepts—such as Baker Hughes’ integrated process modules that combine choke and flowmeter functions in a single, streamlined unit to reduce weight and simplify intervention.

Industry Insights

The oil & gas is unequivocally the dominant segment with 45% market share, as choke valves are fundamentally designed around production well, injection well, and high-pressure flowline service. Authoritative engineering references note that choke valves are mainly deployed on production wellheads, Christmas trees, subsea manifolds, and high-pressure flowlines to manage reservoir pressure, control flow rates, and protect downstream equipment. With world oil production averaging over 81 million barrels per day and OPEC and other major producers supplying the majority of volumes, the sector’s dependence on robust choke performance directly translates into market scale.

Looking ahead, Chemical Processing, which includes refining, petrochemicals, and gas processing, is poised to be among the fastest-growing end-use segments. Massive integrated refinery-petrochemical complexes in Asia Pacific, gas-to-chemicals projects, and hydrogen/blue-ammonia chains increasingly demand severe-service flow control and high-alloy chokes for high-pressure letdown, injection, and corrosive media, creating new avenues for growth beyond traditional upstream fields.

Regional Insights

North America Control Flow Choke Market Trends and Insights

North America is expected to remain the leader with 36% share in control flow chokes market, anchored by the United States, which has been the world’s largest oil producer for several consecutive years. According to data compiled from the U.S. Energy Information Administration (EIA), U.S. crude and condensate production has reached record levels, with the country producing over 13 million barrels per day in 2023, and total world oil production heavily concentrated among a handful of large producers. This intense upstream activity in U.S. shale plays, deepwater Gulf of Mexico, and Canadian oil sands supports substantial demand for both wellhead and subsea choke systems, as well as severe-service control valves in associated gas processing and midstream infrastructure.

The region also benefits from a mature regulatory and innovation ecosystem. Safety and environmental regulations enforced by agencies such as the Bureau of Safety and Environmental Enforcement (BSEE) and adherence to API standards drive adoption of high-integrity choke equipment on offshore platforms and subsea trees. On the technology front, North American operators have been early adopters of smart valve controllers, predictive diagnostics, and digital twin applications. Solutions like Fisher FIELDVUE smart positioners and advanced surge-control and anti-surge valve systems are widely used to optimize process reliability and reduce unplanned downtime in gas compression, midstream, and refining applications.

Europe Control Flow Choke Market Trends and Insights

In Europe, the control-flow choke market is shaped by a mix of mature offshore fields, stringent environmental regulations, and accelerated energy-transition policies. The North Sea—particularly Norway and the U.K.—remains a key hub for offshore oil & gas production, requiring high-performance chokes for topside and subsea applications that must withstand corrosive environments, high pressures, and challenging weather conditions. European operators often favor duplex stainless steels and other CRAs for subsea pipelines and topside process equipment, reflecting a strong focus on long-term integrity and reduced maintenance in remote, harsh settings. This, in turn, supports demand for premium CRA-based chokes and multistage severe-service trims.

Regulatory harmonization across the European Union (EU), including pressure equipment, emissions, and safety directives, encourages standardized approaches to valve design, qualification, and lifecycle documentation, benefiting vendors with strong engineering and documentation capabilities. At the same time, Europe’s decarbonization agenda is fostering growth in gas storage, hydrogen pilot projects, and CCUS facilities, many of which will require specialized choke and control solutions for CO-injection, hydrogen service, and high-integrity flow control in underground storage or depleted fields.

Asia Pacific Control Flow Choke Market Trends and Insights

The Asia-Pacific region is expected to be the fastest-growing market for control-flow chokes over 2026–2033, supported by a powerful combination of refining, petrochemical, LNG, and regional upstream developments. Industry and regional statistics indicate that the Asia Pacific accounts for roughly one-third of global refining capacity, ahead of North America and Europe, and global refining capacity reached about 103.5 million barrels per day in 2023, with net capacity additions heavily concentrated in Asian economies. The EIA reports that crude oil processing in China averaged around 14.8 million barrels per day in 2023, a record high driven by both transport fuel and petrochemical feedstock demand. These large refining and petrochemical complexes rely extensively on severe-service choke and control valves for high-pressure letdown, gas and liquid injection, and handling of corrosive or erosive fluids.

In parallel, Asia Pacific is expanding its upstream and gas infrastructure footprint, including offshore developments in China, Malaysia, Indonesia, Australia, and India, as well as onshore unconventional plays and extensive LNG value chains. Regional oil and gas investment reports and government data from countries such as India highlight multi-billion-dollar annual capital expenditures on exploration, field redevelopment, and pipeline networks, all of which utilize chokes for wellhead and pipeline pressure control. As operators in the region pursue higher automation and reliability standards comparable to North American and European peers, adoption of automated chokes, subsea choke modules, and multistage severe-service trims is expected to accelerate.

Competitive Landscape

The global control-flow choke market exhibits a moderately concentrated structure, characterized by large, diversified flow-control suppliers alongside a long tail of specialized manufacturers serving severe-service applications. Market leadership is typically held by multinational engineering groups with broad product portfolios, global service networks, and strong integration capabilities, while smaller players compete through deep application expertise and customization.

Business strategies across the market are increasingly centered on technology differentiation and lifecycle value creation. Vendors prioritize advanced trim and cage designs to manage erosion, cavitation, and noise under high-pressure conditions, supported by the use of corrosion-resistant alloys for extended operating life. Digital monitoring, predictive maintenance, and condition-based diagnostics are being embedded to reduce unplanned downtime and optimize asset performance. Modular and standardized designs—particularly for subsea and offshore environments—are also gaining traction to shorten project timelines and lower installation costs.

Key Developments:

- February 2026 – SLB launched a fully electric Cameron frac fluid delivery system to boost efficiency, reliability, and safety in hydraulic fracturing through electric actuation and digital control.

- January 2025 – InflowControl launched the Gas Autonomous Inflow Control Valve, the world’s first autonomous flow control valve tailored for gas reservoirs to enhance production stability and manage unwanted water breakthrough.

- October 2024 – Valveworks USA acquired Lancaster Flow Automation, adding its innovative choke technology products to expand manufacturing infrastructure and product offerings for oil and gas flow control.

Companies Covered in Control Flow Choke Market

- Schlumberger Limited

- The Weir Group PLC

- National Oilwell Varco, Inc.

- TechnipFMC Plc.

- IMI Plc.

- Nova Inc.

- Emerson Electric Co.

- Baker Hughes Company (BHGE)

- KOSO Kent Introl

- Master Flo Valve Inc.

- Velan Inc.

- Taylor Valve Technology

- CORTEC

- Lancaster Flow Automation, LLC

- Cyclonic Valve Company, Inc.

- Flowserve Corporation

- CIRCOR International, Inc.

- Forum Energy Technologies, Inc.

- SPX FLOW, Inc.

Frequently Asked Questions

The control flow choke market is projected to reach around US$ 804.3 million in 2026, driven by upstream oil & gas investment, refinery expansions, and higher automation.

Demand is driven by rising upstream activity, the need to manage extreme pressure and corrosive conditions, and growing adoption of digital valve control technologies.

North America leads the market, supported by high U.S. oil production, a large installed asset base, and early adoption of advanced flow-control technologies.

Key opportunities lie in advanced trim designs, corrosion-resistant materials, and digital diagnostics for harsh applications such as subsea, sour gas, hydrogen, and CCUS.

Prominent companies include Schlumberger Limited, Baker Hughes Company (BHGE), TechnipFMC Plc., Emerson Electric Co., The Weir Group PLC, IMI Plc., National Oilwell Varco, Inc., Master Flo Valve Inc., etc.