- Marine

- Boat Control Lever Market

Boat Control Lever Market Size, Share, and Growth Forecast, 2026 – 2033

Boat Control Lever Market by Control Type (Mechanical Control Levers, Electronic Control Levers, Joystick-Integrated Control Systems), Vessel Type (Recreational Boats, Commercial Vessels, Military & Defense Vessels), Sales Channel (OEM, Aftermarket), and Regional Analysis for 2026 - 2033

Boat Control Lever Market Share and Trends Analysis

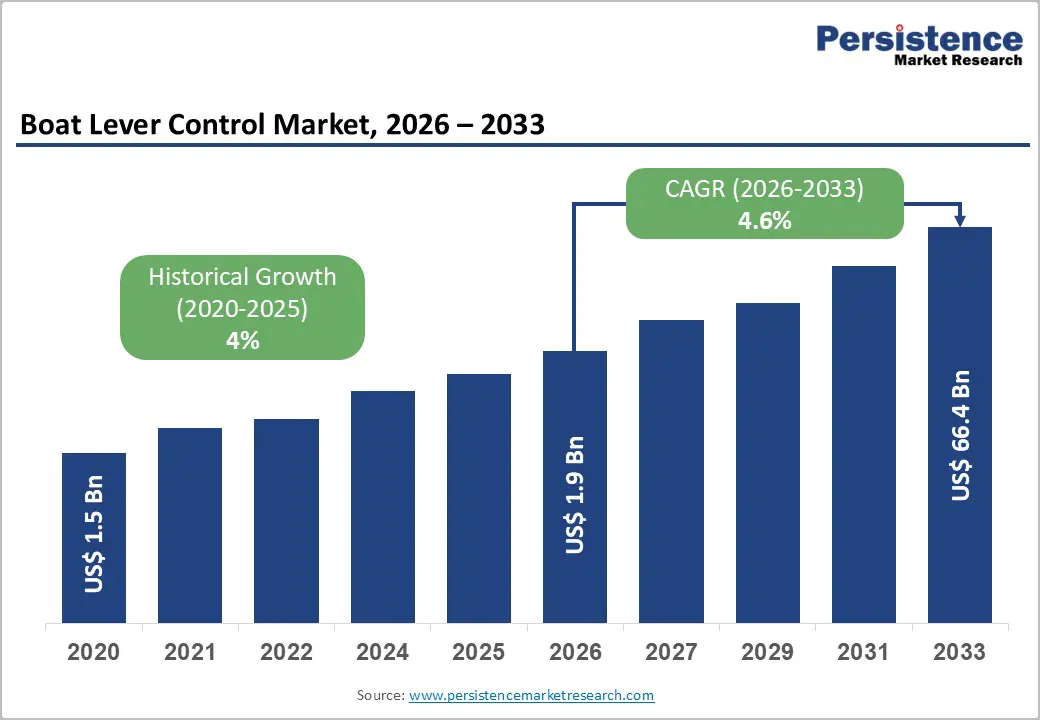

The global boat control lever market size is likely to be valued at US$ 1.9 billion in 2026, and is projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 4.6% during the forecast period 2026-2033.

This robust market growth is driven by escalating demand for advanced marine navigation and propulsion control systems across recreational, commercial, and defense vessels. Increasing marine automation is enabling more precise vessel handling, while rising global boat ownership, particularly in North America and Europe, is fueling new installations and replacements. Fleet modernization programs across commercial and military segments are creating further demand for technologically advanced control levers that integrate seamlessly with engine management and digital navigation systems. Moreover, the adoption of electronic and joystick-integrated systems is transforming operator expectations by improving safety, ergonomics, and maneuverability. Simultaneously, retrofit and aftermarket upgrades are gaining traction as older vessels transition to digital-ready control solutions, expanding the addressable market.

Key Industry Highlights

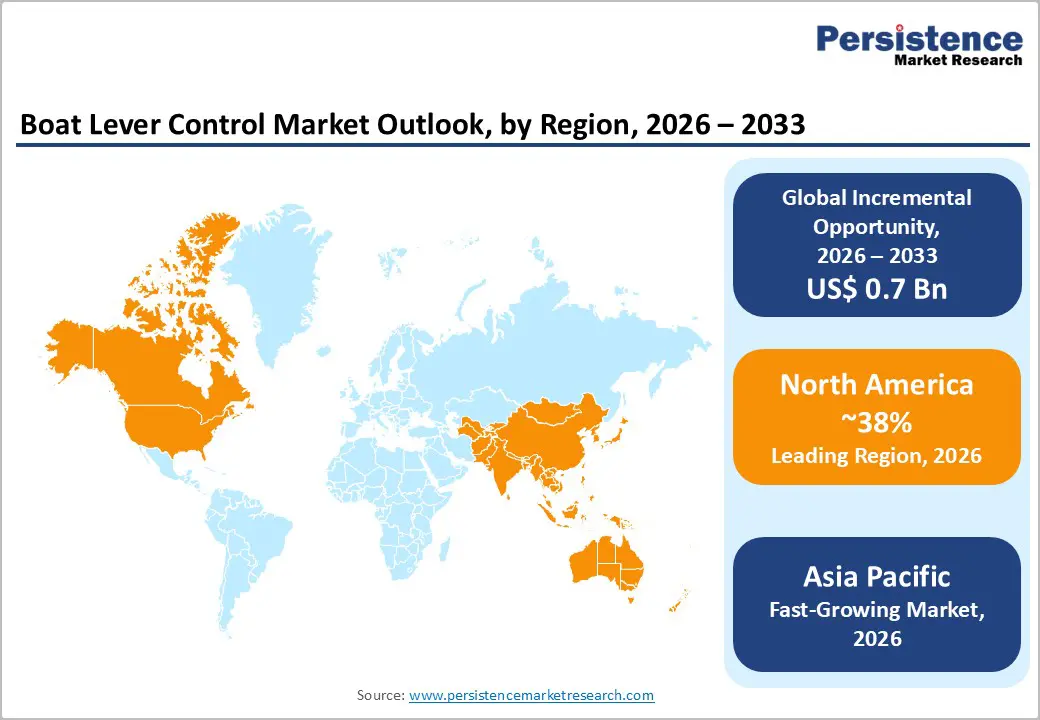

- Regional Leadership: North America is projected to hold around 38% market share in 2026, whereas the Asia Pacific market is likely to grow the fastest at 6.1% CAGR through 2033.

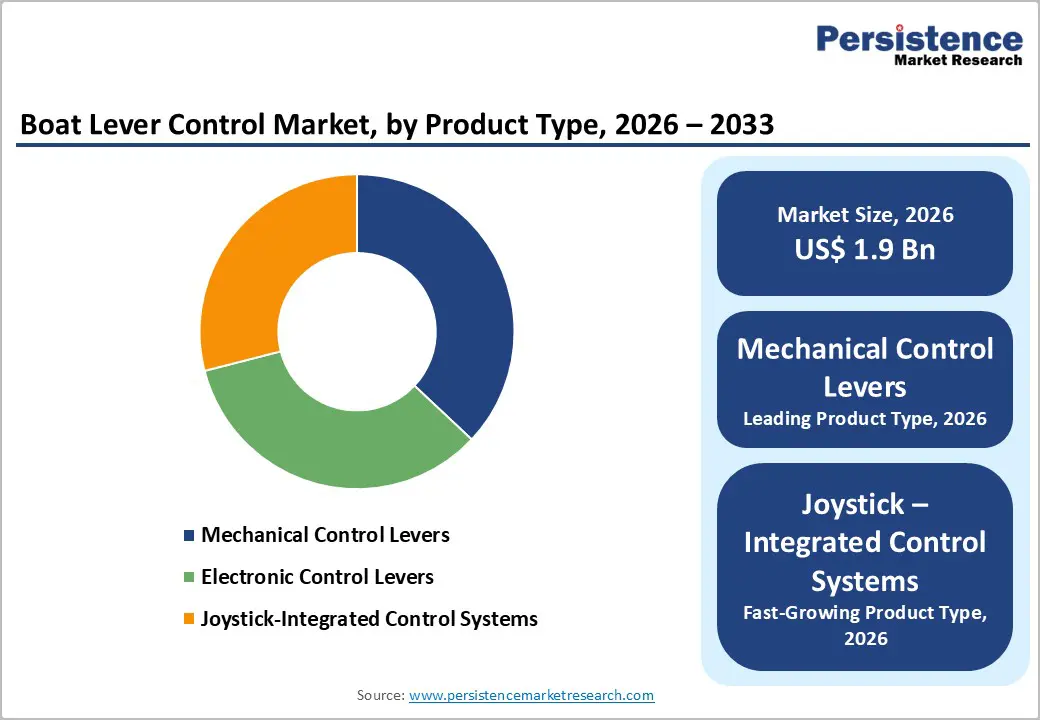

- Dominant Control Types: Mechanical levers are set to command around 45% revenue share in 2026, while joystick systems are likely to grow the fastest at about 4.8% CAGR through 2033, driven by automation and digital integration.

- Leading Vessels: Recreational boats are expected to hold an estimated 52% market share in 2026, with commercial vessels projected to record the highest growth from 2026 to 2033, powered by fleet modernization.

- Primary Sales Channels: Original equipment manufacturers (OEMs) are anticipated to lead with nearly 60% revenue share in 2026, whereas aftermarket channels are poised to display the highest 2026-2033 CAGR, fueled by retrofits and digital upgrades.

- October 2025: Volvo Penta enhanced its Electronic Vessel Control (EVC) system with joystick functionality for V8 single gasoline engines to improve maneuverability, comfort, and control across a wider range of recreational boats.

| Key Insights | Details |

|---|---|

| Boat Control Lever Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Adoption of Electronic and Joystick-Integrated Controls

Advances in marine electronics are driving a shift from traditional mechanical levers to electronic control levers and joystick-integrated systems, offering higher precision, faster response times, and seamless digital interfacing. OEMs are increasingly embedding these systems at production to enhance vessel maneuverability, operational safety, and operator comfort across recreational, commercial, and defense vessels. These modern controls provide real-time feedback, compatibility with navigation platforms, and intuitive handling that reduces operator error. They are particularly valued in congested or coastal environments, where precise docking and low-speed control are critical. By replacing manual systems, electronic and joystick controls also improve reliability and reduce maintenance needs. This technological adoption is accelerating the transition toward fully digitally integrated marine control systems.

The industry trend is reinforced by recent innovations, such as Yamaha’s introduction of the Helm Master® EX Wireless Control System at the Miami International Boat Show, allowing operators to control vessels freely while maintaining precision. Similarly, Mercury Marine expanded joystick piloting functionality to single-engine vessels, bringing advanced maneuvering capabilities to a wider range of boats. These developments illustrate the growing real-world deployment of smart controls beyond luxury yachts, reinforcing demand for digital-ready solutions across all vessel types. As operators increasingly prioritize automation, safety, and digital integration, electronic and joystick systems are positioned to dominate both new installations and aftermarket upgrades.

Growth in Recreational Boating and Fleet Modernization

The rise in recreational boating, supported by higher disposable incomes, tourism growth, and coastal lifestyle trends, is significantly supporting the adoption of advanced boat control levers. Motorboats and yachts are primary beneficiaries, with North America and Europe leading adoption, while Asia Pacific is rapidly catching up. Growing fleet sizes in both leisure and commercial segments directly fuel OEM production cycles and aftermarket sales for upgrades and replacements. Vessel owners increasingly demand smooth, reliable, and ergonomic controls that enhance user experience. Investments in marinas, waterfront infrastructure, and boating facilities are further strengthening the ecosystem for marine technology adoption. These factors combine to sustain demand for both mechanical and digital-ready control solutions.

Fleet modernization and regulatory compliance are adding another layer of growth. For example, the IMO’s updated ECDIS standards, effective January 2026, require enhanced electronic navigation capabilities, while the U.S. Coast Guard’s 2025 cybersecurity rule mandates vessel systems to support digital resilience and monitoring. Smart marine technology was also highlighted at Metstrade 2025, demonstrating industry-wide adoption of digital systems for safety, efficiency, and performance. These developments are encouraging operators to replace older mechanical levers with advanced electronic and joystick systems, driving long-term aftermarket and retrofit opportunities. This ensures continued growth for innovative control solutions across all vessel categories.

High Initial Technology Costs and Integration Complexity

Advanced electronic and joystick-integrated control systems involve significantly higher upfront costs compared to traditional mechanical levers. Expenses include not only hardware but also software integration, calibration, and operator training, particularly when aligning with diverse propulsion systems. Smaller OEMs and aftermarket providers may struggle to absorb these costs, limiting adoption in price-sensitive segments such as small recreational boats or low-margin commercial fleets. Higher procurement costs slow penetration of premium systems and can extend the lifecycle of older mechanical controls in many regions. Even as demand for digital-ready systems grows, adoption may lag among operators who prioritize cost efficiency over advanced functionality.

Integration complexity further adds to barriers. Installing advanced control systems requires expertise, compatibility checks, and technical support to ensure seamless operation with engines and navigation platforms. Misalignment can cause operational inefficiencies or downtime, raising indirect costs. Recent real-world developments illustrate this challenge: in mid-2025, major ports including Rotterdam, Ningbo-Zhoushan, and Cape Town reported vessel delays up to 10 days, with congestion increasing by nearly 300%, disrupting the delivery of electronics and precision components. U.S. container imports declined 6.8% in January 2026 following front-loaded tariff avoidance, introducing additional cost volatility for semiconductors and sensors essential to control systems.

Supply Chain Challenges and Component Scarcity

Manufacturers of marine control levers continue to face persistent supply chain disruptions, particularly for electronics and semiconductor components. Global logistical uncertainties, port congestion, and competition for advanced sensors and digital interfaces have created lead-time volatility that can delay system rollouts, especially during seasonal boating peaks. These disruptions are intensified by trade policy changes and tariffs, which add administrative and cost burdens for importing critical parts. As a result, OEMs and aftermarket suppliers may struggle to maintain inventory levels, limiting responsiveness to market demand and slowing production cycles for advanced systems.

Component scarcity is further compounded by ongoing global pressures. Reports highlight the rising transport costs, material inflation, and procurement delays, with major ports such as Singapore, Rotterdam, and Cape Town experiencing significant congestion. Tariff-related trade adjustments in key manufacturing regions such as ASEAN and India also increased complexity in sourcing semiconductors and digital interfaces. These real-world supply chain constraints amplify the structural challenges of adopting electronic and joystick-integrated levers, making production schedules and inventory management more vulnerable to external shocks. Consequently, even as market demand for advanced controls grows, supply limitations and cost volatility remain critical restraints.

Expansion in Asia Pacific and Latin America Markets

Emerging economies in Asia Pacific (APAC) and Latin America, particularly China, India, and Brazil, offer significant growth potential for the boat control lever market. These regions are seeing rapid maritime infrastructure development, including new ports, marinas, and leisure boating facilities, which supports fleet expansion. Rising disposable incomes and growing middle-class populations are increasing participation in recreational boating, while commercial operators are investing in modern vessels for transport and logistics. Accelerated digital adoption, including electronic and joystick-integrated levers, positions manufacturers to capitalize on this market expansion. OEMs and aftermarket providers can capture new revenue streams as demand for modernized vessel controls rises in these regions.

Recent industry developments reinforce this opportunity. For example, Singapore commissioned its first fully electric harbor tug in early 2026, while India and China expanded hybrid-electric and electrified ferry fleets, reflecting broader electrification adoption in APAC. In Latin America, Brazil’s tourism-driven fleet modernization initiatives are increasing demand for ergonomic and reliable vessel controls. These developments indicate both consumer and commercial willingness to adopt advanced control systems, validating growth prospects for OEM and aftermarket channels across emerging APAC and Latin American markets.

Retrofit and Integration with Electrified Propulsion Systems

Retrofit and aftermarket modernization initiatives continue to create actionable growth opportunities. Operators of aging fleets are increasingly upgrading mechanical levers to electronic and joystick systems to improve fuel efficiency, responsiveness, and compliance with safety regulations. Aftermarket demand is projected to grow at rates exceeding 5% annually, reflecting strong potential for revenue uplift. Retrofitting older vessels reduces environmental impact by optimizing propulsion performance while extending vessel lifespan. These upgrades are relevant for both commercial fleets seeking cost-efficient modernization and recreational owners desiring improved operational experience.

The rise of hybrid and electric marine propulsion further expands this opportunity. Real-world deployments, including New York’s hybrid-electric passenger ferry and the expansion of electric ferry construction in Europe, demonstrate commercial adoption and fleet modernization. Electrified propulsion requires control levers tailored to electric motor torque profiles, regenerative braking, and advanced battery management, creating demand for specialized interfaces. Early adoption enables manufacturers to capture first-mover advantages and supply next-generation vessels. By addressing both retrofit and new electrified vessels, manufacturers can capture multiple revenue streams across OEM and aftermarket channels.

Category-wise Analysis

Control Type Insights

Mechanical control levers are likely to dominate with around 45% market share in 2026 due to their reliability, cost-effectiveness, and simplicity. Widely used in entry-level recreational and many commercial vessels, they sustain a large installed base and strong aftermarket demand. Favored for predictable performance, durability, and easy maintenance, they offer a practical balance of functionality and affordability in price-sensitive regions. Their adoption anchors new builds and retrofits alike. Even as electronic and joystick systems grow, mechanical levers remain essential, with International Maritime Organization (IMO) autonomous shipping regulations emphasizing their foundational role in integrating modern control technologies safely.

Joystick-integrated control systems are anticipated to be the fastest growing segment, projected at 4.8% CAGR during the 2026-2033 forecast period, appealing to operators seeking precision, digital interfacing, and automation in modern yachts, commercial vessels, and defense platforms. They enhance interoperability with navigation, engine management, and safety systems, improving docking and low-speed maneuverability. The 2025 deployment by H-Line Shipping of AI-driven autonomous navigation on 30 commercial vessels validates electronic controls optimizing routes and fuel usage. This demonstrates practical adoption of smarter, digitally managed systems, showing joystick and advanced electronic levers becoming integral to both new vessels and retrofits across applications

Vessel Type Insights

Recreational vessels, including yachts and motorboats, are poised to hold approximately 52% of the boat control lever market revenue share in 2026, driven by leisure boating adoption and premiumization trends. Owners prioritize smooth throttle and gear control, ergonomic design, and digital dashboard integration, fueling demand for both mechanical and advanced control levers. The Incat large electric ship trials in early 2026 illustrate adoption of advanced control systems for maneuvering and energy management, highlighting the sector’s shift toward digital integration. Frequent upgrades, aftermarket retrofits, and the pursuit of intuitive operation and performance ensure recreational vessels remain the backbone of market revenue.

Commercial vessels are slated to exhibit the fastest growth with an estimated 5.5% CAGR through 2033, driven by fleet modernization, safety standards, and complex operational needs. Electronic and joystick systems are increasingly adopted to improve precision, interoperability, and navigational efficiency. Supporting this trend, the government of Andhra Pradesh approved India’s first autonomous maritime shipyard in late 2025, with trial production slated for 2026, focused on unmanned and autonomous maritime platforms. This kind of infrastructure expansion reflects a wider emphasis on next-generation vessels requiring integrated control technologies and digital readiness. Growth is fueled by both new builds and retrofits, as defense and commercial fleets prioritize digitally ready, mission-capable vessel controls for operational efficiency and regulatory compliance.

Regional Insights

North America Boat Control Lever Market Trends

North America is likely to dominate in 2026, accounting for a projected 40% of the boat control lever market share in 2026, driven by the United States’ strong boating culture, advanced maritime OEM infrastructure, and strict regulatory emphasis on safety and emissions compliance. The U.S. reported double-digit recreational boat sales in early 2026, fueling demand for mechanical and electronic control levers in leisure segments. Regulatory pressures, including fuel efficiency guidelines of the U.S. Environmental Protection Agency (EPA) and U.S. Coast Guard equipment mandates, further reinforce adoption of advanced control systems that improve performance, operational safety, and compliance.

Recent developments highlight growth momentum. For example, the most recent report of the National Marine Manufacturers Association (NMMA) confirms sustained recreational boat sales, while VETUS Maxwell’s North American service expansion enhances aftermarket support and OEM integration capabilities. These initiatives enable operators to upgrade fleets confidently and adopt digital and mechanical controls. Canada contributes with growing recreational and commercial marine activity, reinforcing North America’s leadership in both new builds and retrofits. Investment in integrated helm solutions and extended warranties further strengthens the market’s competitive structure and adoption potential.

Europe Boat Control Lever Market Trends

Europe holds a significant share of the global market, with concentrated demand in Germany, the U.K., France, and Spain. The region benefits from a strong cruising culture, extensive commercial shipping activity, and harmonized European Union (EU) maritime safety regulations, driving adoption of mechanical and digital control systems integrated with navigation and emission monitoring technologies. Fleet modernization and leisure boating expansion across Mediterranean and Baltic markets continue to accelerate demand. Regulatory incentives for decarbonization and sustainable operations further stimulate investments in advanced vessel control systems.

Supporting this, the FuelEU Maritime Regulation (effective 2025) mandates decarbonization and zero-emission operations at berth, compelling operators toward digitally enabled, energy-efficient control systems. Additionally, the deployment of electric harbor vessels by Noatum Maritime demonstrates practical adoption of sustainable control technologies. European operators are increasingly investing in ergonomic designs, hybrid propulsion integration, and advanced marine software systems, positioning the region as a hub for innovation, regulatory compliance, and next-generation vessel control solutions.

Asia Pacific Boat Control Lever Market Trends

Asia Pacific is projected to be the fastest-growing regional market for boat control levers, projected to expand at a 4.9% CAGR from 2026 to 2033, driven by rising middle-class incomes, expanding boating culture, and rapid fleet additions in China, Japan, and India. Shipbuilding growth and marine logistics expansion in ASEAN economies boost demand for commercial and defense vessels equipped with advanced control systems. Recreational boating adoption is also increasing, contributing to OEM and aftermarket revenue growth across multiple vessel segments.

In 2025–2026, the Asia Pacific Maritime (APM) 2026 exhibition in Singapore introduced a dedicated Electric & Hybrid Power segment, highlighting innovations in sustainable propulsion and integrated control systems. Coupled with regional government investments in naval and coast guard modernization, these initiatives reinforce electrification and digital integration trends. Smart port strategies and autonomous vessel programs amplify growth opportunities, positioning Asia Pacific as a key investment region for advanced marine controls, while supporting both retrofit and new-build adoption across diverse vessel types.

Competitive Landscape

The global boat control lever market structure is moderately consolidated, with leading vendors such as Rolls-Royce Marine, Vetus, Kongsberg Gruppen, Mercury Marine, and ZF Marine collectively controlling over 50% of total revenue in 2026. These established players leverage their extensive relationships with OEMs and fleet operators, in-depth knowledge of regulatory and safety requirements, and integrated hardware-software control platforms. Heavy investment in R&D allows them to maintain leadership in electronic and joystick control systems, precision navigation integration, and advanced marine automation.

Regional and niche competitors, including Yamaha Marine, H-Line Shipping, and Wärtsilä Marine, focus on specialized vessel segments and specific geographic markets, addressing commercial, defense, and recreational needs. Barriers such as stringent maritime safety regulations, integration complexity, and high technology costs limit new entrants. However, growing digitization and electrification trends enable software-centric providers to participate via retrofit solutions and integration partnerships. Market consolidation is expected to continue gradually as global leaders pursue strategic acquisitions, geographic expansion, and technology partnerships to enhance control system offerings and penetrate emerging markets.

Key Industry Developments

- In January 2026, IES Holdings completed a US$ 192 million acquisition of Gulf Island Fabrication, integrating the 450,000 sq.ft. Houma facility into its Infrastructure Solutions segment. The deal strengthens IES’s fabrication capabilities for custom-engineered products, including generator enclosures, and expands its footprint in the U.S. marine and industrial fabrication sector.

- In January 2026, VETUS launched the E-LINE 22 kW electric inboard motor, delivering zero-emission propulsion, instant torque, and advanced range management for vessels up to 15 m, while offering a compact, modular system that simplifies installation and upgrades. The solution supports the shift toward sustainable boating and compliance with emerging electric-only waterways.

- In September 2025, Electric boat manufacturer Arc partnered with Curtin Maritime to deploy eight hybrid-electric ship-assist tugboats for the Ports of Los Angeles and Long Beach. This project, the largest commercial deployment of electric workboats to date, features 6 MWh batteries and over 4,000 horsepower per vessel, advancing zero-emission port operations.

Companies Covered in Boat Control Lever Market

- SeaStar Solutions

- Yamaha Motor Co., Ltd.

- Mercury Marine

- Volvo Penta

- ZF Friedrichshafen

- Twin Disc, Inc.

- Dometic Group

- Uflex USA

- Glendinning Products

- Vetus B.V.

- Kobelt Manufacturing Co.

- Maretron

- Teleflex

- Honda Marine

- Ultraflex Group

Frequently Asked Questions

The market is experiencing growth due to the increasing demand for precision marine control systems, advancements in electronic throttle and shift (ETS) technologies, and a rising focus on enhancing boating safety.

The shift towards digital control systems offers benefits such as improved responsiveness, fuel efficiency, and integration with electronic navigation, contributing to the market's evolution.

Ongoing material advancements, such as the use of lightweight and corrosion-resistant materials like composites and alloys, are enhancing the durability and performance of boat control levers in diverse marine environments.

Stringent regulations related to emissions, safety, and fuel efficiency are driving manufacturers to develop compliant control systems, fostering innovation, and shaping the competitive landscape of the global boat control lever market.

Growing consumer preferences for customizable and ergonomic designs, coupled with the integration of user-friendly features like joystick controls and wireless connectivity, are influencing the design and functionality of boat control levers in the global market.