- Metals & Minerals

- Cobalt Sulfate Market

Cobalt Sulfate Market Size, Share, and Growth Forecast 2025 - 2032

Cobalt Sulfate Market By Grade (Battery, Industrial, Agricultural), Application (Batteries, Metal Finishing, Agriculture, Inks & Pigments, Chemicals, Other), and Regional Analysis for 2025 - 2032

Cobalt Sulfate Market Size and Trends Analysis

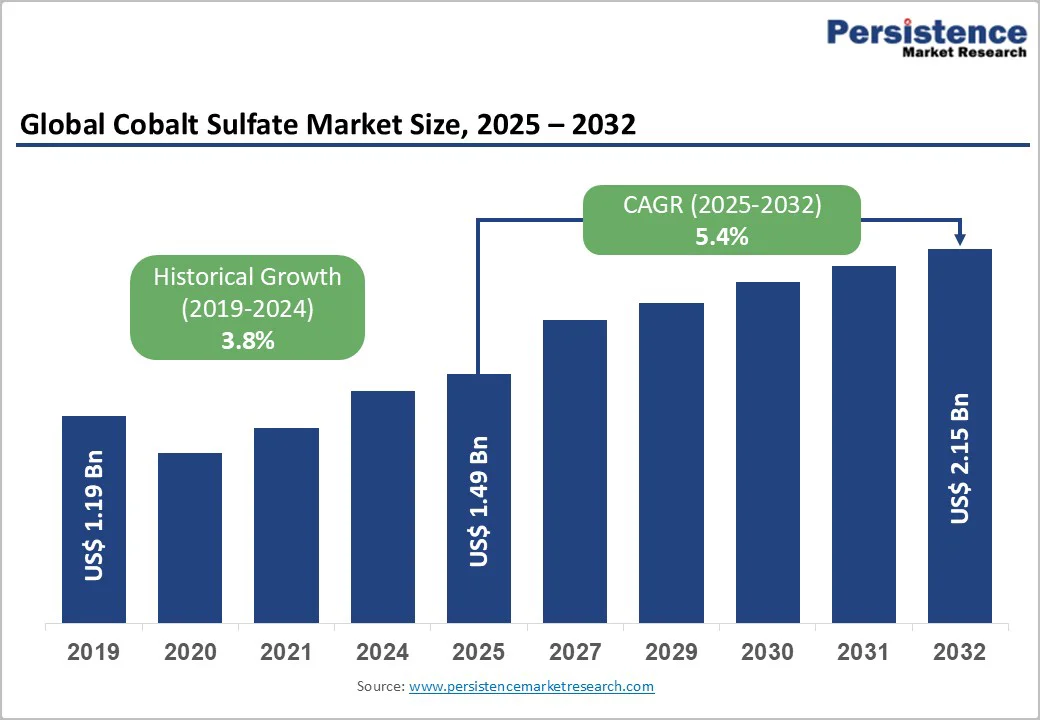

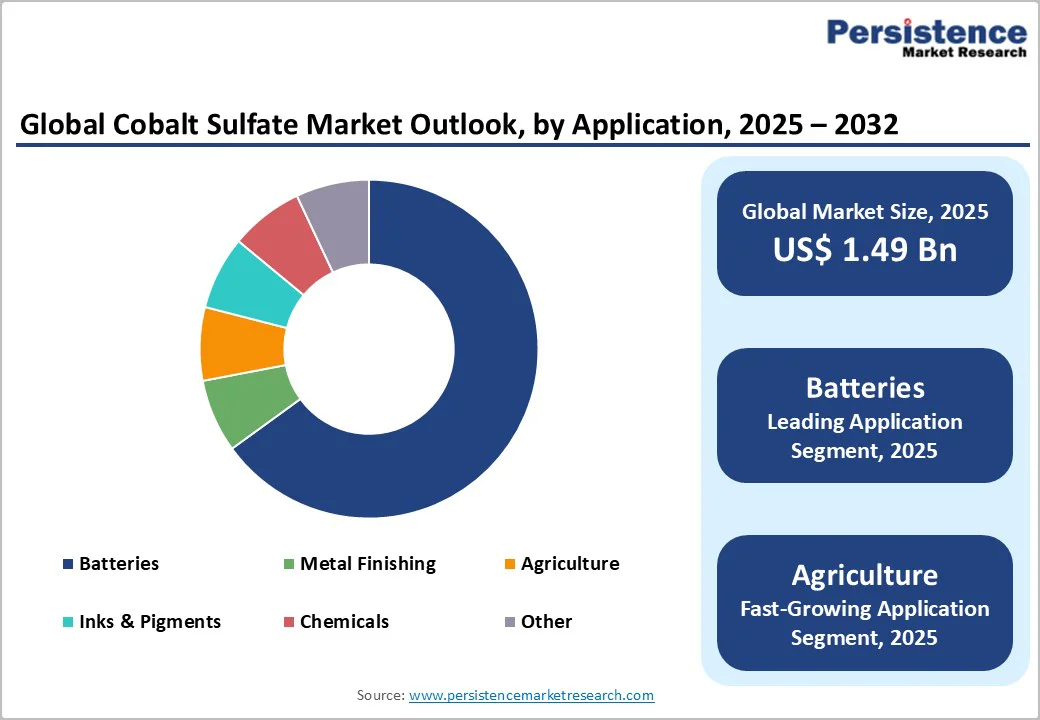

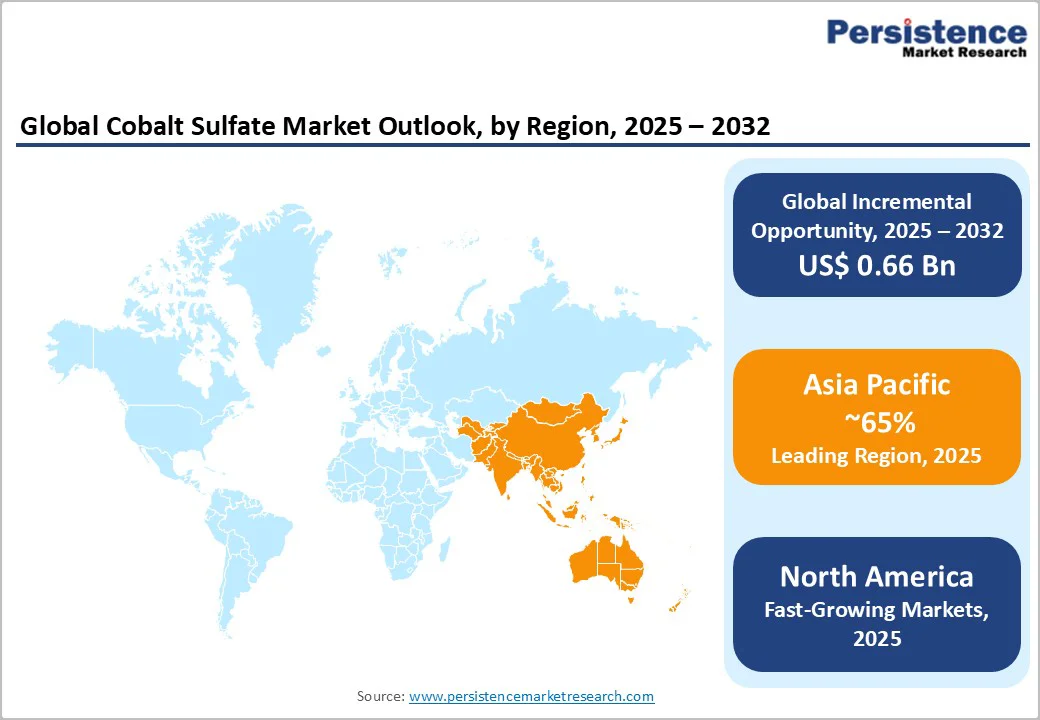

The global cobalt sulfate market size is likely to be valued at US$1.49 billion in 2025 and is expected to reach US$2.15 billion by 2032, growing at a CAGR of 5.4% during the forecast period from 2025 to 2032, driven by the surging demand from the electric vehicle sector, where cobalt sulfate is essential for lithium-ion battery cathodes. This growth is supported by global shifts toward renewable energy storage and consumer electronics, with the International Energy Agency (IEA) reporting that electric vehicle (EV) sales reached over 14 million units in 2023, amplifying the need for high-purity cobalt compounds.

Key Market Highlights

- Regional Leader: Asia Pacific leads the cobalt sulfate market, driven by China's refining dominance and EV manufacturing, capturing 65% share through cost-effective production hubs.

- Fastest Growing Region: North America emerges as the fastest-growing region, propelled by IRA incentives and recycling initiatives.

- Leading Segment: Battery Grade dominates grades, with a 75% share, driven by lithium-ion battery demand in EVs and the need for high-performance cathodes.

- Fastest Growing Region: Batteries application grows fastest, fueled by renewable storage needs, with a 6.5% annual demand surge from global electrification.

- Growth Opportunities: Strategic development of battery recycling infrastructure represents the highest-potential opportunity, with recycled cobalt projected to supply 19% of European demand by 2030 and 40-53% globally by 2035-2040.

| Key Insights | Details |

|---|---|

|

Cobalt Sulfate Market Size (2025E) |

US$1.49 Bn |

|

Market Value Forecast (2032F) |

US$2.15 Bn |

|

Projected Growth CAGR (2025-2032) |

5.4% |

|

Historical Market Growth (2019-2024) |

3.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand in EV Batteries

The exponential growth in EV adoption worldwide is a major driver for the cobalt sulfate market, as it serves as a critical precursor in lithium-ion battery production. Governments are pushing for cleaner transportation, with the European Union targeting 30 million zero-emission vehicles by 2030, thereby increasing demand for cobalt sulfate in cathode materials.

This demand is evident in the lithium-ion battery market, where cobalt-enhanced batteries dominate due to their superior stability and energy density, accounting for nearly 60% of global EV battery use. The synergy between rising EV production and the lithium-ion battery market has established cobalt sulfate as a strategic material, with market participants forecasting continued demand growth.

Expansion of Renewable Energy Storage Systems

The global push for renewable energy integration is fueling cobalt sulfate demand through its role in grid-scale battery storage solutions. According to the IEA, renewable capacity additions reached 510 GW in 2023, necessitating efficient batteries for managing intermittency, where cobalt sulfate improves cycle life and performance. This is particularly evident in solar and wind projects, with the Li-ion pouch battery market relying on cobalt for compact, high-density designs used in energy storage.

Cobalt sulfate is used in stationary storage applications, where cobalt-stabilizer additives improve the stability of lithium iron phosphate (LFP) cathodes, enhancing battery cycle life and safety performance. Grid operators and utilities are increasingly deploying large-scale battery storage facilities to manage peak demand and address the intermittency of renewable energy sources. This trend creates a structural demand driver that is independent of the EV market cycles. As a result, it strengthens market resilience by diversifying applications beyond automotive uses and supporting long-term growth.

Barrier Analysis - Supply Chain Vulnerabilities and Geopolitical Risks

The cobalt sulfate market is currently facing significant challenges due to concentrated supply chains, primarily from the Democratic Republic of Congo (DRC), which accounts for over 70% of global cobalt production. In February 2025, the DRC implemented a complete export ban on raw and semi-processed cobalt. Starting in October 2025, the country will transition to a quota-based export system. This policy aims to promote domestic processing and value addition within the DRC, but it has created substantial disruptions in the supply chain for global cobalt sulfate manufacturers.

Major mining companies, such as CMOC Group (CMOC), produced approximately 114,165 metric tons of cobalt in 2024. However, they now face export quotas that limit shipments to just 27% of their 2024 production volumes in 2026. These restrictions exacerbate raw material shortages for sulfate production, making it difficult for battery manufacturers to secure a stable supply and driving up costs. Such vulnerabilities undermine market predictability and investor confidence.

Stringent Environmental and Competition from Alternative Battery Chemistries

Regulatory pressures on cobalt mining and processing create obstacles, as agencies such as the European Chemicals Agency (ECHA) classify cobalt sulfate as a carcinogen and enforce strict exposure limits under REACH. This has increased compliance costs for EU producers by 20-30%, slowing expansion and encouraging the use of alternative materials. In the US, EPA waste management guidelines add further complexity, potentially delaying projects and reducing production. Although these rules aim to ensure safety, they also limit market growth by restricting production scalability.

Furthermore, the global battery industry is shifting toward alternative chemistries, such as lithium iron phosphate (LFP) and lithium manganese iron phosphate (LMFP), which either reduce or eliminate cobalt requirements. LFP batteries decrease material costs by 20-30% per kilowatt-hour and offer better thermal stability and safety, making them increasingly popular for mass-market EVs and stationary storage. In 2023, nearly 50% of passenger EVs used non-cobalt chemistries, highlighting the trend toward wider adoption.

Opportunity Analysis - Strategic Diversification of Cobalt Mining Outside DRC

Significant market opportunities exist for cobalt sulfate manufacturers and downstream users capable of securing supply from non-DRC sources. Indonesia ranks as the world’s second-largest cobalt producer, increasing its output from 19,000 metric tons in 2023 to 28,000 metric tons in 2024. Australia's Cobalt Blue project represents the first dedicated primary cobalt mining operation outside mixed copper-nickel operations, with plans to produce battery-grade cobalt sulfate at its Kwinana facility beginning in 2025-2026.

European initiatives led by Jervois Finland, which operates the Kokkola facility in Finland with a current capacity of 6,250 metric tons per year, are planning to expand this capacity to 12,250 metric tons. This expansion aims to provide Western sources of responsibly sourced cobalt sulfate, which command premium prices from battery manufacturers looking to diversify their supply chains. Companies investing in both mining diversification and recycling capabilities position themselves to capture significant value as supply chains transition toward resilience and circularity.

Growth in Emerging Markets for Agricultural Applications

Expanding agricultural use in developing regions offers significant potential, as cobalt sulfate serves as a vital trace mineral in animal feed and fertilizers. Cobalt is an essential micronutrient for leguminous crops, including pea, faba bean, chickpea, and lentil varieties, where it facilitates nitrogen fixation through the enhancement of nitrogenase enzyme activity in root nodules.

With global livestock production projected to rise by 14% by 2030, according to the Food and Agriculture Organization (FAO), demand for feed-grade cobalt could increase by 25% in Asia and Africa. This opportunity is enhanced by soil deficiency programs in India, where cobalt supplementation improves ruminant health and milk yield by 15-20%. Market players can leverage this by developing affordable formulations and tapping into underserved segments to drive volume growth.

Category-wise Insights

Grade Analysis

The battery grade segment leads the cobalt sulfate market with an approximate 75% share, driven by its high purity requirements for lithium-ion battery cathodes. Battery-grade cobalt sulfate is distinguished by exceptionally stringent purity specifications, with metal impurities typically limited to below 10 ppm and cobalt content standardized at 20.5%, meeting or exceeding ISO and industry-specific standards for NMC and NCA cathode precursor applications.

Battery manufacturers impose strict quality controls because impurities can degrade battery performance, reduce cycle life, and compromise safety characteristics in high-energy-density applications. The premium pricing commanded by battery-grade material reflects manufacturing process complexity, rigorous testing requirements, and long-term supply agreements with tier-one battery makers.

Application Analysis

Batteries hold a dominant market position, with approximately 65% market share, driven by their crucial role in cathode production for energy storage. The rapid adoption of EVs bolsters this segment's significance. According to the International Energy Agency (IEA), in 2023, the supply of cobalt and nickel exceeded demand by 6.5% and 8%, respectively, leading to lower prices for critical minerals and lower battery costs.

NMC (Nickel Manganese Cobalt) cathode formulations lead the battery market due to their high energy density, long cycle life, and cost-effectiveness. Cobalt sulfate is transformed into cobalt hydroxide or other compounds for use in cathode precursor materials. Secondary battery applications include consumer electronics, power tools, and sodium-ion batteries, where cobalt remains competitive in premium segments. In lithium-ion batteries, cobalt sulfate improves stability and prevents thermal runaway in high-density packs.

Regional Insights

North America Cobalt Sulfate Trends

North America is transitioning from reliance on imported cobalt sulfate to developing domestic refining capabilities, thanks to government initiatives. The U.S. and Canada have historically sourced refined cobalt sulfate from China. To bolster supply chain resilience, the U.S. Department of Defense is investing in domestic cobalt refining, including funding for Jervois to build a refinery projected to produce 6,000 metric tons initially, with an eventual capacity of 10,000 metric tons. This will support the supply of cobalt sulfate for around 1.2 million EVs annually.

Regulatory frameworks, including the Inflation Reduction Act (IRA) and Critical Minerals Strategy, have catalyzed investments in North American battery manufacturing, creating localized cobalt sulfate demand among emerging gigafactories operated by Tesla, Ford, General Motors, and joint ventures.

Europe Cobalt Sulfate Trends

Europe's cobalt sulfate market is shaped by harmonized regulations under REACH and the Battery Regulation, emphasizing ethical sourcing and recycling to build a resilient supply chain.

Germany, Belgium, and Finland operate major cobalt sulfate refining and processing facilities, with Belgium historically serving as a primary European refining hub before production decentralization. Finland's Kokkola Industrial Park hosts Jervois Finland operations, one of only two Western sources of cobalt sulfate certified as conformant to Responsible Minerals Initiative (RMI) standards, reflecting European emphasis on ethical sourcing and supply chain transparency.

The European Union Battery Regulation mandates minimum cobalt recovery rates of 90% by 2027 and 95% by 2031 from end-of-life batteries, creating structured demand for recycling infrastructure and recycled cobalt sulfate material. By 2031, the EU requires a minimum 6% recycled cobalt content in new lithium-ion batteries, escalating to 12% by 2036, establishing regulatory pull for battery recycling technologies and secondary cobalt sulfate production.

Asia Pacific Cobalt Sulfate Trends

Asia Pacific dominates the cobalt sulfate market, accounting for 65% of global market share, driven by China's position as the world's largest EV producer and the primary cobalt refining hub. Chinese battery manufacturers, including CATL, BYD, and GEM, operate integrated supply chains extending from DRC mining operations through refining to cathode material production and battery assembly, enabling cobalt sulfate optimization at each process stage. Indonesia has emerged as a transformational secondary cobalt producer.

India demonstrates the fastest Asia-Pacific growth trajectory, driven by government electrification initiatives, emerging battery manufacturing capacity through partnerships with Tesla, CATL, and Samsung SDI, and rising agricultural micronutrient demand for cobalt sulfate-based fertilizers to support crop productivity in Indian farming systems.

Competitive Landscape

The global cobalt sulfate market exhibits a consolidated structure, with top players controlling over 60% of supply through vertical integration in mining and refining. Companies pursue expansion via strategic partnerships, such as joint ventures for recycling, while R&D focuses on low-cobalt cathodes to counter shortages. Key differentiators include ESG compliance and traceability, with leaders such as Norilsk Nickel emphasizing sustainable sourcing. Emerging models involve blockchain for supply chain transparency, enhancing competitiveness in regulated regions.

Key Industry Developments

- February 2025: The Democratic Republic of Congo implemented a complete ban on raw and semi-processed cobalt exports, transitioning to a quota-based system in October 2025. This policy shift triggered global supply chain restructuring, signaling strategic stockpiling and processing capacity enhancement within the DRC.

- January 2025: Jervois Global completed pre-arranged bankruptcy restructuring with Millstreet Capital Management, injecting US$145 Million and converting US$100 Million+ in debt to equity, enabling Jervois Finland expansion to 12,250 metric tons capacity.

Companies Covered in Cobalt Sulfate Market

- Suchem Industries

- American Elements

- Vital Materials Co., Ltd.

- Jigchem Universal

- Jay Intermediates and Chemicals

- Shanghai Shunbo Metal Materials

- Stellantis

- Jervois Finland

- Jiayuan Cobalt Holdings Limited

- Jinchuan Group International Resources Co. Ltd.

- Nicomet Industries Limited

- Norilsk Nickel

- Zhangjiagang Huayi Chemical Co., Ltd

- Jilin Jien Nickel Industry Company Limited

- CMOC Group Ltd.

- Glencore PLC

- Umicore SA

Frequently Asked Questions

The cobalt sulfate market is valued at US$1.49 Billion in 2025 and is expected to reach US$2.15 Billion by 2032, growing at a 5.4% CAGR driven by battery demand.

The rise in EV adoption is a primary driver, with cobalt sulfate essential for lithium-ion cathodes, supported by IEA projections of 17 million EV sales in 2024.

Battery grade leads with 75% share, justified by its high-purity needs in EV batteries for enhanced energy density and stability.

Asia Pacific leads, holding a 65% share due to China's refining dominance and EV manufacturing hubs such as those of BYD.

Strategic battery recycling infrastructure development represents the highest potential opportunity, with recycled cobalt projected to supply 19% of European demand by 2030 and 40-53% globally by 2035-2040.

Leading players include Jinchuan Group and Jervois Finland, dominating through integrated production and ESG focus.