- Medical Devices

- Coagulation Markers Market

Coagulation Markers Market Size, Share, and Growth Forecast, 2026-2033

Coagulation Markers Market by Test Type (D-dimer Assays, Fibrinogen Assays, PT/INR Tests, aPTT Tests, Thrombin Time Tests, Anti-Factor Xa Assays, Platelet Function Tests), Technology (Immunoassays, Immunoturbidimetric Assays, Mechanical Clot Detection, Optical Clot Detection, Thromboelastography (TEG), Automated Analyzers), End-User (Hospitals, Diagnostic Laboratories, Specialty Clinics, Research Institutes, Pharmaceutical & Biotech Companies, Home Healthcare Providers), and Regional Analysis for 2026-2033

Coagulation Markers Market Share and Trends Analysis

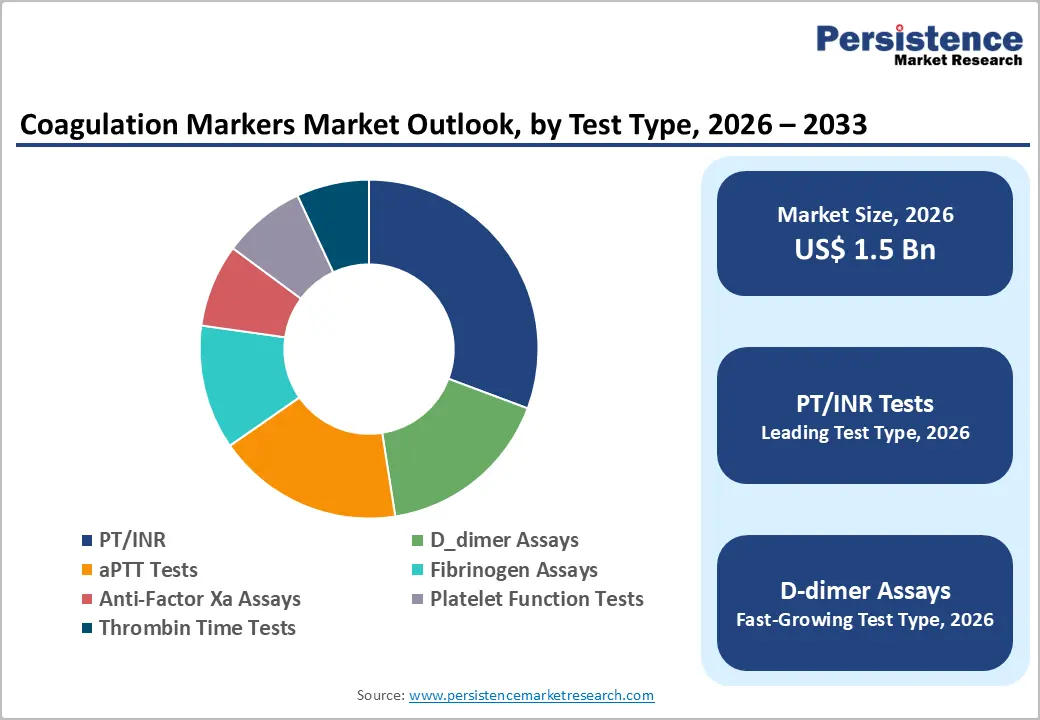

The global coagulation markers market size is likely to be valued at US$ 1.5 billion in 2026, and is projected to reach US$ 2.2 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026–2033.

Sustained growth in the coagulation testing market is driven by the rising global burden of cardiovascular diseases, venous thromboembolism (VTE), and rapidly aging populations. Healthcare systems increasingly rely on hemostasis testing to diagnose thrombotic disorders, monitor anticoagulant therapy, and manage surgical risk. Clinical guidelines now emphasize routine PT/INR, D-dimer, and anti-Factor Xa testing for evidence-based treatment decisions. The laboratories are adopting advanced automated analyzers and high-sensitivity immunoassays to enhance diagnostic precision and reduce turnaround time. These technological improvements increase testing volumes, optimize workflow efficiency, and strengthen the long-term growth outlook for the broader in-vitro diagnostics (IVD) market.

Key Industry Highlights

- Dominant Test Type: PT/INR tests are set to command around 29% revenue share in 2026, while D-dimer assays are projected to grow the fastest at a 6.8% CAGR through 2033, owing to strong emergency diagnostics demand.

- Leading Technology: Immunoassays are expected to lead with nearly 33% share in 2026, while thromboelastography (TEG) is likely to expand at the fastest pace during 2026–2033, driven by critical care and trauma applications.

- Primary End-User: Hospitals are anticipated to dominate with approximately 41.6% revenue share in 2026, whereas diagnostic laboratories are set for the fastest growth through 2033, reflecting outsourcing and centralized testing trends.

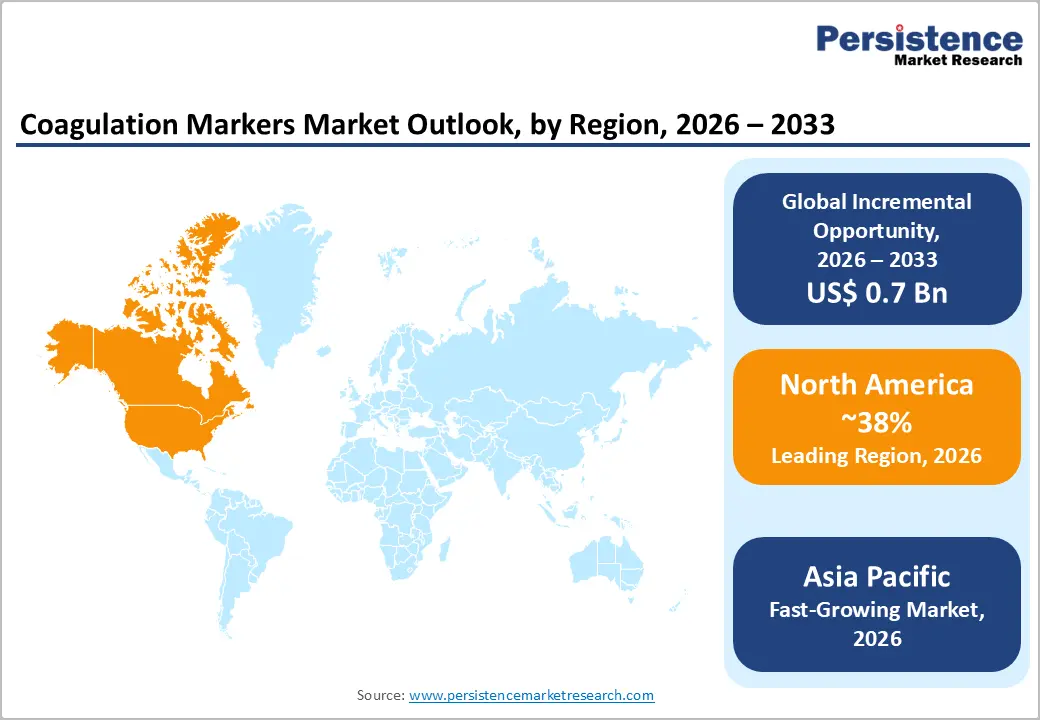

- Regional Leadership: North America is poised to hold about 38% share in 2026, while the Asia Pacific market is projected to register the highest 2026-2033 CAGR of nearly 7.1%, fueled by expanding diagnostic access.

- Competitive Environment: Strategic priorities include accelerated laboratory automation, expansion of decentralized and point-of-care coagulation testing, and investments in reagent manufacturing capacity.

| Key Insights | Details |

|---|---|

|

Coagulation Markers Market Size (2026E) |

US$ 1.5 Bn |

|

Market Value Forecast (2033F) |

US$ 2.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Cardiovascular Disease Burden, Aging Demographics, and Evolving Clinical Guidance

According to the World Health Organization (WHO), cardiovascular diseases account for approximately 20 million deaths annually, making them the leading cause of mortality worldwide. The Centers for Disease Control and Prevention (CDC) estimates that up to 900,000 cases of venous thromboembolism (VTE) occur each year in the United States. In parallel, the United Nations projects that the global population aged 65 years and above will double between 2020 and 2050. Older adults face higher incidences of atrial fibrillation, thrombosis, and chronic diseases requiring anticoagulation therapy. These demographic and epidemiological trends structurally increase the need for routine coagulation assessment. Healthcare systems therefore depend on scalable, standardized coagulation testing protocols.

In late 2025, the Association for Diagnostic and Laboratory Medicine (ADLM) released updated guidance to improve accuracy in coagulation testing for patients receiving anticoagulants, particularly direct oral anticoagulants. The recommendations emphasize appropriate assay selection and interpretation to prevent misclassification of thrombotic risk. In early 2026, findings presented at the American Heart Association International Stroke Conference highlighted variability in anticoagulant response among stroke patients, underscoring the importance of precise hemostasis diagnostics. These validated clinical discussions move coagulation testing from optional screening to guideline-driven practice, strengthening recurring demand across hospital and emergency care settings.

Expanding Surgical Volumes and Acceleration of Laboratory Automation

Rising global surgical volumes, particularly in cardiovascular and orthopedic procedures, continue to drive perioperative coagulation screening requirements. Hospitals routinely conduct PT/INR, aPTT, fibrinogen, and thrombin time testing before and after surgery to minimize bleeding and thrombotic complications. This testing forms part of standardized risk management frameworks embedded in hospital accreditation systems. As surgical access expands in both developed and emerging healthcare markets, laboratories experience consistent increases in test volumes. The procedural nature of this demand ensures repeat utilization rather than one-time diagnostic events. Consequently, surgical expansion acts as a stable and predictable growth lever for the coagulation markers market.

The implementation of the European Union (EU) In Vitro Diagnostic Regulation (IVDR), overseen by the European Commission (EC), has required manufacturers to strengthen clinical validation and quality documentation for coagulation assays. This regulatory shift supports higher-standard, performance-verified diagnostics across EU laboratories. In parallel, continued approvals by the U.S. Food and Drug Administration (FDA) for automated coagulation analyzers reinforce automation adoption in high-throughput hospital networks. Laboratories increasingly integrate immunoturbidimetric assays, optical clot detection, and digital workflow systems to reduce turnaround time and manual variability. These technology investments expand per-instrument testing capacity, increase reagent consumption, and enhance operational efficiency, directly contributing to sustainable revenue growth within the global coagulation testing market.

High Capital Investment and Regulatory-Driven Cost Pressures

Advanced coagulation analyzers and TEG systems involve significant capital expenditure, often exceeding mid-six-figure investments for high-throughput platforms. Smaller diagnostic laboratories in emerging markets face budget constraints, limiting adoption. Procurement cycles in public healthcare systems frequently require multiyear capital approvals, delaying equipment upgrades. In 2025, implementation challenges under the EU IVDR continued to strain manufacturers and laboratories due to limited notified body capacity. Extended conformity assessment timelines increased compliance costs and delayed new product availability. These structural pressures reinforce financial caution in capital investment decisions.

The recurring costs related to reagents, calibration, and quality control compliance increase operational expenditure. Laboratories must maintain stringent documentation and post-market surveillance systems to remain compliant with evolving regulatory frameworks. Service contracts, software validation, and instrument maintenance further raise total cost of ownership. In late 2025, European hospital associations publicly warned that regulatory complexity under the IVDR could disrupt access to certain diagnostic technologies, affecting procurement planning. Such uncertainty discourages rapid modernization of coagulation platforms. As a result, high capital intensity and compliance-linked costs moderate overall market acceleration.

Regulatory Uncertainty and Reimbursement Variability

Stringent regulatory requirements across regions create extended approval timelines for new IVD coagulation tests. Compliance with CE marking under EU IVDR and FDA premarket pathways requires extensive clinical validation and technical documentation. Regulatory transitions often require manufacturers to reassess legacy product portfolios, increasing administrative burden. In 2025, evolving oversight discussions around laboratory-developed tests (LDTs) by the U.S. FDA introduced temporary uncertainty regarding future compliance expectations. Such policy shifts complicate long-term product planning strategies. Companies must therefore allocate additional resources toward regulatory monitoring and risk mitigation.

Reimbursement inconsistencies further affect test adoption rates across healthcare systems. In several markets, bundled payment models compress laboratory margins and reduce flexibility for premium assay adoption. Hospitals and independent laboratories often evaluate return on investment before integrating advanced coagulation platforms. Variability in payer policies creates uneven incentives for adopting higher-sensitivity or specialty assays. This financial unpredictability influences purchasing behavior, particularly in mature healthcare markets. These regulatory complexities and reimbursement variability create measurable friction within the global coagulation testing market, tempering short- to mid-term growth momentum.

Emerging Market Expansion and Government-Backed Diagnostic Modernization

Healthcare expenditure growth in Asia Pacific and Latin America presents untapped opportunities for the coagulation testing market. Government-backed insurance programs in countries such as China and India are expanding access to diagnostic services and increasing patient participation in formal healthcare systems. Several ASEAN governments strengthened primary care networks in 2025 by integrating point-of-care diagnostics into public screening initiatives, particularly in semi-urban and rural regions. These policy-driven efforts aim to improve early detection of chronic and cardiovascular conditions. With improving laboratory infrastructure and rising cardiovascular disease prevalence, emerging markets represent a high-potential revenue pool for coagulation testing solutions. This structural expansion enhances long-term demand visibility.

Localization of manufacturing and reagent production can enhance cost competitiveness and expand addressable demand. Governments across Asia continue encouraging domestic medical device production through regulatory incentives and procurement preferences. Infrastructure investments in regional diagnostic hubs are accelerating laboratory automation upgrades. As accreditation standards rise, laboratories increasingly adopt standardized hemostasis testing platforms. The expansion of universal health coverage programs further increases routine diagnostic utilization. Together, public health funding, infrastructure modernization, and policy support create a scalable opportunity for manufacturers seeking geographic diversification.

Decentralized Care Models and Clinical Research Collaboration

The growing shift toward decentralized diagnostics creates opportunities for compact, point-of-care PT/INR testing devices. Increased adoption of direct oral anticoagulants (DOACs) still requires periodic monitoring in high-risk populations. In December 2025, the Centers for Medicare & Medicaid Services introduced the ACCESS pilot model to evaluate outcome-based reimbursement structures supporting technology-enabled chronic care. This initiative encourages the integration of remote and point-of-care diagnostics into long-term disease management. Home healthcare providers are incorporating portable coagulation analyzers to reduce hospital readmissions. As value-based care models expand, decentralized hemostasis testing becomes increasingly viable and financially aligned with reimbursement innovation.

Simultaneously, regulatory bodies are promoting connected and interoperable diagnostic systems. The U.S. FDA advanced initiatives supporting digital and connected point-of-care diagnostics to enhance real-time data integration across healthcare networks. These efforts strengthen clinical oversight while enabling decentralized testing environments. The expansion of anticoagulant drug pipelines also necessitates biomarker validation in clinical trials, increasing demand for specialized anti-Factor Xa assays and platelet function testing. Collaborative partnerships between diagnostic manufacturers and pharmaceutical companies create recurring institutional demand. As therapeutic innovation accelerates, research-driven assay development offers a high-margin, strategically attractive growth pathway within the global coagulation markers market.

Category-wise Analysis

Test Type Insights

PT/INR tests are projected to command approximately 29% of the coagulation markers market revenue share in 2026, driven by their critical role in anticoagulant monitoring and standardized clinical use. Clinicians widely rely on PT/INR to guide warfarin dose adjustments and perioperative risk assessment. These tests remain integral to chronic care workflows in hospitals and diagnostic labs, reinforcing stable demand across healthcare settings. External quality programs such as the UK NEQAS Point of Care (POC) Programme continue to include INR testing in their 2025–2026 proficiency schemes, underscoring sustained clinical relevance and quality emphasis.

D-dimer assays are likely to represent the fastest-growing test type, with an estimated 6.8% CAGR through 2033, as emergency departments increasingly use them to rule out deep vein thrombosis and pulmonary embolism. Recent market analyses indicate D-dimer testing is becoming a frontline diagnostic tool in acute settings, supported by improved availability of point-of-care and laboratory diagnostics. Emergency medicine protocols emphasize rapid D-dimer utilization to streamline patient triage, further accelerating uptake. Combined with ongoing awareness campaigns about thrombotic disorder detection in acute care, this elevates D-dimer’s growth trajectory within the coagulation markers market.

Technology Insights

Immunoassays are expected to hold nearly 33% of the coagulation markers market share in 2026, reflecting their established role in high-throughput laboratories and automation-driven hospital networks. These platforms deliver high analytical sensitivity and reproducibility, which are essential for routine PT/INR and D-dimer assessments. As core lab systems continue to integrate coagulation testing into comprehensive diagnostic panels, immunoassays maintain their technological leadership. Their broad application across centralized hospitals reinforces operational efficiency and test standardization at scale. Supporting this, external quality assessment programmes for coagulation, including D-dimer and INR tests within POC proficiency initiatives, highlight the importance of immunoassay accuracy in clinical practice and quality systems.

Thromboelastography is poised to be the fastest-growing technology segment, with an estimated 7.2% CAGR through 2033, as clinical use expands beyond traditional surgical settings. In April 2025, clinical studies on viscoelastic haemostatic assays (including TEG and ROTEM) demonstrated their growing availability in emergency care environments, confirming broader utility for rapid hemostatic profiling. TEG’s real-time, whole-blood assessment continues to attract adoption in trauma, critical care, and specialized procedure units. Its dynamic profiling capability differentiates it from static clotting tests, positioning TEG as a high-growth, advanced hemostasis technology within the evolving coagulation diagnostics landscape.

Regional Insights

North America Coagulation Markers Market Trends

North America is expected to remain the leading regional market, commanding around 38% of global revenue in 2026 due to mature healthcare systems, established reimbursement frameworks, and high diagnostic utilization. Hospitals and centralized laboratories invest heavily in automated systems and digital integration to manage high procedure volumes. For instance, in January 2026, Insight Molecular Diagnostics Inc. announced FDA de novo submission for its GraftAssureDx test kit, illustrating ongoing innovation in advanced diagnostics in the U.S. market. Hospitals continue adopting point-of-care tools and high-throughput analyzers to accelerate workflows and improve clinical outcomes.

Healthcare systems in the U.S. and Canada further prioritize diagnostic expansion and consolidation to strengthen capacity and accessibility. In early 2026, Quest Diagnostics revealed plans for a CAD 1.35 billion acquisition of LifeLabs in Canada to bolster testing capacity and speed innovation, demonstrating continued strategic investment in clinical diagnostics infrastructure. These activities, combined with widespread use of AI-supported digital pathology and EHR integration, reinforce demand for coagulation and other clinical testing panels. Together, these structural and investment trends solidify North America’s dominant position in the global coagulation markers landscape.

Europe Coagulation Markers Market Trends

Europe accounts for an estimated 27% of global revenue in 2026, supported by well-entrenched healthcare systems, widespread laboratory networks, and harmonized regulatory frameworks across the EU. The EC’s October 2025 ‘call for evidence’ on future medical device and in vitro diagnostic regulation reflects ongoing regional efforts to streamline regulation, reduce administrative burdens, and improve international competitiveness. These policy moves aim to stabilize diagnostic markets while maintaining high safety standards, directly influencing the way laboratories adopt and deploy new assay technologies.

National commitments to expanding laboratory capacity and digital workflows further support demand. In 2025, efforts to expand diagnostic quality and capacity in India and Europe alike, such as the introduction of performance standards for diagnostic labs during India’s National Virus Research & Diagnostic Laboratory Conclave, underscore broader regional emphasis on diagnostic accuracy and infrastructure modernization. While these reforms affect various diagnostic categories, they help sustain clinical testing demand, including coagulation markers, as European healthcare systems modernize and align operational standards with quality imperatives.

Asia Pacific Coagulation Markers Market Trends

Asia Pacific is poised to be the fastest-growing regional market, with a projected 7.1% CAGR from 2026 to 2033. The growth is supported by expanding healthcare access, policy reforms, and rapid diagnostic modernization across China, India, Japan, and ASEAN nations. Governments in the region are strengthening laboratory infrastructure and digital diagnostics; a 2025 clinical laboratory outlook report highlights rapid capacity expansion across public hospitals and diagnostics hubs, with investments in high-throughput analyzers and digital result integration improving clinical workflows. This modernization directly supports broader adoption of hemostasis testing across emerging economies.

Population health initiatives and regulatory reforms further enhance demand for clinical diagnostics. For example, India’s government launched India-oriented performance standards for diagnostic laboratories in September 2025, aiming to improve consistency, accuracy, and reliability of test results across the country. These national standards contribute to strengthening quality assurance in clinical labs, which drives greater adoption of advanced diagnostic assays, including coagulation markers.

Rising healthcare expenditure, improving insurance coverage, and the growth of private diagnostic networks continue to accelerate regional demand, positioning Asia Pacific as the most dynamic market segment globally.

Competitive Landscape

The global coagulation markers market structure is moderately consolidated, with leading players such as Siemens Healthineers, Roche Diagnostics, Abbott Laboratories, and Werfen Group collectively controlling over half of the total revenue share. These established companies leverage extensive hospital and laboratory networks, deep regulatory expertise, and integrated diagnostic platforms combining automated analyzers with high-sensitivity assays. They also invest heavily in R&D for new coagulation tests, advanced immunoassay technologies, and point-of-care platforms, maintaining technological leadership and addressing evolving clinical needs.

Meanwhile, regional and niche competitors, including Instrumentation Laboratory (IL) and Diagnostica Stago, focus on specialized coagulation assays, thromboelastography, and strong presence in selected geographies such as Europe and Asia Pacific. Barriers such as stringent regulatory approval, laboratory accreditation requirements, and high capital costs limit new entrants. However, digitalization and laboratory automation trends are enabling software-enabled diagnostics companies to participate through integrated analyzer solutions and cloud-based lab management platforms. Market consolidation is expected to continue as global leaders pursue acquisitions to expand their geographic footprint and product portfolios.

Key Industry Developments

- In March 2026, India’s Health Ministry proposed amendments to the Drugs Rules, 1945 to align blood product testing with international pharmacopoeial standards and eliminate duplicate viral testing of plasma-derived medicines. The change removes the requirement to retest finished products when pooled plasma has already been screened for different infections.

- In August 2025, researchers at Tulane University began testing a portable diagnostic device that can detect life-threatening blood-clotting disorders in trauma patients using only a single drop of blood. The battery-powered system uses acoustic “tweezing” technology to analyze how a suspended blood droplet deforms, enabling clinicians to assess coagulation status rapidly in emergency settings.

- In June 2025, Sysmex launched its XR-Series Automated Hematology Analyzer in the U.S. after receiving FDA 510(k) clearance, enhancing automation and high-throughput diagnostic capabilities. This launch highlights continued industry investment in integrated laboratory platforms, improving workflow efficiency and supporting broader adoption of advanced testing panels.

Companies Covered in Coagulation Markers Market

- Roche Diagnostics

- Siemens Healthineers

- Abbott Laboratories

- Danaher Corporation

- Sysmex Corporation

- Thermo Fisher Scientific

- Werfen

- Bio-Rad Laboratories

- Grifols

- Trinity Biotech

- Sekisui Diagnostics

- Instrumentation Laboratory

Frequently Asked Questions

The integration of artificial intelligence (AI) and big data analytic is a key opportunity in the market.

Some of the leading players profiled in the market are Accuquik™ Test Kits, CTK Biotech, Inc., Siemens Healthcare Private Limited, Quidel Corporation, and Eurolyser Diagnostica GmbH.

The coagulation markets market is projected to record a CAGR of 6.50% during the forecast period.

Rising aging population is driving the demand for coagulation markets.

The coagulation markers market is poised for significant expansion in the United Kingdom.