- Medical Devices

- Chest Drainage Systems Market

Chest Drainage Systems Market Size, Share, and Growth Forecast 2026 - 2033

Chest Drainage Systems Market by Product (Pleural Drainage Systems (Traditional Pleural Drainage Systems, Digital Pleural Drainage Systems), Pleural Drainage Systems Kits, Pleural Drainage Systems Accessories), Indication (Pleural Effusion, Hemothorax, Spontaneous Pneumothorax, Tension Pneumothorax, Traumatic Pneumothorax, Cardiac Tamponade, Others), End-User, and Regional Analysis, 2026–2033

Chest Drainage Systems Market Share and Trends Analysis

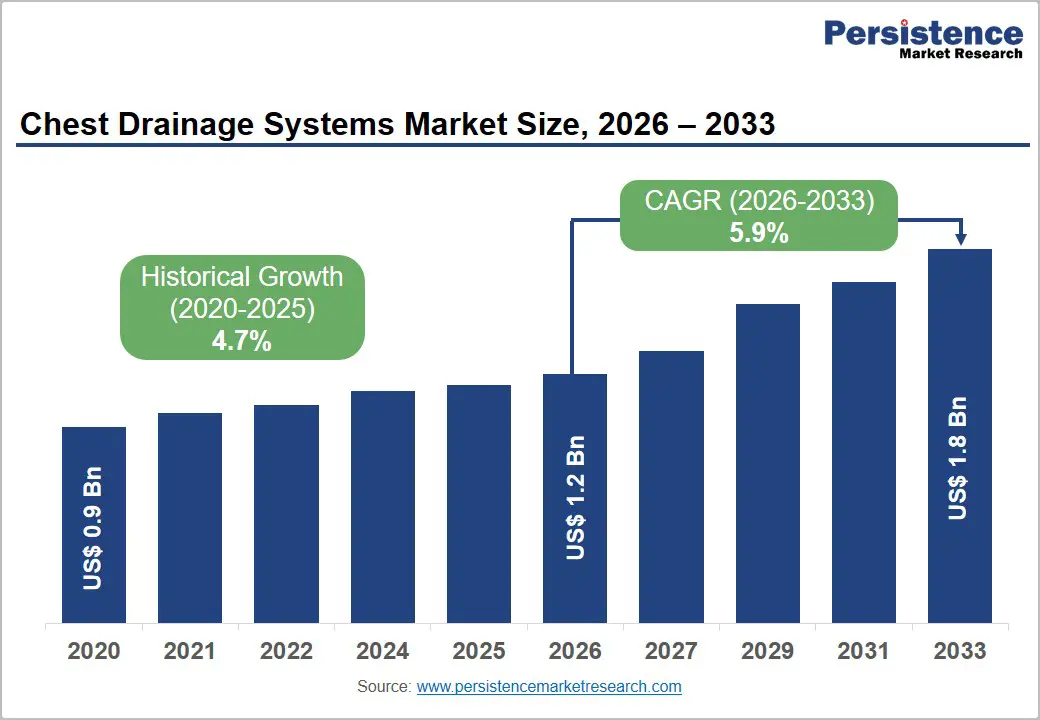

The global chest drainage systems market size is expected to be valued at US$ 1.2 billion in 2026 and projected to reach US$ 1.8 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033. It is witnessing a steady growth due to the increasing incidence of respiratory diseases, thoracic surgeries, traumatic chest injuries, and cardiovascular disorders worldwide. These systems are widely used to remove air, blood, and excess fluids from the pleural cavity following surgery or emergency treatment procedures. Rising adoption of minimally invasive surgeries and growing demand for advanced digital drainage monitoring solutions are supporting market expansion.

Healthcare providers are increasingly preferring portable and infection-control drainage devices to improve patient safety and reduce hospitalization time. Additionally, expanding healthcare infrastructure and rising critical care admissions in emerging economies are creating strong long-term growth opportunities for the market.

Key Industry Highlights:

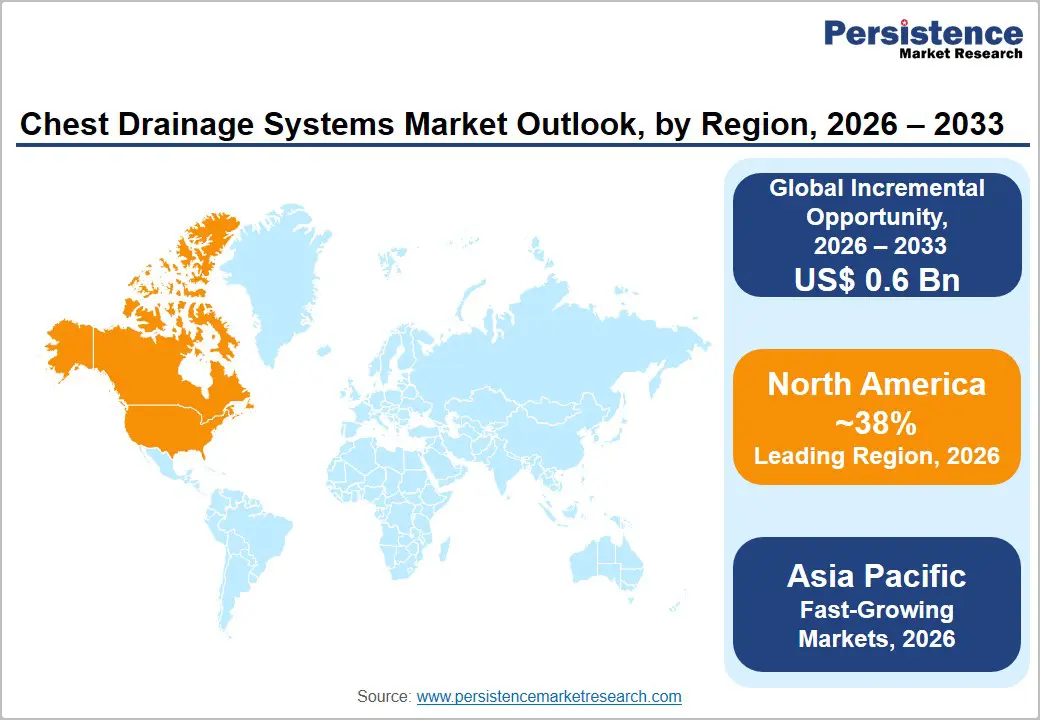

- Leading Region: North America is likely to dominate the global chest drainage systems market with 38% market share in 2026, driven by high pleural disease prevalence, strong reimbursement coverage, and rapid adoption of digital pleural drainage systems across academic medical centers and large hospital networks.

- Fastest Growing Region: Asia Pacific is projected to register the highest CAGR during 2026–2033, fueled by China’s Healthy China 2030 hospital expansion initiative, India’s high TB and lung cancer burden, and rapidly growing private thoracic surgery capacity across Japan and Southeast Asia.

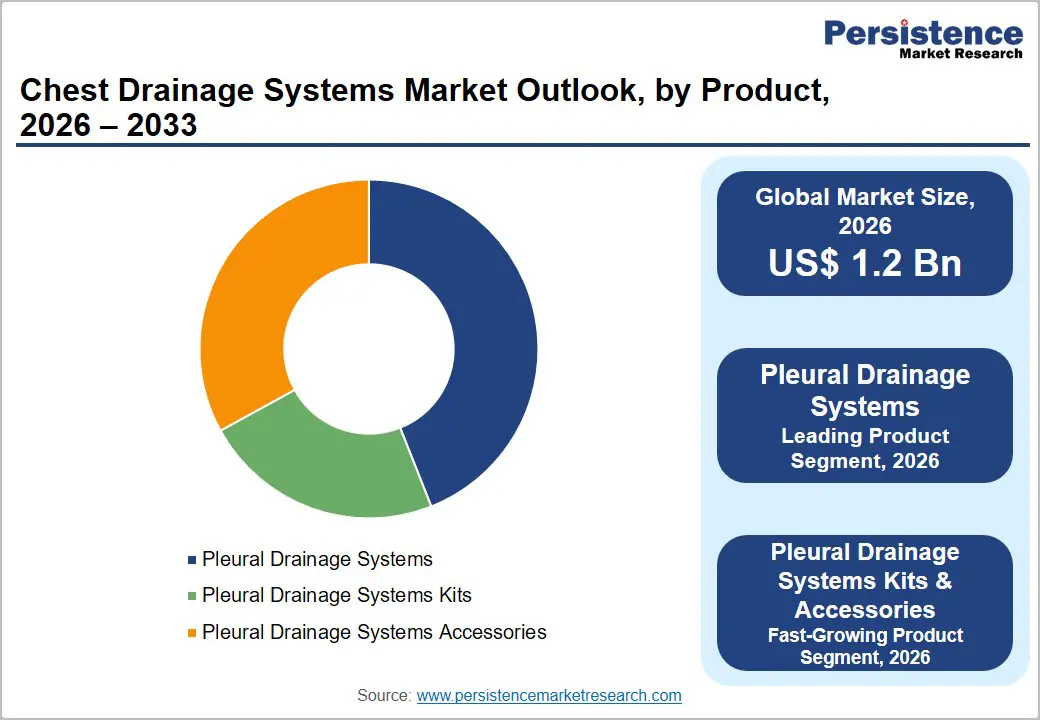

- Dominant Segment: Pleural Drainage Systems lead the product category with 44% market share in 2025, underpinned by their role as the standard-of-care intervention for pleural effusion, pneumothorax, and post-surgical thoracic drainage, supported by BTS and ACCP clinical guidelines across all major geographies.

- Fastest Growing Segment: Pleural Drainage Systems Kits & Accessories represent the fastest growing product segment over 2026–2033, driven by procedure volume growth, consumable replenishment demand, and hospital standardization on integrated drainage kits for consistency and infection control compliance.

- Key Market Opportunity: The convergence of digital pleural drainage and ambulatory care management, validated by BTS guidelines and Lancet Respiratory Medicine research, presents an incremental US$ 0.6 billion absolute dollar opportunity between 2026 and 2033, particularly for compact portable digital drainage platforms.

Market Dynamics

Drivers - Rising Incidence of Pleural Diseases and Thoracic Trauma

The increasing global burden of pleural diseases, thoracic trauma, and post-surgical complications requiring drainage represents the most significant demand driver for the chest drainage systems market. According to a clinical review published in the British Medical Journal (BMJ), pleural effusion affects approximately 1.5 million patients in the United States annually, while pneumothorax is estimated to occur in approximately 20 per 100,000 men and 6 per 100,000 women per year.

Globally, the WHO reports that road traffic injuries and thoracic traumas generate substantial emergency thoracic drainage needs across both high- and low-income countries. Additionally, the growing volume of cardiothoracic, lung resection, and esophageal surgeries globally creates consistent procedural demand for post-operative pleural drainage systems, sustaining reliable baseline revenue growth for manufacturers and distributors.

Expanding Adoption of Digital Pleural Drainage Systems in Clinical Practice

The transition from traditional water-seal chest drainage systems to digital pleural drainage platforms is an emerging clinical trend generating significant revenue uplift in advanced markets. Digital systems, such as those commercialized by Medela AG (Thopaz+®) and Getinge AB, offer real-time continuous monitoring of air leak flow rates, intrapleural pressure, and drainage volumes, enabling earlier and more objective clinical decision-making on chest tube removal.

Multiple randomized controlled trials, including studies published in The Annals of Thoracic Surgery and The Journal of Thoracic and Cardiovascular Surgery, have demonstrated that digital systems significantly reduce chest tube duration and hospital length of stay compared to traditional analog systems. These outcomes translate directly into hospital cost savings, accelerating institutional procurement decisions and supporting premium pricing for digital platforms across North America and Europe.

Restraints - High Cost of Digital Drainage Systems Limiting Adoption in Cost-Sensitive Markets

While digital pleural drainage systems offer superior clinical outcomes, their significantly higher unit cost compared to conventional water-seal systems presents an adoption barrier in government-funded and resource-limited healthcare environments. Digital platforms can cost 5 to 10 times more than traditional chest drainage units, restricting procurement to well-funded tertiary care hospitals and private health systems. In Latin America, South Asia, and Sub-Saharan Africa, limited reimbursement coverage and constrained capital equipment budgets slow the transition from analog to digital drainage technologies, moderating overall market revenue growth relative to underlying clinical demand.

Risk of Device-Associated Complications and Regulatory Compliance Burden

Chest tube insertion and pleural drainage carry inherent procedural risks, including infection, bleeding, tube malposition, and re-expansion pulmonary edema. The British Thoracic Society (BTS) guidelines acknowledge that complications from chest drain procedures are not uncommon, particularly when performed outside specialist settings. These clinical risks create medico-legal scrutiny and require stringent post-market surveillance by manufacturers. Additionally, compliance with EU MDR (Regulation 2017/745) and U.S. FDA 510(k) requirements for Class II medical devices extends product development timelines and increases regulatory compliance costs, creating barriers particularly for smaller regional manufacturers seeking to enter or expand within regulated markets.

Opportunities - Growth of Digital Pleural Drainage and Ambulatory Chest Drain Management

The convergence of digital monitoring technology and ambulatory care models is opening a high-growth commercial frontier for chest drainage system manufacturers. Portable digital drainage devices that allow patients to be managed at home or in outpatient settings following pneumothorax or pleurodesis procedures are gaining clinical validation. Research published in The Lancet Respiratory Medicine and endorsed by the British Thoracic Society (BTS) supports outpatient management of selected spontaneous pneumothorax patients using ambulatory drainage devices, significantly reducing hospitalization costs. As healthcare systems globally prioritize shifting care from inpatient to community settings, demand for compact, portable, and digitally connected chest drainage solutions is expected to accelerate. Manufacturers investing in miniaturized, battery-powered digital drainage platforms with remote monitoring capabilities are well-positioned to capture this rapidly expanding ambulatory segment through 2033.

Emerging Markets Demand Driven by Expanding Thoracic Surgery and Trauma Care Capacity

The rapid expansion of thoracic surgery programs and trauma care infrastructure across the Asia Pacific and Latin America represents a substantial incremental market opportunity for chest drainage system suppliers. China’s Healthy China 2030 initiative is driving investment in specialist surgical capacity, including cardiothoracic surgery centers, while India’s Ayushman Bharat PM-JAY scheme is expanding access to surgical care across tier-2 and tier-3 cities with a growing thoracic disease burden. The International Association for the Study of Lung Cancer (IASLC) reports increasing lung cancer incidence across East Asia, generating growing surgical resection volumes that require post-operative pleural drainage. Affordable product tiering strategies, local distribution partnerships, and regulatory approvals aligned with national frameworks in China (NMPA) and India (CDSCO) will be critical success factors for companies targeting these high-growth emerging markets.

Category-wise Analysis

Product Insights

Pleural drainage systems are likely to lead the product category, accounting for approximately 44% of the chest drainage systems market in 2026s. This dominance reflects the fundamental clinical necessity of pleural drainage systems as the primary therapeutic intervention across all major thoracic indications, including pleural effusion, pneumothorax, hemothorax, and post-cardiothoracic surgery drainage management. The segment encompasses both traditional water-seal multi-chamber systems, which maintain strong volume share in cost-sensitive settings, and the rapidly growing digital pleural drainage sub-segment. Clinical guidelines from the British Thoracic Society (BTS) and the American College of Chest Physicians (ACCP) establish chest tube drainage as the standard of care for multiple thoracic conditions, ensuring consistent prescriptive demand. The integration of suction regulation, digital air-leak monitoring, and safety features in next-generation pleural drainage systems is sustaining both volume growth and per-unit revenue expansion.

Indication Insights

Pleural effusion represents the leading indication segment in the chest drainage systems market in 2026, reflecting its status as the most prevalent thoracic condition requiring drainage intervention globally. According to clinical epidemiology data published in peer-reviewed thoracic medicine literature, pleural effusion affects an estimated 1.5 million patients annually in the U.S. alone and is associated with a wide range of underlying conditions, including congestive heart failure, malignancy, pneumonia, and cirrhosis. The American Heart Association (AHA) reports that heart failure, one of the most common causes of pleural effusion, affects over 6.2 million adults in the U.S. This large and growing patient population consistently drives thoracentesis and pleural drainage procedures, generating sustained demand for pleural drainage systems and associated consumable accessories across hospital and specialty clinic settings globally.

End-User Insights

Hospitals represent the dominant end-user segment in the chest drainage systems market in 2025, accounting for the largest share of procurement volume and revenue. Hospitals serve as the primary site of care for all major chest drainage indications from emergency pneumothorax and hemothorax management in trauma bays to elective post-thoracic surgery drainage and malignant pleural effusion management in oncology wards. The American Hospital Association (AHA) reports approximately 6,093 registered hospitals in the U.S., each maintaining thoracic drainage device inventories across emergency, surgical, and critical care departments. Globally, rapid hospital capacity expansion in China, India, and Brazil is expanding the institutional procurement base for chest drainage consumables and capital devices, reinforcing hospitals as the anchor revenue-generating end-user segment through the forecast period.

Regional Insights

North America Chest Drainage Systems Market Trends and Insights

North America is likely to lead the global chest drainage systems market with 38% share in 2026, underpinned by high thoracic disease prevalence, well-established reimbursement frameworks, and rapid adoption of digital pleural drainage systems in academic medical centers and large hospital systems. The region’s leadership is reinforced by active clinical guideline development from ACCP and ATS, promoting evidence-based drainage protocols.

U.S. Chest Drainage Systems Market Size

The United States accounts for approximately 88% of North American market revenues, driven by high annual pleural effusion incidence exceeding 1.5 million cases, a large volume of cardiothoracic surgeries, and strong adoption of premium digital drainage platforms across major hospital systems. Favorable Medicare and private insurance reimbursement for thoracic drainage procedures supports consistent high-value procurement.

Europe Chest Drainage Systems Market Trends and Insights

Europe is the second-largest regional market, characterized by universal public healthcare systems with structured procurement frameworks and growing clinical adoption of digital pleural drainage aligned with BTS and ERS (European Respiratory Society) guidelines. Increasing lung cancer surgical volumes and aging demographics across Western Europe are sustaining strong post-operative drainage demand, while EU MDR compliance requirements are consolidating market share among established manufacturers.

Germany Chest Drainage Systems Market Size

Germany accounts for an estimated 23–25% of European market revenues, driven by a large hospital network with over 1,900 registered facilities, high cardiothoracic surgery volumes, and early adoption of digital drainage systems. Germany’s statutory health insurance framework supports the procurement of advanced drainage technologies, and BOWA-electronic and Getinge AB maintain strong regional distribution presence.

U.K. Chest Drainage Systems Market Size

The U.K. contributes approximately 17–19% of European revenues. The NHS drives centralized procurement of chest drainage consumables across its trust network, with BTS guidelines serving as the primary clinical procurement standard. The UK’s growing lung cancer incidence and expanding thoracic oncology surgical programs sustain consistent demand for pleural drainage systems and ambulatory drainage devices.

France Chest Drainage Systems Market Size

France contributes approximately 14–16% of European market revenues, supported by a national hospital system of over 3,000 public and private facilities managed under Agence Régionale de Santé (ARS) frameworks. French thoracic surgery centers are increasingly adopting digital pleural drainage systems aligned with European Respiratory Society (ERS) recommendations, supporting above-average per-unit revenue growth in the country.

Asia Pacific Chest Drainage Systems Market Trends and Insights

Asia Pacific is the fastest-growing regional market for chest drainage systems in the forecast period, driven by the rise in lung cancer and tuberculosis incidence, expanding thoracic surgery capacity, and improving hospital infrastructure. China leads regional demand, with the Healthy China 2030 initiative funding specialist surgical center construction and driving procurement of modern drainage systems under NMPA regulatory oversight, while domestic manufacturers are expanding competitive product offerings.

India Chest Drainage Systems Market Size

India accounts for approximately 12% of Asia Pacific revenues, with growth driven by high tuberculosis burden. India accounts for approximately 26% of global TB cases according to the WHO Global TB Report 2023, generating significant pleural effusion management demand. Expanding private hospital cardiothoracic surgery programs and Ayushman Bharat PM-JAY coverage are accelerating the procurement of chest drainage systems across tier-1 and tier-2 cities.

Competitive Landscape

The global chest drainage systems market is highly competitive, with manufacturers focusing on technological advancements, portability, and patient safety to strengthen market position. Companies are increasingly developing digital drainage monitoring systems that improve fluid measurement accuracy, reduce manual errors, and support faster clinical decision-making. Strategic collaborations with hospitals and surgical centers, along with product launches targeting minimally invasive thoracic procedures, are intensifying market competition. Market participants are also emphasizing disposable and infection-control solutions to meet rising healthcare safety standards.

Key Developments:

- In February 2026, Medanta Hospital launched a dedicated 24x7 chest trauma support service aimed at strengthening emergency care for patients with severe chest injuries across North India. The initiative was introduced following an internal study showing that chest injuries accounted for nearly 70% of poly-trauma admissions in the NCR region.

- In October 2025, Synchrony Medical launched the LibAirty™ Airway Clearance System in the U.S. for patients with chronic lung diseases such as COPD, bronchiectasis, and cystic fibrosis. The company introduced the FDA-cleared at-home respiratory therapy device featuring synchronized chest compressions with app-guided breathing to improve mucus clearance and enhance patient comfort.

Global Chest Drainage Systems Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 0.9 Billion |

|

Current Market Value (2026) |

US$ 1.2 Billion |

|

Projected Market Value (2033) |

US$ 1.8 Billion |

|

CAGR (2026–2033) |

5.9% |

|

Leading Region |

North America, 38% market share (2026) |

|

Dominant Product (Category-1) |

Pleural Drainage Systems, 44% market share (2026) |

|

Top-ranking Indication (Category-2) |

Pleural Effusion, leading share (2026) |

|

Incremental Opportunity |

US$ 600 Million (2026–2033) |

Companies Covered in Chest Drainage Systems Market

- Medtronic

- Teleflex Incorporated

- Becton, Dickinson and Company

- Getinge AB

- Smiths Medical

- Cook Medical

- Cardinal Health

- Medela AG

- Vygon SA

- Redax S.p.A.

- Rocket Medical plc

- ATMOS MedizinTechnik GmbH & Co. KG

- Utah Medical Products, Inc.

Frequently Asked Questions

The global chest drainage systems market is projected to be valued at US$ 1.2 billion in 2026.

Growing volumes of cardiac and thoracic surgeries, particularly minimally invasive procedures, are further supporting product adoption. Increasing cases of traumatic chest injuries caused by road accidents and emergency conditions are also accelerating demand in hospitals and trauma centers.

North America leads with approximately 38% market share in 2025, anchored by high thoracic disease prevalence, strong Medicare and private insurance reimbursement for drainage procedures, and widespread adoption of premium digital pleural drainage systems, including the Thopaz+® from Medela AG across major U.S. hospital systems and academic medical centers.

A key growth opportunity in the Chest Drainage Systems Market lies in the increasing adoption of digital and portable drainage systems in minimally invasive thoracic and cardiac procedures.

Key players include Medtronic, Teleflex Incorporated, Becton Dickinson and Company, Getinge AB, Medela AG, Smiths Medical, Cook Medical, Cardinal Health, Vygon SA, Redax S.p.A., Rocket Medical plc, ATMOS MedizinTechnik GmbH & Co. KG, Utah Medical Products Inc., Argon Medical Devices, and Poly Medicure Ltd.