- Medical Devices

- Cervical Total Disc Replacement Market

Cervical Total Disc Replacement Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Cervical Total Disc Replacement Market by Device Type (Metal on a Biocompatible Material (M-o-B), Metal on Metal (M-o-M)), Indication (Constrained Discs, Semi Constrained Discs, Unconstrained Discs), Material (Cobalt Chromium, Titanium, Ceramic, Others), End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers), and Regional Analysis from 2026 to 2033

Cervical Total Disc Replacement Market Size and Share Analysis

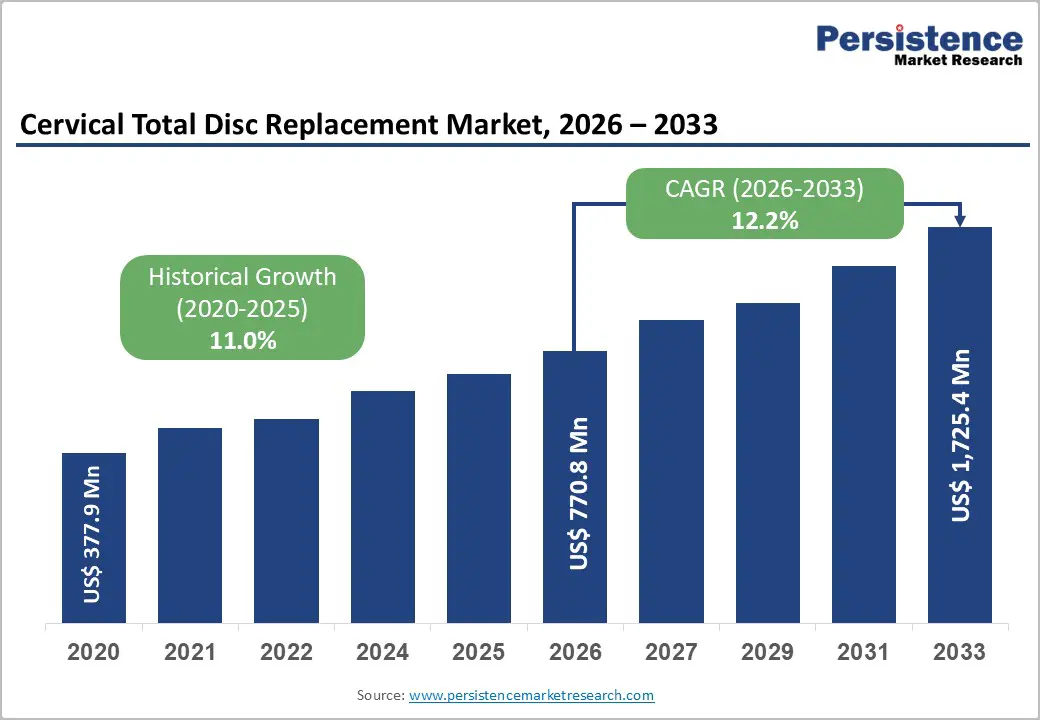

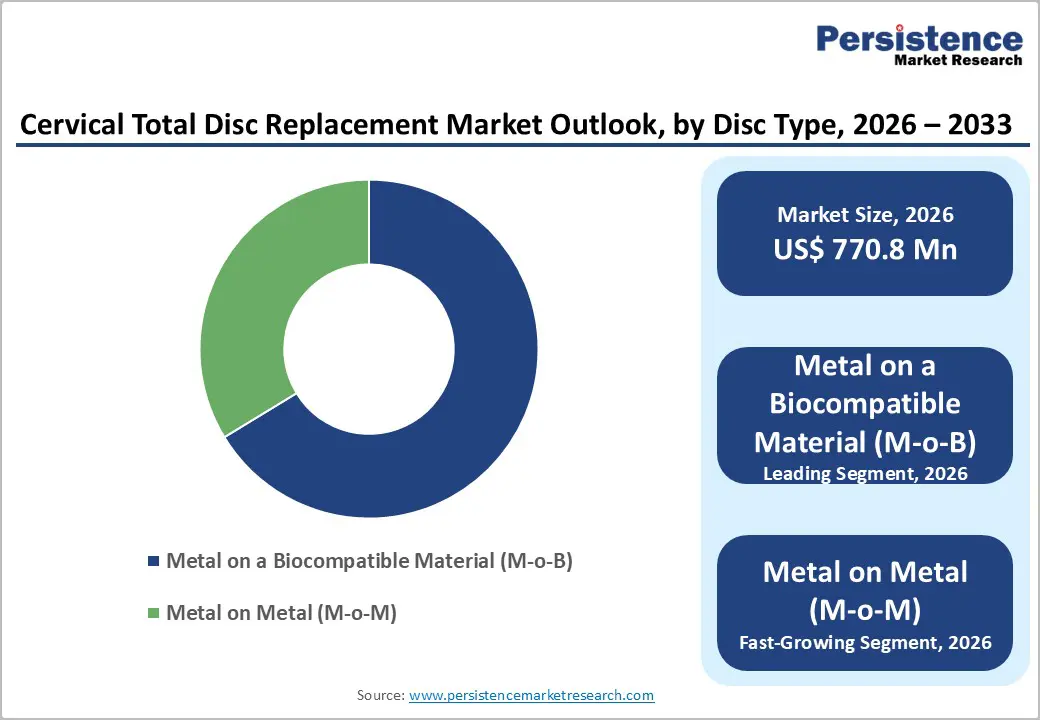

The global cervical total disc replacement market is estimated to grow from US$ 770.8 Mn in 2026 to US$ 1,725.4 Mn by 2033. The market is projected to record a CAGR of 12.2% during the forecast period from 2026 to 2033.

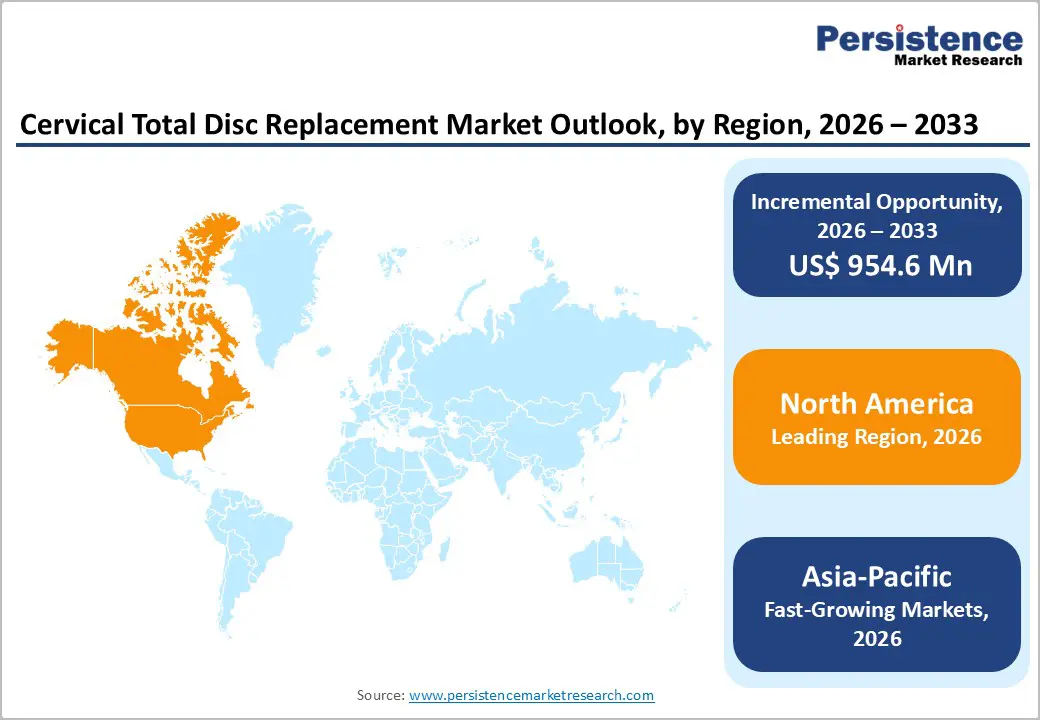

The global cervical total disc replacement market is expanding steadily, driven by rising prevalence of cervical degenerative disc disease, growing preference for motion-preserving spine surgeries, and technological advancements in implant design. North America dominates due to advanced spine care infrastructure and early adoption, while Asia-Pacific is the fastest-growing region, supported by expanding hospitals, rising patient volumes, improving access to spine surgery, and increasing awareness.

Key Industry Highlights

- Dominant Segment: Metal-on-biocompatible material cervical discs account for the largest market share in 2025 with 66.3% , driven by superior durability, improved range of motion, reduced wear rates, and strong clinical outcomes. Adoption is high across hospitals and specialty spine centers due to proven long-term safety and surgeon familiarity.

- Dominant Region: North America leads the market in 2025 with 43.8% share, supported by advanced spine surgery infrastructure, high procedure volumes, favorable reimbursement, and early adoption of motion-preserving technologies. Asia-Pacific is the fastest-growing region, driven by expanding spine care facilities, rising degenerative disc disease prevalence, improving access to advanced surgeries, and growing patient awareness.

- Market Drivers: Growth is driven by increasing incidence of cervical degenerative disc disease, rising geriatric population, growing preference for motion-preserving alternatives to fusion, shorter recovery times, and continuous advancements in cervical disc implant materials and designs.

- Market Opportunity: Key opportunities include next-generation cervical discs with enhanced biomechanics, minimally invasive implantation techniques, expansion into emerging markets, increasing outpatient spine surgeries, and rising adoption in younger, active patient populations seeking mobility-preserving treatments.

| Report Attribute | Details |

|---|---|

|

Global Cervical Total Disc Replacement Market Size (2026E) |

US$ 770.8 Mn |

|

Market Value Forecast (2033F) |

US$ 1,725.4 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

12.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.0% |

Market Dynamics

Driver: Rising prevalence of cervical degenerative disc disease and cervical spondylosis

The rising prevalence of cervical degenerative disc disease and cervical spondylosis significantly drives demand for cervical total disc replacement procedures. Degenerative changes in cervical discs increase with age, with radiographic evidence found in about 25 percent of individuals under 40, 50 percent of those over 40, and up to 85 percent of people older than 60, reflecting a large and growing affected population globally. Symptomatic cervical spondylosis often manifests as neck pain and neurological symptoms, contributing to high clinical demand for interventions that preserve motion and function. These demographic and disease trends underscore the growing clinical need for motion-preserving surgical solutions.

Global neck pain, a common symptom of cervical degenerative pathologies including spondylosis, affected an estimated 203 million people in 2020, with numbers projected to rise by more than 30 percent to approximately 269 million by 2050 due primarily to population growth and ageing. The high and increasing prevalence of neck-related disability reflects the substantial burden of cervical degenerative conditions. These epidemiological trends fuelling symptomatic demand emphasize the expanded patient pool seeking advanced surgical interventions like cervical total disc replacement.

Restraints: High procedure and implant costs compared to conventional fusion surgeries

High procedure and implant costs represent a key restraint for the Cervical Total Disc Replacement market relative to conventional fusion surgeries. In the United States, artificial disc replacement procedures often cost between approximately $25,000 and $70,000, reflecting advanced implants and surgical resources, whereas cervical fusion costs can sometimes fall in similar but occasionally lower ranges depending on levels and complexity. Medicare reimbursement–based analyses show that cervical total disc replacement incurred higher average costs than anterior cervical discectomy and fusion (ACDF) by about $2,139 over a 24-month period, indicating greater upfront financial burden. This higher price point can constrain adoption, especially where payer coverage is limited.

Cost variability across regions further illustrates this restraint. In major healthcare markets like the U.S., spine surgeries including cervical disc replacement may exceed typical procedural costs due to implant technology and hospital charges, deterring patients without comprehensive insurance support. Comparatively, in countries like India, artificial disc replacement can still be expensive relative to local incomes even if lower in absolute terms, with procedures ranging broadly. The often elevated upfront costs combined with variable insurance coverage and reimbursement policies create a financial barrier that can slow wider utilization of cervical total disc replacement despite clinical benefits.

Opportunity: Expanding adoption in emerging economies with improving spine care infrastructure

Expanding adoption in emerging economies is a key opportunity for the Cervical Total Disc Replacement market as spine care infrastructure and access improvement. In India, government healthcare reforms have significantly strengthened hospital and tertiary care capacity; over 31,000 hospitals are empanelled under Ayushman Bharat, with more than 9.84 crore hospital admissions authorised under the scheme as of July 2025, indicating broader access to advanced surgical interventions. This expansion enhances the likelihood that complex spine procedures, including disc replacement, will become more accessible to larger segments of the population. Greater hospital coverage and rising admissions reflect ongoing improvements in surgical infrastructure.

Emerging economies also show rising healthcare investment and workforce capacity that support advanced procedures. India’s healthcare sector is rapidly growing, with increased doctor numbers and expanded medical education infrastructure, strengthening surgical care delivery. Moreover, reductions in out-of-pocket expenditures, from above 60 percent in 2014 to under 40 percent in 2024 demonstrate gradual improvement in financial access to healthcare, which can increase uptake of costly procedures. These trends indicate that as spine care infrastructure and insurance coverage expand, adoption of advanced treatments like cervical total disc replacement is expected to rise in emerging markets.

Category-wise Analysis

By Disc Type, Metal on a Biocompatible Material (M-o-B) Dominates the Cervical Total Disc Replacement Market

Metal on a Biocompatible Material (M-o-B) occupies 66.3% share of the global market in 2025, because their constituent materials typically titanium alloys or cobalt-chromium alloys, offer excellent biocompatibility, corrosion resistance, and mechanical strength, enabling durable fixation and physiological motion at the cervical segment. Titanium alloys, in particular, promote osseointegration due to a modulus of elasticity closer to bone, reducing stress shielding and improving long-term stability, while cobalt-chromium components exhibit high wear resistance necessary for repetitive cervical motion. Clinical evidence indicates that metal devices demonstrate favorable postoperative imaging and reliable motion preservation, which supports surgeon preference, implant longevity, and patient outcomes compared to alternative materials with higher wear or less mechanical compatibility.

By Design, Semi-constrained discs dominate by preserving cervical motion while ensuring stability, reducing adjacent degeneration and revision risks

Semi-constrained disc designs dominate the cervical total disc replacement market because they balance stability and mobility in a manner that closely replicates natural cervical spine kinematics, making them suitable for a wide range of patients. Semi-constrained devices allow controlled translation and rotation, helping preserve segmental motion while moderating excessive movement that could stress surrounding tissues, which contrasts with fully unconstrained or overly rigid constrained designs. Clinical evidence indicates that semi-constrained designs are associated with lower risk of adjacent segment degeneration and index level reoperation compared with some constrained alternatives, while maintaining superior motion preservation versus fusion procedures like ACDF. Their biomechanical profile supports functional outcomes and reduces long-term complications, driving surgeon preference and broader adoption.

Regional Insights

North America Cervical Total Disc Replacement Market Trends

North America dominates the cervical total disc replacement market with 43.8% share in 2025, because of its advanced healthcare infrastructure, high procedural volumes, and robust reimbursement environment. In the United States, specialized spine centers routinely perform complex cervical procedures, supported by clear regulatory pathways through the FDA and coverage from Medicare and major private insurers, which expands patient access. Neck pain affects about 15?percent of American adults annually, creating a substantial clinical population for surgical intervention when conservative care fails. The region accounts for over 40?percent of global cervical disc replacements, with tens of thousands of procedures performed annually, reflecting strong clinical adoption and technological uptake.

Europe Cervical Total Disc Replacement Market Trends

Europe is an important region for the cervical total disc replacement market because it combines a high burden of spinal disorders, advanced healthcare systems, and broad procedural access across multiple countries. OECD data show that intervertebral disc disorders account for up to 4.9–21.1?% of musculoskeletal hospital discharges in European nations, reflecting substantial clinical demand for spine interventions. Public healthcare systems in Germany, France, the United Kingdom, Italy, and other EU countries ensure widespread availability of diagnostic tools such as MRI and CT scans, and promote motion?preserving procedures through structured clinical pathways. An aging demographic with roughly 21?percent of Europeans aged 65 and older further increases prevalence of degenerative cervical conditions requiring surgical solutions.

Asia-Pacific Cervical Total Disc Replacement Market Trends

Asia?Pacific is the fastest growing region in the cervical total disc replacement market due to rapid improvements in healthcare infrastructure, rising surgical capacity, and demographic trends. Governments across China, India, Japan, and Southeast Asia are expanding hospital networks, increasing access to advanced surgical care, and investing in modern operating suites capable of complex spine procedures, which supports adoption of motion?preserving surgeries. The region’s aging population Asia contains a growing share of the global elderly demographic drives higher prevalence of degenerative cervical conditions requiring surgical intervention. Additionally, expanding medical tourism and lower procedural costs attract both domestic and international patients, further accelerating uptake of cervical disc replacement in the region.

Market Competitive Landscape

The cervical total disc replacement market is competitive, driven by global and regional players focusing on device safety, durability, and surgical efficiency. Innovation in implant materials, semi-constrained designs, minimally invasive procedures, and imaging-guided techniques, along with strategic partnerships and hospital network expansion, intensifies competition, enhances clinical outcomes, and differentiates offerings across the growing global spine surgery landscape.

Key Industry Developments:

- In January 2026, VB Spine completed the acquisition of Stryker’s Cestas manufacturing facility, strengthening its production capabilities for spinal implants. The purchase allows VB Spine to expand manufacturing capacity, streamline supply chains, and accelerate delivery of advanced spinal solutions to global markets. The acquisition reflects VB Spine’s strategic focus on scaling operations and enhancing its presence in key regions for spine care.

- In October 2025, Synergy Spine Solutions and Johnson & Johnson MedTech extended their strategic collaboration into Germany, aiming to enhance the availability of advanced cervical spine solutions. The partnership focused on expanding the distribution of Synergy’s innovative spinal implants and technologies within the German market, leveraging Johnson & Johnson’s established healthcare network to improve surgeon access and patient outcomes across the region.

Companies Covered in Cervical Total Disc Replacement Market

- LDR Holdings

- Johnson and Johnson

- Medtronic

- Globus Medical, Inc.

- NuVasive Inc.

- Stryker Corporation

- Orthofix Medical Inc.

- Centinel Spine, Inc.

- FH Orthopedics S. A. S.

- Zimmer Biomet Holdings, Inc

- Spine Innovations

- AxioMed LLC

- Others

Frequently Asked Questions

The global cervical total disc replacement market is projected to be valued at US$ 770.8 Mn in 2026.

Rising cervical degenerative disc disease, aging population, motion-preserving preference, advanced implants, and shorter recovery drive growth.

The global cervical total disc replacement market is poised to witness a CAGR of 12.2% between 2026 and 2033.

Next-generation implants, minimally invasive surgery, emerging economies, outpatient procedures, and increased patient awareness present key opportunities.

LDR Holdings, Johnson and Johnson, Medtronic, Globus Medical, Inc., NuVasive Inc., Stryker Corporation.