- Medical Devices

- Cervical Spacer Systems Market

Cervical Spacer Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Cervical Spacer Systems Market by Spacer (12x12mm, 12x14mm, 14x16mm, 16x18mm), Material (PEEK Radiolucent Polymer, Metal, Alloy), and Regional Analysis for 2026 - 2033

Cervical Spacer Systems Market Size and Trends Analysis

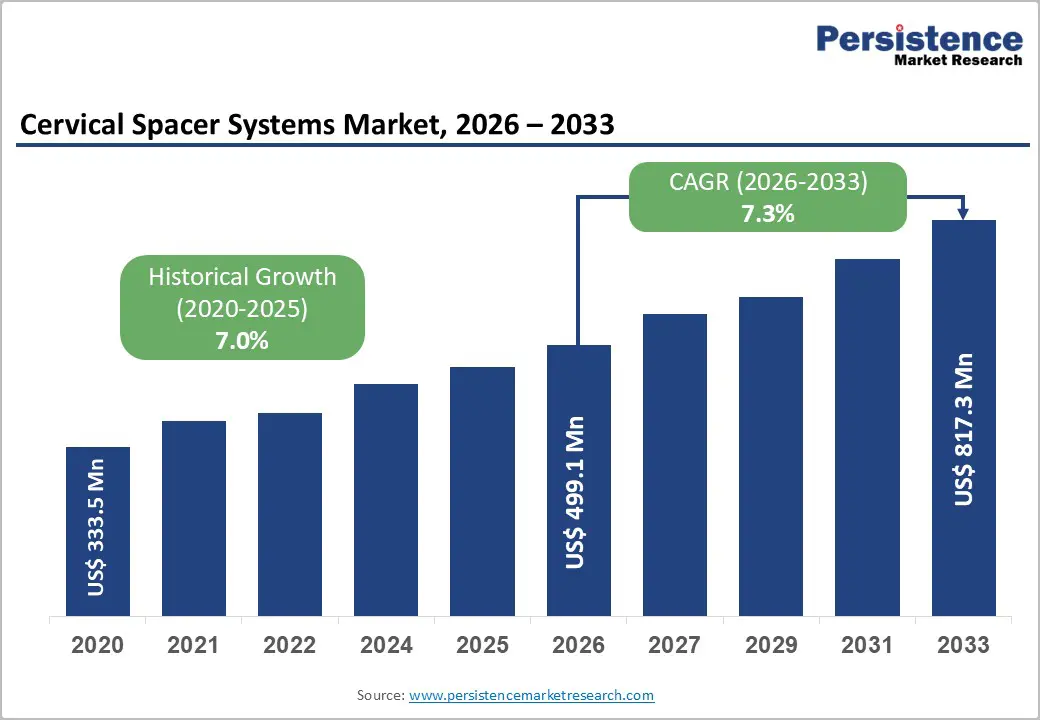

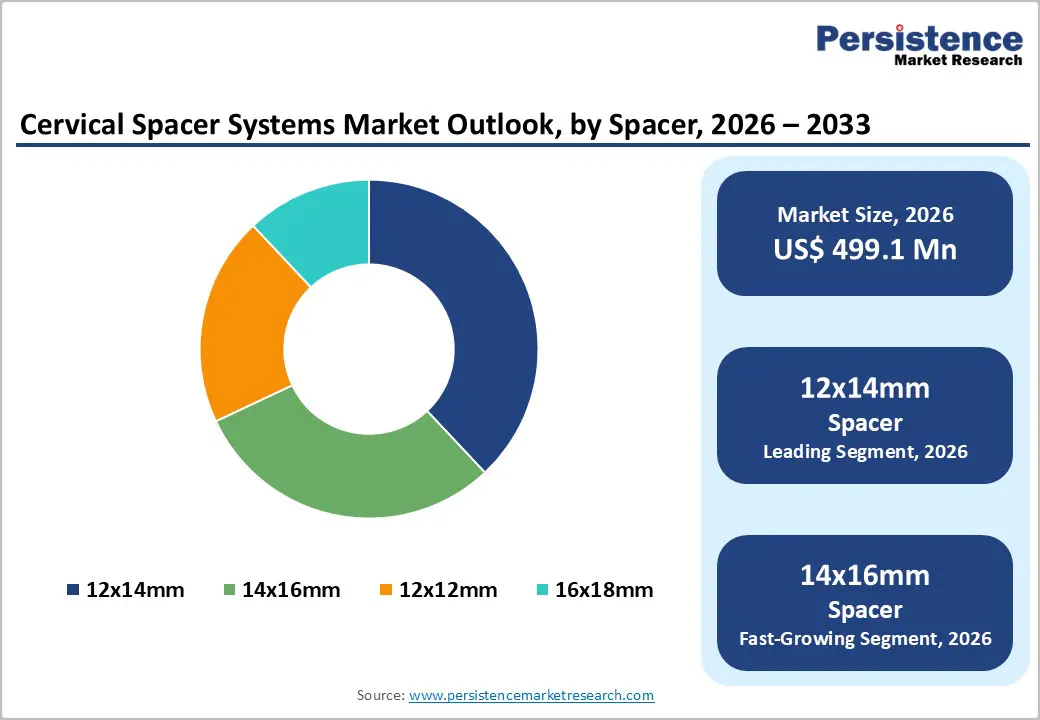

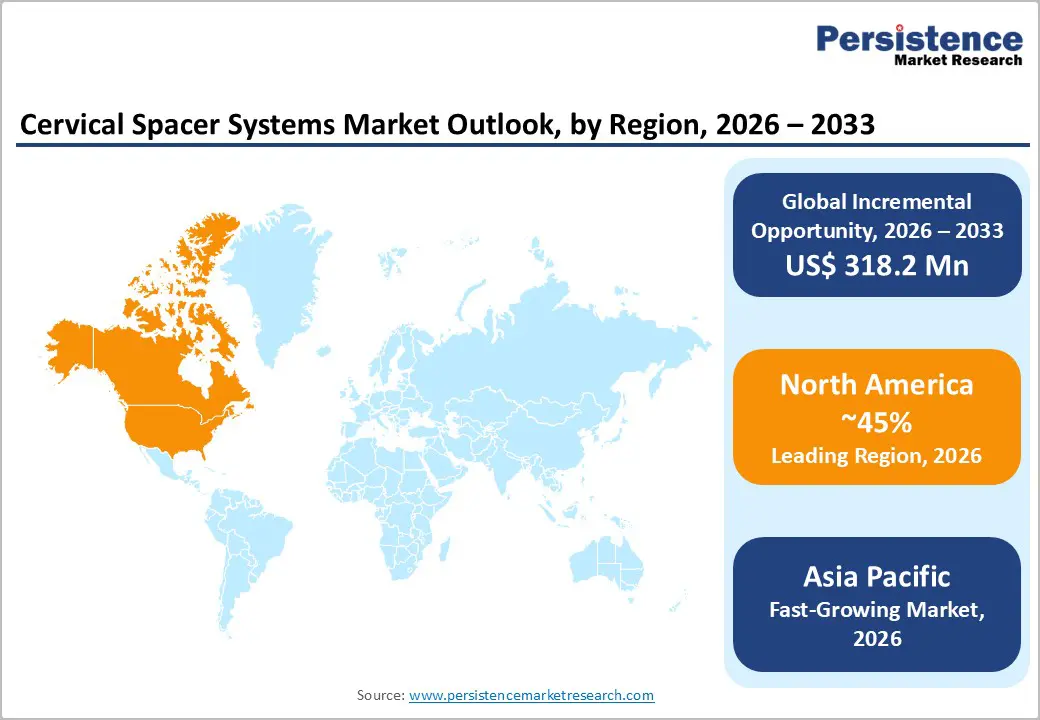

The global cervical spacer systems market size is likely to be valued at US$499.1 million in 2026, and is expected to reach US$817.3 million by 2033, growing at a CAGR of 7.3% during the forecast period from 2026 to 2033, driven by the increasing prevalence of degenerative disc disease and cervical spondylosis in aging populations, rising demand for motion-preserving spinal implants, and growing adoption of minimally invasive anterior cervical discectomy and fusion (ACDF) procedures.

The growing demand for PEEK radiolucent cervical spacers, particularly 12x14mm and 14x16mm sizes, is driving adoption in hospitals and surgery centers. Advances in zero-profile spacers, bioactive coatings, and 3D-printed, patient-specific designs are enhancing fusion rates and reducing the risk of dysphagia. Cervical spacer systems are increasingly recognized for their role in restoring disc height, stabilizing segments, and preserving motion, fueling market growth.

Key Industry Highlights:

- Leading Region: North America, anticipated to account for a 45% market share in 2026, driven by high procedure volumes, advanced reimbursement, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by a rising geriatric population, increasing spinal surgery rates, and expanding healthcare infrastructure in China and India.

- Dominant Spacer Size: 12x14mm, to hold approximately 38% of the market share, as it remains the most used size for average disc heights.

- Leading Material: PEEK radiolucent polymer, contributing nearly 68% of the market revenue, due to superior radiolucency and biomechanical compatibility.

- In the U.S., the FDA regulates cervical spacers under the 510(k) pathway as Class II devices per 21 CFR 888.3080. Manufacturers must show substantial equivalence to predicate devices before commercialization. For instance, Reliance Medical Systems received FDA 510(k) clearance for its Cervical IBF System (K202266).

| Key Insights | Details |

|---|---|

| Cervical Spacer Systems Market Size (2026E) | US$499.1 Mn |

| Market Value Forecast (2033F) | US$817.3 Mn |

| Projected Growth CAGR (2026 - 2033) | 7.3% |

| Historical Market Growth (2020 - 2025) | 7.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Aging Population and Rising Cervical Spine Procedures

The world’s population is aging rapidly, with the number of people aged 60 years and older projected to rise from around 1.1 billion in 2023 to 1.4 billion by 2030, as life expectancy increases and fertility rates decline. This demographic shift leads to a higher prevalence of age-related degenerative conditions of the spine, including cervical spondylosis, disc degeneration, and spinal stenosis, which are more common with advancing age. Older adults experience wear-and-tear changes in spinal discs and joints that often result in pain, neurological symptoms, and functional impairment, making surgical intervention increasingly necessary to relieve symptoms and restore spinal stability.

Rising surgical volumes reflect this trend, with anterior cervical surgeries continuing to be a common intervention for degenerative cervical pathologies globally. Historical data from the U.S. showed a significant increase in cervical spine procedures over time, indicating growing treatment utilization among aging adults. As more patients require surgical solutions to address complex cervical spine disorders, demand for cervical spacer systems that support fusion and alignment during surgery intensifies, stimulating market growth for advanced implants and instrumentation used in these procedures.

Shift Toward Motion-Preserving and Outpatient Procedures

The healthcare industry is witnessing a clear shift toward motion-preserving and outpatient procedures, driven by a combination of technological advancements, patient preferences, and cost considerations. Motion-preserving procedures, such as artificial disc replacements in spinal surgeries, aim to maintain the natural movement of affected body parts while alleviating pain and restoring function. These procedures reduce the long-term risk of adjacent segment degeneration, a common issue with traditional fusion surgeries, and promote faster rehabilitation, allowing patients to regain mobility sooner. Outpatient procedures are gaining traction due to their efficiency, lower infection risks, and reduced healthcare costs.

Minimally invasive techniques, advanced anesthesia, and improved post-operative care enable patients to undergo complex interventions without extended hospital stays. This approach enhances patient comfort and convenience while allowing hospitals and clinics to optimize bed utilization and reduce operational expenses. The convergence of motion-preserving and outpatient strategies aligns with broader healthcare trends emphasizing value-based care. Patients increasingly prefer procedures that minimize downtime and preserve quality of life. Surgeons are adopting innovative tools and imaging technologies to ensure precision and safety in outpatient settings. Government healthcare initiatives and reimbursement policies supporting less invasive and cost-effective procedures further encourage the adoption of these approaches, shaping the future of surgical care.

Barrier Analysis - High Device Cost and Reimbursement Pressure

High device costs and reimbursement pressures are significant challenges in modern healthcare, particularly for advanced medical procedures and technologies. Innovative devices, such as motion-preserving implants, robotic surgical tools, and specialized orthopedic systems, often involve complex engineering, high-quality materials, and extensive regulatory compliance. These factors drive up manufacturing costs, which are then reflected in the prices hospitals and patients pay. High device costs can limit accessibility, especially in regions with constrained healthcare budgets, and can lead hospitals to prioritize cost-effective alternatives over technologically advanced options.

Reimbursement pressure further complicates adoption. Healthcare payers, including government programs and private insurers, are increasingly scrutinizing medical device pricing, often offering limited coverage or requiring stringent justification for reimbursement. Hospitals and providers face challenges in aligning device costs with reimbursement levels while maintaining profitability. In some cases, delays or denials in reimbursement can discourage the use of advanced devices, slowing the uptake of innovation. Balancing technological benefits with affordability remains a critical concern, requiring collaboration among manufacturers, payers, and healthcare providers to ensure patients receive effective care without undue financial burden.

Regulatory and Clinical Evidence Requirements

Regulatory and clinical evidence requirements are critical factors influencing the development, approval, and adoption of medical devices and procedures. Regulatory authorities, such as the U.S. Food and Drug Administration (FDA) or the European Medicines Agency (EMA), mandate rigorous evaluation processes to ensure the safety, efficacy, and quality of medical technologies. Manufacturers must provide comprehensive data from preclinical studies, bench testing, and clinical trials before a device can enter the market. These regulations are designed to protect patients from potential risks, but also add significant time and financial investment to product development.

Clinical evidence is equally essential for market acceptance. Physicians, hospitals, and payers increasingly demand robust real-world and trial-based data demonstrating device effectiveness, durability, and safety compared to standard treatments. Randomized controlled trials, long-term follow-ups, and post-market surveillance studies are often required to build confidence among stakeholders. Without sufficient clinical evidence, even innovative devices may face slow adoption, limited reimbursement, or regulatory delays.

Opportunity Analysis - Growth in Zero-Profile and 3D-Printed Cervical Spacers

The increasing adoption of zero-profile and 3D-printed cervical spacers presents a significant opportunity for the cervical spacer systems market. Zero-profile spacers are designed to sit entirely within the disc space without anterior protrusion, reducing soft-tissue irritation. Clinical outcomes demonstrate that the use of zero-profile devices in anterior cervical discectomy and fusion (ACDF) can maintain fusion rates comparable to those of traditional plate-and-cage systems while significantly reducing the rate of post-operative dysphagia. One study reported only 5.6% incidence of dysphagia with zero-profile devices versus much higher rates historically seen with anterior plating in multilevel surgeries. These clinical advantages can make zero-profile spacers preferable for surgeons and patients, supporting broader clinical adoption.

Three-dimensional (3D) printing adds another dimension of benefit by enabling patient-specific and optimized implant geometries that can promote better anatomical fit and bone integration. The U.S. FDA notes that 3D-printed medical devices, including orthopedic implants, are increasingly reviewed and cleared, with more than 100 devices already assessed through regulatory pathways. This regulatory acceptance reflects the maturation of additive manufacturing in medical applications and helps reduce barriers to market entry.

Enhanced Patient-Specific Solutions

Patient-specific solutions represent a key opportunity in the cervical spacer systems market by enabling devices that more precisely match an individual’s anatomy and biomechanical needs. Customized implants and digital surgical planning can improve implant fit and load distribution across vertebral endplates, potentially reducing complications such as subsidence and nonunion seen with off-the-shelf devices. The U.S. Centers for Medicare & Medicaid Services (CMS) has acknowledged the clinical importance of personalized devices by granting New Technology Add-On Payment (NTAP) status for cervical fusion procedures using customized interbody implants, providing up to an additional US$21,125 in reimbursement on top of standard payments for qualifying cases beginning in the 2025 fiscal year. This policy endorsement from a major government payer underscores strong potential uptake and supports hospital investment in personalized spacers.

Wider use of patient-specific cervical spacers has the potential to enhance surgical outcomes and align with value-based care objectives by tailoring interventions to each patient’s unique spinal morphology. Personalized devices designed with advanced imaging and planning software may encourage adoption among surgeons seeking improved alignment correction and better long-term results, especially in complex or multilevel cases where standard implants are less ideal. Financial incentives such as NTAP reimbursements further enhance their appeal within healthcare systems focused on outcome-driven care.

Category-wise Analysis

Spacer Insights

The 12x14mm segment is anticipated to dominate the market, accounting for approximately 38% of the market share in 2026. Its dominance is driven by versatile size, which suits a broad range of patient anatomies and surgical scenarios. Its dimensions offer an optimal balance between stability and load distribution, reducing risks of subsidence or implant migration. Surgeons favor this size for single-level and multilevel cervical fusions, enabling predictable outcomes and easier implantation. The combination of clinical reliability, widespread applicability, and compatibility with standard surgical techniques makes the 12x14mm spacer highly preferred. Kodiak Cervical Implant by MET 1 Technologies, LLC, which is specifically manufactured in a 12×14 mm size used in anterior cervical fusion procedures. This device is designed to improve spinal stability while supporting fusion and is commercially distributed in the U.S. with a 12 mm depth and 14 mm width, accommodating varying patient anatomy.

The 14x16mm segment is the fastest-growing, driven by an optimal balance of support and anatomical fit. Surgeons increasingly prefer this size for patients requiring enhanced spinal stability without excessive bone removal, allowing for better fusion outcomes and reduced post-operative complications. Its dimensions accommodate a wider range of cervical vertebrae anatomies, improving implant versatility and procedural efficiency. Hospitals and surgical centers are stocking this size more frequently, reflecting growing demand. Globus Medical, Inc. offers the COLONIAL™ ACDF spacer, which includes a 14×16 mm footprint option used in anterior cervical discectomy and fusion (ACDF) procedures. This size provides surgeons with an implant that balances anatomic fit and load-bearing capacity for patients undergoing multi-level fusion, helping maintain cervical alignment while resisting subsidence.

Material Insights

PEEK, a radiolucent polymer, is expected to dominate the market, accounting for nearly 68% of revenue in 2026, driven by clinical and operational advantages. Radiolucency enables clear post-operative imaging to assess fusion progress without artifact interference, improving follow-up decisions. The material offers a modulus of elasticity closer to that of cortical bone than that of metals, supporting load sharing and reducing subsidence risk. PEEK resists corrosion, maintains dimensional stability under cyclic loads, and tolerates sterilization methods used in operating rooms. Cervical Peek Cage Curved Shape is a radiolucent cervical spacer made from medical-grade PEEK polymer. PEEK’s radiolucency allows surgeons and radiologists to clearly visualize bone healing and fusion progression on X-rays and CT scans, without artifacts from metal interference, improving post-operative assessment accuracy.

Alloy represents the fastest-growing material, with its superior mechanical strength, fatigue resistance, and ability to support load in complex spinal fusion cases. Alloys provide robust construct stability and long-term durability, which is critical in multi-level or severe degenerative conditions. Their adaptability to 3D printing and porous-surface technologies enhances bone ingrowth, further improving fusion outcomes and expanding clinical adoption among spine surgeons. The TigerShark® C 3D-Printed Titanium Cervical Spacer by ChoiceSpine is a titanium alloy implant designed for anterior cervical discectomy and fusion, featuring a porous BioBond® structure to promote bone graft placement and structural support.

Regional Insights

North America Cervical Spacer Systems Market Trends

North America is projected to dominate, accounting for nearly 45% of the revenue in 2026, fueled by the region’s high ACDF procedure volumes, advanced reimbursement, and high public awareness of motion-preserving benefits. Distribution systems in the U.S. and Canada provide extensive support for cervical spacer programs, ensuring wide accessibility across 12x14mm, PEEK, and hospital populations. The increasing demand for zero-profile, convenient, and easy-to-implant forms is further accelerating adoption, as these formats improve outcomes and reduce the barriers associated with traditional cages.

Innovation in cervical spacer technology, including stable, zero-profile designs, improved bioactive delivery, and targeted outpatient enhancements, is attracting significant investment from both public and private sectors. Government initiatives and CMS campaigns continue to promote use against fusion risks, dysphagia concerns, and emerging motion-preservation threats, creating sustained market demand. The growing focus on 14x16mm grades and specialty uses, particularly in standard ACDF and other applications, is expanding the target applications for cervical spacer systems.

Europe Cervical Spacer Systems Market Trends

The growth of Europe is increasing awareness of motion-preserving benefits, strong regulatory systems, and government-led outpatient spine programs. Countries such as Germany, the U.K., France, and Italy have well-established spine surgery frameworks that support routine cervical spacer use and encourage adoption of innovative zero-profile delivery methods. These high-performance formulations are particularly appealing for 12x14mm populations, regulation-conscious hospitals, and outpatient users, improving fusion rates and coverage rates.

Technological advancements in cervical spacer development, such as enhanced bioactive coatings, application-targeted delivery, and improved alloy grades, are further boosting market potential. European authorities are increasingly supporting research and trials for spacers against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-dysphagia options aligns with the region’s focus on reducing the risk of complications and expanding outpatient care. Public awareness campaigns and promotion drives are expanding reach in both hospital and ASC segments, while suppliers are investing in radiolucent materials and novel variants to increase efficacy.

Asia Pacific Cervical Spacer Systems Market Trends

Asia Pacific is likely to be the fastest-growing market for cervical spacer systems in 2026, driven by rising awareness of degenerative spine conditions, expanding government initiatives, and expanding application programs across the region. Countries, including China, India, Japan, and South Korea, are actively promoting spacer campaigns to address the aging population and emerging spine surgery needs. Cervical spacer systems are particularly attractive in these regions due to their scalable administration, ease of adoption, and suitability for large-scale hospital and outpatient drives in both urban and semi-urban populations.

Technological advancements are enabling the development of stable, effective, and easy-to-implant cervical spacer systems that can withstand challenging patient profiles and minimize reliance on revisions. These innovations are critical for reaching domestic hospitals and improving overall spine care coverage. The growing demand for 12x14mm PEEK and standard applications is driving market expansion. Public-private partnerships, increased healthcare expenditure, and rising investment in space research and production capacity are further accelerating growth. The convenience of spacer delivery, combined with improved stability and reduced risk of complications, positions it as a preferred choice.

Competitive Landscape

The global cervical spacer systems market is shaped by competition between established spine implant leaders and emerging motion-preservation specialists. In North America and Europe, Medtronic and NuVasive maintain leadership through sustained R&D investment, dense surgeon training networks, and long-term hospital partnerships. Their zero-profile device programs and PEEK-based spacer portfolios support faster procedures, lower profile-related complications, and predictable post-operative imaging.

Across Asia Pacific, regional manufacturers expand access with cost-competitive cervical spacers, helping hospitals adopt modern ACDF workflows at scale. Wider PEEK adoption improves radiolucency, reduces imaging artifacts during follow-up, and supports standardized integration across high-volume cervical fusion programs. Strategic partnerships, collaborations, and acquisitions consolidate design, manufacturing, and clinical expertise, accelerating time-to-market and portfolio breadth. Zero-profile formulations mitigate dysphagia risk and suit shorter stays, driving uptake in ambulatory and outpatient surgical settings.

Key Industry Developments:

- In August 2025, Carlsmed, Inc. announced that CMS granted NTAP reimbursement under the FY 2026 IPPS Final Rule for cervical fusion procedures using its aprevo® personalized interbody implants.

- In October 2023, Spine Wave, a leading provider of spine surgery solutions, and eCential Robotics, a growth MedTech company that designs and produces an open platform unifying robotics, surgical navigation, and 2D/3D robotic imaging, today announced they have entered into a long-term collaboration agreement. The collaboration, involving development, marketing, and commercialization, will deliver an optimized solution and enhance robotic spine surgery.

- In September 2023, ChoiceSpine LLC received standalone FDA clearance to market the Blackhawk® Ti 3D Printed Cervical Spacer System. The company launched the device with preassembled integrated anchor technology and a cam-locking mechanism. Blackhawk® Ti used BioBond® 3D-printed porous titanium structure and launched in two anatomical footprints, with large graft space and lateral windows for improved visual confirmation.

Companies Covered in Cervical Spacer Systems Market

- Life Spine

- Exactech

- Stryker

- Zimmer Biomet

- Medtronic

- DePuy Synthes

- NuVasive

- Globus Medical

- Orthofix

- Paonan Biotech

Frequently Asked Questions

The global cervical spacer systems market is projected to reach US$499.1 million in 2026.

Rising cervical degenerative disorders and trauma cases have increased demand for fusion procedures and spacer systems.

The cervical spacer systems market is poised to witness a CAGR of 7.3% from 2026 to 2033.

Growing uptake of personalized and AI-assisted implant planning created demand for patient-specific cervical spacers.

Medtronic, NuVasive, Zimmer Biomet, Stryker, and Globus Medical are the key players.