- Healthcare IT

- E-Clinical Solution Market

E-Clinical Solution Market Size, Trends, Share, Growth, and Regional Forecast, 2025 - 2032

E-Clinical Solution Market by Product (Clinical Data Management, Clinical Trial Management System (CTMS), Electronic Clinical Outcome Assessment (eCOA) Solution, Randomization and Trial Supply Management (RTSM), Safety Solution, Others), Mode of Delivery, End-user, and Regional Analysis from 2025 - 2032

E-clinical Solution Market Share and Trends Analysis

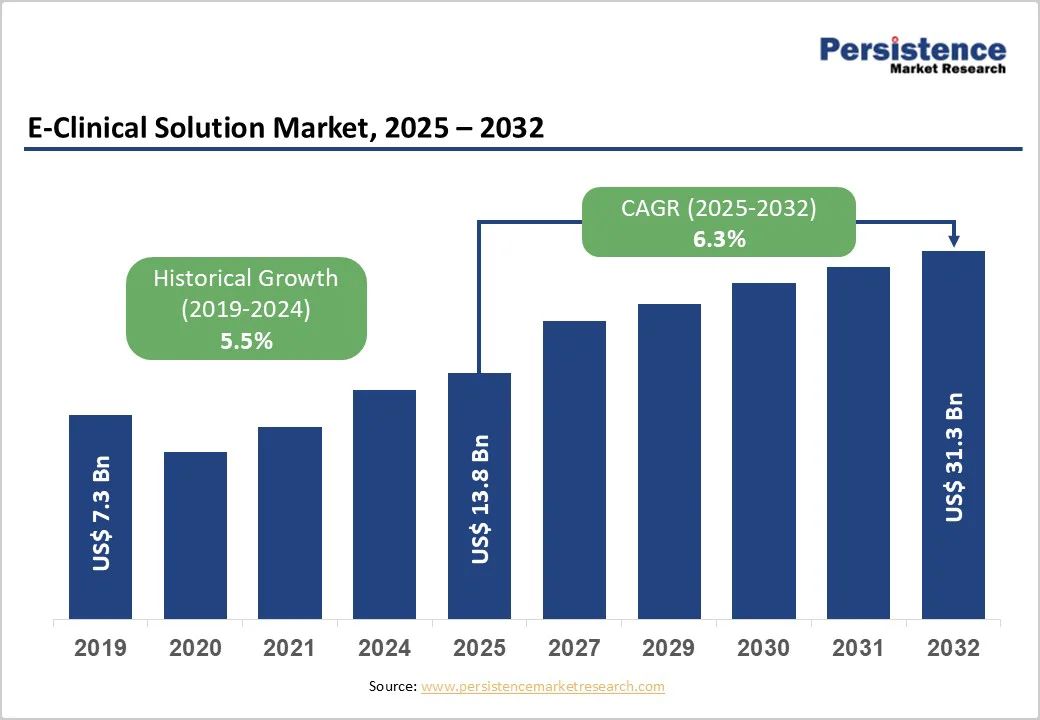

The global E-clinical solution market size is estimated to reach US$ 13.8 billion in 2025 and is projected to reach US$ 31.3 billion by 2032, growing at a CAGR of 12.4% between 2025 and 2032. E-clinical solutions refer to digitally enabled platforms that help researchers capture, manage, analyze, and track clinical trial data with greater accuracy and efficiency. Widely adopted across pharmaceutical companies, biotechnology firms, medical device developers, and clinical research organizations, these tools streamline study design and data workflows using advanced, technology-driven capabilities.

As clinical trials assess the safety and effectiveness of drugs and medical devices before commercialization, the growing global internet footprint and improved digital accessibility are accelerating adoption. Additionally, the promise of higher data reliability, real-time insights, and improved operational efficiency over traditional manual processes is driving wider integration of e-clinical solutions.

Key Industry Highlights:

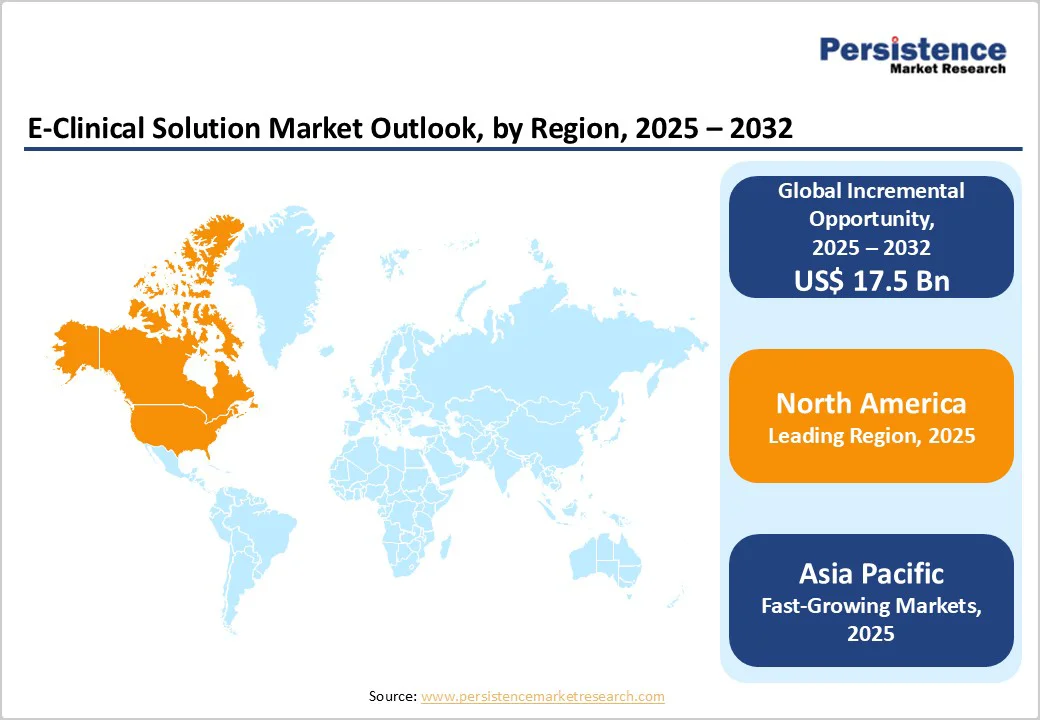

- Leading Region: North America dominates the global market with 47.8%, driven by advanced clinical trial infrastructure, strong regulatory compliance adoption, and rapid integration of AI-enabled e-clinical platforms.

- Fastest-Growing Region: Asia Pacific market is expected to grow rapidly with a CAGR of 15.2% in the forecast period, fueled by rising trial volumes, digital transformation investments, and expanding e-clinical technology adoption among regional CROs and sponsors.

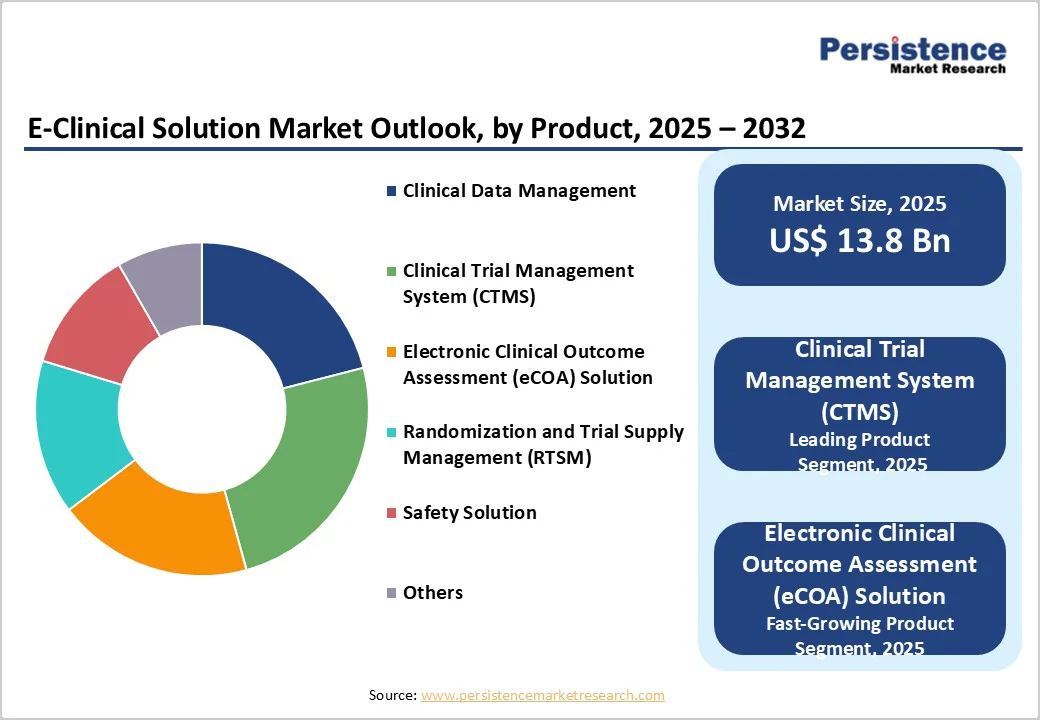

- Leading Product: Clinical trial management system (CTMS) lead with 24.7% share, supported by increased demand for centralized oversight, real-time operational visibility, and improved trial planning and monitoring efficiency.

- Leading Mode of Delivery: Web-hosted (on-demand) solutions (WHS) to remain dominant with 52.6%, driven by lower deployment costs, seamless scalability, easy multi-site access, and reduced IT maintenance needs.

- Leading End-user: Pharma & biopharma companies to lead with 32.7% share due to rising R&D spending, complex study designs, and strong reliance on digital tools for global trial management.

- Expansion of decentralized and hybrid clinical trials is accelerating demand for remote monitoring, eConsent, eCOA, and virtual engagement platforms to improve recruitment and retention.

- Global regulatory bodies pushing digital compliance, including EU CTR and FDA 21 CFR Part 11, is increasing adoption of compliant cloud-based e-clinical systems.

- Contract Research Organizations increasingly adopt advanced e-clinical systems to manage global studies, improve operational efficiency, and meet sponsor expectations for faster trial execution.

| Key Insights | Details |

|---|---|

|

Global E-Clinical solution Market Size (2025E) |

US$ 13.8 Billion |

|

Market Value Forecast (2032F) |

US$ 31.3 Billion |

|

Projected Growth (CAGR 2025 to 2032) |

12.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

11.4% |

Market Dynamics

Driver - Rigorous Global Regulatory Frameworks Strengthening Clinical Data Integrity and Increasing Trust in Digital Compliance Systems

The global e-clinical solutions market is increasingly driven by rising clinical trial activity, expanding R&D investments, and the growing burden of chronic diseases, which together heighten demand for faster, safer, and more efficient trial execution. As clinical trials registered worldwide climbed from 477,203 in 2024 to 558, 242 in November 2025, sponsors are turning to digital platforms that reduce cycle times and enhance data integrity. The regulatory environment further accelerates adoption, with stringent frameworks—FDA 21 CFR Part 11/50/54/56/312/812, EU CTR 536/2014, and ICH E6 R2/R3 & E8—requiring validated, traceable, audit-ready systems.

In line with this, several major developments underscore the sector’s shift toward AI-enabled, patient-centric, and cloud-powered solutions. In May 2024, Medidata expanded its AI-driven platform deployment to improve trial feasibility and site selection. In September 2024, Fortrea and Medidata advanced AI-enabled diversity modeling, while an investment by GI Partners boosted eClinical Solutions’ cloud-based data-management capabilities.

By October 2024, Medidata introduced lightweight EDC tools optimized for early- and late-phase trials. In February 2025, Medidata launched AI innovations such as virtual twins to enhance recruitment and forecasting. Further progress continued with July 2025 data-unification tools from Medidata cutting review cycles substantially and November 2025 eCOA accreditation strengthening patient engagement through Medidata and CTI Clinical Trial & Consulting. Collectively, these advancements illustrate how technology, regulation, and rising trial complexity converge to propel market growth.

Restraints - Complex, Multi-Agency Compliance Requirements Creating Operational Burden and Slowing Adoption of Advanced Data Management Platforms

The growth of the global e-clinical solutions market faces notable restraints, primarily driven by high implementation costs, complex regulatory compliance, and persistent technical fragmentation across regions.

For many mid-sized biotechnology companies and Contract Research Organizations (CROs)—particularly those operating in Latin America, Southeast Asia, and Eastern Europe—the investment required to deploy a full-suite eClinical platform remains prohibitive, often ranging between USD 300,000 and USD 500,000. These costs limit technology adoption and delay digital transformation, despite growing trial volumes.

Regulatory compliance further intensifies these challenges, as organizations must align with stringent international frameworks such as the General Data Protection Regulation (GDPR) in the European Union and the U.S. Food and Drug Administration (FDA) 21 Code of Federal Regulations (CFR) Part 11 governing electronic records and electronic signatures.

Many sponsors continue to rely on legacy systems that are incompatible with modern cloud-based architectures, creating data silos, reduced interoperability, and limited analytical insight generation. Together, these structural barriers underscore why eClinical modernization remains uneven across global trial ecosystems.

Opportunity - Growing Need for Harmonized Global Compliance Solutions Enabling Scalable, Multi-Region Digital Validation and Audit Readiness

The global e-clinical solutions market is poised for strong opportunity creation as rapid advances in artificial intelligence (AI), machine learning (ML), unified data platforms, and patient-centric technologies reshape how trials are designed, monitored, and executed.

Momentum began in May 2023, when eClinical Solutions enhanced its Elluminate IQ Review module by embedding deeper AI/ML capabilities into the Clinical Data Cloud, enabling faster anomaly detection, higher data quality, and significantly shorter review cycles.

In June 2023, Syneos Health and uMotif introduced an integrated patient-centric eClinical platform combining electronic consent (eConsent), electronic clinical outcome assessments (eCOA), electronic patient-reported outcomes (ePRO), and digital engagement tools—paving the way for higher retention and decentralized, hybrid trial models.

By December 2024, ClinChoice expanded its long-standing partnership with Medidata by adopting Medidata’s Clinical Data Studio, strengthening global workflows through AI-driven analytics and process automation.

Opportunities accelerated further in March 2025, when PhaseV launched causal machine-learning capabilities that simulate design parameters and reduce failure risk. In April 2025, insights from the Medidata NEXT conference highlighted how unified data science models enhance oversight and risk management.

Finally, in September 2025, PhaseV and Bioforum partnered to integrate Trial Optimizer, enabling adaptive and Bayesian simulations that cut timelines and costs. These advances create substantial opportunities for next-generation, AI-enabled eClinical ecosystems.

Category-wise Analysis

By Product Insights

Clinical trial management system (CTMS) are expected to account for a leading 24.7% share of the global e-clinical solution market by 2025, driven by the growing operational complexity of multicountry clinical trials and the need for real-time oversight. As protocols expand and study volumes rise, sponsors increasingly prioritize platforms that consolidate budgeting, site performance tracking, compliance documentation, and milestone monitoring. CTMS adoption is further accelerated by regulatory expectations for structured audit trails and harmonized reporting. Together, these factors position CTMS as the preferred product category for enabling efficient, transparent, and compliant trial execution.

By Mode of Delivery Insights

Web-hosted (on-demand) solutions are projected to command 52.6% of the global e-clinical solutions market in 2025, reflecting sponsors’ preference for scalable, low-maintenance systems. These cloud-based platforms eliminate the need for expensive on-premises infrastructure, enabling rapid deployment, seamless updates, and easier global collaboration across sites. Their compatibility with remote monitoring, decentralized trial models, and integrated data workflows makes them highly attractive as digital transformation accelerates. Additionally, improved data security standards and compliance frameworks support broader adoption, allowing organizations to manage rising trial volumes with greater flexibility and operational efficiency.

By End-user Insights

Pharma and biopharma companies are expected to account for 32.7% of the global e-clinical solutions market in 2025, reflecting their extensive trial pipelines and strong push toward digital transformation. These organizations rely heavily on integrated platforms to manage complex, multinational studies and ensure regulatory-compliant data workflows. As R&D portfolios expand into precision therapies, adaptive designs, and decentralized models, the need for unified systems—covering data capture, site management, monitoring, and analytics—becomes critical. This group’s higher technology investment capacity and continuous demand for operational efficiency reinforce its position as the largest end-user segment.

Regional Insights

North America E-Clinical Solution Market Trends

By 2025, North America is expected to capture nearly 47.8% of the global e-clinical solutions market, driven by steady digitalization and rapid integration of artificial intelligence (AI) across clinical research workflows. The momentum began in August 2022, when Clario launched its Translation Workbench to accelerate electronic Clinical Outcome Assessment (eCOA) study start-ups by 20–30%, improving translation efficiency and expanding patient accessibility.

In October 2023, Mednet strengthened decentralized and hybrid trial enablement through new electronic informed consent (eConsent) capabilities within its iMednet eClinical platform, enhancing regulatory compliance and participant comprehension. The pace continued, with Medidata, part of Dassault Systèmes, introducing Clinical Data Studio in June 2024, an AI-driven environment that unifies Medidata and non-Medidata sources to reconcile data up to 80% faster, significantly improving safety signal detection.

By November 2024, the National Institutes of Health (NIH) advanced automation further with TrialGPT, a large language model–based tool that speeds up patient-to-trial matching by 40% with near-human accuracy. Collectively, these innovations illustrate how AI-powered platforms, unified data ecosystems, and decentralized trial technologies are consolidating North America’s leadership in the e-clinical solutions landscape.

Europe E-Clinical Solution Market Trends

By 2025, Europe is projected to hold nearly 22.4% of the global e-clinical solutions market, driven by accelerating regulatory modernization and expanding adoption of advanced data infrastructures across the region. The momentum was strengthened in September 2023, when Ireland-based ICON plc introduced its next-generation Clinical Trial Tokenisation solution, enabling secure, privacy-protected record linkage (PPRL) and ethically consented integration of real-world data. This capability supports more accurate long-term safety and efficacy assessments and enhances evidence generation across diverse therapeutic areas.

Building on this innovation, the European Union advanced a broader transformation in 2024 through the Accelerating Clinical Trials in the EU (ACT-EU) initiative, which emphasizes smarter, technology-enabled trials supported by harmonized ethics review processes, improved regulatory standards, and greater cross-border collaboration.

ACT-EU’s roadmap, targeting authorization of 500 multinational clinical trials by 2030, is encouraging sponsors and contract research organizations to adopt unified digital platforms, decentralized tools, and data-driven decision systems to meet new operational expectations. Together, these developments highlight how Europe’s regulatory reforms and investment in next-generation data technologies are reinforcing demand for robust e-clinical solutions across the region.

Asia Pacific E-Clinical solution Market Trends

Asia Pacific e-clinical solutions market is expanding rapidly and is projected to grow at a compound annual growth rate (CAGR) of 15.2%, supported by rising digital maturity, data-driven trial models, and strong investment activity across the region.

The momentum began in October 2023, when Lokavant secured an USD 8 million investment from Mitsui & Co. to scale its artificial intelligence (AI)-powered clinical trial intelligence platform across Asia Pacific. This initiative included establishing a regional hub in Tokyo to enhance predictive analytics for sponsors and contract research organizations (CROs), strengthening trial performance and risk management.

Advancing this trajectory, Perceptive eClinical launched ClinPhone 5 in November 2024, a cloud-native, multi-tenant Randomization and Trial Supply Management (RTSM) system co-developed with CRScube, enabling faster study start-up, greater scalability, and improved supply forecasting—capabilities increasingly demanded in high-growth markets such as Japan, China, South Korea, and Australia.

By November 2025, CRScube further accelerated regional and global expansion through its acquisition of Mednet, integrating long-established electronic data capture (EDC) and workflow technologies and reinforcing its position as a leading Asia-based e-clinical solutions provider with over 6,000 supported trials worldwide. Collectively, these investments and technology advancements strongly propel Asia Pacific’s adoption of advanced e-clinical platforms.

Market Competitive Landscape

The competitive landscape of the e-clinical solutions market is characterized by rapid technological advancement, strong focus on unified trial platforms, and growing investment in cloud-native, API-driven architectures. Vendors compete on integration strength, data security, real-time analytics, and decentralized trial enablement, while expanding service capabilities such as implementation support, workflow customization, and AI-enabled study automation to differentiate in a highly innovation-driven market.

Key Industry Developments:

- In November 2024, RealTime eClinical Solutions expanded its Professional Services to help research sites, academic medical centres (AMCs), sponsors, and CROs fully leverage its eClinical suite. The “white-glove” offering includes customized visioning, implementation, data migration, template design, and change-management services.

- In June 2023, ICON plc launched an updated version of its Digital Platform, unifying patient, site, and sponsor services with harmonized data and customizable workflows. Cloud-first, API-first architecture supports eConsent, eCOA, televisits, and mobile capture, speeding study start-up and enhancing decentralized trial participation.

Companies Covered in E-Clinical Solution Market

- Oracle

- Signant Health

- eClinical Solutions LLC

- RealTime Software Solutions, LLC

- CRF Health

- Viedoc Technologies

- Florence Healthcare

- Anju

- Medidata

- eClinicalWorks

- IQVIA

- Summit Partners L.P.

- Clario

- Clinfinite Solutions

- Suvoda LLC

Frequently Asked Questions

The global e-clinical solution market is projected to be valued at US$ 13.8 Billion in 2025.

Growing decentralized trials, rising data complexity, and adoption of cloud-based platforms are driving rapid expansion of the global e-clinical solutions market.

The global market is poised to witness a CAGR of 12.4% between 2025 and 2032.

AI-driven trial automation, real-time analytics, and adoption of unified digital platforms in emerging markets offer strong opportunities for e-clinical solution providers.

Major players in the global are Oracle, Signant Health, eClinical Solutions LLC, RealTime Software Solutions, LLC, Medidata, eClinicalWorks, IQVIA, Clario, and others.