- Pharmaceuticals

- Controlled Release Cannabis Pills Market

Controlled Release Cannabis Pills Market Size, Share, and Growth Forecast, 2026 - 2033

Controlled Release Cannabis Pills Market by Product Type (High CBD Capsules, THC Balanced Capsules), Dosage Form (Tablets, Capsules, Softgels), End-User (Hospitals, Home Care Settings, Elderly Care Centers), and Regional Analysis for 2026 - 2033

Controlled Release Cannabis Pills Market Share and Trends Analysis

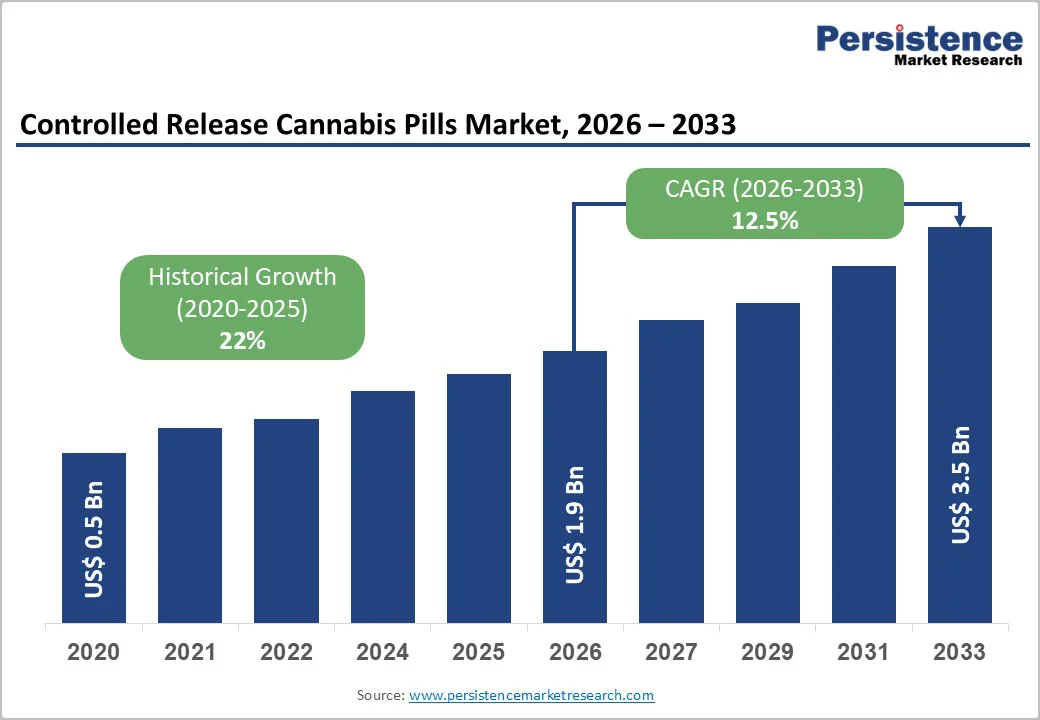

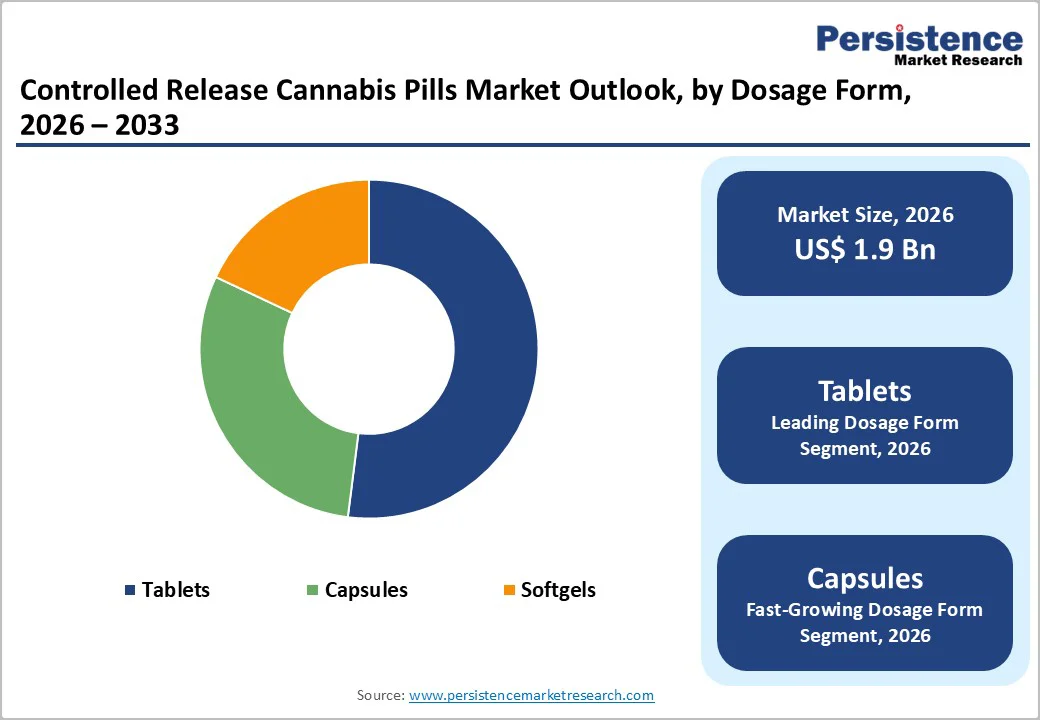

The global controlled release cannabis pills market size is likely to be valued at US$ 1.9 billion in 2026, and is projected to reach US$ 3.5 billion by 2033, growing at a CAGR of 12.5% during the forecast period 2026−2033. Increasing legalization of medical cannabis across multiple jurisdictions, growing acceptance of cannabis-based pharmaceuticals for chronic disease management, and technological advancements in controlled-release drug delivery systems are factors favoring market expansion.

The pharmaceutical industry's pivot toward cannabis-derived therapeutics, coupled with favorable regulatory developments in North America and Europe, has created a conducive environment for market growth. The rising prevalence of chronic pain conditions, neurological disorders, and cancer-related symptoms has further amplified the demand for sustained-release cannabinoid formulations that offer consistent therapeutic effects with reduced dosing frequency.

Key Industry Highlights

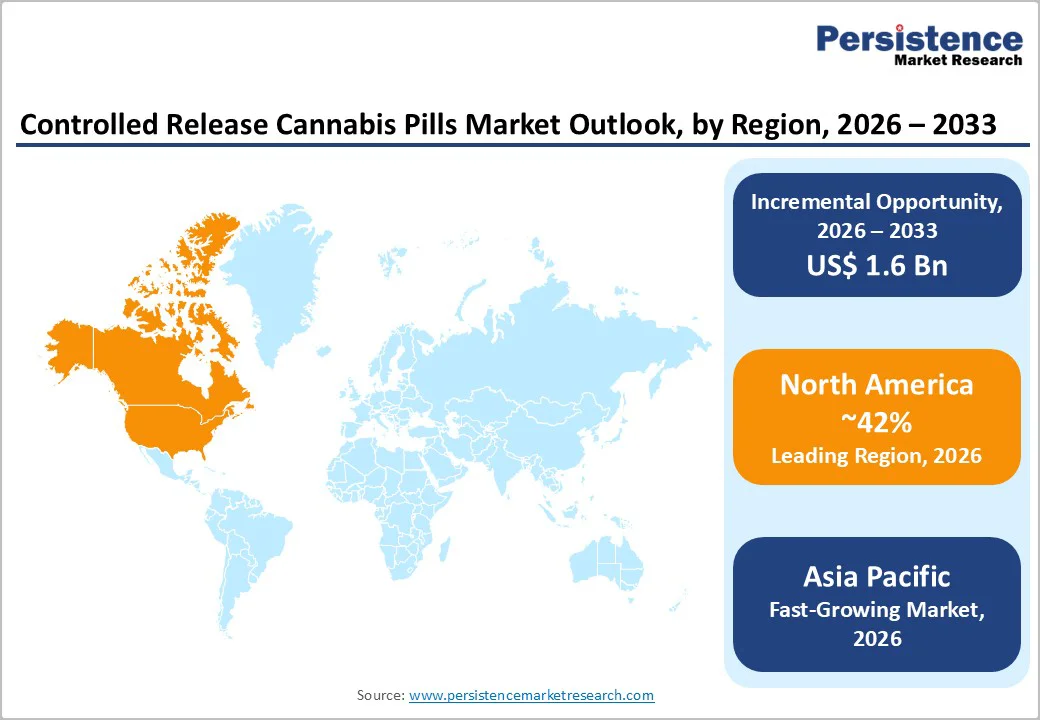

- Dominant Region: North America is expected to command a market share of about 42% in 2026, supported by advanced regulatory frameworks and well-established medical cannabis ecosystems.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market through 2033 due to large and aging patient populations and steadily improving healthcare infrastructure.

- Leading & Fastest-growing Product Types: High-CBD capsules are expected to hold an estimated 2026 share of 52%, while THC balanced capsules are likely to post the highest CAGR during the 2026-2033 forecast period.

- Dominant & Fastest-growing Dosage Forms: Tablets are slated to dominate with around 52% in 2026, with capsules expected to grow the fastest from 2026 to 2033.

- Key Drivers: The escalating global burden of chronic diseases serves as a critical catalyst for the consumption of controlled-release cannabis pills.

- Market Opportunities: The rapid expansion of clinical research into new therapeutic applications is likely to create diverse investment and innovation opportunities for market player

| Key Insights | Details |

|---|---|

|

Controlled Release Cannabis Pills Market Size (2026E) |

US$ 1.9 Bn |

|

Market Value Forecast (2033F) |

US$ 3.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

22% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Chronic Disease Prevalence and Opioid Crisis

The escalating global burden of non-communicable diseases (NCDs) has created unprecedented demand for pain management solutions. According to the World Health Organization (WHO), NCDs account for approximately 74% of worldwide deaths, with cardiovascular diseases leading at 19 million deaths annually. This expanding population of chronically ill patients has historically fueled aggressive opioid prescribing, as healthcare providers sought to address persistent pain. Research from UC Davis Health indicates that between 1999 and 2014, prescription opioid dispensing nearly doubled from 105 million to 207 million annual prescriptions in the United States, yet fatal overdoses quintupled during the same period, rising from 4,000 to 19,000 deaths per year. A 2018 meta-analysis published in JAMA demonstrated that despite widespread opioid deployment in chronic pain management, these medications provide only modest pain reduction of 0.69 centimeters on a standard 10-centimeter pain scale and minimal functional improvements of 2.04 points on a 100-point functional capacity measure.

This disconnect between therapeutic efficacy and risk has prompted sustained investigation into alternative pharmacological interventions, particularly controlled release cannabis pills. These formulations deliver cannabinoid compounds through oral pharmaceutical delivery systems designed for sustained therapeutic effects. A 2024 analysis in the medical cannabis literature found that among patients transitioning to medical cannabis, 97% reported decreased opioid reliance, while 81% expressed greater satisfaction with cannabis monotherapy compared to cannabis-opioid regimens. The controlled release cannabis pills market has emerged as a direct response to this therapeutic imperative, offering patients with chronic musculoskeletal pain, neuropathic disorders, and other pain-related conditions a pharmaceutical alternative that demonstrates superior safety tolerability profiles compared to opioids. Pharmaceutical developers recognize that cannabinoid receptors provide a distinct pharmacological target that circumvents opioid-specific risks including respiratory depression, addiction liability, and dose-dependent overdose mortality. As healthcare systems increasingly acknowledge the limitations of opioid-centric pain management strategies, the integration of controlled release cannabis pills into treatment protocols represents a paradigm shift.

Limited Reimbursement Infrastructure and Market Access Barriers

Limited reimbursement infrastructure and untiring market access barriers continue to constrain the adoption of controlled-release cannabis pills. The lack of comprehensive insurance coverage for cannabis-based medicines means that many health plans, including public programs, do not reimburse these therapies, leaving patients to bear the full cost. This financial burden restricts uptake, particularly among lower-income groups that could benefit from alternative pain management options. The high price of pharmaceutical-grade controlled release formulations, driven by stringent quality standards and complex manufacturing processes, further limits accessibility and slows overall market growth.

Non-financial barriers also significantly influence market dynamics. The stigma around medical cannabis use continues to affect both doctors' prescribing habits and patients' willingness to start or continue treatment, especially in more conservative areas. Fears of regulatory scrutiny and damaging their professional reputation may lead some clinicians to exclude these products from routine care. At the same time, restrictions on financial services for cannabis-related businesses make daily operations more difficult, limit access to capital, and slow down the development of strong distribution and support systems. These economic, social, and operational challenges are bound to slow down market growth, even when clinical benefits, increasing evidence, and patient demand could otherwise promote wider adoption.

Expansion of Therapeutic Applications through Clinical Research

The controlled-release cannabis pills market growth can gain new momentum owing to the rapid expansion of clinical research into new therapeutic applications. Current use remains focused on pain management, epilepsy, and cancer-related symptom control, but emerging studies increasingly examine the role of cannabinoids in treating psychiatric conditions such as anxiety, depression, and post-traumatic stress disorder. Research pipelines are also broadening to include neurodegenerative diseases, inflammatory bowel disease, and autoimmune disorders, all of which could significantly expand the potential treatment population for controlled-release cannabis formulations.

The development of cannabinoid–opioid combination therapies is gaining attention as a strategy to enhance pain relief while potentially reducing reliance on high-dose opioid regimens. These combination approaches may provide more balanced and sustainable pain control for patients with complex chronic conditions that are poorly managed by existing options. Pharmaceutical companies that invest in robust clinical trial programs and proactively pursue regulatory approvals for new indications are well-positioned to capture high-value, underserved therapeutic segments. Such efforts can generate defensible intellectual property, justify premium pricing, and reinforce competitive differentiation as the clinical evidence base for cannabinoid-based pharmacotherapies continues to mature.

Category-wise Analysis

Product Type Insights

High CBD capsules are expected to maintain a dominant position in the market, with an estimated 2026 share of 52%. This segment’s leadership is driven by the non-psychoactive profile of cannabidiol (CBD), broad therapeutic applications, and relatively favorable regulatory treatment in many markets. The approval of a CBD-based oral solution for severe epilepsy helped legitimize cannabinoids as a formal therapeutic class and strengthened physician confidence in prescribing CBD products. High-CBD controlled-release capsules are used to manage conditions such as chronic pain, inflammation, anxiety disorders, and seizure-related disorders. Because they do not produce intoxicating effects, they are particularly suitable for patients who need to maintain cognitive and functional capacity throughout the course of treatment.

Tetrahydrocannabinol (THC) balanced capsules are likely to be the fastest-growing segment during the 2026-2033 forecast period. These formulations leverage the support effect, in which multiple cannabinoids act synergistically to enhance therapeutic outcomes while CBD helps modulate the psychoactive effects of THC. Balanced formulations have shown strong potential in managing neuropathic pain, muscle spasticity in multiple sclerosis, and a range of cancer-related symptoms. The segment also gains momentum from a growing body of clinical evidence supporting combination cannabinoid therapy and rising physician comfort with prescribing products that contain carefully controlled levels of THC. In addition, market growth is supported by patient preference for comprehensive symptom relief and by advances in controlled-release technologies that help maintain optimal cannabinoid ratios over the entire dosing interval.

Dosage Form Insights

Tablets are slated to dominate in 2026 with an estimated 52% of the controlled release cannabis pills market revenue share. This segment’s leadership is supported by well-established manufacturing infrastructure, strong patient familiarity with oral solid dosage forms, and the broad availability of controlled-release technologies originally developed for conventional pharmaceuticals. Extended-release tablets use advanced delivery mechanisms such as matrix systems, osmotic technologies, and multilayer coatings to provide prolonged drug release, which supports better adherence than regimens that require multiple daily doses. The segment also benefits from scalable production, attractive cost structures, and the ability to secure strong intellectual property protection around proprietary delivery platforms, reinforcing its competitive position within the controlled-release cannabis pills market.

Capsules are expected to be the fastest-growing segment between 2026 and 2033. This acceleration is driven by several factors, including capsules ability to mask the taste of cannabis extracts, their flexibility in accommodating multi-component cannabinoid blends, and their compatibility with a wide range of release-modification technologies such as pellet-based systems and lipid encapsulation. Hard gelatin and hydroxypropyl methylcellulose (HPMC) capsules filled with sustained-release pellets or beads allow precise control over cannabinoid release kinetics while maintaining formulation stability. The segment growth is further supported by patient preference for capsules over tablets, particularly among individuals with swallowing difficulties, as well as manufacturing advantages such as simplified production processes and lower equipment requirements compared with tablet compression systems.

End-User Insights

Hospitals are anticipated to lead with an approximate 52% of market revenue share in 2026. This dominance reflects the central role of hospitals in managing complex medical conditions that require cannabis-based therapies, including cancer symptom control, severe epilepsy, and palliative care. Hospital settings provide a controlled environment for initiating treatment, monitoring patient responses, and adjusting dosing regimens under direct physician supervision. The hospital segment is expected to grow more rapidly as the use of controlled-release cannabis pills expands for indications such as muscle spasm, chronic pain, nausea, and dizziness. This segment also benefits from established procurement channels with pharmaceutical manufacturers, formulary inclusion of approved cannabis medicines, and integration with electronic health record systems, which streamlines prescribing and medication management.

Home care settings are anticipated to be the fastest-growing segment during the 2026-2033 forecast period, as they align directly with the shift from hospital-based to community-based management of chronic diseases, where patients increasingly prefer to manage long-term symptoms in their own homes rather than in institutional settings. Controlled-release cannabis pills fit this model particularly well because they provide convenient, once- or twice-daily oral dosing with sustained symptom relief, reducing the need for frequent clinical visits and complex titration in hospital environments.

Regional Insights

North America Controlled Release Cannabis Pills Market Trends

North America is set to command a significant portion of the controlled release cannabis pills market share at approximately 42% in 2026. The region’s leadership reflects advanced regulatory frameworks, well-established medical cannabis ecosystems, and relatively high healthcare spending. The United States underpins this dominance through a combination of progressive state-level medical cannabis programs, a strong pharmaceutical R&D base, and the presence of multiple leading cannabis-focused drug developers. A large share of the U.S. population now resides in jurisdictions where some form of cannabis use is legal, supporting broad patient access and meaningful commercial scale. Canada’s federally regulated medical cannabis regime has created a mature, pharmaceutical-grade production and quality-control infrastructure that is widely viewed as a benchmark for other markets.

Market growth in North America is further supported by a widening clinical evidence base for cannabinoid therapies, greater physician education on cannabis pharmacology, and ongoing policy debates on federal rescheduling that could reduce barriers to research and commercialization. The region also benefits from sophisticated healthcare infrastructure and strong intellectual property protections, which together encourage sustained pharmaceutical investment. However, unsettled challenges such as banking restrictions, inconsistencies between federal and state law, and limited insurance reimbursement continue to temper overall market growth. Investment activity increasingly features major pharmaceutical companies acquiring cannabinoid-focused biotechnology firms and forming strategic partnerships, creating a competitive landscape that blends specialist cannabis innovators with large, diversified drug manufacturers.

Europe Controlled Release Cannabis Pills Market Trends

Europe is set to emerge as the second-largest regional market for controlled release cannabis pills, characterized by regulatory harmonization efforts, strong pharmaceutical manufacturing capabilities, and progressive medical cannabis policies in key markets. Germany remains the primary driver of European adoption, underpinned by one of the most comprehensive and mature medical cannabis frameworks globally. France is signaling broader acceptance as health authorities extend national trials and appoint formal medical cannabis suppliers, reinforcing the integration of cannabis-based therapies into its healthcare system. The United Kingdom, despite relatively restrictive prescribing practices, continues to exert significant influence through its strong pharmaceutical research base and the presence of leading cannabis-focused drug developers.

Regulatory environment impacts are profound, with the European Medicines Agency (EMA) providing centralized approval pathways for cannabinoid pharmaceuticals, enabling simultaneous market access across member states. However, national implementation varies significantly, with some countries imposing restrictive prescribing conditions or limited reimbursement. The region's pharmaceutical industry benefits from extensive expertise in controlled release technologies, rigorous quality manufacturing standards, and established distribution networks. Competitive landscape characteristics include strong positioning of European pharmaceutical companies in generic drug manufacturing, creating opportunities for controlled-release cannabis pill production once intellectual property protections expire.

Asia Pacific Controlled Release Cannabis Pills Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing controlled release cannabis pills market through 2033, on account of regulatory liberalization in traditionally conservative countries, large and aging patient populations, and steadily improving healthcare infrastructure. The region encompasses highly diverse market contexts China’s established strength in pharmaceutical manufacturing now extends into cannabinoid ingredient production for export, even though domestic medical use remains tightly restricted. Japan maintains very conservative cannabis regulations but permits limited use of certain cannabis-derived pharmaceuticals under narrowly defined medical criteria, while India’s broader push into advanced drug delivery technologies signals strong potential as its medical cannabis framework gradually evolves.

The regional market benefits from significant manufacturing advantages, including cost-efficient pharmaceutical production, extensive experience in generic medicines, and growing investment in biotechnology and formulation science. These capabilities intersect with a large population of patients living with chronic conditions such as diabetes, cardiovascular disease, cancer, and persistent pain, creating strong demand for long-acting symptom control solutions. Investment activity increasingly focuses on technology-transfer collaborations between Western innovators and Asian manufacturers, joint ventures that combine competitive regional production costs with international-quality standards, and strategic positioning ahead of broader policy legalization.

Competitive Landscape

The global controlled release cannabis pills market operates as a moderately fragmented structure, with a small group of established players accounting for 55–60% of total market share. Leading companies in this space include Jazz Pharmaceuticals, Inc., Aurora Cannabis Inc., Tilray Brands, Inc., and Cronos Group Inc., each leveraging scale, regulatory experience, and commercial infrastructure to maintain strong positions. These firms focus on pharmaceutical-grade manufacturing, robust clinical data packages, and securing reimbursement from public and private payers to differentiate their products. The market features high barriers to entry, driven by stringent regulatory approval requirements for controlled substances, significant research and development (R&D) investment needs, and the specialized expertise required for controlled release formulation and Good Manufacturing Practice (GMP) compliance. Despite this, the landscape remains dynamic, with a growing number of small and medium enterprises entering the space through niche innovations in cannabinoid ratios, novel excipients, and advanced delivery technologies such as gastroretentive or transmucosal systems.

Companies that generate high-quality evidence on efficacy, safety, and real-world outcomes in chronic pain, spasticity, and other approved indications are better positioned to gain formulary inclusion and physician adoption. Firms with prior experience in developing controlled release oral dosage forms for other therapeutic areas also benefit from established relationships with regulatory bodies, contract manufacturing organizations, and healthcare providers. As reimbursement policies evolve and payers demand greater value demonstration, players that combine strong clinical data with clear health economic models and patient support services will be best placed to expand their footprint.

Key Industry Developments

- In December 2025, the U.S. Federal Government issued an executive order reclassifying marijuana from a Schedule I (alongside heroin and LSD) to a Schedule III controlled substance, marking the most significant federal cannabis policy shift in over 50 years. The reclassification would enable cannabis companies to operate under different tax rules, facilitate research, and ease interstate commerce.

- In December 2025, 113 Botanicals Ltd launched a £ 2 million crowdfunding raise to commercialize SpheriCann, its patent-protected controlled-release capsule developed in partnership with the University of Sussex that delivers sustained cannabinoid absorption and precise dosing to U.K. patients. The company aims to revolutionize medical cannabis prescription formats by eliminating multiple daily doses through its advanced delivery technology.

- In November 2025, Canopy Growth rolled out new Spectrum Therapeutics medical cannabis softgel capsules in Australia, introducing Yellow, Red, and Blue formulations. The launch represents Canopy's response to growing patient demand for convenient, standardized treatment formats and reinforces the company's commitment to expanding its market share in Australia's regulated medical cannabis sector.

Companies Covered in Controlled Release Cannabis Pills Market

- Jazz Pharmaceuticals, Inc.

- Canopy Growth Corporation

- GW Pharmaceuticals Limited

- Organigram Holding, Inc.

- Tilray Brands, Inc.

- Aurora Cannabis Inc.

- Cronos Group Inc.

- Corbus Pharmaceuticals Holdings, Inc.

- Zynerba Pharmaceuticals

- InMed Pharmaceuticals

- Clever Leaves Holdings Inc.

- Tetra Bio-Pharma Inc.

- Insys Therapeutics, Inc.

- AbbVie, Inc.

- Emerald Health Pharmaceuticals Inc.

Frequently Asked Questions

The global controlled release cannabis pills market is projected to reach US$ 1.9 billion in 2026.

Rise in global chronic disease burden, soaring demand for safer long-term pain management, and advances in precision oral delivery technologies are driving the market.

The market is poised to witness a CAGR of 12.5% from 2026 to 2033.

Key market opportunities include expanding indications into psychiatric and neurodegenerative disorders, rapid growth in emerging markets, and increased adoption in homecare and elderly care settings.

Jazz Pharmaceuticals, Inc., Aurora Cannabis Inc., Tilray Brands, Inc., and Cronos Group Inc are some of the key players in the market.