- Pharmaceuticals

- Medicinal Cannabis Compounding Market

Medicinal Cannabis Compounding Market Size, Share, and Growth Forecast 2026 – 2033

Medicinal Cannabis Compounding Market by Product Type (Extract, Flower, Leaves, Others), Compound Type (Tetrahydrocannabinol, Others), Formulation (Full Spectrum, Others), Application (Chronic Pain, Others), and Regional Analysis 2026 – 2033

Medicinal Cannabis Compounding Market Size and Trends Analysis

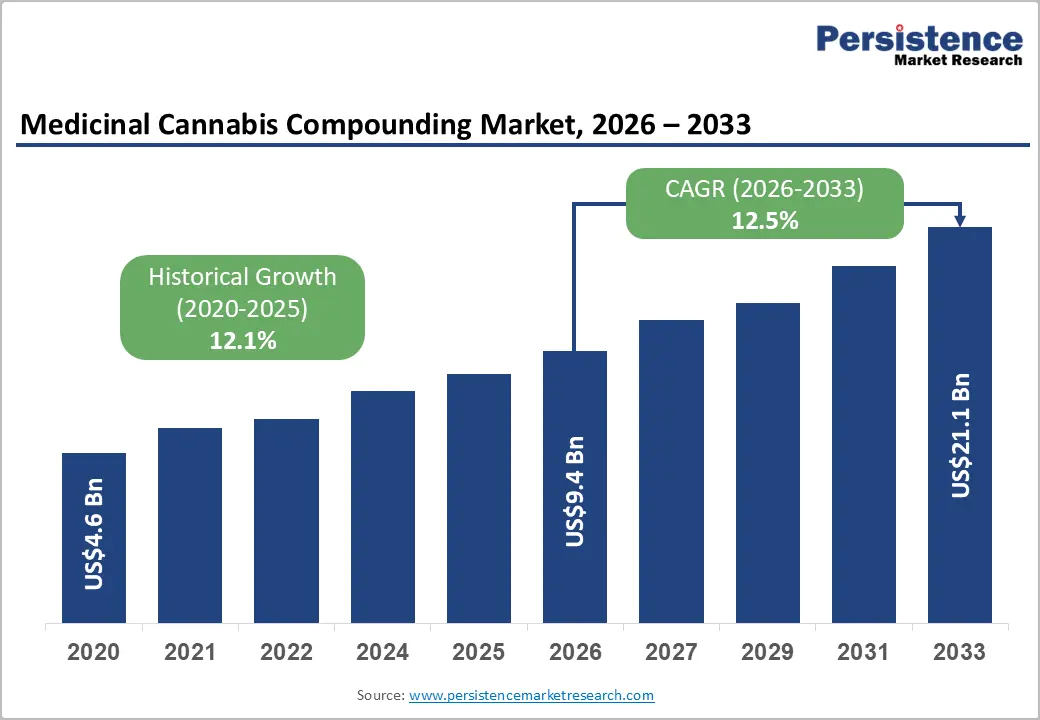

The global medicinal cannabis compounding market size is projected to be valued at US$ 9.4 Bn in 2026 and is projected to reach US$ 21.1 Bn by 2033, growing at a CAGR of 12.5% during the forecast period between 2026 and 2033, driven by the increasing global prevalence of chronic pain and neurological disorders, necessitating personalized therapeutic regimens that standard pharmaceuticals cannot address. Technological advancements in extraction and bioavailability are further validating compounded cannabis as a legitimate, reproducible medical intervention, fostering trust among healthcare practitioners and patients alike.

Key Industry Highlights

- Leading Market Region: North America is expected to dominate the global medical cannabis market, accounting for over half of the total revenue. Market leadership is supported by established medical programs, high patient penetration for chronic pain management, and expanding institutional participation following favorable regulatory reclassification.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid regulatory liberalization and expanding medical access frameworks. Australia plays a central role through scaled cultivation, clinical adoption, and growing export-oriented pharmaceutical cannabis production.

- Fastest-growing Type: Flower-based medical cannabis products are likely to represent the fastest-growing type. Growth is supported by increasing physician acceptance, expanding patient preference for inhalation-based therapies, and improving quality standardization across regulated markets.

- Market Driver: The rising prevalence of chronic pain and neurological disorders is the primary market driver. Demand is reinforced by growing clinical acceptance of cannabinoid-based therapies, expanding reimbursement discussions, and increasing emphasis on precision dosing through compounded formulations.

- Market Restraint: Regulatory fragmentation across regions continues to restrain market expansion. Inconsistent prescribing rules, cross-border trade limitations, and controlled substance classifications create operational complexity and delay large-scale institutional adoption.

- Key Opportunity: Personalized medicine presents a significant opportunity. Patient-specific compounding, nanoemulsion technologies improving bioavailability, and genomics-aligned dosing models are reshaping therapeutic differentiation and long-term clinical value.

- Key Industry Developments: In April 2025, Jack Herer Brand entered a strategic partnership with SOMAÍ to expand into the global pharmaceutical cannabis market. The collaboration introduces iconic Jack Herer strains as EU GMP-certified medical products, reinforcing the industry’s shift toward pharmaceutical-grade APIs and regulated therapeutic use. This move reflects growing consolidation as brands align with compliant manufacturing and distribution partners. It also aligns with regulatory easing in key European markets, including Germany, enabling broader institutional and prescription-led adoption. The development underscores the transition from consumer-led cannabis markets to medically regulated growth pathways.

| Key Insights | Details |

|---|---|

|

Medicinal Cannabis Compounding Market Size (2026E) |

US$9.4 Bn |

|

Market Value Forecast (2033F) |

US$21.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

12.1% |

Market Dynamics – Drivers, Restraints, and Opportunities

Precision Medicine and Technological Convergence

Precision medicine is emerging as a primary structural driver for the medicinal cannabis compounding market, reshaping how cannabinoid therapies are developed and prescribed. Advances in pharmacogenomics enable compounders to move beyond standardized dosing toward genetically informed formulation strategies. By understanding individual metabolic pathways involved in cannabinoid processing, pharmacists can tailor cannabinoid ratios to patient-specific tolerance and therapeutic response profiles. The integration of AI-driven decision support further reinforces this shift by translating complex biological inputs into actionable compounding guidance.

Technological convergence across extraction, formulation, and digital workflow systems further accelerates this market driver. Digital formulation platforms streamline compounding processes while embedding genetic insights, prescription data, and quality documentation into a unified workflow. These efficiencies lower operational risk, expand scalable capacity, and make advanced cannabinoid personalization economically viable across pharmacy sizes. Demographic pressures from aging populations with complex medication needs amplify demand for such precision-oriented solutions. Collectively, these forces position technological and clinical precision as a central engine of sustained growth in medicinal cannabis compounding.

Lack of Standardized Clinical Dosing Guidelines

A core structural restraint in the medicinal cannabis compounding market is the absence of universally accepted, evidence-based dosing frameworks. Unlike regulated pharmaceutical products with clearly defined label instructions, compounded cannabis formulations often depend on incremental titration guided by practitioner experience rather than standardized protocols. This inconsistency creates uncertainty in treatment outcomes and reinforces physician reluctance to prescribe compounded cannabinoids at scale. The lack of harmonized clinical reference points also complicates patient monitoring, as dosing adjustments vary widely across providers, care settings, and indications, weakening clinical comparability and limiting broader institutional adoption.

The challenge is further intensified by compositional variability within full-spectrum extracts, where minor cannabinoids and terpene profiles differ across batches and suppliers. Without large-scale, controlled clinical studies establishing clear dose-response relationships for specific compounded formulations, standardization remains elusive. This evidence gap restricts integration into mainstream clinical pathways and reinforces perceptions of therapeutic unpredictability. As a result, medicinal cannabis compounding continues to be positioned as a complementary or niche option rather than a primary, guideline-supported standard of care within formal healthcare systems.

Neurological and Oncology Application Expansion

Neurological disorders are emerging as a powerful growth driver for medicinal cannabis compounding due to their clinical complexity and need for individualized therapy. Conditions such as epilepsy and multiple sclerosis often require highly specific cannabinoid profiles and delivery systems that standardized commercial products cannot provide. Compounding pharmacies enable precision formulations that balance dominant and trace cannabinoids to support seizure control, spasticity management, and neuropathic pain relief. Regulatory pathways for rare neurological conditions further support clinical adoption, reinforcing compounding as a credible and necessary solution within specialized neurology care settings.

Oncology, particularly palliative care, represents a parallel expansion pathway as healthcare systems seek alternatives to opioid centric symptom management. Compounded cannabinoid formulations address chemotherapy-induced nausea, appetite loss, and pain through customizable delivery formats that improve onset control, tolerability, and adherence. Physicians value the flexibility to adjust potency and formulation based on evolving patient needs, including swallowing difficulties and breakthrough symptoms. Together, neurological and oncology applications strengthen the market’s clinical relevance and drive sustained demand for advanced, patient-centric compounding solutions.

Category-wise Analysis

Product Type Insights

Extracts are expected lead the product type segmentation with a 45% market share in 2026 and simultaneously represent the fastest-growing subsegment, reflecting structural preference for standardized, high precision formulations across regulated therapeutic markets. Dominance is driven by superior bioavailability relative to raw plant forms, consistent API concentration, and formulation flexibility supporting oils, tinctures, capsules, and compounded dosage formats. Advanced extraction technologies, including supercritical CO? processes, further strengthen quality consistency and purity benchmarks, positioning extracts as the preferred input for chronic and long-term treatment protocols where a predictable therapeutic response is critical.

Flowers account for 35% of market share, maintaining relevance through demand for whole-plant therapies that preserve terpene profiles and synergistic phytochemical effects, particularly in neurological and pain-management use cases. Leaves represent a marginal 5% share, constrained by lower potency and limited clinical standardization, resulting in secondary market positioning. Others, comprising 15%, benefit from niche expansion in topicals and alternative delivery formats supporting localized treatment without systemic exposure.

Compound Type Insights

Cannabidiol is expected to lead the compound segmentation with a 65% market share, reflecting its central role in regulated medical cannabis formulations and compounding practices. This dominance is structurally supported by CBD’s non-intoxicating pharmacological profile, broad regulatory acceptance, and suitability across high-volume therapeutic indications, including epilepsy, anxiety management, and inflammatory disorders. Prescribers and pharmacies prioritize CBD due to predictable dosing, favorable safety margins, and reimbursement compatibility, which collectively reduce clinical and regulatory friction. Its function as a primary entry compound for first-time patients further stabilizes demand, while integration into standardized oils, tinctures, and capsules reinforces supply chain reliance and long-term revenue visibility.

Tetrahydrocannabinol is likely to be the fastest-growing compound type, driven by expanding clinical utilization in oncology, neuropathic pain, and palliative care, where symptom severity necessitates stronger therapeutic intervention. Evolving clinical protocols increasingly favor controlled THC inclusion, particularly in balanced formulations that enhance efficacy without disproportionate psychoactive burden. Other compounds, including minor cannabinoids such as CBG and CBN, account for 4% of the market and remain niche, with adoption limited to experimental, sleep, and specialty neurology applications, indicating supplementary rather than core market participation.

Formulation Type Insights

Full-spectrum formulations are expected to lead the market with a 50% share in 2026, reflecting sustained clinical and commercial preference for therapeutically comprehensive profiles that preserve cannabinoids, terpenes, and flavonoids in their natural ratios. This dominance is structurally reinforced by the widespread acceptance of the entourage effect, which supports multi-pathway efficacy across complex indications such as chronic pain, PTSD, and neurological disorders. Full-spectrum products are favored in compounding environments where outcome reliability, patient response breadth, and formulation familiarity drive prescribing behavior. Their leadership also translates into pricing resilience and formulary stability, as practitioners prioritize holistic efficacy over single-compound optimization, securing long-term demand continuity.

Isolate formulations are likely to represent the fastest-growing segment, driven by demand for pharmaceutical-grade purity, zero-THC compliance, and precise dose reconstruction in tightly regulated medical settings. This growth reflects rising sensitivity to workplace drug testing, adverse compound tolerance, and regulatory scrutiny. Broad-spectrum formulations account for 30% of the market, occupying a strategic middle ground by retaining minor cannabinoids while excluding THC, supporting steady adoption among risk-averse patients. Isolates hold 20%, transitioning from niche use toward targeted therapeutic standardization.

Application Type Insights

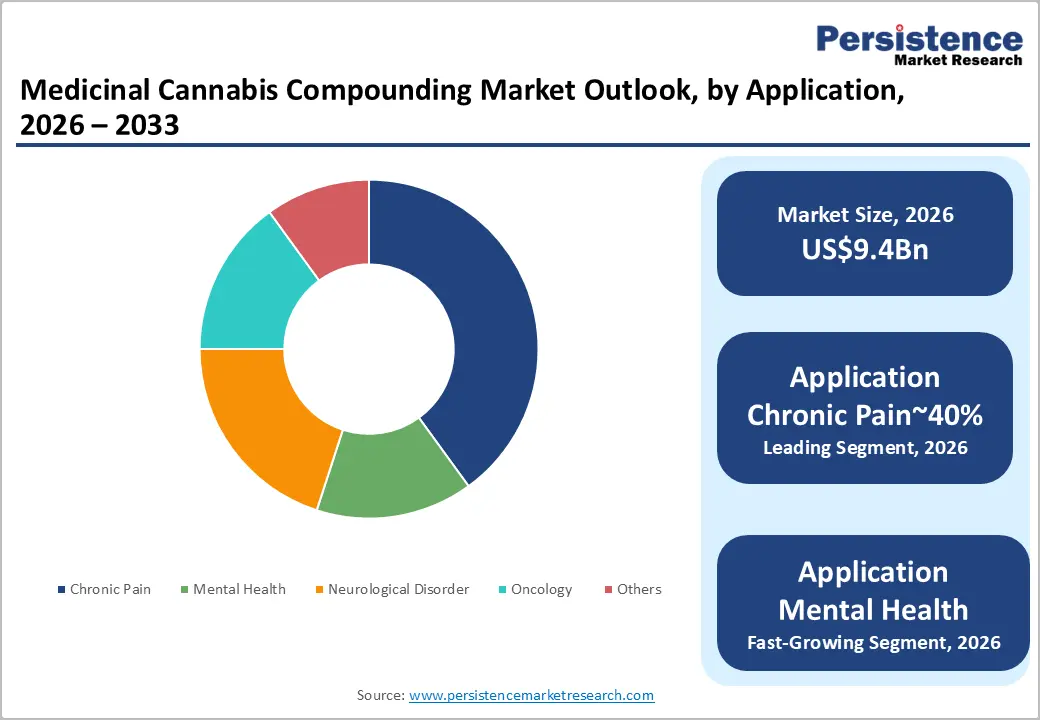

Chronic pain is expected to dominate the application landscape, capturing a 40% share in 2026, underscoring its established role as the primary therapeutic use for compounded cannabinoid formulations. This demand is fueled by the persistent global prevalence of pain, strategies to substitute opioids, and the need for adjustable cannabinoid ratios to manage neuropathic and musculoskeletal conditions. Compounded products allow for personalized dosing, tolerance management, and alignment with long-term therapy, making chronic pain the most structurally resilient revenue segment. Its leadership is further supported by prescriber familiarity, repeat-use economics, and integration into multidisciplinary pain management protocols across outpatient and specialty care settings.

Mental health is likely to be the fastest-growing application area, driven by rising cases of anxiety, depression, PTSD, and sleep disorders, alongside increasing acceptance of cannabinoid-based neuromodulation. Growth is further fueled by demand for non-addictive alternatives and symptom-specific formulations. Neurological disorders account for 20% of demand, primarily in refractory epilepsy and neurodegenerative treatments. Oncology represents 15%, largely for adjunct management of pain and nausea, while Other applications make up 10%, encompassing emerging wellness and palliative uses with steady but secondary market contribution.

Regional Insights

North America Medicinal Cannabis Compound Market Trends

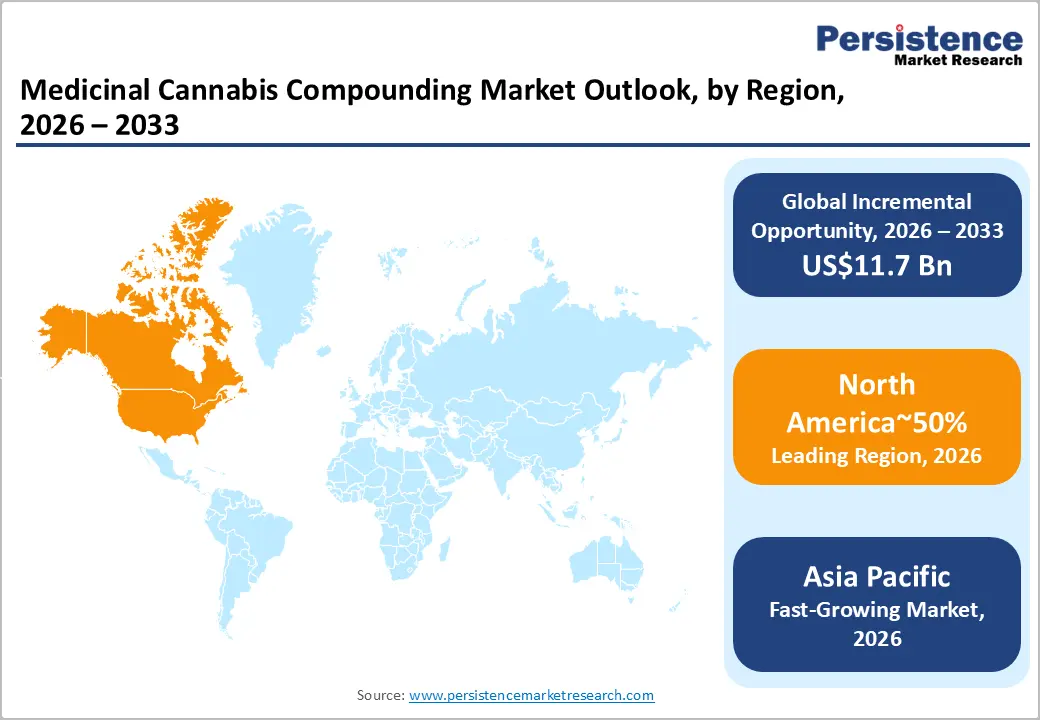

North America is expected to be the leading regional market, accounting for 50% of global market share in 2026, underpinned by a mature regulatory ecosystem, advanced healthcare infrastructure, and strong consumer adoption. The region benefits from widespread acceptance of regulated compounding practices, a large base of GMP-certified facilities, and an evolving policy environment that balances federal oversight with state-level flexibility. The competitive structure favors vertically integrated operators with scale advantages, regulatory expertise, and strong distribution control, positioning North America as the global benchmark market.

The U.S. dominates regional performance, driven by broad state-level legalization enabling compounding activities and a dense network of specialized pharmacies. Regulatory clarity through standardized quality frameworks has supported innovation while maintaining patient safety, encouraging deeper integration of compounding into holistic and wellness-focused medical practices. The U.S. also acts as the primary innovation engine, attracting institutional investment and accelerating commercialization relative to other global markets.

Europe Medicinal Cannabis Compound Market Trends

Europe is a stable market, shaped by a highly regulated healthcare environment and strong emphasis on pharmaceutical-grade compliance. Market development is driven by centralized regulatory oversight, harmonized quality standards, and increasing acceptance of cannabinoid-based therapies within formal medical systems. Unlike lifestyle-oriented markets, Europe prioritizes clinical efficacy, safety validation, and controlled distribution, which favors established operators with EU GMP capabilities and regulatory expertise.

Germany anchors regional performance, supported by a clear legal framework that streamlined prescribing pathways and enabled insurance reimbursement for compounded medical cannabis. This has positioned Germany as the reference market for broader European adoption, influencing regulatory approaches in neighboring countries. Its strong pharmaceutical infrastructure, physician acceptance, and institutional procurement mechanisms reinforce Europe’s role as a compliance-driven, medically focused market rather than a consumer-led one.

Asia Pacific Medicinal Cannabis Compound Market Trends

Asia Pacific is likely to be the fastest-growing regional market, accounting for 25% of global share in 2026, driven by expanding medical adoption, evolving regulatory acceptance, and strong manufacturing economics. The region is characterized by rapid policy experimentation, cost-sensitive healthcare systems, and cultural acceptance of plant-based therapeutics, which collectively support accelerated market expansion. Fragmented competitive structures and improving regulatory clarity continue to lower entry barriers, reinforcing Asia Pacific’s role as a global growth engine.

China plays a pivotal role due to its large-scale pharmaceutical manufacturing base and government-backed pilot programs supporting hemp-derived and medicinal compound development. Its vertically integrated supply chains, cost-efficient GMP infrastructure, and growing domestic medical acceptance position China as both a demand center and a future export hub. These structural advantages strengthen Asia Pacific’s trajectory as a fast-growing, production-driven region rather than a regulated, strained mature market.

Competitive Analysis

The global medicinal cannabis compounding market is moderately concentrated, with the top five players controlling about 40-45% of the total market value. Jazz Pharmaceuticals and GW Pharmaceuticals lead through vertically integrated cultivation, extraction, and formulation capabilities, supported by strong GMP compliance and clinical partnerships. Tilray, Aurora Cannabis, and Canopy Growth follow with scale advantages in pharmaceutical-grade extracts and standardized formulations. Competitive positioning increasingly favors players able to sustain high compliance costs, ensure batch consistency, and support prescribers with validated dosing formats, driving gradual consolidation as smaller non-compliant entities exit.

Recent strategic activity centers on geographic expansion, cost optimization, and supply chain control. Curaleaf pursued vertical integration in Europe through distributor acquisition, securing downstream pharmacy access. Bedrocan introduced GMP-certified APIs for Australian pharmacies, Organigram strengthened compounding capacity through Motif Labs acquisition, and SOMAÍ Pharmaceuticals expanded full-spectrum offerings via UK partnerships, underscoring sustained focus on scale, regulatory strength, and differentiated medical formulations.

Key Industry Developments

- In May 2025, Curaleaf International launched a range of branded medical cannabis flower products in Australia via Canngea distribution. This entry into a high-growth market emphasized clinical integrity, with plans for further formats to meet rising demand for compounded therapies.

- In April 2025, Tilray Medical introduced Good Supply Pastilles, its first medical cannabis edibles, to Australian patients. These discreet, compliant products catered to wellness-focused users, driving Tilray's market share in edibles amid a 24% sales increase in related segments.

- In January 2025, Avicanna Inc. formed a scientific and medical affairs collaboration with Vectura Fertin Pharma. The joint committee aimed to advance research and improve patient access to medical cannabis in Canada.

- In December 2024, Aurora Cannabis Inc. entered a distribution partnership with The Entourage Effect for MedReleaf Australia products. This expanded nationwide access to premium medical cannabis, supporting pharmacies and patient care in Australia.

- In October 2024, Aurora Cannabis Inc. launched an expanded medical cannabis oil range in partnership with MedReleaf Australia. The new oils offered varied cannabinoid ratios, improving tailored treatments for diverse patient needs in a growing market.

- In September 2024, Paindrainer AB partnered with Complete Care Partners LLC to accelerate the U.S. commercial rollout. This collaboration provided access to thousands of chronic pain patients, enhancing personalized digital health solutions in the medicinal cannabis compounding space.

Medicinal Cannabis Compounding Market

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2020 – 2025 |

|

Forecast Period |

2026 – 2033 |

|

Market Analysis |

Value: US$ Bn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

Companies Covered in Medicinal Cannabis Compounding Market

- Jazz Pharmaceuticals PLC

- GW Pharmaceuticals

- Aurora Cannabis Inc.

- Tilray Brands Inc.

- Canopy Growth Corporation

- Curaleaf Holdings Inc.

- Trulieve Cannabis Corp.

- Green Thumb Industries (GTI)

- Bedrocan

- Cronos Group Inc.

- Avicanna Inc.

- SOMAÍ Pharmaceuticals

- Organigram Holdings

- MGC Pharma

- MediPharm Labs

- Medisca

- Fagron

Frequently Asked Questions

The global medicinal cannabis compounding market is projected to be valued at US$9.4 billion in 2026 and is expected to reach US$21.1 billion by 2033, reflecting the rapid expansion of regulated medical cannabis programs worldwide.

Clinical acceptance is rising due to the growing prevalence of chronic pain and neurological disorders, increasing physician confidence in cannabinoid-based therapies, and demand for patient-specific dosing through compounded formulations.

The global medicinal cannabis compounding market is expected to grow at a CAGR of 12.5% between 2026 and 2033, supported by regulatory liberalization and expanding institutional participation.

The fastest growth opportunities are emerging in Asia Pacific, driven by regulatory easing, expanding medical access frameworks, pharmaceutical-grade cultivation investments, and increasing export-oriented production capacity.

Key players include Aurora Cannabis Inc., Curaleaf International, Avicanna Inc., SOMAÍ Pharmaceuticals, MedReleaf Australia, Canngea, Medcana, and Awshad.