- Technology

- Buy Now Pay Later Market

Buy Now Pay Later Market Size, Share, and Growth Forecast 2026 - 2033

Buy Now Pay Later Market by Channel (Online, POS), by End-use (Retail, Consumer Electronics, Fashion and Garment, Others; Healthcare; Leisure and Entertainment; Automotive; Others), Enterprise Size (Large Enterprises, Small and Medium Enterprises), by Regional Analysis, 2026 - 2033

Buy Now Pay Later Market Size and Trend Analysis

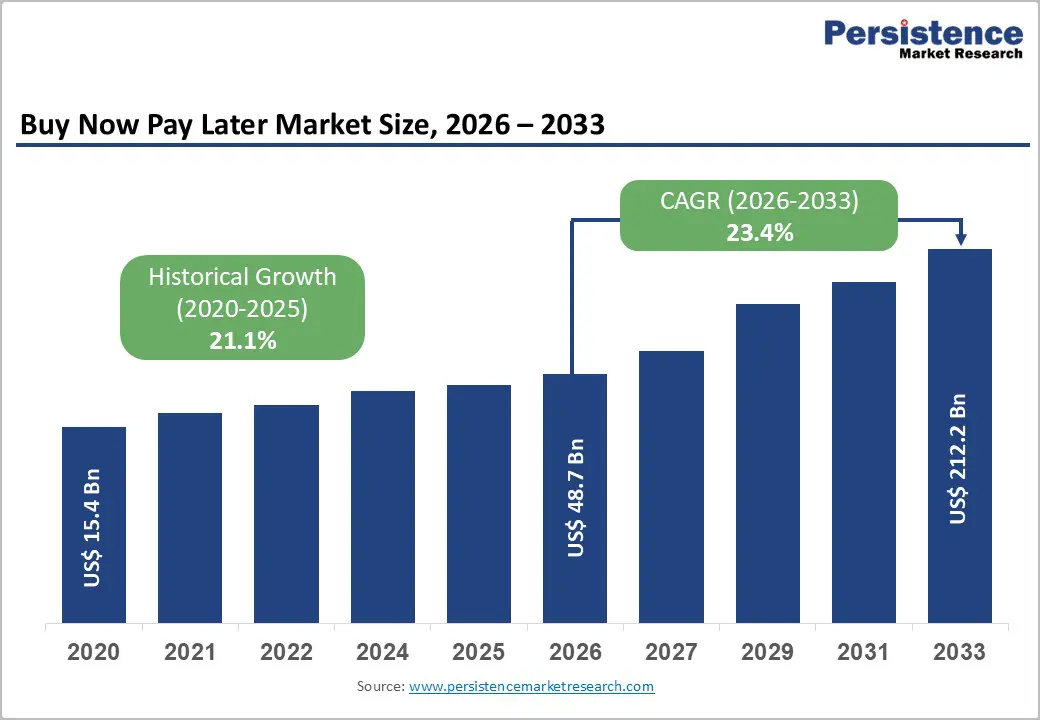

The global buy now pay later market size is expected to be valued at US$ 48.7 billion in 2026 and projected to reach US$ 212.2 billion by 2033, growing at a CAGR of 23.4% between 2026 and 2033.

This exceptional growth trajectory is primarily driven by the global shift in consumer payment preferences toward flexible, interest-free installment solutions and the rapid expansion of e-commerce ecosystems across developed and emerging markets alike. The structural decline of traditional credit card usage among younger demographics, particularly Millennials and Generation Z consumers, who collectively represent over 40% of global spending power, is catalyzing widespread BNPL adoption as a preferred alternative to revolving credit. Simultaneously, the entry of major financial institutions, technology giants, and neobanks into the BNPL space, alongside evolving regulatory frameworks that are formalizing the sector’s credibility, is broadening merchant acceptance and consumer access at an unprecedented pace, reinforcing sustained double-digit compound annual growth well into the 2030s.

Key Industry Highlights

- Leading Region: North America leads the global BNPL Market with approximately 31% of market share in 2025, driven by the U.S.’s vast e-commerce transaction base, deep BNPL merchant integration across major retailers, and the competitive presence of globally significant players including Affirm, PayPal Pay Later, and Perpay.

- Fastest Growing Region: Asia Pacific is the fastest-growing BNPL region, propelled by India’s rapidly expanding fintech BNPL ecosystem, China’s embedded digital credit infrastructure, and Southeast Asia’s large underbanked populations gaining first-time credit access through mobile-first BNPL platforms across Indonesia, Vietnam, and the Philippines.

- Dominant Segment: Online channel dominates with approximately 67% market share in 2025, reflecting BNPL’s foundational integration within e-commerce checkout workflows globally, where real-time credit decisioning and seamless installment options consistently reduce cart abandonment and lift merchant average order values by 20-30%.

- Fastest Growing Segment: Automotive is the fastest-growing BNPL end-use segment, as BNPL financing expands beyond traditional retail into vehicle accessories, EV charging equipment, and used car purchase financing, sectors with high average transaction values that are structurally well-suited to installment payment architectures.

- Key Opportunity: Healthcare BNPL represents the most compelling emerging opportunity, with over 40% of American adults carrying medical debt according to the Kaiser Family Foundation, creating a massive underserved market for installment-based medical expense financing across hospital systems, dental practices, and digital health platforms globally.

| Key Insights | Details |

|---|---|

| Buy Now Pay Later Market Size (2026E) | US$ 48.7 Billion |

| Market Value Forecast (2033F) | US$ 212.2 Billion |

| Projected Growth CAGR (2026 - 2033) | 23.4% |

| Historical Market Growth (2020 - 2025) | 21.1% |

Market Dynamics

Drivers - Accelerating E-Commerce Growth and Shifting Consumer Payment Preferences Fueling BNPL Adoption

The explosive growth of global e-commerce is the most consequential structural driver underpinning Buy Now Pay Later market expansion. According to the United Nations Conference on Trade and Development (UNCTAD), global e-commerce sales surpassed US$ 6.6 trillion in 2023 and continue to grow at a robust pace across both developed and developing economies. BNPL solutions are deeply embedded within online checkout workflows, offered natively by platforms including Amazon, Shopify, and Walmart, providing consumers with seamless, frictionless access to installment financing at the point of purchase without a credit check requirement. Research from the Consumer Financial Protection Bureau (CFPB) indicates that BNPL loan originations in the United States alone grew from US$ 2 billion in 2019 to over US$ 24.2 billion in 2021, reflecting the extraordinary velocity of adoption. The psychological appeal of splitting purchases into manageable, interest-free installments is proving particularly compelling for high-consideration purchases in consumer electronics, fashion, and home goods, consistently lifting average order values for BNPL-integrated merchants by 20-30% compared to standard checkout flows.

Rising Financial Inclusion Agenda and Underbanked Population Creating a Vast Addressable Market

BNPL platforms are uniquely positioned to serve the globally significant underbanked and credit-underserved population, which remains largely excluded from conventional credit card and personal loan products. According to the World Bank Global Findex Database, approximately 1.4 billion adults worldwide remained unbanked as of the most recent survey, with billions more possessing bank accounts but lacking access to formal credit products. BNPL providers, by leveraging alternative data sources including transaction histories, digital footprints, and behavioral analytics for credit decisioning, are able to extend installment credit to consumers who would be declined by traditional credit scoring models. In high-growth markets such as India, Indonesia, Brazil, and Nigeria, BNPL is emerging as a primary vehicle for bringing first-time credit users into the formal financial ecosystem. India’s Reserve Bank of India (RBI) has acknowledged BNPL as a meaningful contributor to the country’s financial inclusion policy goals, recognizing the sector’s role in expanding credit access across underserved populations. This vast and largely untapped addressable market represents a structurally durable and globally significant demand driver for BNPL platforms through the forecast period.

Restraints - Rising Consumer Debt Levels and Default Risk Undermining Platform Profitability

The rapid growth of BNPL adoption has been accompanied by mounting concerns regarding consumer over-indebtedness and credit risk. A study published by the Consumer Financial Protection Bureau (CFPB) in 2023 found that BNPL users in the United States were significantly more likely to carry revolving credit card debt, use overdraft facilities, and have subprime credit scores compared to non-BNPL users, highlighting the elevated credit risk profile of the segment’s core user base. As macroeconomic conditions tighten, with elevated interest rates increasing the cost of capital for BNPL providers who fund their installment portfolios, rising delinquency and default rates are compressing margins and threatening platform unit economics, with some providers publicly disclosing increased provisions for credit losses.

Intensifying Regulatory Scrutiny Imposing Compliance Costs and Operational Constraints

The regulatory environment governing BNPL services is tightening substantially across major markets, introducing compliance complexity and cost burdens that are reshaping the competitive landscape. The UK’s Financial Conduct Authority (FCA) has proposed bringing BNPL products within the scope of the Consumer Credit Act, requiring credit affordability checks and mandatory financial promotions approval, a framework that, when enacted, will significantly increase compliance costs for BNPL operators in one of the sector’s largest markets. Similarly, the European Consumer Credit Directive (2023/2225/EU), adopted in November 2023, explicitly extends consumer credit regulations to many BNPL products previously exempt from such requirements across the European Union. These evolving regulatory obligations are increasing operational complexity for BNPL providers, potentially creating barriers to entry that favor well-capitalized incumbents while constraining the growth of smaller and fintech-native BNPL platforms.

Opportunity - Automotive BNPL Emerging as the Fastest-Growing End-Use Vertical with Transformational Potential

The automotive sector represents one of the most compelling and underexplored growth frontiers for Buy Now Pay Later platforms, with the segment projected to expand at a significantly above-average CAGR through 2033. The application of BNPL in automotive contexts, spanning vehicle accessories and parts purchases, electric vehicle (EV) charging equipment financing, insurance premium installments, and increasingly, partial financing of used vehicle purchases, is gaining meaningful commercial traction. Splitit Payments has pioneered automotive BNPL integrations with major dealership networks, enabling consumers to spread accessory and service costs interest-free over existing credit limits.

The global used car market, valued at approximately US$ 1.6 trillion according to Statista, presents a particularly large opportunity for BNPL platforms offering deferred payment solutions to consumers in the sub-prime and near-prime credit segments who lack access to traditional auto loans. As EV adoption accelerates globally and consumers face higher upfront equipment costs, BNPL-driven financing solutions for home chargers, battery upgrades, and fleet management technology are expected to generate significant incremental demand, establishing automotive as a structurally high-growth application domain for the sector.

Healthcare BNPL Unlocking Significant Untapped Demand Amid Rising Out-of-Pocket Patient Costs

Healthcare is emerging as a strategically significant growth opportunity for BNPL providers, driven by escalating out-of-pocket medical expenses and the growing consumer expectation of flexible, transparent payment options in healthcare settings. In the United States, the Kaiser Family Foundation (KFF) estimates that over 40% of American adults carry medical debt, and a significant proportion of patients delay or forgo necessary medical treatment due to upfront cost concerns. BNPL products tailored for healthcare, enabling patients to split dental bills, elective procedure costs, vision care expenses, and pharmacy payments into manageable installments, are being adopted by healthcare providers as a tool to improve patient payment compliance and reduce accounts receivable aging. CareCredit (a Synchrony Financial product) and newer BNPL-native entrants are expanding healthcare installment financing availability across hospital systems, dental practices, and veterinary clinics. As digital health platforms and telehealth services proliferate globally, the WHO projects that digital health spending will continue to grow significantly across OECD nations, the integration of embedded BNPL payment options within healthcare provider billing workflows represents a major and largely untapped revenue opportunity for BNPL operators through 2033.

Category-wise Analysis

Channel Insights

The online channel dominated the global buy now pay later market, commanding approximately 67% of total market share in 2025. The online channel’s leadership reflects the foundational alignment between BNPL’s digital-native user experience and the e-commerce transaction environment in which it was originally conceived and most deeply integrated. BNPL providers including Klarna, Afterpay, Affirm, and Zip Co. have built their core value propositions around seamless integration within online checkout workflows, embedding installment payment options directly within merchant websites and mobile apps as native payment methods alongside cards and digital wallets. The online channel benefits from frictionless instant credit decisioning powered by real-time algorithms, enabling sub-second approval outcomes that preserve the checkout momentum critical to reducing cart abandonment. The average documented online shopping cart abandonment rate stands at approximately 70%, with payment complexity cited as a leading abandonment trigger, a dynamic that BNPL’s simplified checkout integration directly addresses. The POS (point-of-sale) channel represents the fastest-growing segment, gaining rapid momentum as BNPL QR code and tap-to-pay integrations expand into physical retail, restaurant, and healthcare billing environments.

End-user Insights

By end-user, retail is the dominant segment, accounting for approximately 72% of total market share in 2025. Retail’s commanding leadership reflects BNPL’s origins as a checkout financing solution specifically designed to address the friction inherent in high-consideration retail purchases, particularly in Consumer Electronics, Fashion and Garment, and home goods categories, where average transaction values frequently exceed typical single-payment comfort thresholds.

Consumer Electronics represents the largest retail sub-segment, with platforms including Affirm and Klarna reporting that electronics purchases, including smartphones, laptops, and gaming consoles, consistently rank among the highest average order value BNPL transactions globally. Fashion and Garment is a close second, with Afterpay, now part of Block, Inc., building its initial growth primarily through fashion retail integrations. The global retail sector’s continued digital transformation, combined with growing merchant recognition that BNPL integration lifts both conversion rates and average basket sizes by 20-30%, is sustaining retail’s dominant position in the BNPL end-use landscape. Automotive represents the fastest-growing end-use vertical through the forecast period.

Enterprise Size Insights

Large enterprises dominated the global buy now pay later market by enterprise size, representing approximately 58% of total share in 2025. The dominance of large enterprises reflects the greater technical and financial resources available to major retail chains, multinational e-commerce platforms, and healthcare conglomerates for integrating and promoting BNPL payment options within their digital commerce infrastructure. Enterprise-grade BNPL integrations, typically implemented through dedicated API connections with providers such as Klarna, Affirm, and PayPal (via its Pay Later product), require significant technical investment in payment gateway configuration, checkout flow optimization, and back-end reconciliation systems that larger organizations are better positioned to resource and manage. Major enterprise merchants including Target, Apple, IKEA, and H&M have deployed BNPL as a standard checkout option across their digital and physical retail channels, generating substantial transaction volume. Small and Medium Enterprises (SMEs) represent the fastest-growing enterprise size segment, propelled by the expanding availability of plug-and-play BNPL plugins for platforms including Shopify, WooCommerce, and Magento that dramatically lower the technical barrier to BNPL integration for smaller merchants.

Regional Insights

North America Buy Now Pay Later Market Trends and Insights

North America leads the global market, holding approximately 31% of total market share in 2025, anchored by the United States, the world’s most commercially advanced BNPL market by transaction volume, merchant acceptance penetration, and competitive density. The U.S. market benefits from a highly sophisticated e-commerce ecosystem, with eMarketer data indicating that U.S. e-commerce sales exceed US$ 1 trillion annually, providing an enormous transaction base into which BNPL services are deeply integrated. Key U.S.-based BNPL providers including Affirm, Inc., which counts Amazon and Shopify among its anchor merchant partners, and Perpay Inc. have established substantial consumer user bases, while PayPal’s Pay Later solution leverages the company’s 430+ million active accounts globally to drive BNPL transaction volume at scale.

The North American regulatory environment is in a pivotal evolution phase. The Consumer Financial Protection Bureau (CFPB) has moved to classify BNPL providers as credit card issuers under the Truth in Lending Act (TILA), requiring periodic billing statements, dispute resolution rights, and refund credit obligations, a rulemaking that, while adding compliance overhead, simultaneously increases consumer confidence in the product, which is expected to support long-term market growth. Canada is a secondary but growing market, with BNPL adoption expanding through integrations with major Canadian retailers and the growing presence of international BNPL platforms. The region’s innovation ecosystem continues to attract substantial venture capital and institutional investment into BNPL technology infrastructure, reinforcing North America’s competitive lead in product sophistication.

Europe Buy Now Pay Later Market Trends and Insights

Europe represents the second-largest regional market for Buy Now Pay Later, with Sweden, home of Klarna, the global BNPL market pioneer, holding a disproportionate influence over the region’s BNPL innovation trajectory. Germany, the United Kingdom, France, and Spain collectively constitute the region’s largest national BNPL markets, each at different stages of regulatory maturation and consumer adoption depth. Klarna’s deep market penetration in Germany and the Nordics, where the company reports over 90 million global active users, underscores the region’s position as a global BNPL leader in terms of consumer familiarity and merchant integration breadth. The UK remains the largest single national BNPL market in Europe by transaction volume, with approximately 17 million UK adults having used a BNPL service at least once according to the Financial Conduct Authority (FCA).

The European regulatory landscape is undergoing substantial harmonization under the EU Consumer Credit Directive (CCD2), Directive (EU) 2023/2225, which mandates that BNPL products offering deferred payment terms meet standardized affordability assessment and transparency requirements across all EU member states by November 2025. This framework, while increasing near-term compliance costs, is expected to build long-term consumer trust and market credibility. France and Spain are experiencing accelerating BNPL adoption in e-commerce fashion and electronics retail, supported by growing domestic fintech ecosystems. The region’s strong regulatory culture, once a source of uncertainty, is increasingly being viewed as a competitive advantage that filters out lower-quality providers and elevates the operational standard of market participants.

Asia Pacific Buy Now Pay Later Market Trends and Insights

Asia Pacific is the fastest-growing regional market for Buy Now Pay Later, projected to register a robust CAGR significantly above the global average through 2033, driven by the world’s largest concentration of mobile-first digital consumers, an enormous and rapidly growing e-commerce ecosystem, and vast underbanked populations across key high-growth markets. China’s domestic BNPL ecosystem, dominated by Ant Group’s Huabei and JD.com’s JD Baitiao embedded installment credit products, represents by far the largest BNPL market in the region by transaction volume, integrated within the country’s super-app payment infrastructure. However, regulatory tightening by the People’s Bank of China (PBOC) and the China Banking and Insurance Regulatory Commission (CBIRC) has moderated growth of the largest domestic platforms, creating space for innovation in adjacent segments.

India is one of the most dynamically growing BNPL markets globally, with platforms including Slice, Simpl, OlaMoney Postpaid, and MobiKwik ZIP reporting rapid user base expansion among India’s massive young, urban, digitally-enabled consumer population. The Reserve Bank of India (RBI) has progressively developed a regulatory framework for digital lending that is bringing greater governance and consumer protection to the Indian BNPL ecosystem, supporting long-term market credibility.

In Southeast Asia, platforms including LatitudePay and regional neobanks are serving rapidly growing consumer bases in Indonesia, Philippines, Thailand, and Vietnam, markets where smartphone penetration is rising sharply and traditional banking credit access remains limited. Japan and Australia are mature BNPL markets, with Zip Co., Ltd. and Openpay operating established consumer and merchant networks across Australasia, while Japan’s market is characterized by a distinct cultural preference for installment payment structures that creates natural BNPL adoption affinity.

Competitive Landscape

The global buy now pay later market exhibits a moderately fragmented competitive structure at the global level, but shows consolidation within national and regional markets. Leading platforms including Klarna, Afterpay (Block, Inc.), Affirm, and PayPal Pay Later, command dominant positions in their respective core geographies through first-mover advantage, deep merchant integration networks, and superior brand recognition. Competitive differentiation is increasingly centered on data analytics capabilities, credit risk modeling sophistication, embedded finance partnerships with banks and retailers, and geographic expansion into high-growth emerging markets. Emerging trends include the rise of B2B BNPL for SME trade finance, BNPL integration within super-apps, and bank-led BNPL products from institutions such as HSBC Group seeking to defend their retail banking share. Strategic M&A activity and white-label BNPL infrastructure partnerships are reshaping competitive boundaries.

Key Developments:

- February 2026: Airbnb expanded its “Reserve Now, Pay Later” feature globally, allowing travelers to secure eligible bookings without upfront payment and defer charges until shortly before check-in.

- November 2025: Flipkart’s fintech arm Super.money plans to launch Buy Now Pay Later services in India by partnering with banks, expanding beyond UPI payments to offer credit at e-commerce checkout.

- January 2025: Klarna Inc. filed for an initial public offering (IPO) in the United States, targeting a valuation of approximately US$ 15 billion, marking one of the most anticipated fintech listings of 2025 and signaling renewed investor confidence in the BNPL sector’s long-term profitability potential.

Companies Covered in Buy Now Pay Later Market

- Afterpay Limited (Block, Inc.)

- Affirm, Inc.

- PayPal Holdings, Inc.

- Perpay Inc.

- Klarna Inc.

- Openpay

- Splitit Payments, Ltd.

- HSBC Group

- LatitudePay Financial Services

- Zip Co., Ltd.

- Slice

- OlaMoney Postpaid

- Simpl

- MobiKwik ZIP

- Amazon Pay Later

- Sezzle Inc.

- Paidy Inc. (PayPal)

- Laybuy Group Holdings

- Scalapay S.r.l.

- Tabby

Frequently Asked Questions

The buy now pay later market is projected to reach US$ 48.7 billion in 2026, growing strongly from US$ 15.4 billion in 2020 due to rapid e-commerce expansion and shifting payment preferences.

Demand is driven by global e-commerce growth, rising financial inclusion needs, and increasing preference for installment-based payments among Millennials and Gen Z.

North America leads with around 31% share, supported by strong U.S. e-commerce penetration and widespread merchant adoption of BNPL platforms.

Major opportunities lie in automotive installment financing and healthcare BNPL solutions addressing rising medical payment burdens.

Key players include Klarna, Afterpay, Affirm, PayPal, Zip, Splitit, HSBC, Perpay, Sezzle, Paidy, Tabby, Laybuy, and others.