- Retail

- Binder Clips Market

Binder Clips Market Size, Share, and Growth Forecast, 2026 - 2033

Binder Clips Market by Product Type (Standard, Mini, Heavy-duty, Spring), Size (Small, Medium, Large), Material (Plastic, Metal, Eco-Friendly), and Regional Analysis for 2026-2033

Binder Clips Market Share and Trends Analysis

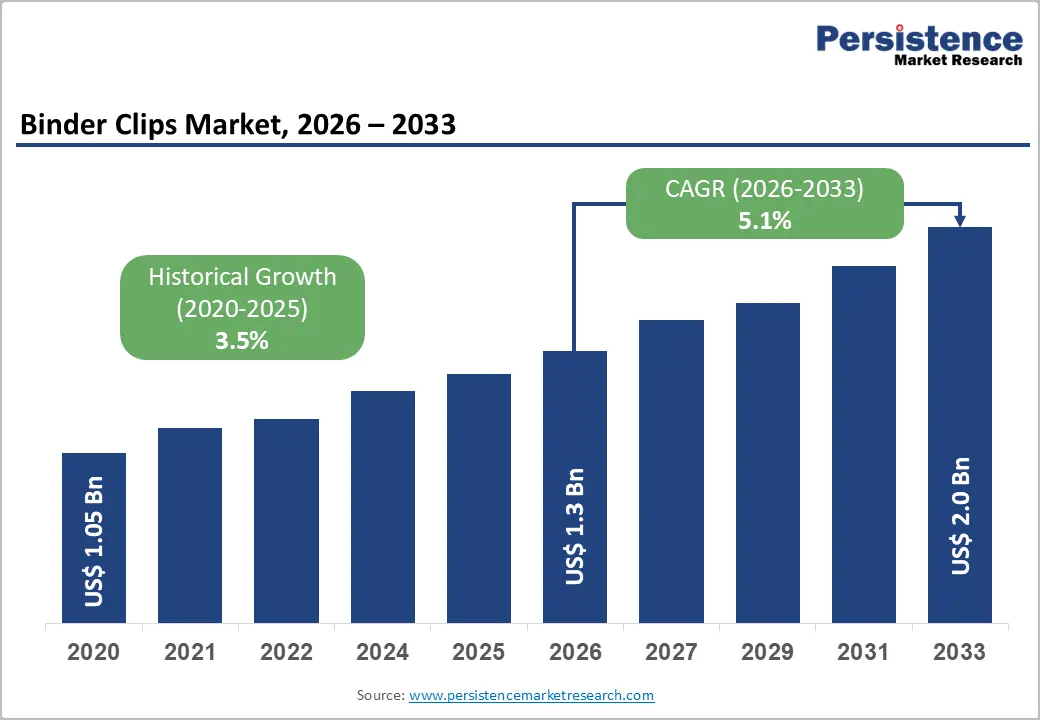

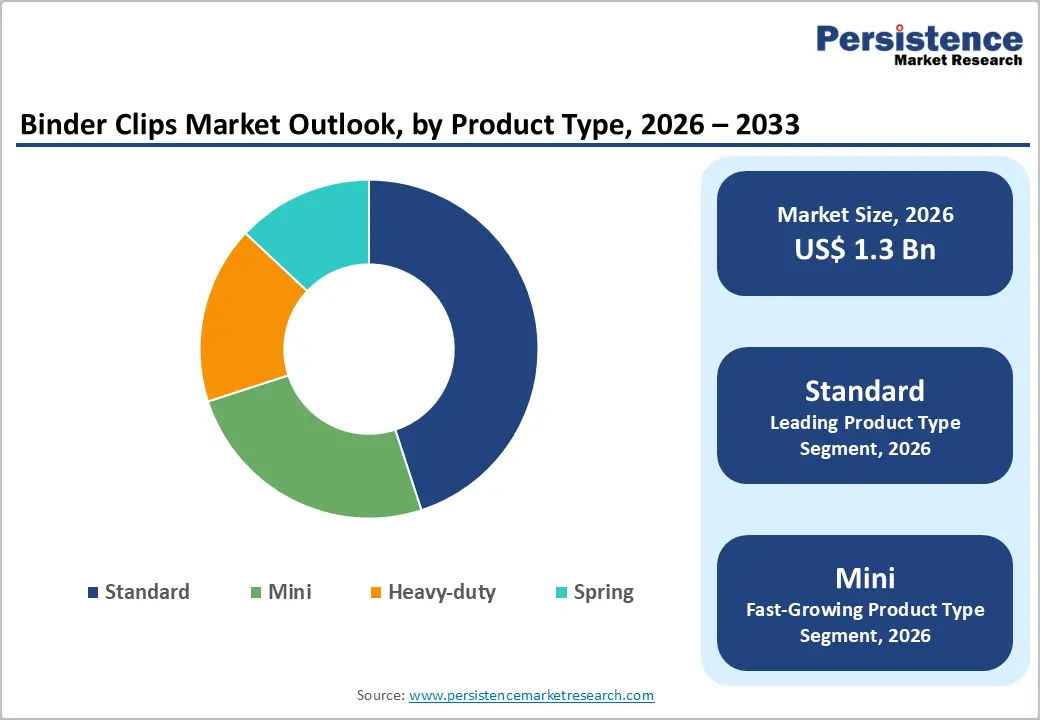

The global binder clips market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026−2033. This sustained growth trajectory is driven by the structural expansion of the global office products sector, rising commercial and educational infrastructure in emerging economies, and incremental product innovation in materials and design. The market demonstrates resilience across economic cycles due to the essential nature of document organization tools in government, education, and professional services sectors. Innovations in reusable, eco-friendly, and rust-resistant materials are opening new addressable markets in premium office segments, while bulk procurement by large institutional buyers continues to anchor volume demand.

Key Industry Highlights

- Product Type Dynamics: Standard binder clips are set to command an estimated 58% revenue share in 2026, whereas mini binder clips are likely to be the fastest-growing segment through 2033.

- Size Dominance: Medium clips are slated to dominate with approximately 43% revenue share in 2026, while large clips are expected to be the fastest-growing segment over the 2026-2033 forecast period.

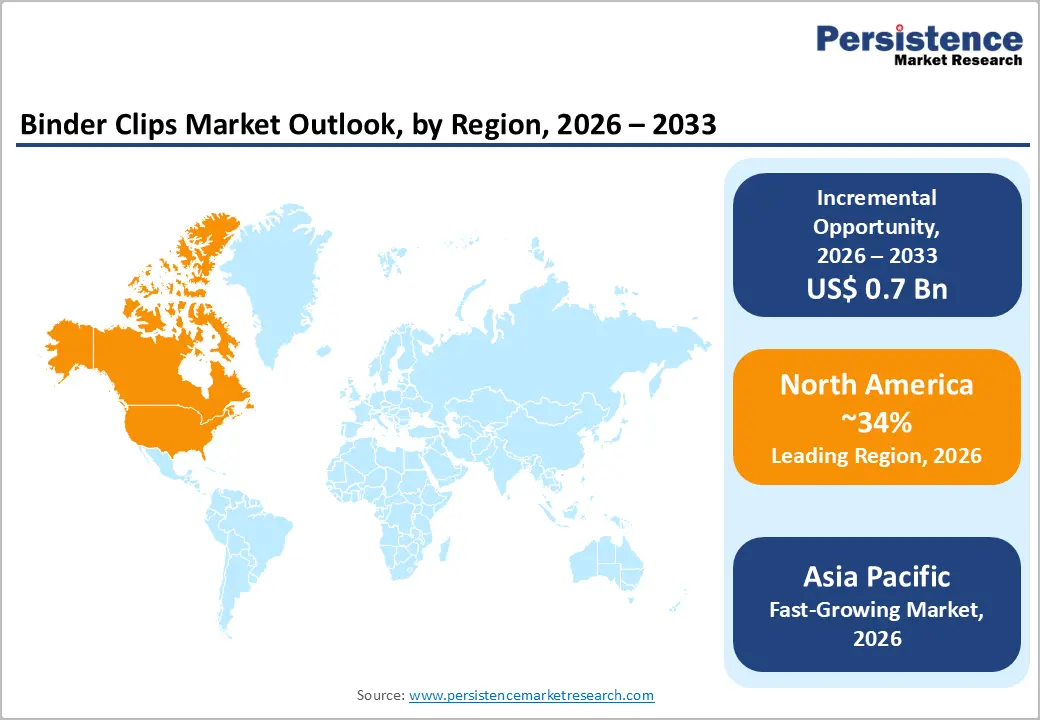

- Regional Leadership: North America is poised to hold about 34% market share in 2026, supported by a large corporate services economy and extensive government procurement infrastructure.

- Fastest-growing Market: The Asia Pacific market is likely to be the fastest-growing through 2033, powered by an expanding corporate sector and burgeoning educational institutions.

| Key Insights | Details |

|---|---|

| Binder Clips Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 2.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth of the Global Office Products & Stationery Sector

Binder clips function as essential organizational tools within modern office environments and are benefiting from broader developments across the commercial workspace sector. Corporations are increasing investments in workplace infrastructure following the COVID-19 pandemic as companies expand office footprints across North America, Europe, and Asia Pacific. These expansions are generating sustained demand for operational consumables that support daily administrative activities, including binder clips. Large organizations in industries such as financial services, legal services, healthcare administration, and public sector institutions are relying on these products to maintain efficient document management and workflow coordination.

Organizations are also adopting binder clips for a wider range of functional uses that extend beyond traditional document binding. Employees are using these clips for cable organization, quick assembly of project materials, and temporary bundling of reports or training resources. Managers are increasingly selecting durable and reusable options that support waste reduction objectives and align with corporate sustainability commitments. Suppliers are responding to these expectations by introducing customizable designs that offer varied sizes, enhanced grip strength, and improved material quality suited to different workplace applications. Hybrid work arrangements are further sustaining product relevance, as employees heavily rely on compact desk accessories that enable efficient physical organization alongside digital workflows.

Shift toward Sustainable & Eco-Friendly Office Products

Corporations are intensifying their emphasis on environmental sustainability, and this shift is driving product innovation as well as expansion within premium segments of the binder clips market. Several organizations are adopting the International Organization for Standardization (ISO) 14001 Environmental Management System (EMS) certification and are implementing procurement policies that prioritize environmentally responsible office supplies. These policies are encouraging manufacturers to redesign conventional products using materials that reduce environmental impact. Producers are developing binder clips from recycled steel, stainless alloy blends, and biodegradable polymer composites that meet corporate sustainability requirements while maintaining structural durability.

Moreover, suppliers are advancing innovation further by incorporating post-consumer recycled materials into manufacturing processes, which is appealing to procurement teams that are prioritizing circular economy practices. Corporate purchasing departments in regions that maintain strict environmental compliance frameworks are favoring vendors that demonstrate measurable sustainability credentials and transparent sourcing standards. This shift is motivating manufacturers to obtain environmental certifications and provide detailed documentation of supply chain traceability. Companies that are demonstrating leadership in sustainable manufacturing are strengthening relationships with institutional buyers and are securing long-term procurement agreements with large organizations.

Digital Transformation and Paperless Office Initiatives

Enterprises are accelerating the adoption of digital document management technologies, including Document Management Systems (DMS) and cloud-based collaboration platforms that enable real-time information sharing. These systems are creating structural challenges for traditional paper-based office tools such as binder clips. Organizations across North America and Europe are implementing paperless workplace initiatives to streamline administrative workflows and reduce long-term storage expenses. Regulatory frameworks are also encouraging digital documentation practices. For example, the European Union (EU) has introduced the e-Invoicing Directive, which requires electronic recordkeeping across multiple commercial sectors.

Manufacturers are therefore encountering pressure to adapt as corporate offices are prioritizing virtual organization systems over traditional physical filing practices. Many businesses are integrating document scanning technologies, automated indexing software, and digital storage platforms that are eliminating large volumes of paper-based records. However, hybrid administrative environments are still maintaining some reliance on binder clips during document review, audit preparation, and temporary file organization. Continued paper reliance in sectors such as legal services, healthcare administration, and creative industries is sustaining a baseline level of product demand despite the broader digital transition.

Raw Material Price Volatility and Supply Chain Risks

Manufacturers are producing binder clips primarily from carbon steel, galvanized steel, and stainless steel wire, which exposes the industry to fluctuations in global metal prices. These materials are experiencing cost volatility due to changing energy expenses, shifting trade dynamics, and disruptions across international supply routes. Energy price variations are directly influencing smelting, processing, and transportation costs that determine final production expenses. Geopolitical tensions and export restrictions from major steel-producing countries are also increasing uncertainty within raw material procurement cycles. Small and medium-sized manufacturers are facing the greatest pressure because they operate with narrow profit margins while serving price-sensitive buyers that prioritize affordability.

Several producers are also shifting toward regional suppliers to shorten logistics routes and reduce dependence on complex global transportation networks. By sourcing materials closer to manufacturing facilities, firms are minimizing delays caused by shipping congestion and international trade disruptions. Some manufacturers are incorporating recycled metal content into production processes to decrease reliance on volatile virgin steel supplies while supporting sustainability goals. In certain premium market segments, companies are transferring moderate cost increases to buyers who are prioritizing durability and product quality over low prices. Ongoing port congestion and unpredictable shipping timelines are increasing procurement risks, which is encouraging firms to maintain strategic buffer inventories and explore nearshoring production alternatives.

Development and Promotion of Eco-Friendly Binder Clips

Consumers are increasingly prioritizing environmental sustainability and are actively seeking products that minimize ecological impact across their lifecycle. This shift is creating a significant opportunity for binder clip manufacturers to introduce environmentally responsible product innovations. Companies are developing binder clips using recycled metals and biodegradable composite materials that appeal to environmentally conscious buyers in offices, educational institutions, and home workspaces. These products are differentiating themselves within competitive retail environments and digital marketplaces where sustainability credentials are influencing purchasing decisions. By reducing reliance on virgin raw materials and improving waste management within production systems, firms are lowering environmental impact while reinforcing brand credibility among sustainability-focused consumers.

Corporate procurement departments are increasingly selecting suppliers that demonstrate verifiable environmental sourcing practices through recognized certification frameworks such as those issued by the Forest Stewardship Council (FSC) or equivalent sustainability standards. Vendors that meet these criteria are gaining access to premium pricing opportunities and repeat purchasing agreements with large organizations. Educational marketing initiatives are also communicating lifecycle advantages that extend from raw material sourcing and manufacturing efficiency to product durability and responsible disposal. Manufacturers that are investing in environmentally responsible materials and transparent sourcing practices are positioning themselves for long-term expansion as regulatory frameworks governing sustainable production continue evolving worldwide.

Private Label and Customization Strategies

Large institutional buyers such as government departments, universities, and multinational corporations are increasingly requesting customized binder clip solutions that align with internal document management practices. This preference is creating a significant opportunity for manufacturers to diversify revenue streams beyond standard commodity products. Procurement teams are requesting specialized features that include company-branded designs, color-coded finishes for document classification, non-standard clip dimensions, and protective coatings such as anti-rust or anti-scratch treatments. Manufacturers are responding by tailoring product specifications to match the operational requirements of institutional clients, which is strengthening long-term supplier relationships. Office supply retailers and distribution partners are also promoting private label programs that allow organizations to procure branded office supplies through exclusive production agreements.

This customization strategy is strengthening trust between suppliers and institutional buyers while encouraging long-term procurement contracts rather than one-time purchasing transactions. Tailored binder clip designs are improving workplace organization by supporting structured document sorting systems that reflect internal administrative workflows. Some companies are adopting digital printing technologies that allow precise branding applications, while others are experimenting with advanced metal alloys that enhance durability and corrosion resistance. Distribution partners are also benefiting from exclusive product lines that distinguish their catalogs from competing office supply providers. As large institutions continue formalizing procurement policies and centralized purchasing systems, customized binder clips are becoming integrated into standardized supply chains.

Category-wise Analysis

Product Type Insights

The standard segment is slated to hold roughly 58% of the binder clips market revenue share in 2026, fueled by their widespread applicability across institutional and commercial environments. Offices, educational institutions, and government departments are relying heavily on these clips for routine document organization and administrative record management. Bulk procurement programs implemented by large organizations are ensuring consistent purchasing volumes, while the relatively low unit cost of standard clips continues attracting budget-conscious buyers. Established manufacturing systems and extensive distribution networks are working toward maintaining product availability across both developed economies and emerging markets.

Mini binder clips are expected to represent the fastest-growing segment during the 2026-2033 forecast period. These clips are gaining popularity for small-scale document organization, home office management, craft projects, do-it-yourself activities, and resealing food packaging. The expansion of remote and hybrid work arrangements after the COVID-19 pandemic is encouraging individuals to equip personal workspaces with compact and multifunctional stationery tools. Healthcare facilities are employing these clips in specialized tasks such as temporary specimen labeling and document attachment during medical processing procedures. This expansion into varied applications is strengthening demand beyond conventional office settings.

Size Insights

Medium binder clips are poised to dominate by accounting for approximately 43% of the total market revenue in 2026, as they provide an effective balance between holding capacity and everyday usability. These clips are widely used for standard office document bundling, legal file management, and classroom paper organization across educational institutions. Their size allows users to secure moderate stacks of documents without damaging pages or reducing ease of handling. Institutional procurement programs implemented by government departments and corporate offices are strongly favoring medium-sized clips because they meet most routine administrative needs. This standardization is strengthening the segment’s market leadership and ensuring stable production volumes for manufacturers that supply institutional buyers.

Large binder clips are expected to record the fastest growth between 2026 and 2033, on account of organizations managing high volumes of physical documentation in specific professional sectors. These clips are designed to secure thick bundles of paper efficiently, which supports document storage, archival preparation, and administrative record organization. Their reinforced metal construction allows them to maintain strong grip strength during repeated use in busy office environments. Employees in legal practices, financial institutions, and administrative departments are frequently handling extensive contracts, compliance records, and operational reports that require reliable physical bundling. This sustained reliance is preserving the relevance of larger clip formats even as digital record systems are expanding across modern workplaces.

Regional Insights

North America Binder Clips Market Trends

North America is projected to secure around 34% of the binder clips market share in 2026. This leadership position is supported by the region’s mature corporate environment and strong emphasis on workplace organization and administrative efficiency. Businesses across the U.S. rely on simple yet effective productivity tools that support structured document handling and workflow management. The United States is serving as the primary demand center due to its extensive network of corporations, universities, public institutions, and structured office environments. Consumer awareness of environmental responsibility is also influencing purchasing behavior in this region. Product innovation is seen through features such as color-coded clip designs and protective coatings that enhance durability and support efficient document classification across complex office workflows.

Retailers across North America are offering premium binder clip variants that appeal to environmentally conscious consumers as well as employees working in hybrid office environments. Educational institutions are also incorporating these tools within classroom management systems and administrative offices, which is sustaining widespread usage among students, teachers, and support staff. As remote and flexible work arrangements continue evolving, individuals are equipping home offices with practical stationery tools that support personal document organization. Market participants are increasingly investing in localized production facilities to shorten supply chains and reduce logistical costs associated with international sourcing. The region’s stable economic environment and structured purchasing channels are therefore supporting long-term market expansion driven by demand for reliable and multifunctional document fastening solutions.

Europe Binder Clips Market Trends

Europe occupies a significant position in the global market for binder clips, with Germany, the U.K., and France generating consistent demand across institutional and commercial sectors. Corporations throughout the region are relying on binder clips to support efficient document organization within structured office environments. Universities, schools, and research institutions are also incorporating these tools into both administrative processes and classroom activities, ensuring steady product utilization. Businesses are valuing binder clips for their reliability in organizing reports, contracts, training documents, and compliance materials within standardized workflow systems. The expansion of remote and hybrid working arrangements across Europe is further strengthening demand as professionals are equipping home offices with essential stationery supplies.

Government agencies and corporate organizations are continuing to emphasize workplace efficiency, which is sustaining procurement volumes through centralized bulk purchasing programs. Consumers across the region are increasingly prioritizing environmentally responsible office supplies, which is encouraging manufacturers to introduce binder clips produced from recycled materials and sustainable protective coatings. Retailers are promoting these environmentally conscious alternatives to align with broader regional sustainability initiatives and consumer expectations. Distributors are strengthening partnerships with manufacturers to deliver customized solutions that address the operational needs of specialized industries such as legal services, government administration, and financial services. Market participants are differentiating their offerings through improvements in product durability, ergonomic handling, and material quality.

Asia Pacific Binder Clips Market Trends

The market for binder clips in Asia Pacific is forecasted to register the highest 2026-2033 CAGR. Rapid industrial development is encouraging corporations to scale operations and expand administrative capacity across sectors such as manufacturing, services, and information technology. Businesses are investing in office infrastructure that supports larger workforces and more complex operational workflows. Employees in these environments are relying on binder clips for secure document management and routine administrative organization. Educational institutions are also proliferating throughout the region, propelling the need for basic office and classroom stationery supplies. China, India, and Japan are generating substantial demand due to rising business activity, growing student populations, and expanding corporate ecosystems.

Professionals across Asia Pacific are adopting structured document management practices to improve productivity within highly competitive business environments. Governments are supporting this trend through large-scale commercial infrastructure initiatives that are increasing procurement requirements for office supplies across administrative institutions. Retail distribution networks are expanding rapidly to serve both institutional buyers and individual consumers who are equipping personal workspaces. Suppliers are introducing durable binder clip designs that perform reliably in humid climates and demanding workplace conditions common across many parts of the region. Demographic expansion, urban workforce growth, and ongoing industrialization are collectively strengthening the region’s market potential.

Competitive Landscape

The global binder clips market structure features moderate fragmentation, characterized by a mix of major manufacturers maintaining a notable revenue share while numerous regional producers competing across different price segments. Leading companies such as ACCO Brands, Advantus Corp, Baumgarten's, Guangbo Group, and Deli Group control nearly two-fifths of the market. Despite this concentration, the industry continues hosting a wide range of regional manufacturers and emerging suppliers that compete in price-sensitive segments. Companies operating within the market are strengthening their positions through product innovation, portfolio expansion, and strategic partnerships that enhance operational capabilities. These collaborative arrangements are enabling firms to broaden distribution reach, improve supply chain efficiency, and access new customer groups across institutional and retail markets.

Market participants are allocating significant resources toward research and development initiatives that support product modernization and sustainability improvements. These investments are generating new product lines designed to meet evolving consumer expectations and corporate procurement standards. Manufacturers are introducing binder clips made from environmentally responsible materials and are offering versatile designs that accommodate modern workplace organization practices. Distributors are also strengthening competitive positioning by forming partnerships with manufacturers that streamline procurement networks and expand product portfolios.

Key Industry Developments

- In August 2025, Sun-Star introduced new pastel “dreamy” colors for its Ukanmuri book clip, a tool designed to hold books open from the sides without covering text or damaging pages. The lightweight clip, which has sold over 2.2 million units, is gaining popularity among students, readers, and musicians for hands-free reading and compact portability.

- In May 2025, Officemate launched “The Great Paperclip Hunt” to celebrate National Paperclip Day, releasing 1,000 special boxes containing golden paperclips and QR codes that reveal instant prizes. The campaign offers rewards such as office makeovers, ergonomic desks, and gift cards, aiming to highlight the importance of everyday workspace tools and inspire improved productivity.

Companies Covered in Binder Clips Market

- ACCO Brands Corporation

- Advantus Corp

- Baumgarten's

- Guangbo Group

- Deli Group Co., Ltd.

- Comix Group

- M&G Stationery

- True Color Stationery

- Maped Group

- Leitz

- Rapesco Office Products

- Faber-Castell

- Staedtler

- Kokuyo Co., Ltd.

- Camlin

Frequently Asked Questions

The global binder clips market is projected to reach US$ 1.3 billion in 2026.

The market is driven by urbanization, office expansion, and sustainability regulations, which are boosting the demand for organizational tools.

The market is poised to witness a CAGR of 5.1% from 2026 to 2033.

Major opportunities lie in the rapidly evolving corporate sector in developing economies, niche industrial uses, and customized eco-friendly solutions.

ACCO Brands Corporation, Advantus Corp, Baumgarten's, Guangbo Group, and Deli Group Co., Ltd. are some of the key players in the market.