- Food Ingredients & Additives

- Food Binders Market

Food Binders Market Size, Share, and Growth Forecast, 2026 - 2033

Food Binders Market by Source (Plant based, Animal based), Nature (Natural Binder, Synthetic Binder), Form (Powder, Liquid, Granules), Product Type (Starch, Gums, Proteins), End-user Industry, Application, and Regional Analysis 2026–2033

Food Binders Market Share and Trends Analysis

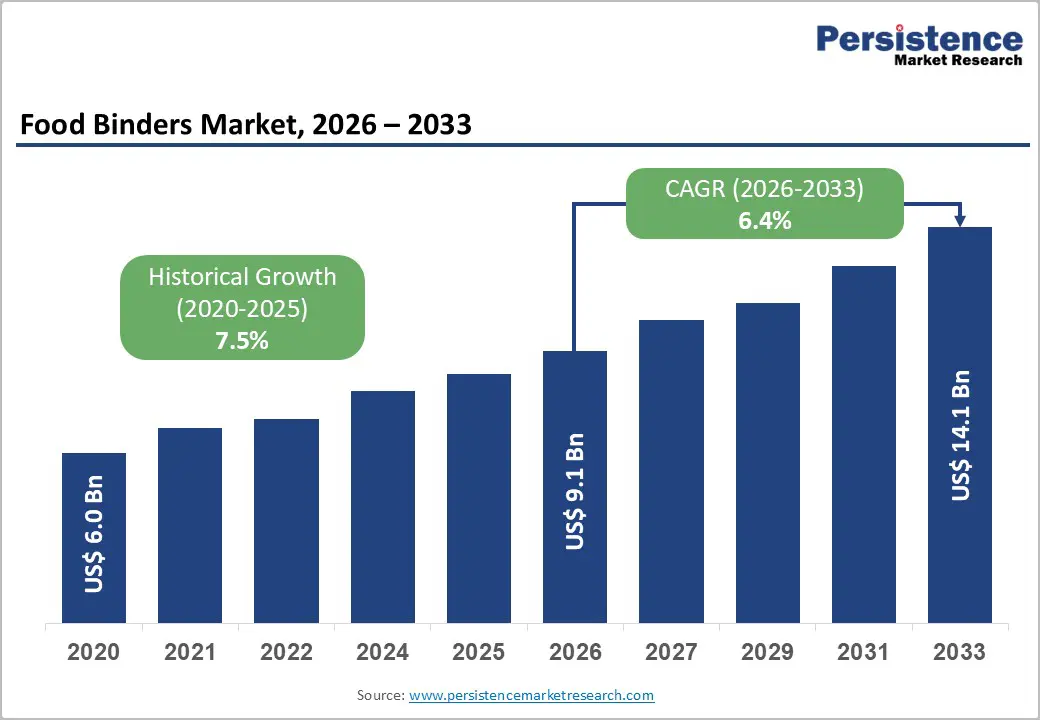

The global food binders market size is likely to be valued at US$9.1 billion in 2026 and is expected to reach US$14.1 billion by 2033, growing at a CAGR of 6.4% during the forecast period between 2026 and 2033, driven by the escalating demand for processed and convenience foods, particularly in emerging economies. The proliferation of the convenience food sector in emerging economies, alongside significant R&D investments in functional hydrocolloids and modified starches, provides robust structural support for market valuation.

Key Industry Highlights:

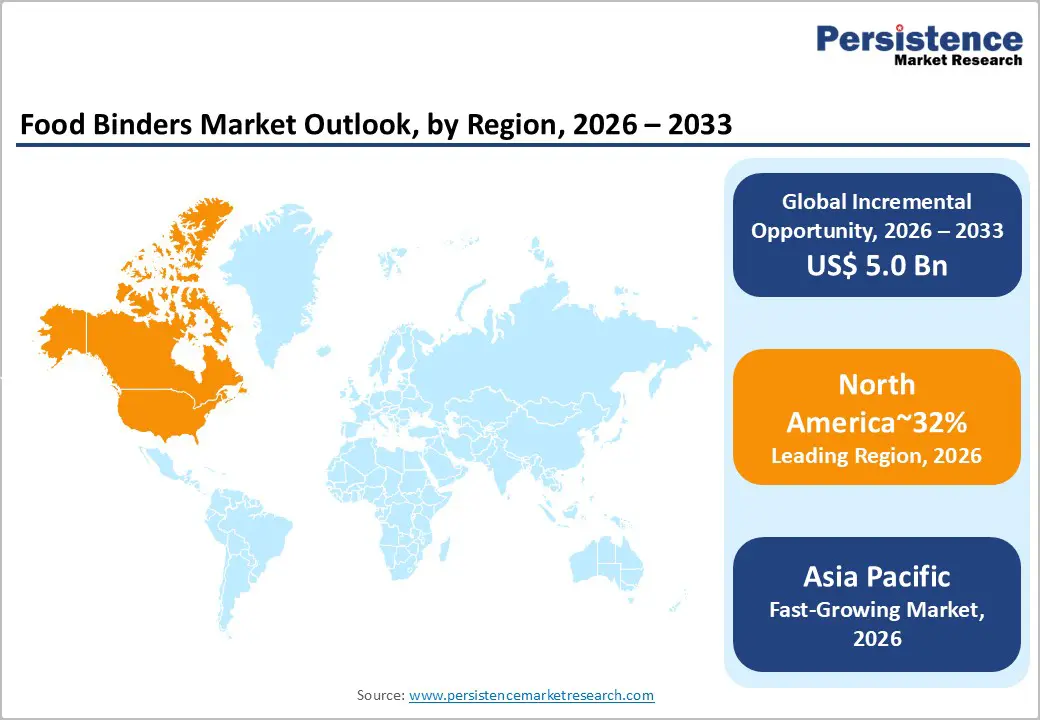

- Leading Market Region: North America is projected to remain the leading region in the food binders market, accounting for approximately 32% share, driven by advanced technological adoption, a mature regulatory framework, and a concentrated food-tech innovation hub.

- Leading Source: Plant based binders are expected to lead with 65% share, driven by clean label, allergen-friendly, and sustainable ingredient adoption, reinforced by protein blends and functional fortification.

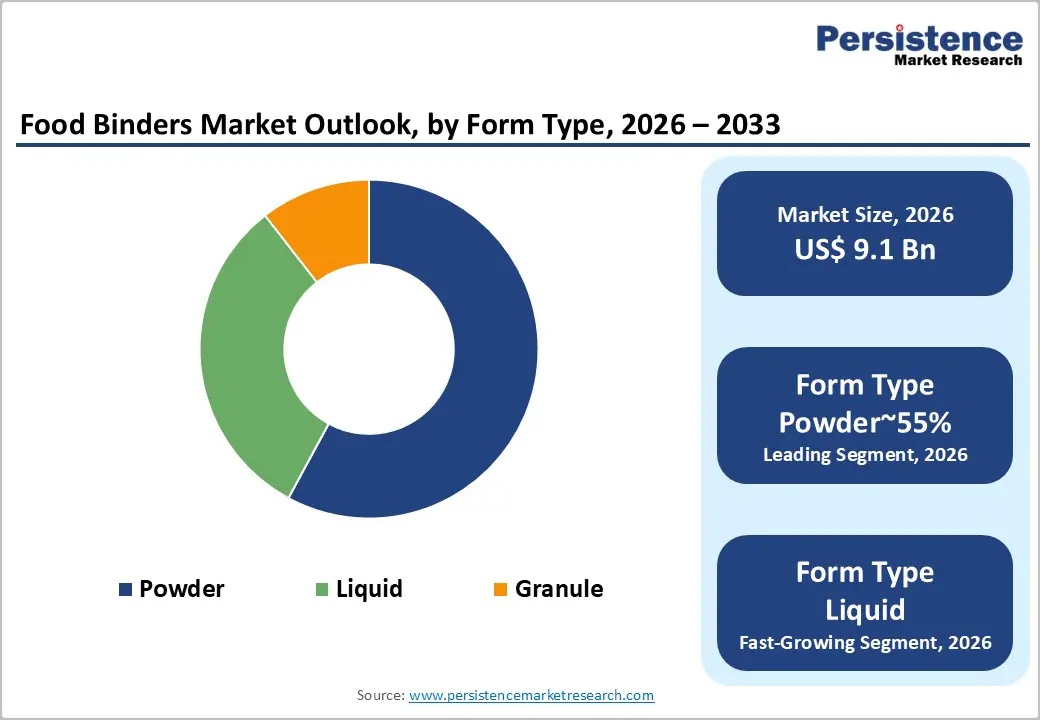

- Leading Form Type: Solid forms, including powders and granules, are projected to remain the leading format with 55% share, favored for shelf stability, dosing precision, and high-volume production efficiency.

- Leading Application: Meat, seafood, and egg alternative products are expected to lead, anchored by functional performance, texture enhancement, and commercial-scale adoption of plant-based binders.

- Key Industry Developments: In October 2025, Roquette launched AMYSTA™ L 123, a patented thermally soluble pea starch designed as a high-performance, label-friendly binder for the convenience food sector.

| Key Insights | Details |

|---|---|

|

Food Binders Market Size (2026E) |

US$9.1 Bn |

|

Market Value Forecast (2033F) |

US$14.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Urbanization and the Rise of Convenience Foods in APAC

Rapid urbanization across the Asia Pacific region, led by China and India, is structurally reshaping food consumption patterns toward processed and ready-to-eat formats. Sustained urban population expansion, cited by FAO at approximately 1% annually, is reinforcing demand for packaged foods with extended shelf stability and consistent sensory performance.

Within this context, food binders play a functional role in controlling syneresis, stabilizing emulsions, and preserving texture across complex distribution chains. This dynamic is intensifying volume demand for cost-efficient, plant-derived binders that can be deployed at scale without compromising formulation economics.

Binder selection in APAC is increasingly constrained by margin sensitivity and regulatory alignment, favoring native starches such as tapioca and corn over premium hydrocolloids. Manufacturers are optimizing formulations to balance functionality, price stability, and clean-label positioning, particularly in mass-market RTE categories.

This creates an uneven competitive landscape where suppliers with localized sourcing, processing scale, and compliance capability are better positioned to capture incremental demand, while higher-cost specialty solutions face adoption friction in price-led segments.

Raw Material Price Volatility and Supply Chain Risks

The market is experiencing sustained cost-side pressure driven by volatility in agricultural and marine raw materials essential to natural binder production. Crop-linked inputs such as guar gum and corn starch, alongside seaweed-derived carrageenan, remain exposed to climate variability, regional supply concentration, and geopolitical disruption.

These factors are compressing input cost predictability and complicating procurement planning across the value chain. Ingredient pricing instability is increasingly translating into shorter contract cycles and more frequent price resets, elevating operational risk for formulators reliant on consistent functional performance.

This volatility is reinforcing margin compression across downstream food manufacturing, particularly where hedging capacity and scale are limited. While larger ingredient suppliers have partially mitigated exposure through diversified sourcing and financial risk management, smaller buyers face constrained pricing flexibility in consumer-facing categories.

As a result, manufacturers are reassessing formulation architectures, accelerating substitution toward more stable starch systems, and prioritizing suppliers with integrated sourcing and inventory buffering capabilities, reshaping competitive dynamics under persistent cost uncertainty.

Expansion in Gluten-Free Bakery Formulation Segments

The expansion of gluten-free bakery applications is creating a structurally attractive niche for advanced food binders, as gluten removal continues to impair texture, moisture retention, and crumb integrity. Conventional formulations frequently result in dry, fragile products, elevating reliance on hydrocolloid systems that can replicate gluten’s viscoelastic function.

Binder combinations such as xanthan gum with psyllium or flax are increasingly deployed to improve gas retention, dough elasticity, and shelf stability, addressing persistent quality gaps in gluten-free baked goods.

Rising global diagnosis rates of celiac disease and non-celiac gluten sensitivity are reinforcing sustained demand for these texturizing solutions, positioning gluten-free bakery as a value-accretive subsegment within the broader binder market.

Adoption is strongest among manufacturers capable of integrating multi-component binder systems without compromising clean-label positioning or cost efficiency. This dynamic favors suppliers with formulation expertise and application-specific validation, while generic starch-based solutions face functional limitations in premium gluten-free bakery formats.

Category–wise Analysis

Source Insights

The plant-based segment is expected to be the leading and fastest-growing segment in the global food binders market, accounting for 65% share in 2026, due to the rising consumer demand for clean-label, sustainable, and allergen-friendly ingredients. Its dominance is reinforced by technological advances such as specialized protein blends and functional fortification, which enhance texture, mouthfeel, and shelf life across meat, seafood, and egg alternatives.

Pea protein has emerged as the fastest-growing source owing to its hypoallergenic, non-GMO profile, while soy continues to serve as the primary volume driver.

Market growth is fueled by health-conscious and flexitarian consumers seeking meat-like textures, alongside trends toward ethical sourcing and reduced environmental impact. Leading suppliers include Cargill, ADM, Ingredion, and Tate & Lyle, with end-product innovators such as Beyond Meat, Impossible Foods, Nestlé, and MorningStar Farms accelerating commercial adoption.

The animal-based binder segment holds a significant market share and remains the structural backbone of the traditional food industry. Industrial updates include precision extraction of collagen and gelatin for high-protein snacks, sustainability retrofitting through upcycled byproducts, and hybrid binders combining animal proteins with plant proteins for enhanced functionality.

The segment’s strength lies in unmatched thermo-reversible gelation and emulsification, simple ingredient perception, and growing demand from high-protein diets. Key drivers include sports nutrition applications using whey and casein, lower inclusion levels enhancing industrial efficiency, and the shift toward bovine and fish collagen for Halal and Kosher compliance. Leading brands include Gelita AG, Rousselot, PB Leiner, Fonterra, Glanbia, and Remedy Valley. Ethical sourcing and traceability increasingly define market positioning.

Form Insights

Solid forms, specifically powders and granules, are expected to remain the leading format in the functional food binders market, commanding a dominant 55% share due to their logistical efficiency, long shelf life, and versatility across dry-mix and rehydrated applications. Their concentrated functionality allows precise dosing with minimal waste, while innovations such as nano-milling, encapsulated solids, and agglomerated granules enhance activation speed, ingredient stability, and handling safety.

These formats support high-volume production for instant foods, powdered mixes, and single-serve products, while trends such as AI-driven micro-batching, solvent-free granulation, and smart desiccant packaging further improve consistency and sustainability.

Regulatory frameworks for combustible dust safety, contaminant detection, and traceability have reinforced the adoption of premium powders, benefiting large-scale manufacturers with advanced infrastructure. Leading suppliers such as Cargill, ADM, Tate & Lyle, Ashland, and CP Kelco continue to innovate in processing technology and formulation design, solidifying solid binders as the preferred choice for stable, scalable, and cost-effective food production systems.

Liquid binders are poised to emerge as the fastest-growing format, driven by their compatibility with automated production, high-moisture formulations, and direct-injection processing. Fully hydrated liquid systems eliminate clumping, enable precise flow-meter dosing, and reduce energy consumption by avoiding extended hydration or high-shear mixing, which is critical for sauces, dressings, meat analogues, and pre-blended emulsions.

Innovations in UHT-stable, cold-water swelling liquids and bio-liquid matrices ensure consistent viscosity, enhanced nutritional retention, and seamless integration into Industry 4.0-enabled plants. Stricter microbial and clean-label regulations have accelerated the adoption of natural liquid fibers and preservative-free formulations, supporting safer, more reliable operation. Key players, including Tate & Lyle, Cargill, Kerry Group, GEA, and Alfa Laval, provide both high-performance liquid ingredients and advanced handling technologies, positioning liquids as a rapidly expanding solution that complements traditional powder systems in modern automated food manufacturing environments.

Regional Insights

North America Food Binders Market Trends

North America is projected to remain the leading regional market, supported by advanced technological adoption, a mature regulatory framework, and a well-established innovation infrastructure. The U.S., accounting for an estimated 32% of global market value, benefits from high consumer expenditure on functional, gluten-free, and keto-aligned products, which sustains strong demand for diverse binder systems. The presence of concentrated food-tech hubs facilitates rapid product development, integration of novel plant-based ingredients, and optimized clean-label starch modifications, reinforcing both market resilience and revenue stability. Investment in sustainable pea-protein extraction and specialty hydrocolloid production further positions the region to capture incremental growth in high-value formulation segments.

Structural advantages in supply chain integration, processing standardization, and compliance adherence enhance North America’s competitiveness relative to other regions. Regulatory oversight ensures ingredient safety and label transparency, encouraging manufacturers to adopt advanced binder systems with predictable functional performance. While market saturation constrains volume expansion, technological innovation and premium product adoption continue to support sustained growth, maintaining the region’s leadership in both high-performance and clean-label binder applications.

Europe Food Binders Market Trends

Europe is projected to remain a strategically important market, supported by harmonized regulatory oversight under EFSA and well-established compliance frameworks. Germany, the U.K., and France collectively anchor the region, with strong consumer preference for non-GMO and organic products driving adoption of natural and specialty binder systems.

Sustainability-focused innovation, including circular production models and resource-efficient processing, reinforces competitive differentiation and positions European manufacturers to capture high-margin opportunities in premium bakery, dairy, and confectionery applications. Consolidation among key players enables scale efficiencies and enhances formulation expertise, sustaining market resilience amid evolving regulatory and consumer expectations.

The region’s emphasis on high-quality potato-based binders and specialty hydrocolloids underpins its technical leadership and premium positioning relative to other global markets.

Infrastructure maturity, advanced processing capabilities, and policy incentives for sustainable production support the adoption of clean-label and specialty formulations. While volume expansion is moderated by high input costs and stringent compliance requirements, Europe continues to attract investment in differentiated, functional ingredients, maintaining its strategic relevance and enabling growth in segments that prioritize quality, traceability, and formulation precision.

Asia Pacific Food Binders Market Trends

Asia Pacific is projected to remain the fastest-growing regional market, underpinned by rapid urbanization, expanding middle-class consumption, and significant manufacturing scale in China, India, and ASEAN nations. The region’s growth is concentrated in volume-driven sectors such as processed noodles, frozen seafood, and ready-to-eat meals, where high-throughput production and cost-efficient binder solutions are critical.

Structural advantages in low-cost production, combined with rising consumer demand for convenience and protein-enriched products, reinforce the adoption of both plant-based and natural binder systems, positioning the region to capture substantial incremental volume compared with more mature markets.

Regulatory evolution across APAC, including stricter food safety standards in China and India, is accelerating the shift from low-grade synthetic binders toward standardized, high-quality natural alternatives.

Investment in local sourcing, quality certification, and process standardization enhances regional reliability and mitigates operational risk for multinational and domestic manufacturers. While infrastructure maturity and policy support vary by country, APAC’s combination of scale, growth velocity, and policy momentum continues to strengthen its strategic significance within the global binder market.

Competitive Landscape

The global food binders market is moderately consolidated, with the top five players capturing a significant share, particularly within high-value hydrocolloids and specialized starches. Leading suppliers leverage economies of scale, extensive patent portfolios, and global supply chain integration to secure dominant positions, while competitive advantage is reinforced through technical support services and sustainability-focused initiatives. The lower-tier market remains fragmented, comprising regional producers that supply commodity starches and basic texturizers to localized food manufacturing operations.

Strategic differentiation is increasingly driven by product functionality, formulation versatility, and regulatory compliance across diverse applications, including bakery, dairy, and confectionery segments. Regional specialization persists, with players focusing on niche binders such as agar-agar in Asia and pectin in Europe, ensuring incremental value capture. Forward-looking dynamics indicate sustained demand for functional, clean-label binders, favoring suppliers with innovation capabilities, supply chain efficiency, and technical service integration, while fragmented regional competitors continue to serve cost-sensitive and application-specific segments.

Key Industry Developments:

- In October 2025, Ingredion expanded its FIBERTEX™ CF citrus fiber portfolio, providing multi-functional binding and texturizing solutions for clean-label bakery and savory applications.

- In September 2025, Denmark-based FERM FOOD launched a suite of cutting-edge fermented binding agents, replacing synthetic additives in plant-based meat and dairy analogues.

- In October 2024, Cargill unveiled a new line of high-efficiency starch-based binders, enhancing the structural integrity of allergen-free and vegan meat alternatives.

Companies Covered in Food Binders Market

- Cargill, Inc.

- Archer Daniels Midland (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- IFF (International Flavors & Fragrances)

- Kerry Group plc

- DSM-Firmenich

- DuPont de Nemours, Inc.

- CP Kelco

- Avebe

- Beneo GmbH

- Ashland Inc.

- MGP Ingredients

- Nexira

- Emsland Group

Frequently Asked Questions

The global food binders market is projected to be valued at US$9.1 billion in 2026 and is expected to reach US$14.1 billion by 2033.

Demand is increasing due to rising consumption of processed and convenience foods, accelerating clean-label adoption, and growing use of binders in bakery, meat analogues, and dairy applications.

The food binders market is expected to grow at a CAGR of 6.4% between 2026 and 2033, supported by functional ingredient innovation and the expansion of plant-based formulations.

The strongest opportunities are emerging in plant-based and clean-label binders, particularly tapioca-based, citrus-fiber-based, and fermentation-derived ingredients used in meat substitutes and ready-to-eat foods.

Key players include Cargill, Archer Daniels Midland, Ingredion, Tate & Lyle, IFF, Kerry Group, DSM-Firmenich, CP Kelco, DuPont de Nemours, Avebe, Beneo GmbH, and Ashland Inc.