- Technology

- Binder Jetting Services Market

Binder Jetting Services Market Size, Share, and Growth Forecast, 2026 – 2033

Binder Jetting Services by Service Provider Type (Pure-play Service Bureaus, OEM In-house Services), Service Level (Standard Printing, Full Post-Processing), Application (Prototyping, Production Parts, Tooling & Molds), and Regional Analysis 2026 – 2033

Binder Jetting Services Market Size and Trends Analysis

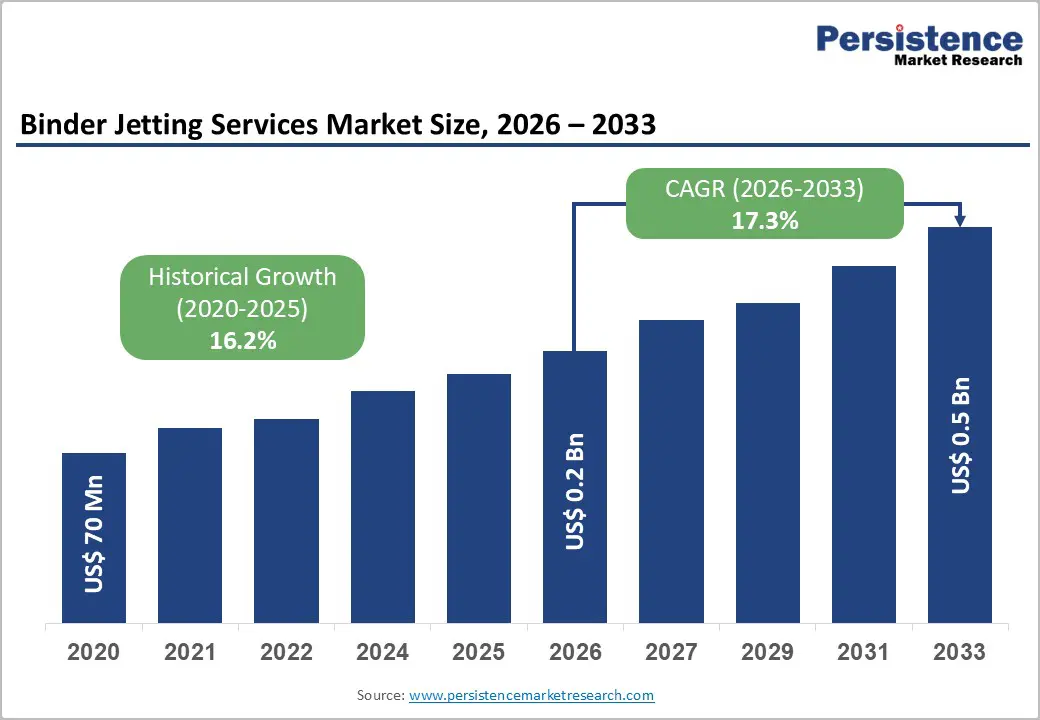

The global binder jetting services market size is likely to be valued at US$0.2 billion in 2026 and is expected to reach US$0.5 billion by 2033, growing at a CAGR of 17.3% during the forecast period from 2026 to 2033, driven by the technology's unique ability to print functional metal and ceramic parts at speeds faster than laser-based methods, significantly reducing cost-per-part. This shift is supported by the adoption of standard Metal Injection Molding (MIM) powders, which lowers material costs and democratizes access for small-to-medium service bureaus. The market remains heavily reliant on post-processing expertise, as the "green" parts produced require sophisticated sintering to achieve final density.

Key Industry Highlights:

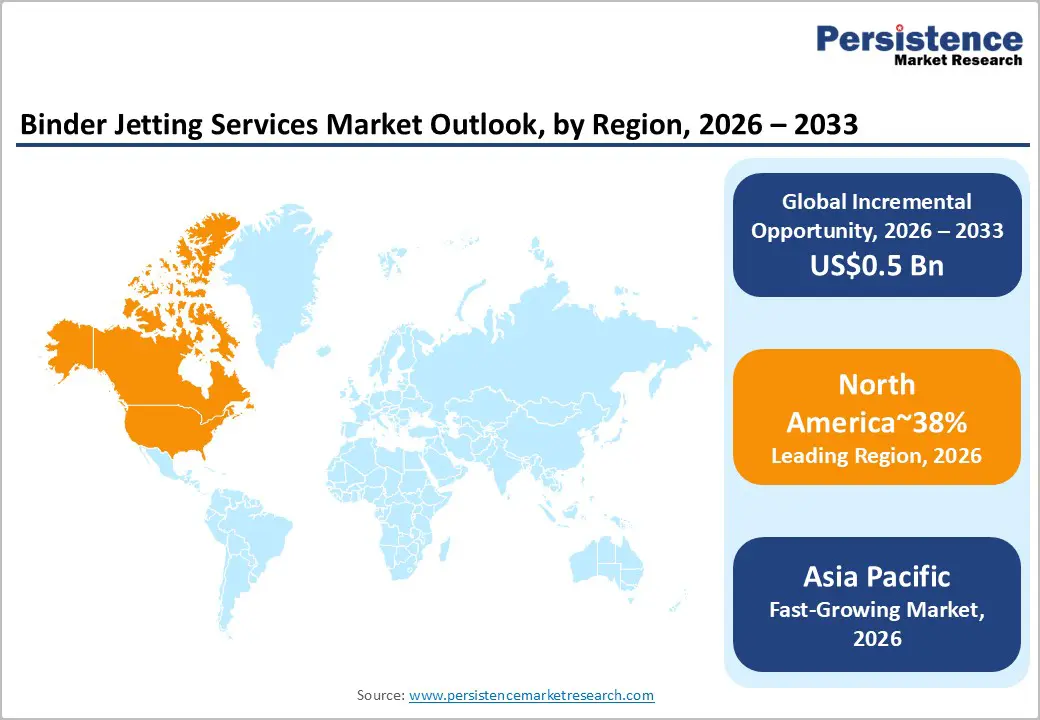

- Leading Region: North America is expected to lead the binder jetting service market with around 38% share, supported by early technology adoption, concentration of advanced manufacturing service providers, strong aerospace and defense demand, and active collaboration between service bureaus, OEMs, and research institutions.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing regional market, driven by expanding additive manufacturing adoption in China, Japan, and South Korea, rising investments in advanced manufacturing hubs, and growing demand from automotive, electronics, and industrial equipment manufacturers.

- Leading Service Provider Type: Pure play service bureaus are expected to hold approximately 58% share, reflecting their role as specialized third-party providers offering design support, material expertise, and scalable production capacity without requiring clients to invest in capital-intensive binder jetting hardware and post-processing infrastructure.

- Leading Service Level: Standard printing is expected to account for around 62% market share, driven by a high demand for green parts used in prototyping and early stage validation, where customers prioritize speed, cost efficiency, and rapid turnaround times over final part densification.

| Key Insights | Details |

|---|---|

|

Binder Jetting Services Market Size (2026E) |

US$0.2 Bn |

|

Market Value Forecast (2033F) |

US$0.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

17.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

16.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Speed and Throughput Advantages

Binder jetting offers a significant structural productivity advantage over point-by-point laser-based additive manufacturing processes, making it a strong contender for mass production of complex metal components. Unlike selective laser melting (SLM), binder jetting’s layer-wise deposition allows for dense nesting of hundreds of parts within a single build volume, enabling parallelized manufacturing at scale. This boosts parts-per-build and utilization rates, compressing production lead times for large batches and supporting continuous-flow manufacturing models that are impractical with serial exposure processes.

From an operational standpoint, binder jetting decouples build speed from part count, making it ideal for high-mix, high-volume production. The absence of high-energy lasers reduces thermal distortion and post-build stress relief needs. Green-part handling and batch sintering workflows streamline downstream processing. These features improve throughput per square meter and lower labor intensity, making binder jetting competitive with traditional methods like casting and CNC machining for series production.

As a result, binder jetting is increasingly favored for applications requiring geometric complexity, such as lattice structures, internal channels, and topology-optimized parts, without sacrificing takt time. Growing adoption by contract manufacturers and OEMs underscores its scalability, cost-effectiveness, and ability to localize production, shorten design-to-production cycles, and minimize tooling costs.

Digital Transformation and Industry 4.0

Digital transformation and Industry 4.0 are structurally repositioning binder jetting services from specialized prototyping toward high-volume, automated industrial adoption. Integration with smart factory infrastructure, IoT-enabled real-time monitoring, and predictive maintenance via digital twins is improving asset utilization and reducing unplanned downtime, while closed-loop quality control systems ensure dimensional fidelity across large production batches. AI-driven process optimization—including generative design for lattice structures, automated post-processing, and shrinkage management during sintering—is enhancing throughput, repeatability, and labor efficiency, addressing historical barriers to scale. Concurrently, supply chain digitalization is enabling on-demand manufacturing, localized production, and lean material usage, reinforcing resilience and shortening lead times, while recycling of unused powder supports circular economy objectives.

Industry 4.0 adoption is expanding the addressable opportunity by enabling mass customization and multi-material production across healthcare and consumer goods sectors. Scalable personalization and precise material allocation increase per-unit content value and broaden application breadth, while digital workflows compress operational cycles and lower per-part costs. Collectively, these dynamics are elevating binder jetting’s industrial relevance, embedding efficiency, sustainability, and flexibility as structural advantages, and differentiating market participants on their integration depth of digital controls, AI-enabled optimization, and end-to-end automated production pipelines.

Barrier Analysis – Sintering-Induced Shrinkage and Distortion

Sintering-induced shrinkage and distortion remain critical technical constraints in the binder jetting service market, as the transition from a porous green part to a solid metal or ceramic component introduces significant dimensional changes. Volumetric contraction during thermal densification requires service providers to anticipate and compensate for non-uniform shrinkage, with thin walls and complex geometries exhibiting differential behavior that can compromise tight tolerances demanded by aerospace, medical, and high-precision industrial applications. Gravity effects, thermal gradients, and interaction with support surfaces further exacerbate distortion, leading to slumping, warping, or internal stresses that challenge consistent part quality.

These technical challenges impose significant operational and economic constraints, limiting scalability and part size for high-precision production. Iterative design cycles and specialized sintering infrastructure extend lead times and reduce throughput efficiency, constraining service adoption in large or geometrically complex components. To mitigate these limitations, advanced sintering simulation software is being integrated into production workflows, generating compensated CAD models that predict and counteract distortion. This digital correction enhances dimensional accuracy, stabilizes yield, and enables broader industrial adoption by reducing trial-and-error iterations and embedding predictive process control across binder jetting applications.

Opportunity Analysis – Medical Device Customization

Medical device customization is emerging as a structurally significant growth avenue in the binder jetting service market, driven by demand for patient-specific solutions and high-volume, precision production. Binder jetting enables the fabrication of intricate orthopedic implants, cranio-maxillofacial grafts, and dental restoratives with controlled porosity and tailored geometries that enhance osseointegration, surgical outcomes, and patient recovery. The technology also supports anatomical replicas and customized surgical instruments, allowing pre-surgical planning, ergonomic optimization, and precision enhancement across complex procedures. These capabilities position binder jetting as a preferred platform for delivering individualized care while maintaining repeatable quality across diverse biocompatible materials.

Binder jetting facilitates cost-effective mass customization by producing multiple unique components simultaneously without extensive post-processing or support structures. Its material versatility accommodates metals, ceramics, and polymeric formulations, while enabling novel pharmaceutical delivery formats, including rapid-release tablets and multi-drug polypills tailored for patient-specific regimens. Collectively, these applications expand the addressable healthcare opportunity, embedding efficiency, personalization, and precision into the production pipeline and reinforcing structural advantages for service providers capable of integrating digital workflows, high-resolution printing, and clinical-grade material management across patient-centric manufacturing.

Mass Production of Automotive EV Components

The mass production of electric vehicle components presents a structurally significant growth avenue for the binder jetting service market, driven by the demand for lightweight, thermally optimized parts such as cooling jackets and fluid connectors. Binder jetting enables the cost-effective production of complex geometries that are challenging for traditional casting or machining, particularly in medium-volume production runs where tooling economics constrain conventional methods. Its ability to deliver consistent part quality with minimal support structures and high repeatability positions the technology to address the industrial-scale needs of EV manufacturers while maintaining design flexibility and rapid iteration capabilities.

Binder jetting’s scalability in medium-volume applications reduces dependency on high-cost tooling and shortens supply chain cycles, supporting localized and on-demand production models. The technology also facilitates material-efficient fabrication, enhancing thermal and mechanical performance without increasing manufacturing complexity. Collectively, these dynamics expand the addressable market for automotive EV components, embedding structural advantages in speed-to-market, customization, and operational resilience while positioning service providers to capture growth in high-value, precision-engineered segments of the electrified mobility ecosystem.

Category-wise Analysis

Service Provider Type Insights

Pure-play service bureaus are expected to dominate with an estimated 58% share in 2026, driven by the high technical complexity and capital expenditure of industrial systems, which make third-party production more viable for most end-users. Market leadership is reinforced by advanced post-processing expertise, including rebinding and sintering, which most OEMs cannot manage in-house. Bureaus maximize asset utilization through aggregated client orders, achieving lower per-part costs and predictable throughput. Sustainability initiatives, AI-enabled process control, and compliance with hazardous material regulations enhance the attractiveness of bureaus, particularly for defense and medical applications. Leading players include Desktop Metal (ExOne), HP Inc., GE Additive (Colibrium), Voxeljet, Proto Labs, and Xometry.

OEM in-house binder jetting services represent the fastest-growing segment, propelled by IP protection, supply chain control, and long-term total cost of ownership advantages. High-speed binder jetting machines, combined with simulation software like Live Sinter, now enable first-time-right production, reducing reliance on external bureaus for high-volume industrial components. OEMs are implementing micro-factory setups, hybrid manufacturing hubs integrating CNC finishing, and closed-loop powder recycling, enabling mass customization and sustainability reporting. Early adopters include Volkswagen Group, Caterpillar, and Eaton, supported by technology partners HP Inc. and GE Additive, who offer subscription or lease-to-own models to lower the entry barrier. These factors collectively drive the rapid uptake of in-house BJT for industrial and high-precision applications.

Service Level Insights

Standard Printing is projected to dominate, accounting for approximately 62% share in 2026, underpinned by its entrenched role in delivering "green" or "brown" parts across industrial workflows, prototyping labs, and sand casting foundries. Adoption remains anchored by low CapEx requirements, rapid throughput, and ease of automation, with providers and enterprises prioritizing distributed manufacturing and workflow decoupling in high-volume environments. Ongoing platform evolution, including AI-enabled binder formulation, digital file integration, and logistics-optimized part transport, continues to reinforce replacement cycles and utilization intensity. Vendors such as Desktop Metal, HP Inc., and Voxeljet are expanding portfolios with modular printing platforms and networked service models to lock in enterprise workflows and long-term contracts. This combination of mature infrastructure, cost efficiency, and predictable demand sustains the segment’s dominance within structured production ecosystems.

Full post-processing is expected to be the fastest-growing segment, driven by the increasing requirement for functional, end-use parts across aerospace, medical, and high-performance industrial applications. Growth is catalyzed by technology inflection points such as automated thermal debinding, Hot Isostatic Pressing, high-temperature sintering, and CNC finishing, which materially improve part density, surface finish, and mechanical performance. Companies including Bodycote, Materialize, and Sintavia are scaling specialized furnaces, post-processing cells, and certification services to capture early-cycle demand and embed supply chain lock-in. As industrial validation, regulatory compliance, and metallurgical confidence improve, full post-processing is expected to outpace overall market growth over the forecast period.

Regional Insights

North America Binder Jetting Services Market Trends

North America is set to maintain its leadership in the binder jetting market, holding around 38% of the global market share in 2026. This is driven by a mature industrial base, advanced manufacturing infrastructure, and early adoption of high-CapEx technologies. The region benefits from integrated R&D ecosystems, including startups, established OEMs, and research institutions, which accelerate binder jetting's deployment in sectors like aerospace, defense, and healthcare. Key players like ExOne, Desktop Metal, HP Inc., and GE Additive lead the way with high-throughput systems for metal, sand, and ceramics, along with AI-driven process optimization.

North America's robust infrastructure supports scale with advanced capabilities in materials such as titanium, aluminum, and stainless steel, alongside smart factory integration for predictive maintenance and real-time adjustments. The market is bolstered by strategic investments in healthcare and defense applications, including patient-specific implants and lightweight components. Emerging trends like multi-material deposition, AI quality control, and recyclable binder systems align with sustainability goals while enhancing industrial throughput. Innovations by Desktop Metal, HP, and GE Additive further solidify North America's position as a leader in binder jetting, underpinned by technological sophistication and regulatory compliance across high-value industries.

Europe Binder Jetting Services Market Trends

Europe maintains a strong position in the global binder jetting market, supported by a sophisticated industrial ecosystem, regulatory alignment, and a specialized manufacturing base. The region benefits from leading automotive OEMs like Volkswagen, BMW, and Stellantis, which drive high-volume adoption of inorganic sand and metal binder jetting for engine components and precision parts. Service bureaus and SMEs in Germany and Switzerland provide expert metallurgical and sintering capabilities, enabling complex applications in aerospace, luxury goods, and technical ceramics.

Regulatory frameworks such as REACH, Euro 7, and the Carbon Border Adjustment Mechanism promote the use of low-emission inorganic binders and automated green-part workflows, encouraging compliance-driven adoption. Key companies like Voxeljet AG, Sandvik, Digital Metal, and Höganäs highlight Europe’s strength in integrating materials, automation, and process monitoring to support sustainable production and supply chain localization.

Investment trends include hybrid sand-metal workflows, robotic depowdering, and in-situ monitoring to reduce labor costs and failure rates. European R&D, led by initiatives like Fraunhofer’s cold binder jetting and Triple-ACT compaction, enhances build quality and precision. These factors, combined with a focus on sustainability and energy-efficient regulations, ensure Europe’s steady leadership in high-value additive manufacturing.

Asia Pacific Binder Jetting Services Market Trends

Asia Pacific is expected to be the fastest-growing region, driven by rapid industrial scaling, cost-efficient adoption, and integration into high-volume manufacturing sectors. China, India, and Southeast Asia lead in electronics, automotive, and EV components, with manufacturers such as EasyMFG, Fenghua Pingshan, and Wipro 3D providing accessible metal and sand BJT systems. Government initiatives, including China’s Additive Manufacturing Action Plan and India’s NSAM, incentivize the replacement of traditional casting with binder jetting, supporting high-speed production while localizing supply chains. APAC also benefits from hybrid sintering solutions, recycled powder utilization, and multi-nozzle printhead innovations, enabling consistent high-volume output across consumer electronics, architectural materials, and medical implants.

Companies such as Ricoh and Kocel exemplify regional capability in large-scale, complex BJT applications, while open-powder ecosystems lower barriers for SMEs. The region’s growth is reinforced by labor-to-automation transitions, increasing EV and smart city infrastructure demand, and medical tourism applications in India and Thailand. Advanced AI inspection systems, cold-pulp and bio-binder applications, and in-line quality control allow APAC to sustain accelerated deployment without compromising precision. Technological innovation, including multi-nozzle printheads, cold-pulp BJT, and in-line AI inspection, is further consolidating regional leadership. Sustainability efforts in Japan and open-powder ecosystems enhance efficiency and cost competitiveness.

Competitive Landscape

The global binder jetting services market is moderately fragmented. While the top hardware OEMs (HP, Desktop Metal) hold significant influence through their own service networks and partner ecosystems, the actual service delivery is distributed among hundreds of independent bureaus. It is estimated that top players control 35-40% of the high-end production market. Leading players differentiate themselves not just by printing, but by their “Furnace Knowledge,” the proprietary recipes and cooling cycles used during sintering to ensure part density and dimensional accuracy.

Key Industry Highlights:

- In November 2025, HP announced innovations to reduce cost per part by 20% by 2026, including new sustainable materials like HP 3D HR PA 11 Gen2, which offers 80% powder reusability and 40% lower variable costs, enhancing cost-efficiency and scalability in industrial production.

- In September 2025, Desktop Metal, after filing for Chapter 11 bankruptcy in July 2025, relaunched under Arc Impact Acquisition Corporation. The relaunch enabled the deployment of binder jetting IP into a new "distributed R&D-as-a-Service network" with universities to support centralized manufacturing hubs.

Companies Covered in Binder Jetting Services Market

- Desktop Metal

- HP Inc.

- GE Additive

- Voxeljet AG

- 3D Systems

- Hoganas AB

- Sandvik Additive Manufacturing

- Proto Labs, Inc.

- Xometry, Inc.

- Materialise NV

- Oerlikon AM

- Ricoh Company, Ltd.

- EasyMFG

- Kocel Machinery

- Wipro 3D

Frequently Asked Questions

The global binder jetting services market is projected to be valued at US$0.2 billion in 2026 and is expected to reach US$0.5 billion by 2033, driven by the technology's transformation into a viable mass-production alternative with superior speed and cost-per-part advantages.

Binder jetting's layer-wise deposition allows for dense nesting of hundreds of parts in a single build, decoupling build speed from part count. This throughput advantage enables mass-production economics, reduces lead times, and makes the technology competitive with traditional methods like casting for series production of complex components.

The binder jetting services market is forecast to grow at a CAGR of 17.3% from 2026 to 2033, reflecting its rapid adoption as it shifts from a prototyping tool to a scalable production solution.

North America is the leading regional market, accounting for approximately 38% share, supported by early technology adoption, a concentration of advanced service bureaus and OEMs, and strong demand from the aerospace, defense, and healthcare sectors.

The binder jetting services market is moderately fragmented, with hardware and service leadership from Desktop Metal, HP Inc., and GE Additive. Specialized service bureaus such as Proto Labs, Xometry, and Voxeljet dominate the pure-play segment, competing on advanced post-processing expertise and "furnace knowledge" for sintering high-quality, functional parts.