- Home Care & Utilities

- Bathroom Vanities Market

Bathroom Vanities Market Size, Share, and Growth Forecast 2026 - 2033

Bathroom Vanities Market by Product Type (Floating / Wall-Mounted Vanities, Freestanding Vanities, Customized / Modular Vanities, Others), by Material (Stone, Ceramic, Glass, Wood, Metal), by Application (Residential, Non-residential), by Distribution Channel (Offline, Online), by Regional Analysis, 2026 - 2033

Bathroom Vanities Market Size and Trend Analysis

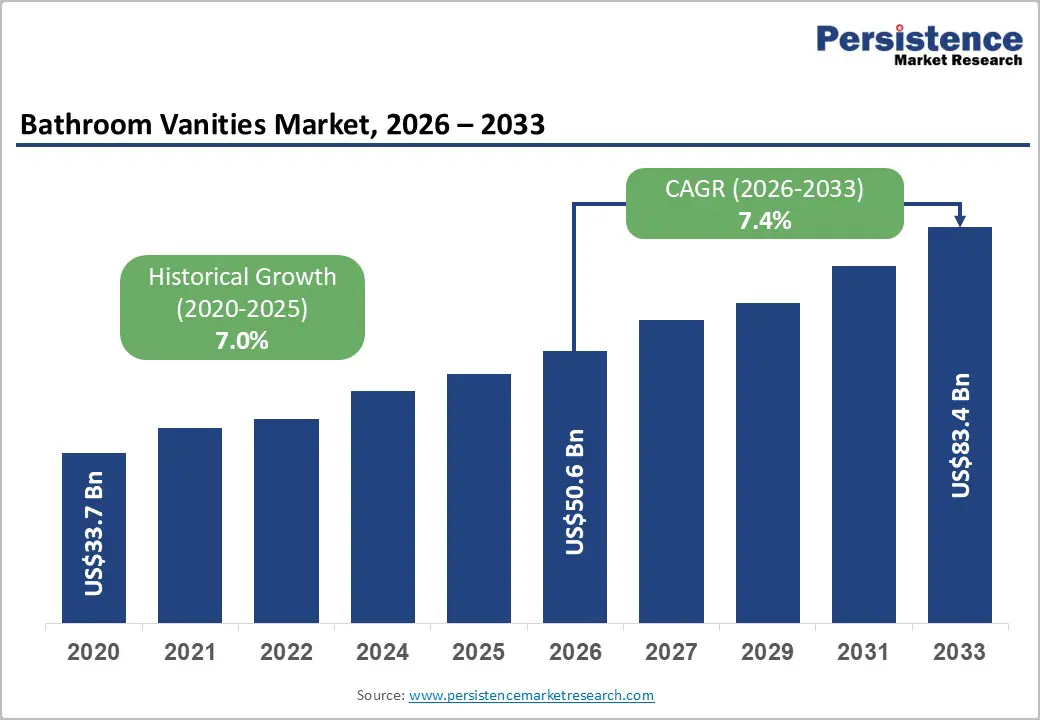

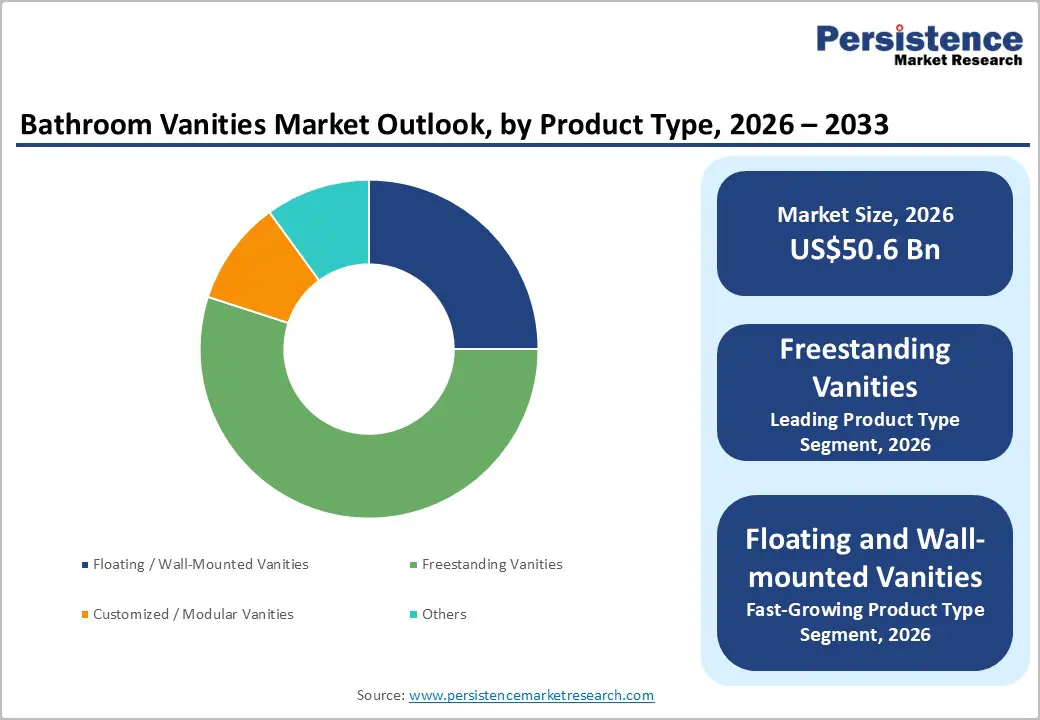

The global bathroom vanities market is projected to reach US$ 50.6 billion in 2026 and climb to US$ 83.4 billion by 2033, expanding at a CAGR of 7.4%.

Growth is strongly influenced by rising residential renovation spending, especially across the United States and Western Europe, where bathrooms are increasingly viewed as personal sanctuary spaces. According to Harvard University’s Joint Center for Housing Studies, home improvement expenditures touched US$ 485 billion in 2024, with bathroom remodels among the top priorities. Increasing home equity, demand for premium double-sink and custom cabinetry designs, and the integration of smart, IoT-enabled features are further elevating market value.

Key Industry highlights:

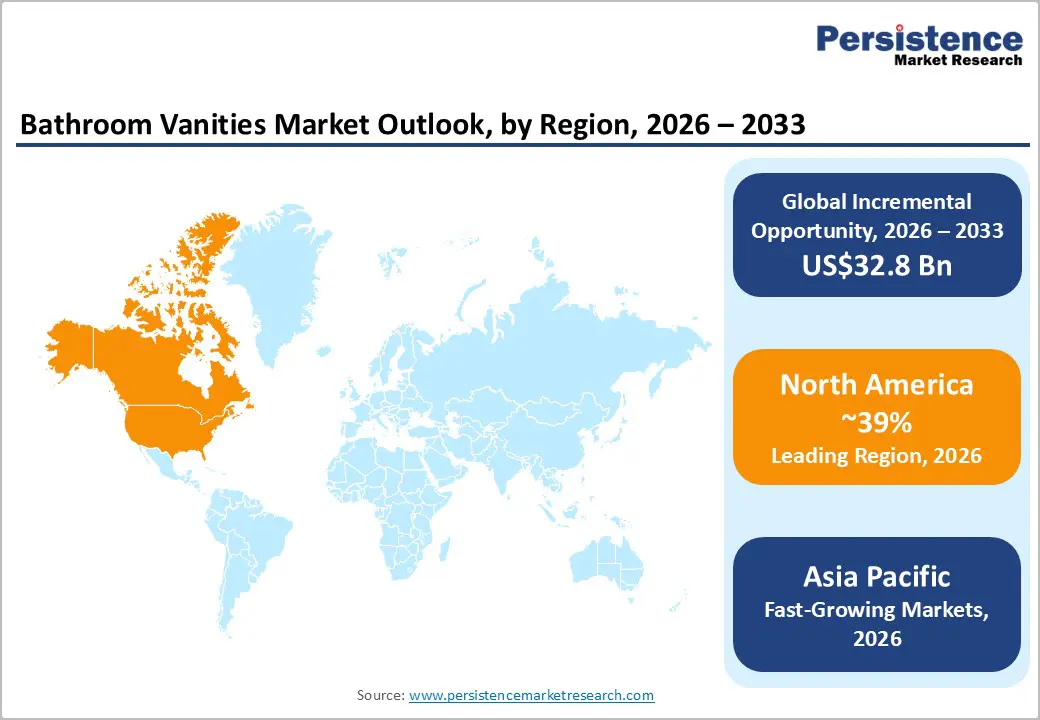

- Leading Region: North America holds 39% of global sales, driven by high renovation spending and large bathroom sizes that favor double-sink vanities.

- Fastest-Growing Region: Asia Pacific contributes roughly 33% of global demand, fueled by rapid urbanization, rising middle-class incomes, and increasing adoption of modular vanity solutions.

- Leading Category: Ceramic is the dominant material segment, projected to hold 42% market share in 2025 due to its durability, moisture resistance, hygiene benefits, and cost-effectiveness.

- Fastest-Growing Category: Floating and wall-mounted vanities are the fastest-growing product type, gaining popularity because of shrinking urban spaces and minimalist modern design trends.

- Key Market Opportunity: The aging global population presents a key opportunity, with rising demand for accessible, luxury vanities featuring seated access and adjustable counter heights.

| Key Insights | Details |

|---|---|

| Bathroom Vanities Market Size (2026E) | US$ 50.6 Billion |

| Market Value Forecast (2033F) | US$ 83.4 Billion |

| Projected Growth CAGR(2026 - 2033) | 7.4% |

| Historical Market Growth (2020 - 2025) | 7.0% |

Market Dynamics

Drivers - Surging Global Expenditure on Residential Renovation and Bathroom Remodeling

A powerful catalyst for bathroom vanities demand is the rapid rise in global spending on home improvement, particularly in mature housing markets. Aging housing stock, higher homeowner equity, and lifestyle upgrades are converging to push bathrooms to the top of renovation priority lists, where consumers increasingly pursue larger layouts, storage-rich cabinetry, and furniture-grade aesthetics. This shift is evident across both new builds and remodeling projects.

As budgets expand, buyers are trading up to double-sink configurations, quartz or stone tops, and custom organization systems that elevate perceived home value. In markets such as the U.S. and Western Europe, the bathroom is being reimagined as a calming retreat, translating into higher average unit prices and sustained revenue momentum for premium vanity manufacturers and encouraging longer-term brand loyalty among design-conscious homeowners.

Accelerating Shift Toward Sustainable, Low-Impact Materials and Eco-Certified Designs

Sustainability has moved from trend to expectation, reshaping how vanities are specified, sourced, and marketed. Consumers increasingly favor natural textures, biophilic tones, and responsibly harvested woods, while seeking assurance through certifications such as FSC. Designers and retailers report growing demand for low-VOC finishes and recycled inputs, reflecting stricter regulations and a broader cultural shift toward healthier homes. This momentum spans residential and hospitality projects.

Manufacturers are responding with engineered stone containing recycled glass, porcelain composites, and durable surfaces that lower lifetime environmental impact. Natural species such as white oak are rising in popularity, offering warm aesthetics while supporting sustainability stories. These innovations reduce material waste while enabling brands to command premium price points and win loyalty among Millennial and Gen Z buyers seeking authenticity and value.

Restraints - Acute Global Shortage of Skilled Tradespeople Slowing Installations and Delaying Market Realization

A tightening labor pool across plumbing, carpentry, and renovation services is emerging as one of the most structural constraints for the bathroom vanities market. With contractor deficits widening and job backlogs increasing, installation lead times are stretching, disrupting renovation timelines and dampening consumer enthusiasm for complex, custom-built vanity systems that require coordinated professional work.

Longer wait times translate into deferred purchases, canceled orders, and higher inventory burdens for manufacturers and retailers. Faced with rising labor costs and difficulty securing qualified tradespeople, many homeowners pivot toward simpler, modular, or DIY alternatives instead of premium multi-component vanities. This not only suppresses revenue in higher-value segments but also erodes upgrade opportunities across complementary categories such as countertops, sinks, and storage accessories.

Elevated Interest Rates Depressing Housing Turnover and Delaying Big-Ticket Renovation Decisions

Higher-for-longer interest rates are restraining bathroom vanity demand by slowing housing transactions and constraining household financing capacity. With mortgage rates hovering well above pandemic-era lows, homeowners remain “locked in,” dramatically reducing existing home sales, historically one of the strongest triggers for bathroom renovation and premium vanity purchases immediately after move-in.

At the same time, costlier borrowing is discouraging the use of HELOCs and personal loans for remodeling budgets that often exceed US$15,000. As financing becomes more expensive, households increasingly postpone upgrades, scale back design ambitions, or opt to refinish existing cabinetry instead of replacing it. This value-engineering trend disproportionately pressures mid- to premium price tiers, narrowing margins and slowing overall market growth despite underlying demand.

Opportunities - Rising “Silver Economy” Creating Strong Demand for Aging-in-Place, Accessible Luxury Vanity Designs

An aging global population is driving demand for bathroom solutions that strike a balance between accessibility and high-end aesthetics. As more seniors choose to remain in their homes longer, vanities designed with universal design principles, including variable-height counters, open knee-space cabinetry, and ergonomically positioned storage, are gaining traction. These products reduce mobility barriers while maintaining seamless integration with modern bath décor.

Manufacturers capable of aligning ADA-inspired features with premium styling can differentiate strongly in remodeling-driven segments. Floating vanities, integrated stability supports, and easy-reach hardware provide safety without the institutional look of traditional assisted-living fixtures. As aging-in-place becomes a mainstream renovation priority, brands that combine performance, dignity, and style stand to secure recurring demand from homeowners preparing for long-term living comfort.

Smart, Connected, and IoT-Enabled Vanities Unlocking Premium Innovation Opportunities

The digitalization of the bathroom presents a compelling pathway for new revenue streams and product differentiation. While smart faucets and toilets are evolving quickly, the vanity remains an underutilized technology platform capable of housing integrated lighting controls, charging ports, health-monitoring interfaces, and antimicrobial UV-C systems. These features transform vanities from passive storage furniture into intelligent, wellness-oriented command centers.

Concepts such as refrigerated skincare drawers, voice-activated lighting scenes, water usage analytics, and smart mirrors enhance functionality while elevating perceived value. Early consumer response to connected bathroom devices signals readiness for tech-forward vanity ecosystems. Brands that embed discreet, intuitive technology particularly in luxury North American markets and tech-oriented Asia Pacific regions can capture higher margins, build ecosystem loyalty, and future-proof their product portfolios

Category-wise Analysis

Product Type Insights

Freestanding vanities continue to dominate product demand, accounting for roughly 55% of global installations, supported by easier placement, lower installation complexity, and broad price availability. Their compatibility with both builder-grade and mid-range projects keeps volumes high, while widespread retail availability through home-improvement chains sustains recurring replacement demand across renovation cycles and entry-level residential projects.

By contrast, floating / wall-mounted vanities represent the fastest-growing segment, expanding at the highest CAGR as urban living spaces shrink and contemporary styling preferences accelerate. Their visual lightness, improved floor access, and compatibility with modular storage systems make them especially attractive for premium remodels and compact apartments, helping brands reposition toward sleeker, design-driven bathroom environments.

Material Insights

Ceramic remains the leading material choice for vanity tops and integrated sink systems, securing an estimated ~42% share in 2025. Its moisture resistance, durability, and non-porous hygiene profile make it ideal for humid bathroom environments, while continued reductions in production costs reinforce ceramic’s value proposition across both mass-market and mid-priced consumer segments globally.

The fastest-growing material category comprises engineered surfaces such as solid surface and engineered stone, advancing at the highest CAGR as homeowners seek thinner profiles, seamless edges, and customizable colors. These materials balance design flexibility with resilience, enabling sleeker Modernist aesthetics while supporting premium pricing and improved brand differentiation in renovation-driven markets.

Application Insights

The Residential segment clearly leads the market, contributing over 80% of total revenue as existing home renovations and new construction projects continue to drive recurring demand. Master bathrooms account for the highest per-unit spending, with double-sink configurations, premium storage, and upgraded tops increasingly replacing basic builder-grade cabinetry in upgrade cycles.

The fastest-growing application area is the commercial segment, advancing at the highest CAGR as hotels, senior-living communities, clinics, and office renovations emphasize durability, hygiene, and coordinated design. Standardized modular vanities, moisture-resistant materials, and service-friendly layouts are helping suppliers capture specification-driven opportunities across hospitality and institutional refurbishment programs.

Distribution Channel Insights

Offline retail retains market leadership, representing about 70% of global bathroom vanity sales. Showrooms, specialty kitchen-and-bath dealers, and big-box improvement stores give buyers the ability to evaluate finishes, drawer mechanisms, and countertop textures in person while also providing design consultation, delivery coordination, and installation services for complex remodel purchases.

However, the fastest-growing channel is online/e-commerce, posting the highest CAGR as consumers increasingly research, compare, and customize purchases digitally. Improved visualization tools, curated logistics, sample programs, and hassle-reduced return policies are enabling shoppers to shift more mid-priced and modular vanity purchases to digital platforms, expanding reach beyond traditional geographic dealer networks.

Regional Insights

North America Bathroom Vanities Market Trends

North America remains the revenue leader in the bathroom vanities market, accounting for around 39% of global sales. Higher disposable incomes, strong homeowner equity, and a mature renovation culture continue to support premium upgrades. U.S. consumers show a strong bias toward Transitional styling shaker fronts, neutral palettes, and natural wood tones while resale-driven remodeling encourages investment in high-quality cabinetry that elevates perceived property value.

The region is also an innovation hub for connected bathroom concepts. Vendors such as Kohler and Moen are integrating power outlets, lighting controls, and tech-ready storage into vanity designs. With design centers, showrooms, and pro-contractor ecosystems well established, North America is expected to maintain leadership across mid- to premium price tiers.

Europe Bathroom Vanities Market Trends

Europe’s bathroom vanities market is driven by sustainability mandates, compact urban layouts, and precision engineering, with growth anchored by strict environmental regulations. Manufacturers are prioritizing FSC-certified wood, recycled composites, and low-VOC finishes to align with EU directives, while minimalist, space-efficient aesthetics remain dominant in Germany, the U.K., and Scandinavia. Wall-mounted systems are especially popular, offering both visual lightness and practical space optimization.

The market is projected to grow at a CAGR of about 7.8%, supported by renovation incentives, circular-economy programs, and innovation in modular, repairable designs. Handle-less fronts, matte finishes, and slim silhouettes reflect a shift toward understated luxury, while leading brands such as Duravit and Villeroy & Boch continue to shape specification-driven residential and hospitality projects across the region.

Asia Pacific Bathroom Vanities Market Trends

Asia Pacific represents the fastest-expanding regional market, now contributing roughly 33% of global bathroom vanity demand. Rapid urbanization in China, India, and Southeast Asia is accelerating apartment living, pushing demand for compact, storage-efficient, modular designs. Rising middle-class incomes are also encouraging a shift from carpenter-built furniture to branded, factory-finished systems with better durability and warranties.

Technology-forward preferences further distinguish the region. In Japan and parts of China, integration with smart mirrors, hygienic features, and coordinated sanitary ware ecosystems (from players such as TOTO and LIXIL) is gaining traction. Meanwhile, India is experiencing premiumization, with consumers upgrading from basic fixtures to contemporary vanities positioned as lifestyle enhancements supporting sustained growth across organized retail and project-based channels.

Competitive Landscape

The global bathroom vanities market is fragmented, blending global sanitary-ware brands with numerous regional specialists focused solely on furniture. Larger players leverage design capabilities, distribution reach, and brand equity, while regional manufacturers compete on customization, craftsmanship, and faster response to local style preferences.

Competition is intensifying as leaders pursue “complete bathroom solution” strategies, adding coordinated vanities to broader product portfolios to capture higher ticket value and simplify buying for developers and homeowners. Meanwhile, niche manufacturers differentiate through modular designs, flexible sizing, premium finishes, and direct-to-consumer channels, creating a dynamic competitive environment across both premium and mid-market price tiers.

Key Market Developments:

- In January 2025, Kohler debuted its "Formation 02" smart toilet and accompanying vanity suite, featuring brutalist design angles and integrated smart lighting, signaling a move toward "art-piece" bathroom furniture.

- In September 2023, Moen launched the "5-Series eToilet" and a compatible smart vanity console designed to conceal plumbing for electronic bidets, directly addressing the installation challenges of smart bathroom fixtures.

- In March 2023, Roca introduced the "In-Wash Insignia" collection, which includes a modular vanity system specifically engineered to integrate with their new smart toilet lines, emphasizing seamless connectivity and hygiene.

Companies Covered in Bathroom Vanities Market

- Kohler Co.

- TOTO Ltd.

- Duravit AG

- Villeroy & Boch AG

- American Standard (LIXIL)

- Roca Sanitario S.A.

- JOMOO Group

- OPPEIN Home Group

- James Martin Vanities

- Wyndham Collection

- Virtu USA

- KingKonree (KKR)

- Jaquar Group

- Moen / House of Rohl

- IKEA

Frequently Asked Questions

The global bathroom vanities market is projected to reach a value of US$ 83.4 Billion by 2033, growing from US$ 50.6 Billion in 2026.

Key demand drivers include a record surge in home renovation spending, the trend of transforming bathrooms into wellness sanctuaries, and the rising popularity of eco-friendly materials like reclaimed wood.

Ceramic is the leading material segment, holding around 42% market share due to its durability, moisture resistance, and widespread use in integrated vanity tops and basins.

North America is the leading region, accounting for 39% of global sales, driven by high disposable incomes, a strong real estate resale market, and a preference for spacious, double-sink master bathrooms.

A major opportunity lies in the "Silver Economy" and "Aging-in-Place" trends, where there is growing demand for accessible yet stylish vanities designed for older adults, as well as the integration of smart IoT technology into vanity units.

Prominent market players include Kohler Co., TOTO Ltd., Duravit AG, LIXIL (American Standard), Roca Sanitario S.A., and furniture-focused brands like James Martin Vanities and Wyndham Collection.