- Display Technologies

- LED Lighting Solutions Market

LED Lighting Solutions Market Size, Share, and Growth Forecast 2026 - 2033

LED Lighting Solutions Market by Product Type (LED Bulbs, Bare LED Tubes, LED Luminaire, LED Down Lights, Others), Services (Consulting Services, Installation Services, Maintenance & Support Services), Application (Indoor LED Lighting, Outdoor LED Lighting, LED Backlighting, Automotive LED Lighting, Others), End-user (Residential, Commercial, Industrial), Regional Analysis, 2026 - 2033

LED Lighting Solutions Market Size and Trend Analysis

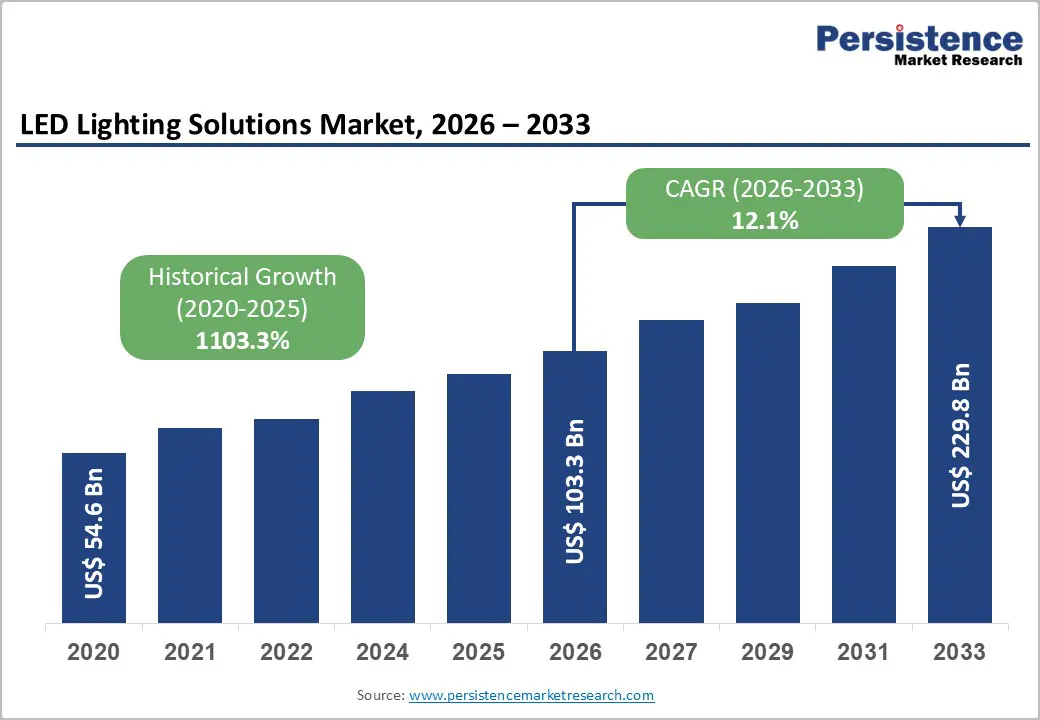

The global LED lighting solutions market is projected to reach US$ 103.3 billion in 2026, expanding to US$ 229.8 billion by 2033 at a CAGR of 12.1%.

Market growth is primarily driven by stringent energy efficiency regulations and significant reductions in LED manufacturing costs, with prices declining over 80% in the past decade. Policies in regions such as the European Union and North America phasing out inefficient lighting technologies, are accelerating adoption across residential, commercial, and industrial sectors. Furthermore, rapid urbanization and smart city initiatives, particularly in the Asia Pacific, are fueling infrastructure investments in intelligent lighting systems, boosting market expansion.

Key Market Highlights

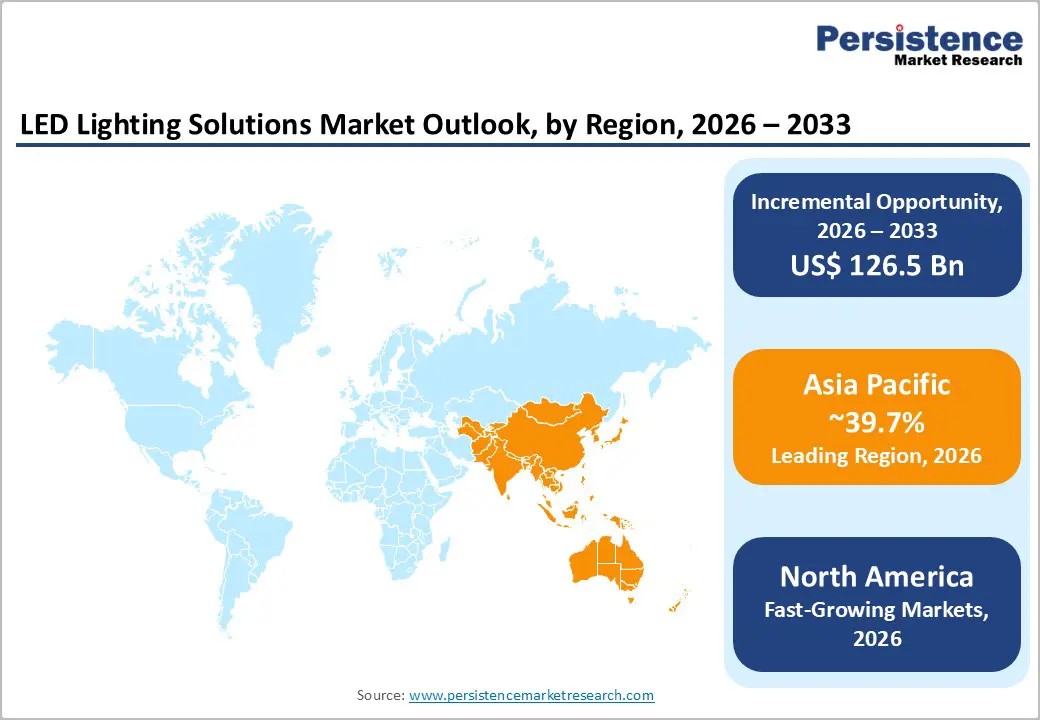

- Leading Region: Asia Pacific leads the global LED lighting market with 39.7% share, driven by rapid urbanization, large-scale infrastructure development, and strong government-led energy-efficiency initiatives.

- Fastest Growing Region: India emerges as the fastest-growing LED market at 14.50% CAGR, supported by national programs such as UJALA and SLNP that have deployed hundreds of millions of energy-efficient LED units.

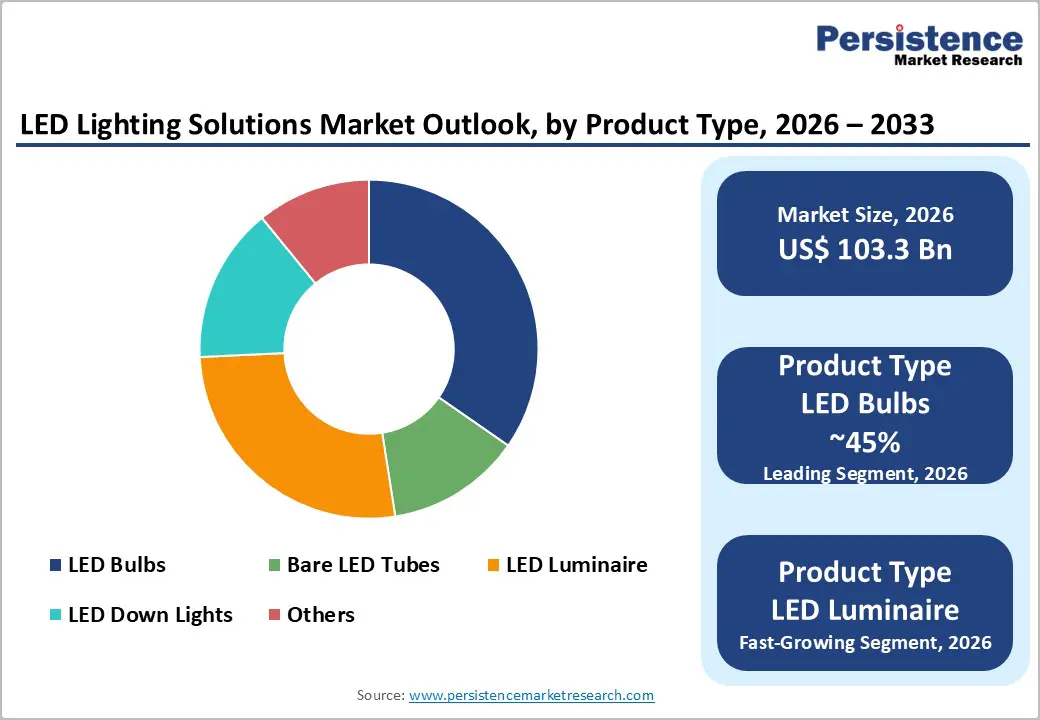

- Dominant Product Segment: LED Bulbs and Lamps hold around 45% share, driven by affordability, compatibility with existing fixtures, and widespread residential adoption supported by quick payback benefits.

- Fastest Growing Application: Smart LED Lighting Systems grow at 22.14% CAGR, propelled by smart city development, IoT integration, and rising consumer demand for connected and adaptive lighting.

- Key Market Opportunity: Automotive LED lighting presents significant growth potential, supported by global EV expansion and regulatory moves mandating energy-efficient, safety-enhancing LED headlight technologies.

| Key Insights | Details |

|---|---|

| LED Lighting Solutions Market Size (2026E) | US$ 103.3 Billion |

| Market Value Forecast (2033F) | US$ 229.8 Billion |

| Projected Growth CAGR (2026 - 2033) | 12.1% |

| Historical Market Growth (2020 - 2025) | 11.2% |

Market Dynamics

Drivers - Accelerating Global LED Adoption Through Stringent Energy Efficiency Mandates and Regulatory Frameworks

Strict energy efficiency regulations in both developed and emerging markets serve as a major catalyst for LED adoption. Policies like the European Union’s Ecodesign Directive and the U.S. Energy Star Program enforce minimum performance standards, phasing out inefficient incandescent and halogen lighting technologies. These regulations drive a structural shift in consumer preference toward LED lighting.

Government incentives such as rebates, tax credits, and dedicated retrofit programs further reinforce adoption. For example, Germany allocated around €3 billion under its “Building Energy Efficiency Program” to encourage LED retrofits. Research shows LED adoption in developed markets surged from 8% in 2015 to 48% in 2020, highlighting the transformative impact of regulatory interventions on market demand.

Sustained Market Growth Driven by Declining LED Manufacturing Costs and Extended Product Lifespan Advantages

The exponential reduction in LED component costs, coupled with superior longevity The rapid decline in LED manufacturing costs, combined with superior longevity, continues to fuel market expansion across residential, commercial, and industrial segments. Prices of LED bulbs dropped from approximately US$ 45-50 per unit in 2011 to under US$ 10 by 2018, reflecting technological advancements, enhanced production capacities, and operational scale economies.

Beyond cost reductions, LEDs offer substantial energy savings, consuming 75% less power than incandescent bulbs while providing up to 50,000 hours of operational life. Minimal heat emission and reduced maintenance requirements create strong economic incentives, delivering quick ROI for businesses and consumers alike. These factors ensure that LED adoption extends well beyond regulatory compliance, making it a strategic choice for efficiency and cost savings.

Restraints - Thermal Management Challenges Limiting LED Adoption in High-Temperature Industrial Applications

Despite their efficiency, LEDs generate substantial heat, with around 55% of energy in high-power applications converted to thermal energy. Elevated temperatures can degrade performance, causing reduced brightness, color shifts, and shorter operational lifespan, particularly in industrial environments like foundries, power plants, and heavy manufacturing zones.

Addressing these issues requires advanced thermal management solutions, including sophisticated heat sinks and thermal interface materials. While effective, these designs increase product complexity and manufacturing costs, creating capital-intensive barriers for businesses weighing LED upgrades against traditional lighting systems.

Smart Lighting Integration Complexity Coupled with Cybersecurity and Interoperability Concerns

The adoption of IoT-enabled smart LED lighting faces technical and security challenges that slow deployment, especially in commercial and industrial settings. Effective integration demands compatible hardware, wireless protocols, cloud connectivity, and robust cybersecurity frameworks to prevent unauthorized access and data breaches.

Small and medium-sized enterprises encounter additional hurdles due to limited technical expertise, integration complexity with existing building management systems, and privacy concerns tied to energy monitoring and occupancy tracking. Furthermore, interoperability issues among competing smart lighting platforms restrict market penetration, particularly for cost-sensitive users seeking simple, plug-and-play solutions.

Opportunity - Expanding Market Potential Through Smart City Infrastructure Development and IoT-Enabled LED Systems

Rapid urbanization and smart city initiatives worldwide are creating significant opportunities for connected LED lighting integrated with IoT ecosystems. Municipalities are replacing conventional high-pressure sodium streetlights with adaptive LED systems that adjust brightness in real time based on traffic, weather, and ambient light conditions.

These intelligent systems reduce energy consumption by up to 70%, improve public safety, and enable data collection for traffic and environmental management. Programs such as India’s Smart Cities Mission and China’s Green Building Action Plan are retrofitting millions of streetlights and new commercial buildings, generating substantial demand for lighting manufacturers and system integrators throughout the forecast period.

Accelerating Growth Opportunities in Automotive LED Lighting Driven by Electric Vehicle Adoption

The automotive sector presents high-growth potential for LED technologies, fueled by the rise of electric vehicles, safety regulations, and consumer demand for premium lighting. In 2023, LEDs captured 46.4% of automotive lighting revenue, reflecting widespread adoption in headlights, tail lights, and interior illumination systems across vehicle segments.

EV manufacturers favor LEDs for low energy consumption, optimizing battery range and vehicle efficiency. Advanced solutions like ams OSRAM’s EVIYOS microLED adaptive headlights enhance safety by dynamically adjusting beam patterns. Regulatory mandates in the U.S. and Europe, along with aftermarket LED conversion markets, further expand addressable opportunities, making automotive lighting a critical growth driver for manufacturers.

Category-wise Analysis

Product Type Insights

LED Bulbs and Lamps dominate the global LED lighting market with approximately 45% share, driven by affordability, ease of installation, and compatibility with existing fixtures. This segment leads across residential, commercial, and industrial applications, as bulbs require minimal infrastructure modification compared to luminaire replacements. Programs like India’s UJALA scheme, distributing over 370 million LED bulbs, underscore adoption potential in emerging economies and the scale of market penetration.

Emerging luminaire replacements and advanced LED panels represent the fastest-growing sub-segment, fueled by improved energy efficiency, smart compatibility, and enhanced design flexibility. Technological innovations in A-type lamps, along with government subsidies and rebate programs, continue to accelerate demand, particularly in price-sensitive residential and commercial spaces where quick payback periods and performance improvements justify investment.

Services Insights

Installation and Maintenance Services account for the largest portion of services revenue, approximately 38%, as commercial and industrial customers outsource lighting deployment and support. Professional installation ensures compliance with building codes, optimal fixture positioning, and integration with electrical systems, reducing implementation risk for complex projects. Recurring maintenance contracts further support long-term reliability, performance monitoring, and emergency repair for extensive lighting networks.

The fastest-growing service segment is professional support for smart and IoT-enabled lighting systems. As smart controls and connected lighting adoption rise, demand for specialized technical expertise, system integration, diagnostics, and lighting-as-a-service models is expanding. Commercial property managers increasingly prefer these services as cost-effective alternatives to capital-intensive equipment purchases, enhancing market potential across industrial and commercial real estate portfolios.

Application Insights

Indoor LED Lighting Applications lead the market with roughly 65% share, spanning residential, commercial offices, retail outlets, and institutions. Indoor LED adoption is driven by energy savings, reduced electricity costs, and superior lighting quality. Commercial facilities consume significant electricity for lighting operations, making retrofits highly attractive. Residential spaces benefit from flicker-free performance and compatibility with smart home automation ecosystems, encouraging widespread deployment.

The fastest-growing application segment includes advanced human-centric and tunable-white LED systems. Commercial and institutional customers increasingly invest in circadian-aligned lighting and occupancy-sensing solutions to enhance productivity, visual comfort, and well-being. Integration with smart controls and automation platforms supports premium pricing and growing adoption, particularly in office environments, educational institutions, and retail spaces seeking high-quality, energy-efficient illumination solutions.

End-user Insights

Commercial applications hold the highest market share at approximately 52%, supported by high energy consumption, regulatory compliance, and rapid adoption of smart lighting controls in offices, retail, and hospitality sectors. Continuous operation during extended hours allows end-users to realize immediate savings on electricity and maintenance. Industrial and manufacturing sectors also adopt LEDs to enhance safety, productivity, and sustainability performance, while institutions benefit from procurement mandates and rebate programs.

The fastest-growing end-user segment is institutional and public sector facilities investing in advanced LED solutions. Schools, universities, and government buildings increasingly implement smart lighting systems to optimize energy efficiency and occupant comfort. Rising emphasis on sustainable infrastructure, coupled with available rebates and budget incentives, drives accelerated adoption of LED technologies in institutional environments, creating significant long-term market potential.

Regional Insights

North America LED Lighting Solutions Trends

North America holds around 30% of the global LED lighting market, supported by strong federal energy-efficiency regulations, extensive utility rebate programs, and vast retrofit potential across aging commercial and residential infrastructure. The U.S. leads adoption through ENERGY STAR standards and state-level mandates that accelerate LED integration across homes, offices, and municipal facilities. Retrofit installations dominate regional volumes, driven by cost savings and simplified upgrade requirements.

Innovation ecosystems across the U.S. and Canada continue to advance lighting controls, occupancy sensors, and smart home integration, strengthening the region’s competitive position. Expanding smart city investments further boost demand for adaptive LED streetlighting systems, reducing municipal energy consumption while improving public safety. Updated load calculations under the 2026 National Electrical Code additionally ease residential retrofit feasibility by eliminating costly electrical panel upgrades.

Europe LED Lighting Solutions Trends

Europe’s LED lighting market is projected to grow at a 15.5% CAGR through 2033, driven by stringent EU-wide regulatory alignment and rapid phase-out of inefficient lighting technologies. The Ecodesign for Sustainable Products Regulation (ESPR) enforces strict minimum performance standards while prohibiting destruction of unsold non-compliant inventory after 2026, intensifying industry-wide transition pressures. Germany, France, and the U.K. lead adoption through advanced manufacturing capabilities and energy-transition programs.

Retrofitting constitutes a substantial share of European LED deployment, supported by aging building stock and aggressive sunset dates for legacy technologies, particularly in Nordic countries. National recovery and sustainability initiatives across Italy and other EU member states allocate billions for LED upgrades in public infrastructure, creating robust procurement opportunities. Suppliers with advanced distribution networks and turnkey installation services benefit most from these accelerated replacement cycles.

Asia Pacific LED Lighting Solutions Trends

Asia Pacific represents the largest regional market with 39.7% share, driven by rapid urbanization, large-scale infrastructure development, and strong government energy-efficiency mandates across China, India, and Japan. China remains the regional powerhouse, supported by extensive manufacturing clusters such as Guangdong, which hosts over 10,000 LED-related enterprises. Continued technological advancement and cost reductions enable widespread adoption across residential, commercial, and industrial settings.

India and Japan further accelerate regional growth through national LED deployment programs and smart city initiatives. India’s UJALA and SLNP programs have installed millions of LED streetlights, producing significant energy savings and emissions reductions. Japan’s focus on sustainability and urban digitalization supports the rapid uptake of IoT-enabled lighting systems, while phased fluorescent lamp bans create significant replacement opportunities throughout the Asia Pacific.

Competitive Landscape

The global LED lighting market remains moderately fragmented, with the top tier of manufacturers accounting for roughly 35-40% of the overall share. This structure leaves substantial room for mid-tier and regional players to compete through geographic specialization, cost efficiency, and application-specific product portfolios. Leading participants differentiate through integrated value chains spanning components, fixtures, software platforms, and service capabilities, enabling comprehensive ecosystem offerings and premium positioning.

Competitive strategies increasingly emphasize vertical integration, strategic partnerships, and technology-led product innovation. Advanced optical designs, human-centric lighting features, IoT-enabled controls, and superior thermal management systems serve as key differentiators. Meanwhile, manufacturers from emerging Asian economies continue to intensify price competition and accelerate market expansion through high-volume production and localized product customization.

Key Market Developments

- In March 2025, Signify announced a joint venture with Dixon Technologies (India) Limited to manufacture LED bulbs, downlights, spotlights, and lighting accessories tailored to competitive Indian market requirements, demonstrating a commitment to localized production and market expansion within Asia's fastest-growing LED markets.

- In August 2025, Acuity Brands Lighting announced that nine innovative LED solutions received selection for the 2025 Illuminating Engineering Society (IES) Progress Report, including advanced high-bay luminaires featuring 186 lumens-per-watt efficiency and patent-pending optical technologies, reflecting ongoing innovation in industrial and commercial lighting applications.

- In August 2025, Samsung Electronics introduced the world's first Micro RGB display featuring sub-100-micrometer individually controlled red, green, and blue microLED arrays for ultra-premium television displays, establishing new benchmarks for color accuracy and contrast ratios while demonstrating technological innovation in advanced display backlighting applications.

Companies Covered in LED Lighting Solutions Market

- Signify N.V.

- ams OSRAM AG

- Cree Lighting

- Samsung Electronics

- Acuity Brands Inc.

- Toshiba Lighting & Technology Corporation

- Eaton Corporation

- GE Lighting

- Havells India Limited

- Hubbell Lighting Inc.

- Seoul Semiconductor Co. Ltd.

- Everlight Electronics Co. Ltd.

- Sharp Corporation

- Zumtobel Group AG

- LG Electronics

- Nichia Corporation

- Crompton Greaves Consumer Electricals Limited

- Syska LED Lights Pvt. Ltd.

Frequently Asked Questions

The global LED lighting solutions market is expected to reach US$ 229.8 Billion by 2033, growing from US$ 103.3 Billion in 2026 at a 12.1% CAGR.

Growth is driven by stringent efficiency regulations, over 80% decline in LED costs, 75% energy savings, and 50,000-hour lifespan advantages.

LED Bulbs and Lamps lead with ~45% share, supported by affordability, fixture compatibility, and simple residential replacement needs.

Asia Pacific dominates with 39.7% share, driven by urbanization, infrastructure development, and large-scale government LED deployment programs.

Smart LED Lighting Systems grow at 22.14% CAGR, supported by IoT integration, smart city projects, and demand for adaptive, connected lighting.

Market leaders include Signify N.V., ams OSRAM AG, Acuity Brands, Inc., Cree LED, Samsung Electronics, and Crompton Greaves Consumer Electricals.