- Home Care & Utilities

- Aquarium Water Treatment Market

Aquarium Water Treatment Market Size, Share, and Growth Forecast, 2026-2033

Aquarium Water Treatment Market by Product Type (Chemical Treatments, Biological Treatments, Mechanical Filtration, Chemical Filtration, UV Sterilization Systems, Others), Purpose (Remove Chlorine, Control Ammonia & Nitrates, Control Algae, Balance pH, Improve Water Clarity), End-User (Residential, Pet Stores, Public Aquariums, Commercial Spaces, Fish Farming Operators), and Regional Analysis for 2026-2033

Aquarium Water Treatment Market Share and Trends Analysis

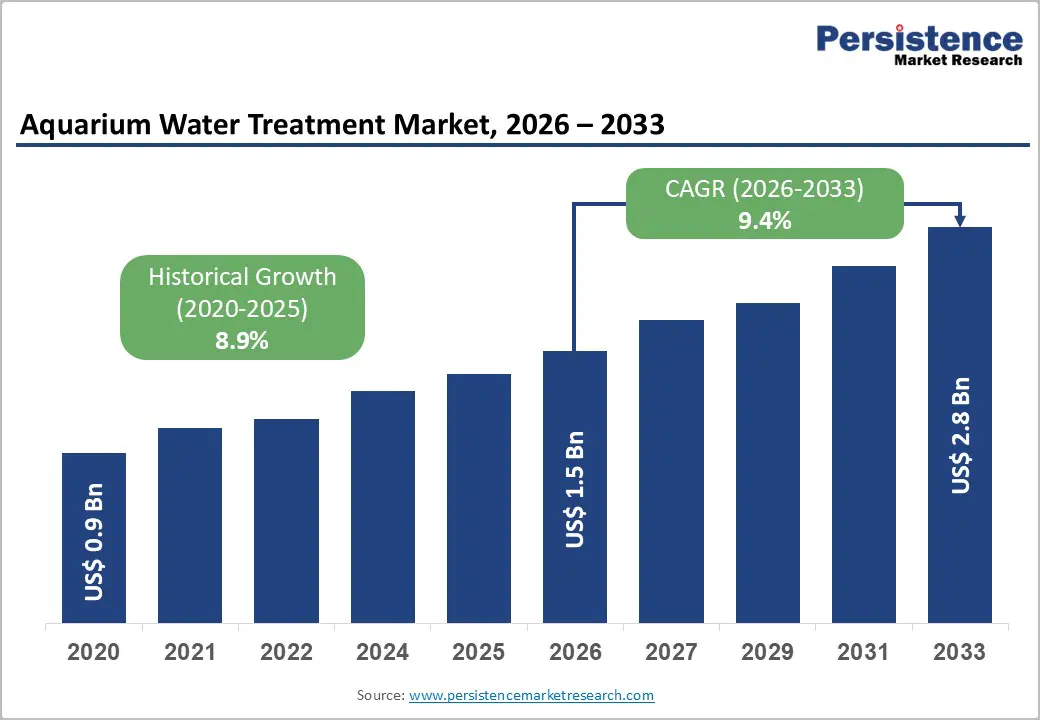

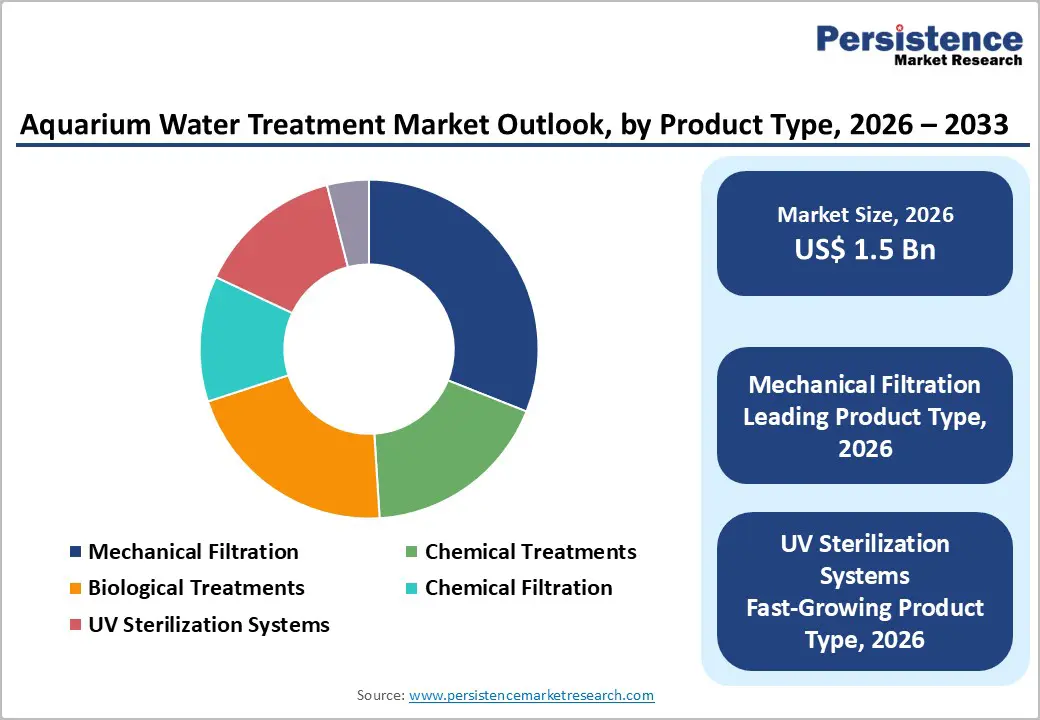

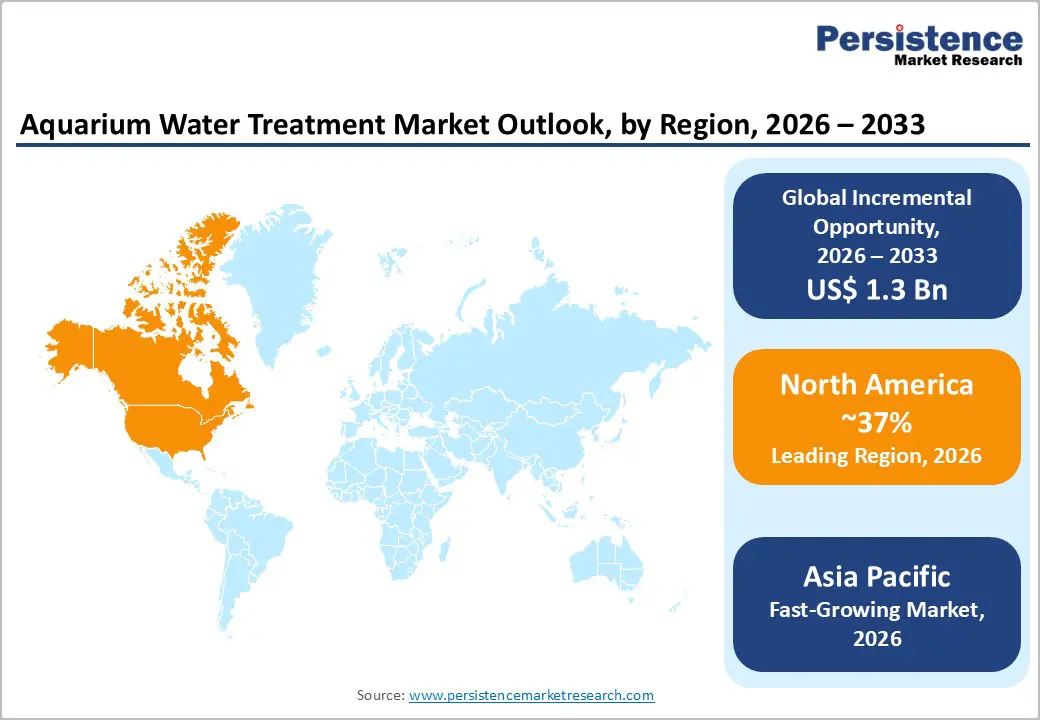

The global aquarium water treatment market size is likely to be valued at US$ 1.5 billion in 2026, and is projected to reach US$ 2.8 billion by 2033, growing at a CAGR of 9.4% during the forecast period 2026–2033.

The market is expanding steadily due to increasing pet ownership rates, rising investments in public aquariums and marine conservation infrastructure, and continuous technological advancements in aquarium filtration systems and UV sterilization technologies. Urbanization and changing lifestyle patterns have encouraged adoption of ornamental fish as low-maintenance companion pets, directly supporting recurring demand for aquarium water treatment solutions.

Public aquariums and marine parks are allocating higher budgets toward life support systems to ensure regulatory compliance and species preservation. Innovation in biological treatments, chemical water conditioners, and smart water monitoring systems is enhancing operational efficiency, improving aquatic health outcomes, and strengthening long-term revenue stability across residential, commercial, and aquaculture end users.

Key Industry Highlights

- Dominant Product Types: Mechanical systems are set to command around 31% revenue share in 2026, while UV sterilization systems are projected to grow the fastest at roughly 10.8% CAGR through 2033, driven by the advent of smart aquarium water treatment solutions.

- Leading Treatment Purpose: Ammonia and nitrate control solutions are expected to hold approximately 35% share in 2026, whereas algae control treatments are likely to expand at the fastest pace during 2026–2033, reflecting rising focus on water clarity and preventive care.

- Dominant End-Users: Residential users are anticipated to account for about 48% of market revenues in 2026, while fish farming operators are forecast to witness the highest 2026-2033 CAGR, supported by commercial aquaculture expansion.

- Regional Leadership: North America is projected to lead with nearly 37% share in 2026, whereas Asia Pacific is expected to record the strongest growth at around 10.9% CAGR through 2033, fueled by heavy investments in aquaculture development.

| Key Insights | Details |

|---|---|

| Aquarium Water Treatment Market Size (2026E) | US$ 1.5 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Pet Ownership and Institutional Investment in Aquatic Infrastructure

According to the American Pet Products Association (APPA), over 66% of U.S. households own a pet, with aquarium fish among the most widely kept indoor pets. The ornamental fish trade exceeds US$15 billion globally, according to the Food and Agriculture Organization (FAO). Urban lifestyles and smaller living spaces have bolstered demand for compact, low-maintenance pets, boosting demand for aquarium water conditioners, biological treatments, and filtration systems. This expanding base of hobbyists continues to create recurring revenue streams for products that maintain water quality and aquatic health. Increasing awareness of fish welfare and proper aquarium management has further encouraged consumers to invest in premium water treatment solutions and regular maintenance routines.

The regulatory attention around aquarium species harvesting has intensified, prompting proposed rule changes in Hawaii aimed at reopening reefs to commercial aquarium fish collection after an eight-year ban. The state’s Board of Land and Natural Resources has advanced a public hearing process on new aquarium fish harvesting rules, which could influence global ornamental fish availability and trade practices once finalized in early 2026. These developments highlight how evolving policy frameworks directly impact water treatment demand in both supply chains and pet care ecosystems. Enhanced sustainability and compliance initiatives by public aquariums and marine parks are also driving investments in high-performance filtration and water monitoring systems to meet both legal and ethical standards.

Technological Innovation and Smart Water Quality Management

The integration of advanced smart sensors and automated water quality monitoring systems is transforming how both hobbyists and professional aquarists maintain aquatic environments. IoT-enabled pH controllers, ammonia sensors, and real-time nitrate monitors allow continuous assessment of critical water parameters, significantly reducing manual effort and helping prevent disease outbreaks. Automated dose adjustments and digital alerts enhance precision and reduce risk, making these technologies increasingly central to modern aquarium water treatment solutions. The growing availability of connected devices and user-friendly apps has also facilitated broader adoption, enabling even small-scale aquarium owners to monitor and control water quality with ease.

Governments and innovators are also promoting real-time water quality surveillance in marine environments using IoT systems that monitor tens of parameters continuously, tailoring conditions to sustain specific aquatic ecosystems. Programs such as Japan’s initiative to deploy IoT devices for constant monitoring of artificial seawater conditions demonstrate broader institutional support for smart water management technologies. These advances not only strengthen water quality control but also position technology-driven solutions as essential for maintaining aquatic health in residential, commercial, and conservation applications. The resulting data-driven insights further empower operators to optimize filtration efficiency, reduce chemical dependency, and improve long-term sustainability outcomes.

High Equipment and Maintenance Costs

Advanced aquarium filtration systems and UV sterilizers require a significant upfront investment, which can account for 15–20% of total aquarium infrastructure costs for commercial-grade installations. Beyond initial procurement, recurring expenses for replacement media, UV bulbs, and chemical dosing solutions add to the total cost of ownership. This combination of capital and operational expenditure can discourage adoption, particularly among residential users and small-scale aquarium operators who are sensitive to upfront and ongoing costs. Many users also factor in electricity consumption, routine inspections, and occasional technical support, which cumulatively increase the operational budget.

Even in well-established markets, businesses face higher engineering and integration costs as regulators tighten safety and environmental requirements for water treatment infrastructure. For example, updated chemical safety standards for handling and storage of hazardous substances in India require manufacturers to enhance testing, documentation, and compliance processes by early 2026, which can prompt additional cost burdens across water treatment products. These financial barriers may moderate growth rates in price-driven segments and require manufacturers to explore cost-optimization, modular system designs, or bundled maintenance programs to make advanced solutions more accessible and attractive to a wider range of users.

Regulatory Restrictions on Chemical Treatments

Chemical additives used for algae control, ammonia reduction, and pH balancing are increasingly subject to scrutiny over environmental and human health impacts. The European Chemicals Agency (ECHA) added multiple hazardous substances to its Candidate List of Substances of Very High Concern in early 2025, requiring companies to manage risks, provide detailed safe-use information, or reformulate products to remain compliant. This regulatory tightening adds to compliance complexity and increases reformulation and testing costs for manufacturers supplying chemical water treatment solutions. Companies must also monitor supply chain chemicals to ensure that all inputs meet new regulatory thresholds, increasing operational oversight.

Major chemical regulatory frameworks are proposing broader restrictions on classes of persistent chemicals, such as per- and polyfluoroalkyl substances (PFAS), to minimize environmental emissions, pushing phased implementation timelines that affect a wide range of water-related chemical products. Such regulatory movements can delay product approvals and mandate extensive compliance reporting, potentially compressing short-term margins, as companies transition their portfolios towards safer formulations. These evolving requirements underscore the growing legislative emphasis on environmentally sound treatment chemicals while raising operational hurdles for existing products and emphasizing the need for sustainable innovation.

Expansion of Commercial Aquaculture and Fish Farming

Aquaculture contributes over 50% of the global fish supply for human consumption, creating a strong demand for industrial-grade aquarium water treatment solutions. Fish farming operators require large-scale systems capable of controlling ammonia, nitrates, and algae to maintain water quality and maximize yield. The adoption of mechanical and chemical filtration, combined with biological treatments, is increasingly critical for operational efficiency and disease prevention in high-density fish farms. Advanced monitoring enables operators to detect early signs of water-quality fluctuations, minimizing losses and improving overall farm profitability.

Recent developments support this growth opportunity; for instance, in 2025, Vietnam piloted IoT-based water-quality monitoring systems in fish ponds, enabling real-time tracking of water conditions and supporting better aquaculture management. Similarly, India’s government launched a national digital traceability system for fisheries and aquaculture to improve export compliance, safety, and operational efficiency. These initiatives demonstrate policy-level support for smart, technology-driven water management, creating a scalable market for automated nitrate control and algae management systems across Asia Pacific and other high-density aquaculture hubs. Adoption of these systems also reduces manual labor and operational errors, reinforcing long-term demand growth.

Growing Demand for Eco-Friendly and Biological Treatments

Consumer awareness regarding sustainability is driving strong interest in eco-friendly aquarium treatments that reduce chemical dependency. Natural bacterial cultures for ammonia control, nitrate reduction, and algae management are gaining traction in premium residential and commercial markets. These solutions are perceived as safer for aquatic life and the environment, aligning with evolving environmental policies and regulatory standards. Increasingly, hobbyists and commercial operators are prioritizing long-term ecological sustainability alongside operational efficiency, encouraging manufacturers to expand their eco-friendly product portfolios.

In 2025, aquaculture innovation competitions highlighted smart water-quality monitoring systems and energy-efficient, eco-friendly treatment solutions. Notable examples include Ghana’s Aquamet system, recognized for its precision water quality monitoring and sustainability impact. In addition, industry forums and conferences, such as World Aquaculture Singapore 2026, are driving the adoption of digital and sustainable solutions across both commercial and residential aquaculture. This growing emphasis on eco-friendly and data-driven solutions positions biological and sustainable treatments as high-value offerings with strong adoption potential in emerging urban markets across India, Southeast Asia, and Latin America. Widening distribution through organized retail and e-commerce further accelerates accessibility and market penetration.

Category-wise Analysis

Product Type Insights

Mechanical filtration systems are projected to hold approximately 31% of the aquarium water treatment market revenue share in 2026, reflecting their essential role in removing particulate waste and maintaining water clarity in both hobbyist and commercial environments. Public aquariums and commercial aquaculture facilities prioritize multi-stage filtration for reliable particulate removal and reduced maintenance downtime, while home aquarium hobbyists adopt advanced filter canisters and cartridges to support biological balance. Filtration’s compatibility with biological media and UV systems, combined with innovations in compact, low-maintenance designs and smart monitoring integration, reinforces its leadership and broad adoption across residential and commercial applications.

UV sterilization systems are expected to grow at the fastest pace during the 2026-2033 forecast period, with an estimated 10.8% CAGR, driven by their pathogen-control efficiency and reduced chemical dependency. Adoption is rising among hobbyists, retail aquariums, and commercial aquaculture operations seeking sustainable solutions. In 2026, for example, IceCap In-Sump UV sterilizers were restocked and widely deployed, demonstrating renewed market interest in easy-to-install systems compatible with sump setups, thereby improving water clarity and biosecurity. Integration with smart monitoring and automated intensity controls further enhances usability. Reduced chemical reliance, energy efficiency, and regulatory compliance support UV sterilizers as a key growth driver in both residential and commercial segments.

End-User Insights

Residential aquariums are projected to account for about 48% market revenue share in 2026, driven by the global popularity of home aquariums and recurring demand for water conditioners, pH balancers, and filtration modules. Hobbyists increasingly adopt smart monitoring systems to simplify maintenance and ensure consistent water quality. In 2025, the market saw expanded availability of smart, energy-efficient home aquarium filters, enhancing accessibility and usability for urban consumers. Modular, low-maintenance, and aesthetically integrated systems further reinforce adoption, supporting a stable revenue base and long-term growth for residential-focused products.

Fish farming operators are expected to experience the fastest growth, with a 2026-2033 CAGR of 11.1%, driven by commercial aquaculture expansion and the need for robust water-quality management. Industrial-scale systems integrate mechanical, biological, and chemical treatments to maintain water stability, reduce disease outbreaks, and improve production efficiency. In 2025, AI and IoT-enabled water quality monitoring adoption in aquaculture demonstrated clear operational benefits, enhancing real-time decision-making and reducing labor costs. Sustainable, automated solutions combined with regulatory compliance support long-term growth in this end-user segment.

Regional Insights

North America Aquarium Water Treatment Market Trends

North America is poised to dominate in 2026, projected to hold around 35% of the aquarium water treatment market share, driven by strong U.S. consumer demand, pet ownership, and institutional investment in aquaculture and aquarium ecosystems. The Aquaculture America 2025 conference in New Orleans, the largest triennial gathering of aquaculture professionals, producers, and technology providers, underscored the region's focus on innovation, sustainability, and advanced water-quality management practices. Government-supported extension programs, such as the NOAA eeBLUE Aquaculture Literacy Mini-Grants, are educating communities on sustainable seafood and aquaculture practices, linking water quality awareness to broader ecosystem stewardship.

The United States also sees continued investment in public aquarium expansions and experiential exhibits, such as the Texas State Aquarium’s US$ 2 million “Ocean Odyssey” project opening ahead of its 36th anniversary, which enhances conservation education and high-tech display environments. Canada’s salmon and cold-water aquaculture sectors drive the adoption of professional systems, while high household aquarium penetration supports recurring demand for advanced water treatment products. Smart monitoring systems, IoT integration, and automated dosing solutions are increasingly incorporated into both residential and commercial installations. Regulatory support, mature supply chains, and strong retail networks underpin sustained market leadership and technology integration across North America.

Europe Aquarium Water Treatment Market Trends

Europe appears to be a significant regional market for aquarium water treatment solutions in 2026, supported by well-established regulatory frameworks and strong consumer interest in sustainable aquatic systems. The Aquaculture Europe 2025 conference in Valencia brought together over 3,000 experts, researchers, and industry professionals, with sessions emphasizing sustainable production, health and welfare, and technology innovation in aquaculture and water quality management. Such gatherings demonstrate active collaboration between government bodies, research institutions, and industry stakeholders to accelerate innovation and compliance with environmental standards.

In Europe, the market, led by Germany, the U.K., France, and Spain, benefits from harmonized policies that support the adoption of eco-friendly and automated solutions. The trade exhibitions at Aquaculture Europe showcased emerging technologies in water monitoring and sustainable systems, helping producers and suppliers adapt to evolving regulatory demands and consumer expectations. Sustainability remains a central purchase driver, encouraging uptake of biological treatments and energy-efficient systems. Combined with strong public aquarium investment and growing ornamental fish trade, Europe continues to balance innovation with stringent environmental compliance, widening market potential across residential and commercial segments.

Asia Pacific Aquarium Water Treatment Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market for aquarium water treatment, with a CAGR of 11.4% forecast for 2026–2033, driven by rapid urbanization, rising disposable incomes, and expanding aquaculture activity in China, India, and ASEAN nations. Large aquaculture events and knowledge exchanges, including strategic focus on sustainable practices at regional forums, are boosting adoption of smart water quality solutions. In 2025–2026, both policy support and industry momentum, exemplified by major conferences relocating to key urban centers such as World Aquaculture 2025 India in Hyderabad, have underscored the region’s growing influence on the global stage.

China continues to lead in ornamental fish production and has implemented technologies that improve large-scale water quality control. Urban middle classes in India and Southeast Asian countries increasingly adopt sophisticated residential aquariums and automated water treatment systems as lifestyle purchases. Aquaculture modernization programs and government policies in countries such as Vietnam and Indonesia support real-time water monitoring and ecosystem management practices, creating demand for industrial water treatment technologies. Investments in manufacturing, strong supply chains, and integrated solutions for both commercial aquaculture and consumer segments further support rapid regional expansion and technology adoption.

Competitive Landscape

The global aquarium water treatment market exhibits a moderately consolidated structure, with leading players such as Pentair, Fluval (Rolf C. Hagen Inc.), AquaLogic, API, and Tetra holding over 50% of the revenue share. These established companies leverage extensive distribution networks, strong brand recognition, and integrated solutions spanning mechanical filtration, UV sterilization, chemical treatments, and biological media. They continue to invest in R&D to maintain technological leadership, focusing on smart monitoring systems, automated dosing solutions, and eco-friendly treatment formulations.

Regional and niche competitors, including AquaOne, Oase GmbH, and Marineland, are focusing on specialized applications such as high-density aquaculture, public aquariums, and ornamental fish systems in their respective geographies. Regulatory compliance, operational complexity, and high equipment costs create barriers for new entrants. However, digital water quality monitoring and IoT-enabled filtration systems are enabling smaller tech-driven companies to participate through cloud-based or automated solutions. Market consolidation is expected to rise gradually as global leaders pursue acquisitions, strategic partnerships, and technology integrations, while innovation-focused firms collaborate to enhance product performance, sustainability, and customer reach.

Key Industry Developments

- In January 2026, GC Rieber AS acquired 100% of Biomega Group to strengthen its circular aquaculture value chain. Biomega will focus on sustainable production of high-quality marine ingredients from salmon and trout, reinforcing GC Rieber’s position in the aquaculture bio-economy.

- In November 2025, Nijhuis Saur Industries (NSI) acquired a majority stake in French water treatment company Coldep to accelerate the deployment of Coldep’s patented Vacuum Air Lift (VAL) technology. The technology enhances aquaculture water treatment by removing micropollutants and reducing chemical usage.

- In September 2025, the NITTE-GOK Aquamarine Innovation Centre in Mangaluru incubated six startups focused on smart aquaculture and marine biotechnology. These ventures are developing solutions such as energy-efficient water-to-water heat pumps and traceable seafood supply chains, supported through mentoring partnerships with ICAR institutes and specialized lab and training facilities.

Companies Covered in Aquarium Water Treatment Market

- ABB Ltd.

- Siemens AG

- Alstom Grid

- Eaton Corporation

- Schneider Electric SE

- Hitachi Energy

- Mitsubishi Electric Corporation

- GE Grid Solutions

- Parker Hannifin Corporation

- Schweitzer Engineering Laboratories, Inc.

- NARI Technology Co., Ltd.

- Guodian Electric Co., Ltd.

- Nozomi Networks, Inc.

- Cisco Systems, Inc.

- Ericsson

Frequently Asked Questions

The global aquarium water treatment market is projected to reach US$ 1.5 billion in 2026.

Rising pet ownership, aquaculture expansion, public aquarium investments, and adoption of advanced filtration and UV sterilization systems are driving the market.

The market is poised to witness a CAGR of 9.4% from 2026 to 2033.

Expansion of commercial aquaculture, demand for eco-friendly biological treatments, and growth in emerging residential markets represent major opportunities.

Pentair, Fluval (Rolf C. Hagen Inc.), AquaLogic, API, and Tetra are among the leading companies in this market.