- Home Care & Utilities

- Aquarium Heaters and Chillers Market

Aquarium Heaters and Chillers Market Size, Share, Trends, Growth, Regional Forecasts 2026 to 2033

Aquarium Heaters and Chillers Market by Product (Submersible Heater, In-line Heater, Hang-on Heater, Thermoelectric Chillers, Others), End-user (Residential, Commercial, Public Aquariums & Institutions, Others), Material (Plastic, Metal Alloys, Others), Sales Channel, and Regional Analysis 2026 - 2033

Aquarium Heaters and Chillers Market Share and Trends Analysis

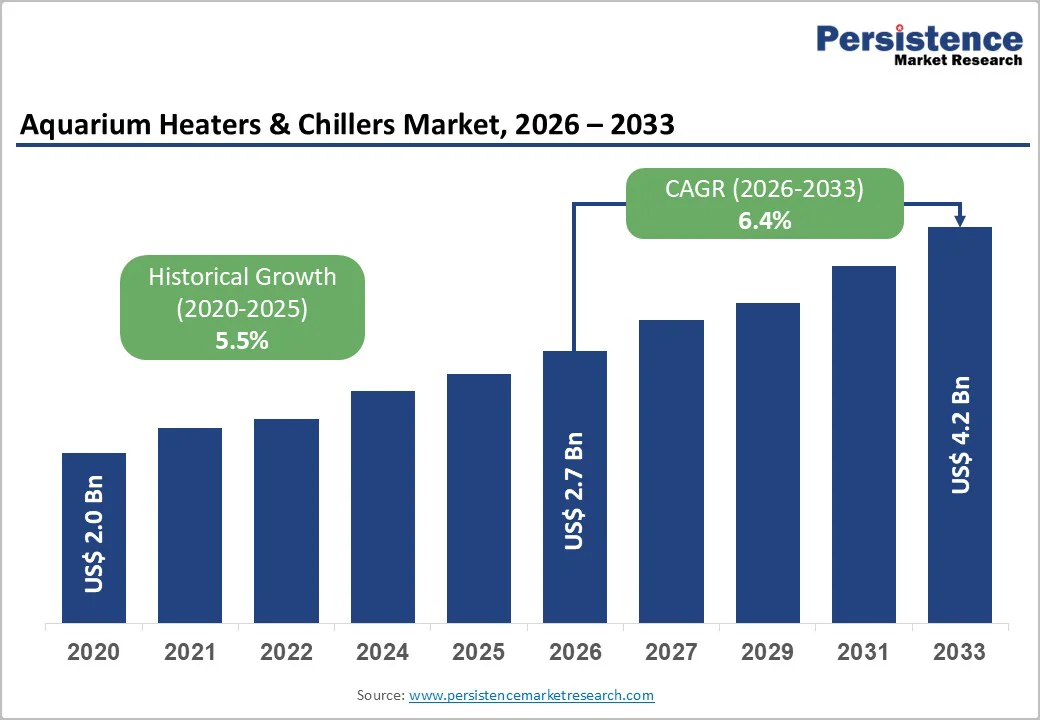

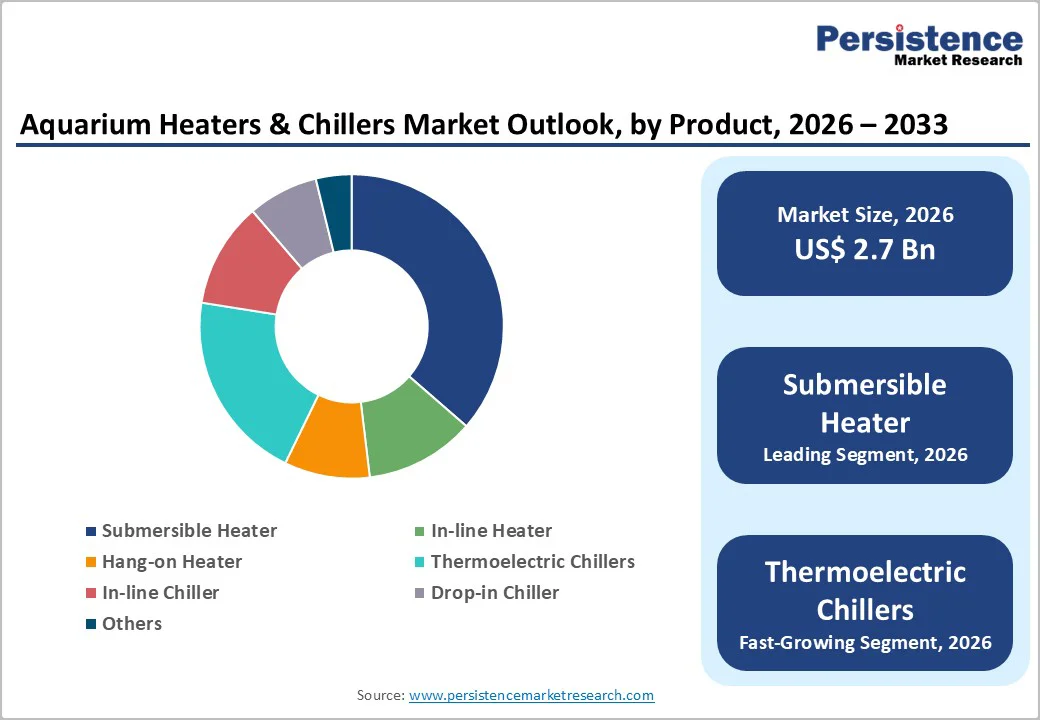

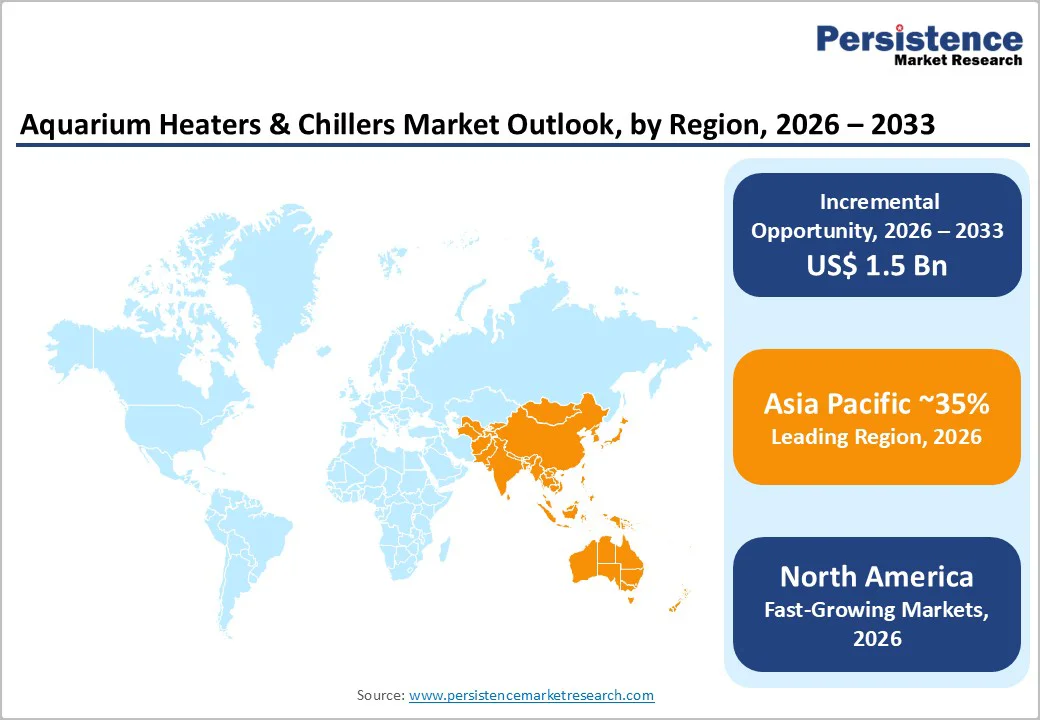

The global aquarium heaters and chillers market size is likely to be valued at US$2.7 billion in 2026 and is projected to reach US$4.2 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

The market's robust growth trajectory is driven by three primary catalysts: increasing global pet ownership and aquarium hobby adoption, technological advancements in energy-efficient temperature control systems, and expanding commercial applications in aquaculture and public aquariums.

The rising middle class in Asia Pacific regions, coupled with growing environmental consciousness regarding energy consumption, continues to fuel demand across both residential and commercial segments. This growth pattern indicates sustained investor interest and manufacturing expansion opportunities throughout the forecast period.

Key Highlights Summary

- Submersible heaters command 36% market share as the leading segment, while thermoelectric chillers accelerate at 7.3% CAGR exceeding overall market growth, driven by specialized aquarium applications and temperature-sensitive species requirements

- Residential end-users dominate with 58% share, while public aquariums and institutions expand at 7.1% CAGR, reflecting facility construction momentum particularly across the Asia Pacific regions supporting long-term commercial segment profitability.Asia Pacific region maintains 35% global market share and fastest growth trajectory, driven by urbanization momentum and aquaculture intensification creating substantial manufacturing and distribution opportunities

- Online sales channels accelerate at 8.2% CAGR, significantly outpacing traditional retail channels, reflecting e-commerce normalization and manufacturer direct-to-consumer strategies fundamentally reshaping distribution competitive dynamics and customer engagement models.

| Key Insights | Details |

|---|---|

| Aquarium Heaters and Chillers Market Size (2026E) | US$ 2.7 billion |

| Market Value Forecast (2033F) | US$ 4.2 billion |

| Projected Growth CAGR (2026 - 2033) | 6.4% |

| Historical Market Growth (2020 - 2025) | 5.5% |

Market Dynamics Analysis

Drivers - Rising Pet Ownership and Aquarium Hobby Popularization

The aquarium hobby has experienced unprecedented growth over the past five years, with the global ornamental fish trade reaching approximately US$357 million in 2023, reflecting consistent year-over-year expansion.

This surge is primarily attributed to the therapeutic benefits of aquariums, with scientific studies demonstrating that observing aquatic environments reduces stress and promotes mental wellness, a critical factor for urban populations experiencing increased occupational pressure. Pet humanization trends have accelerated substantially, with consumers now investing in premium aquarium setups that require sophisticated temperature management systems.

The demographic shift toward younger age groups engaging in aquascaping, the art of arranging aquatic plants and décor, has expanded the addressable market beyond traditional hobbyists. Additionally, the integration of aquariums into interior design schemes, particularly in corporate offices, hotels, and healthcare facilities, has created new commercial demand channels.

This expansion correlates directly with increased disposable income in emerging markets, particularly across Asia Pacific regions where aquaculture and ornamental fishkeeping traditions remain culturally significant.

Technological Innovation and Energy Efficiency Imperative

Smart aquarium technology represents one of the fastest-growing segments, with smart/Wi-Fi-enabled temperature controllers experiencing growth rates exceeding 11% CAGR through 2033.

Modern Heaters and Chillers now incorporate programmable thermostats, IoT connectivity, mobile app controls, and real-time monitoring capabilities that appeal to technology-savvy consumers. Energy efficiency has become a primary purchasing criterion, with consumers actively seeking products that reduce power consumption while maintaining optimal thermal regulation.

The integration of artificial intelligence and predictive analytics enables preventive maintenance alerts, reducing equipment failures and associated costs. Manufacturers such as EHEIM, Finnex, and JBJ have invested heavily in R&D to develop devices that comply with stringent energy efficiency standards across developed economies.

This technological convergence has resulted in a market characterized by continuous product innovation cycles, shorter time-to-market for new offerings, and intensified competitive differentiation through feature enhancement rather than price competition alone.

Restraints- High Initial Capital Investment and Price Sensitivity

Advanced aquarium Heaters and Chillers command premium price points ranging from US$150-2,000+ for commercial-grade units, creating significant barriers to entry for price-sensitive consumer segments. The elevated initial investment requirement, particularly for thermoelectric chillers and smart-enabled systems, constrains adoption among hobbyists with limited budgets.

Additionally, fluctuating raw material costs, including copper, titanium alloys, and semiconductor components, have introduced pricing volatility that complicates consumer purchasing decisions and manufacturer margin management. The market fragmentation across price tiers has resulted in intense competitive pressure in value segments, compressing profitability for manufacturers competing on cost rather than innovation.

This pricing complexity particularly impacts emerging market penetration, where average disposable incomes remain substantially lower than those in developed economies.

Supply Chain Complexity and Manufacturing Constraints

The Aquarium temperature control equipment industry remains heavily dependent on specialized component sourcing, with critical parts sourced from limited supplier bases concentrated in Asia. Supply chain disruptions, whether from geopolitical tensions, transportation bottlenecks, or pandemic-related manufacturing interruptions, have created inventory management challenges for both manufacturers and retailers.

The technical sophistication of modern controllers has increased dependence on semiconductor availability, creating acute vulnerabilities to global chip supply constraints. Additionally, the fragmented manufacturing landscape, characterized by numerous small-to-medium enterprises producing region-specific variants, has limited economies of scale and standardization benefits that could reduce costs.

These structural constraints have resulted in extended lead times for custom orders and limited product availability during peak demand periods, potentially constraining market growth projections.

Opportunity - Expansion and Urbanization Momentum in the Asia Pacific

Asia Pacific represents the dominant regional market with approximately 35% global market share and continues experiencing the highest absolute growth rates. Rapid urbanization across China, India, and Southeast Asian nations has created ~850+ million new urban residents with expanding purchasing power over the past decade.

The rising middle class in India alone, projected to reach 547 million by 2030, represents an enormous addressable market for premium aquarium equipment currently underserved by established manufacturers. Additionally, aquaculture intensification in response to growing protein demand has created substantial commercial opportunities for industrial-scale temperature control systems.

The convergence of cultural affinity for fishkeeping traditions, expanding digital infrastructure enabling e-commerce penetration, and improving logistics networks suggests Asia Pacific market expansion could accelerate from the current 35% share to 40%+ by 2033.

Sustainability-Driven Product Development and Eco-Conscious Consumer Targeting

Consumer preference for environmentally sustainable products has emerged as a significant market segmentation variable, with surveys indicating 65-75% of developed market consumers prioritize eco-friendly credentials when making purchasing decisions for equipment exceeding US$500.

The development of energy-harvesting chillers, recycled materials applications, and carbon-neutral manufacturing processes represents a US$200-350 million market opportunity within sustainability-positioned product segments.

Additionally, recycling programs and circular economy business models, where manufacturers accept trade-in equipment for refurbishment, create recurring revenue streams while addressing environmental concerns. Manufacturers positioning sustainability as core brand identity rather than peripheral marketing messaging have captured market share premiums of 15-25% versus conventional competitors.

Category-wise Analysis

Product Type Insights

Submersible heaters command the dominant market position with 36% market share, driven by their widespread adoption across both residential hobbyist and commercial aquaculture applications. These devices deliver thermal energy through direct immersion in aquatic environments, enabling efficient heat transfer and uniform temperature distribution.

The segment's market leadership reflects user preferences for ease of installation, compact form factors requiring minimal tank space, and cost-effectiveness compared to inline alternatives. Submersible heater applications span freshwater tropical fishkeeping, saltwater reef aquariums, and large-scale aquaculture facilities, creating broad addressable markets across price tiers.

Technological enhancements, including titanium sheathing for increased durability, shatterproof glass alternatives, and integrated safety shut-off mechanisms, have expanded appeal among consumers prioritizing reliability and equipment longevity.

Thermoelectric chillers represent the fastest-growing product category with 7.3% CAGR through 2033, significantly outpacing overall market growth rates. This segment's acceleration reflects increasing demand from specialty aquarium communities maintaining sensitive tropical marine species and rare freshwater ecosystems that require cooling capabilities in warm climates.

The underlying drivers include growing adoption of reef-keeping hobbies, expansion of public aquarium installations in tropical developing markets, and intensifying commercial aquaculture operations in regions with elevated ambient temperatures.

End-user Insights

Residential end-users account for 58% of total market value, reflecting the aquarium hobby's transformation from niche enthusiast pursuit to mainstream consumer activity. This segment encompasses hobbyist aquarists maintaining personal collections ranging from small desktop aquariums to elaborate show-quality installations.

Residential demand patterns exhibit strong correlation with disposable income levels, urban density, and cultural attitudes toward pets, creating distinct geographic variation. The segment benefits from continuous product innovation addressing convenience, aesthetics, and ease-of-use considerations, factors that residential consumers prioritize more heavily than commercial operators focused on operational efficiency and cost minimization.

Rising social media influence, particularly Instagram and TikTok communities celebrating aquascaping aesthetics, has elevated residential segment visibility and aspirational appeal, driving replacement cycle acceleration as established hobbyists upgrade equipment to match premium installation standards.

Public aquariums, zoological facilities, research institutions, and educational organizations constitute the fastest-growing end-user category with 7.1% CAGR. This segment's acceleration reflects the expansion of public aquarium construction globally, particularly in the Asia Pacific, where new facilities opened at record rates in 2023 - 2025.

Institutional end-users demonstrate significantly higher equipment specifications, reliability requirements, and price tolerance compared to residential segments, enabling manufacturers to capture premium margins through specialized product offerings and extended service contracts.

Material Type Insights

Plastic materials account for 51% of product composition by volume and market share, driven by cost advantages, design flexibility, and corrosion resistance in saltwater applications. Modern engineering plastics, including polycarbonate and reinforced composites, deliver performance characteristics approaching premium metal alternatives while maintaining 30-40% cost advantages.

Plastic's lightweight characteristics simplify installation and reduce structural load requirements, particularly advantageous for retrofit applications in existing facilities. However, plastic components face emerging environmental concerns regarding microplastic leaching, creating competitive vulnerability as sustainability-focused regulatory environments potentially restrict plastic applications.

This concern has prompted manufacturer investment in biodegradable alternatives and recycled plastic implementations, addressing environmental consciousness among premium market segments.

Metal alloys, including titanium, stainless steel, and specialized copper compounds, exhibit 7.1% CAGR, driven by premium market segments prioritizing durability, corrosion resistance, and extended equipment lifespans.

Metal alloy heater sheaths and chiller housings demonstrate superior performance in demanding marine environments, justifying 15-25% price premiums among serious aquarists and commercial operators. The segment benefits from marine aquaculture expansion, where saltwater corrosivity necessitates premium materials ensuring multi-decade operational lifespans.

Sales Channel Insights

Traditional wholesaler and retailer distribution channels maintain 34% market share, reflecting entrenched supply chain relationships and physical retail infrastructure serving regional markets. This channel's dominance reflects consumer preferences for tactile product evaluation, professional guidance from specialty staff, and confidence associated with established retail brands.

Independent specialty aquarium retailers, distinct from large-box retailers, provide differentiated expertise and curated product selection attracting hobbyist segments valuing personalized recommendations over purely transactional relationships. However, this channel faces competitive pressures from direct-to-consumer models as manufacturers increasingly bypass traditional intermediaries.

E-commerce platforms constitute the fastest-growing sales channel with 8.2% CAGR, driven by digital commerce normalization, improved logistics infrastructure, and manufacturer direct-to-consumer initiatives.

Online channels offer price transparency, wider product selection, and convenient home delivery, particularly appealing to time-constrained urban consumers and geographically dispersed hobbyists lacking local specialty retailers. Additionally, aggregator platforms enabling product comparison and user reviews have fundamentally altered purchasing dynamics, shifting bargaining power toward informed consumers.

Regional Market Insights

North America Aquarium Heaters and Chillers Market Trends

North America maintains substantial market presence driven by high pet ownership rates exceeding 66% of households, established aquarium hobby infrastructure, and premium pricing tolerance supporting manufacturer profitability. The United States market leadership reflects concentrated wealth, advanced retail infrastructure, and cultural emphasis on pets as family members.

Regulatory compliance requirements, particularly California's stringent energy efficiency standards mandating specific equipment certifications, have created market barriers protecting established manufacturers while elevating product quality standards.

Retail distribution remains concentrated among major chains including Petco and PetSmart, controlling 40%+ of retail channel volume, though specialty independent retailers maintain a significant presence in metropolitan areas. The region's 6.4% projected CAGR reflects mature market characteristics with growth driven by replacement cycles and product upgrades rather than new market penetration.

Commercial applications, including casino aquariums, corporate office installations, and veterinary clinic displays, represent emerging growth segments as interior designers increasingly specify aquariums for wellness environments.

North America's competitive landscape remains intensely fragmented, with numerous manufacturers competing across distinct price tiers. Premium brands, including EHEIM and Finnex command 20-25% share within specialty segments, while value competitors, including generics distributed through large-box retailers, dominate volume metrics.

The region's technological sophistication has driven IoT adoption, with smart-enabled temperature controllers experiencing 12-14% adoption rates among new equipment purchases, substantially exceeding global averages.

Europe Aquarium Heaters and Chillers Market Trends

Europe holds 29% global market share with 5.7% CAGR, characterized by stringent regulatory frameworks, high consumer environmental consciousness, and premium product preferences. Germany, the United Kingdom, France, and Spain collectively represent approximately 75% of the European market value, with Germany maintaining the largest absolute market due to its strong engineering heritage and established aquarium culture.

European regulatory emphasis on energy efficiency, particularly the EU Energy-Related Products Directive establishing minimum performance standards, has accelerated the adoption of advanced controllers and premium-efficiency equipment. Consumer preference for sustainability has driven substantial market share concentration among eco-positioned manufacturers, emphasizing recycled materials and carbon-neutral operations.

The region's distribution landscape remains predominantly retailer-dependent, with specialty aquarium shop networks maintaining a stronger market presence than in North America. Online penetration rates of 15-18% significantly trail North American levels, reflecting consumer preferences for in-store expertise and established retailer relationships.

Commercial applications, particularly public aquariums representing cultural/tourism assets, demonstrate higher growth rates than residential segments, supporting institutional end-user category expansion noted in broader market analysis.

Asia Pacific Aquarium Heaters and Chillers Market Trends

Asia Pacific represents the largest global market with 35% share and the highest absolute growth potential, driven by a massive population base, rapid urbanization, and emerging middle-class consumer segments.

China maintains market dominance with approximately 45% of the regional market value, while India, Japan, and ASEAN nations collectively represent 55% of regional volume. The region's manufacturing concentration, with 70%+ of global aquarium equipment produced in China and Vietnam, creates cost advantages enabling competitive export pricing that pressures developed market manufacturers.

Residential segment expansion reflects urbanization momentum, with metropolitan areas experiencing aquarium adoption rate accelerations of 8-12% annually among affluent urban households.

Commercial aquaculture intensity, particularly shrimp farming in Southeast Asia and tilapia production in Africa, generates substantial industrial-scale temperature control demand poorly served by traditional retail channels. The region's 35% market share is projected to expand toward 40% by 2033 as middle-class expansion accelerates purchasing capacity across India and Indonesia particularly.

Competitive Landscape

The aquarium heaters and chillers market remains highly fragmented, driven by low entry barriers, diverse customer preferences, and strong regional manufacturing bases. Leading players hold limited influence, with competition shaped by product differentiation, channel strength, and localized positioning, while smaller manufacturers thrive through niche specialization and regional focus.

Strategic Developments

- In 2024 - 2025, leading manufacturers such as EHEIM and Finnex introduced IoT-enabled temperature controllers with app connectivity, real-time alerts, and cloud monitoring. These launches target rising demand for smart aquarium systems and reinforce premium positioning through feature-led differentiation.

- In 2024, Sunsun Group and other Asian manufacturers expanded distribution networks across India and Southeast Asia, leveraging rapid aquaculture growth and increasing pet ownership. This strategic move strengthens their presence in high-growth markets and accelerates Asia Pacific market consolidation among major players.

Companies Covered in Aquarium Heaters and Chillers Market

- Central Garden and Pet Company

- Sunsun Group

- Hagan

- Shenzhen Resun Science & Technology

- EHEIM

- Finnex

- Aqueon

- Hydor

- JBJ Lighting

- TECO

- Lando Chillers

- Hailea

- Sicce

- Aqua Design Amano

Frequently Asked Questions

The global aquarium heaters and chillers market was valued at US$1.9741 billion in 2020, reached US$2.7159 billion in 2026, and is projected to attain US$4.1835 Billion by 2033.

Market growth is largely fueled by rising global pet ownership, increasing interest in aquarium keeping, continual technological enhancements, and stricter regulatory standards across mature regions.

The market demonstrates a historical CAGR of 5.46% (2020-2026) and accelerating future growth at 6.4% CAGR between 2026 and 2033.

Critical opportunities include Asian market expansion, integration with smart home ecosystems, and sustainability-driven product development.

Leading global players include Central Garden and Pet Company, Sunsun Group, Hagan, EHEIM, Finnex, Aqueon, TECO, JBJ Lighting, Hydor, Lando Chillers, Hailea, Sicce, and Aqua Design Amano, with market leadership remaining fragmented and regionally distributed, reflecting diverse customer preferences and specialized application requirements.