- Healthcare Services

- Anatomic Pathology Market

Anatomic Pathology Market Size, Share, and Growth Forecast, 2026 - 2033

Anatomic Pathology Market by Product & Service (Instruments, Consumables, Services), Application (Disease Diagnosis, Others), End-user (Hospitals, Diagnostic Laboratories, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies), and Regional Analysis for 2026 - 2033

Anatomic Pathology Market Share and Trends Analysis

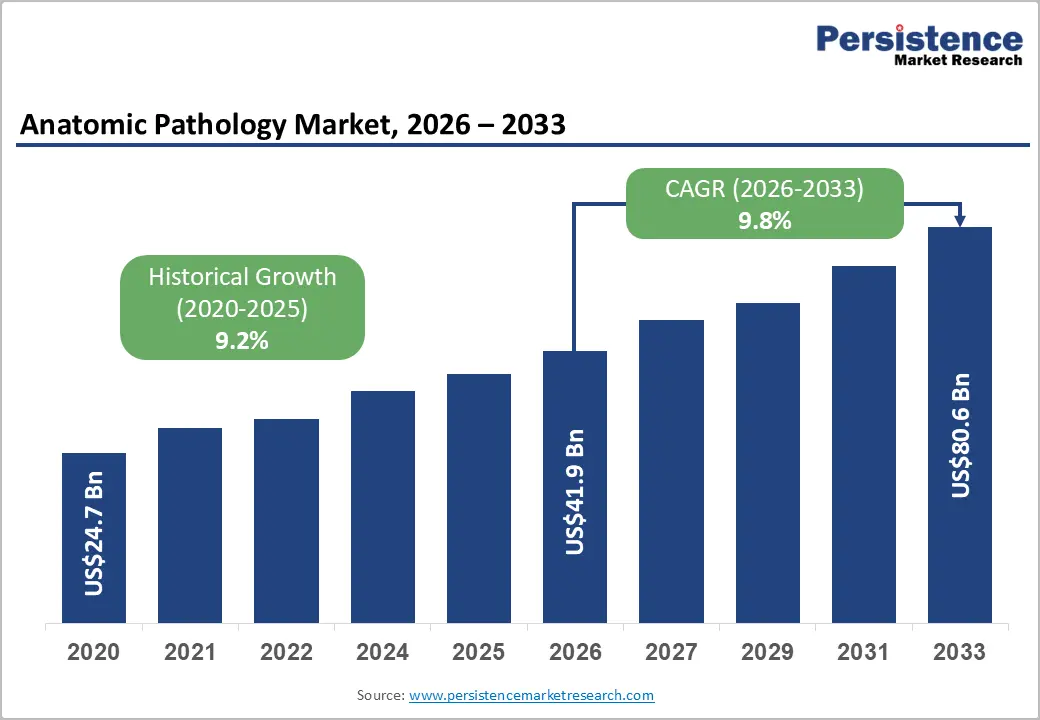

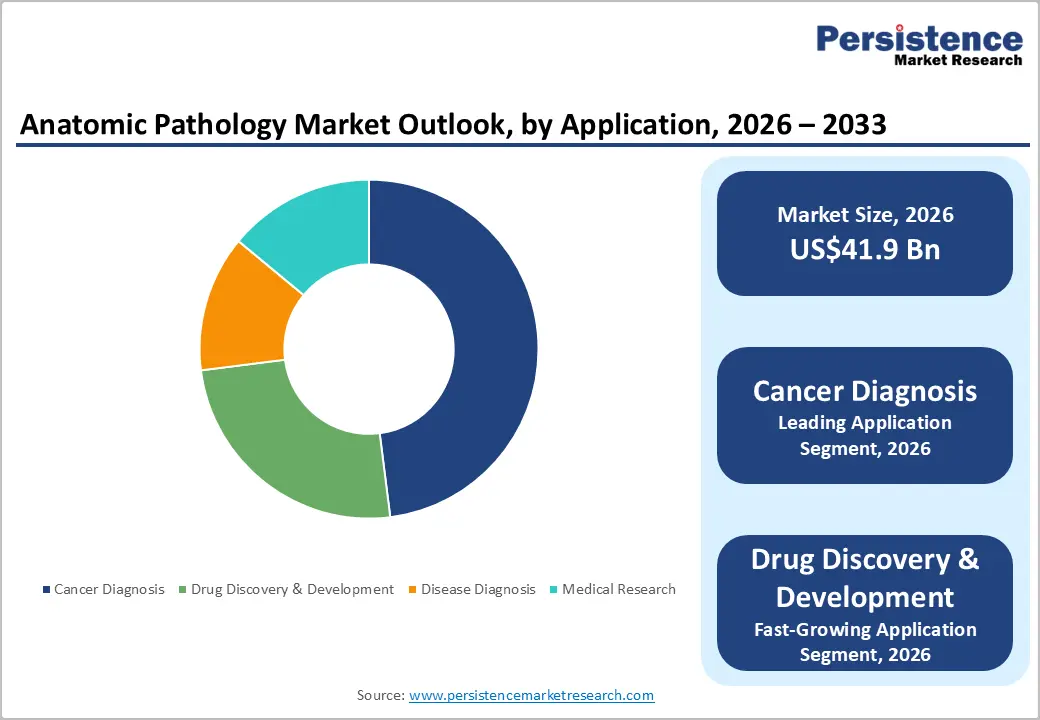

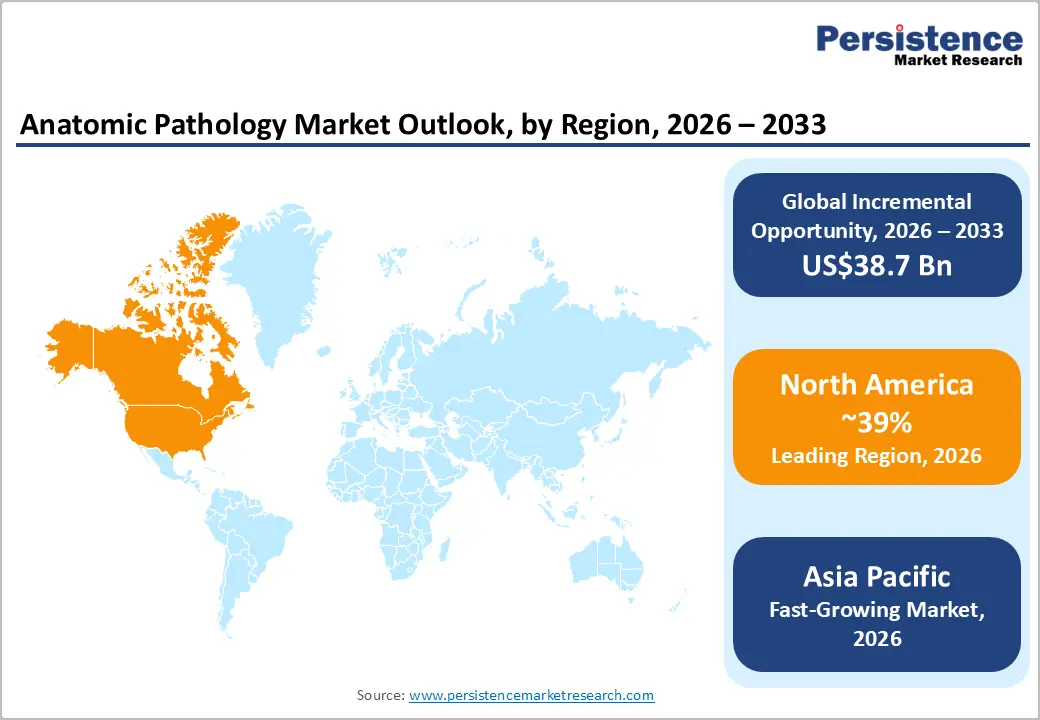

The global anatomic pathology market size is likely to be valued at US$41.9 billion in 2026 and is estimated to reach US$80.6 billion by 2033, growing at a CAGR of 9.8% during the forecast period 2026 - 2033, driven by rising cancer incidence, expansion of precision diagnostics, and accelerated digital pathology deployment.

Aging populations and increasing chronic disease burden are increasing biopsy volumes, creating sustained demand for tissue-based diagnostic workflows. Regulatory support for digital pathology systems and artificial intelligence-enabled image analysis is improving diagnostic efficiency and laboratory standardization.

Key Industry Highlights:

- Leading Product & Service: Consumables is set to hold around 52% revenue share in 2026, driven by non-discretionary reagent and stain procurement across all diagnostic laboratory settings.

- Fastest-Growing Product & Service: Services are projected as the fastest-growing segment, supported by the accelerating outsourcing of pathology functions to specialized reference laboratory networks.

- Leading Application: Cancer diagnosis is estimated to hold roughly 48% revenue share in 2026, due to mandatory tissue-based pathological confirmation embedded in every oncology treatment guideline and care pathway.

- Fastest-growing Application: Drug discovery & development is forecast to record the fastest growth, driven by expanding pharmaceutical investment in tissue-based companion diagnostic co-development programs.

- Regional Leadership: North America is projected to capture roughly 39% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to expanding healthcare digitization and oncology infrastructure.

- Competitive Environment: The market reflects a moderately consolidated structure, with key players such as Roche Diagnostics, Leica Biosystems, and Thermo Fisher Scientific leveraging integrated reagent-instrument ecosystems and AI software partnerships to sustain competitive differentiation.

DRO Analysis

Driver - Escalating Cancer Incidence and Histopathological Demand

Rising cancer incidence rates across all major geographies directly expand the volume of biopsies, surgical resections, and cytology specimens requiring pathological examination. The U.S. Centers for Disease Control and Prevention reported in 2025 that cancer remains the second-leading cause of death in the United States, with over 2,041,910 new cases diagnosed annually. This trajectory forces health systems to scale diagnostic capacity commensurately.

Anatomic pathology serves as the gold standard for definitive cancer diagnosis and staging, making its utilization inseparable from oncology care pathways. The integration of immunohistochemistry and molecular profiling into standard tissue analysis protocols raises per-specimen revenue and extends the scope of services, drawing capital investment from both public and private healthcare institutions.

Restraint - Pathologist Workforce Shortages and Diagnostic Complexity

Growing specimen volumes are increasing workload pressure on trained pathology professionals. Shortages of skilled pathologists and laboratory technicians are limiting diagnostic capacity across healthcare institutions. Increasing complexity of molecular pathology and precision oncology testing requires specialized expertise, creating staffing challenges for laboratories attempting to scale advanced pathology services within limited workforce availability.

Training requirements for digital pathology systems and artificial intelligence-assisted diagnostics are extending workforce transition periods. Rural and community healthcare institutions face greater recruitment difficulties, reducing diagnostic coverage outside major healthcare centers. Workforce limitations increase reporting delays and reduce laboratory productivity. Rising labor expenditure is affecting profitability for diagnostic service providers and constraining expansion of pathology operations.

Opportunity - Expansion of Precision Oncology and Companion Diagnostics

Precision medicine adoption is creating strong growth pathways for biomarker-driven pathology testing. Oncology drug development increasingly depends on tissue-based companion diagnostics for patient stratification and therapy selection. Pharmaceutical companies are integrating pathology analysis into clinical trial workflows to improve targeted treatment identification. Expansion of molecular pathology capabilities is creating long-term opportunities for advanced staining systems, digital image analysis, and tissue diagnostics platforms.

Collaborative partnerships between diagnostics companies and pharmaceutical manufacturers are accelerating pathology innovation. In 2026, Roche agreed to acquire PathAI to strengthen artificial intelligence-enabled pathology capabilities within oncology diagnostics. Regulatory emphasis on personalized medicine is encouraging hospitals to expand molecular testing infrastructure. Rising integration of genomics and pathology data is supporting development of next-generation diagnostic ecosystems.

Category-wise Analysis

Product Type Insights

Consumables are anticipated to secure around 52% of the anatomic pathology market share in 2026, reflecting the non-discretionary nature of reagent, stain, and slide procurement across diagnostic workflows. Leica Biosystems' tissue processing reagents exemplify the recurring purchase cycle that drives predictable revenue. Continuous specimen throughput guarantees consistent consumable replenishment irrespective of capital expenditure cycles.

Services are expected to be the fastest-growing segment, propelled by rising outsourcing of anatomic pathology functions to specialized reference laboratories. Mayo Clinic Laboratories' nationwide tissue consultation network demonstrates the scalability of this model. Healthcare systems seeking to reduce fixed infrastructure costs are transferring specimen analysis to contracted service providers, generating sustained double-digit volume growth in this category.

Application Insights

Cancer diagnosis applications are poised to dominate with a forecast market share of over 48% in 2026, powered by the central role of tissue biopsy in oncology staging and treatment selection. The NCCN Guideline-mandated pathological confirmation of malignancy before systemic therapy initiation locks anatomic pathology into every oncology care pathway, ensuring sustained specimen volume regardless of treatment modality shifts.

Drug discovery & development is estimated to be the fastest-growing segment, fueled by escalating pharmaceutical investment in oncology and immunology pipeline assets requiring histopathological tissue validation at preclinical and early clinical stages. AstraZeneca's extensive investment in tissue biomarker programs exemplifies pharma-driven demand growth, compelling contract research organizations to expand anatomic pathology service capacity.

End-user Insights

Hospitals are likely to be the leading segment with a projected 44% of the anatomic pathology market share in 2026 due to high surgical volume, inpatient biopsy procedures, and integrated pathology department infrastructure. Cleveland Clinic's in-house pathology program, processing more than 20 million tests, reflects the institutional anchoring of hospital-based pathology services in high-acuity care settings.

Pharmaceutical & biotechnology companies are anticipated to be the fastest-growing segment, fueled by the surge in tissue-based companion diagnostic co-development agreements accompanying precision medicine drug approvals. Roche's co-development of PD-L1 immunohistochemistry assays alongside cancer immunotherapy programs demonstrates the structural demand these partnerships generate within anatomic pathology laboratories.

Regional Insights

North America Anatomic Pathology Market Trends

North America is expected to lead with an estimated 39% of the anatomic pathology market share in 2026, supported by advanced oncology infrastructure, high digital pathology adoption, and increasing artificial intelligence integration within hospital laboratories. Expansion of precision medicine initiatives is increasing tissue-based testing demand across healthcare systems. FDA clearances for digital pathology systems are accelerating commercialization of automated diagnostic platforms.

U.S. Anatomic Pathology Market Insights

The U.S. is projected to account for nearly 82% of North America's share in 2026, driven by increasing cancer screening programs, expanding oncology laboratories, and strong reimbursement support for pathology diagnostics. PathAI, Labcorp, and Danaher are expanding artificial intelligence-assisted pathology operations to improve workflow efficiency and remote diagnostics capabilities.

Canada Anatomic Pathology Market Insights

Canada is expected to hold approximately 18% of North America's share in 2026, supported by healthcare digitization programs and increasing pathology modernization within provincial healthcare systems. Academic institutions are expanding molecular pathology capabilities for precision oncology applications. Growing collaboration between hospitals and research laboratories is improving digital pathology integration.

Europe Anatomic Pathology Market Trends

Europe is projected to capture around 28% of the anatomic pathology market share in 2026, supported by increasing precision diagnostics adoption, expanding cancer research programs, and modernization of pathology laboratories across healthcare systems. Regulatory alignment supporting digital healthcare technologies is encouraging deployment of automated pathology platforms.

Germany Anatomic Pathology Market Insights

Germany is forecast to contribute nearly 24% of Europe's share in 2026, driven by advanced hospital infrastructure and increasing deployment of artificial intelligence-enabled pathology imaging systems. University hospitals are integrating molecular pathology platforms into oncology treatment programs. Expansion of cancer screening initiatives is increasing specimen processing volumes across pathology laboratories.

U.K. Anatomic Pathology Market Insights

The U.K. is likely to account for approximately 18% of Europe's share in 2026, stimulated by National Health Service digitization initiatives and rising investment in pathology network consolidation. Centralized laboratory models are improving workflow efficiency and diagnostic standardization. Growing telepathology adoption is supporting remote consultation services across healthcare regions.

Asia Pacific Anatomic Pathology Market Trends

Geography is forecast to be the fastest-growing market for anatomic pathology, stimulated by expanding healthcare infrastructure, rising cancer incidence, and increasing laboratory modernization investments across emerging economies. Fujifilm, Olympus, and Hamamatsu Photonics are expanding pathology imaging and slide scanning capabilities across healthcare institutions.

China Anatomic Pathology Market Insights

China is expected to represent nearly 36% of Asia Pacific share in 2026, driven by the expansion of oncology hospitals, increasing pathology laboratory construction, and rising precision medicine investment. Government initiatives supporting healthcare technology localization are accelerating domestic pathology equipment manufacturing. Large urban hospitals are adopting digital pathology systems to manage rising diagnostic workloads.

India Anatomic Pathology Market Insights

India is projected to account for approximately 17% of Asia Pacific share in 2026, supported by increasing cancer awareness programs, growth in private diagnostic chains, and rising investment in digital healthcare infrastructure. Expansion of pathology laboratory networks is improving access to tissue diagnostics within urban and semi-urban healthcare facilities. Apollo Diagnostics and Dr. Lal PathLabs are strengthening molecular pathology and oncology testing capabilities.

Competitive Landscape

The global anatomic pathology market is moderately consolidated, with a limited number of large multinational corporations controlling premium instrument and reagent segments, while a broader tier of regional and specialty players competes in services and niche consumable categories. Companies such as Roche Diagnostics, Leica Biosystems, Hologic, Sakura Finetek, and Thermo Fisher Scientific anchor the competitive landscape through extensive product portfolios, established distribution networks, and long-term reagent rental agreements.

Scale advantages in reagent manufacturing, proprietary staining chemistries, and integrated software ecosystems create meaningful switching costs that protect the incumbent positions of leading players. Mid-tier competitors differentiate through service responsiveness, regional pricing flexibility, and focused innovation in digital pathology software, creating a bifurcated competitive dynamic where size and specialization each support distinct value propositions.

Key Industry Developments:

- In December 2025, Leica Biosystems expanded its clinical digital pathology portfolio with new Aperio scanners and artificial intelligence-enabled quality control software at DPAI 2025, reinforcing automation and workflow efficiency across pathology laboratories.

- In July 2025, PathAI launched the Precision Pathology Network powered by the AISight platform, reinforcing artificial intelligence-driven collaboration, real-world data integration, and digital diagnostics expansion across pathology laboratories.

Companies Covered in Anatomic Pathology Market

- Roche Diagnostics

- Leica Biosystems

- Hologic Inc.

- Thermo Fisher Scientific

- Sakura Finetek

- Danaher Corporation

- Sysmex Corporation

- Philips Healthcare

- Agilent Technologies

- Becton Dickinson

- Indica Labs

- Paige.AI

- PathAI

- Mindray

Frequently Asked Questions

The global anatomic pathology market is projected to reach US$41.9 billion in 2026.

Rising cancer incidence, increasing adoption of digital pathology and artificial intelligence-based diagnostics, and expanding precision medicine programs drive the anatomic pathology market.

The anatomic pathology market is poised to witness a CAGR of 9.8% from 2026 to 2033.

Growing cancer screening volumes, rising demand for precision diagnostics, and increasing adoption of digital pathology technologies drive the anatomic pathology market.

Some of the key market players include Roche Diagnostics, Leica Biosystems, Hologic, Sakura Finetek, and Thermo Fisher Scientific.