- Pharmaceuticals

- Amyloidosis Therapeutics Market

Amyloidosis Therapeutics Market Size, Share, and Growth Forecast 2026 - 2033

Amyloidosis Therapeutics Market by Treatment (Chemotherapy, Immunosuppressive Drugs, Transplantation, Supportive Care, Surgery, Others), End-user (Hospitals & Clinics, Home Care, Ambulatory Surgical Centers, Others), and Regional Analysis, 2026 - 2033

Amyloidosis Therapeutics Market Share and Trends Analysis

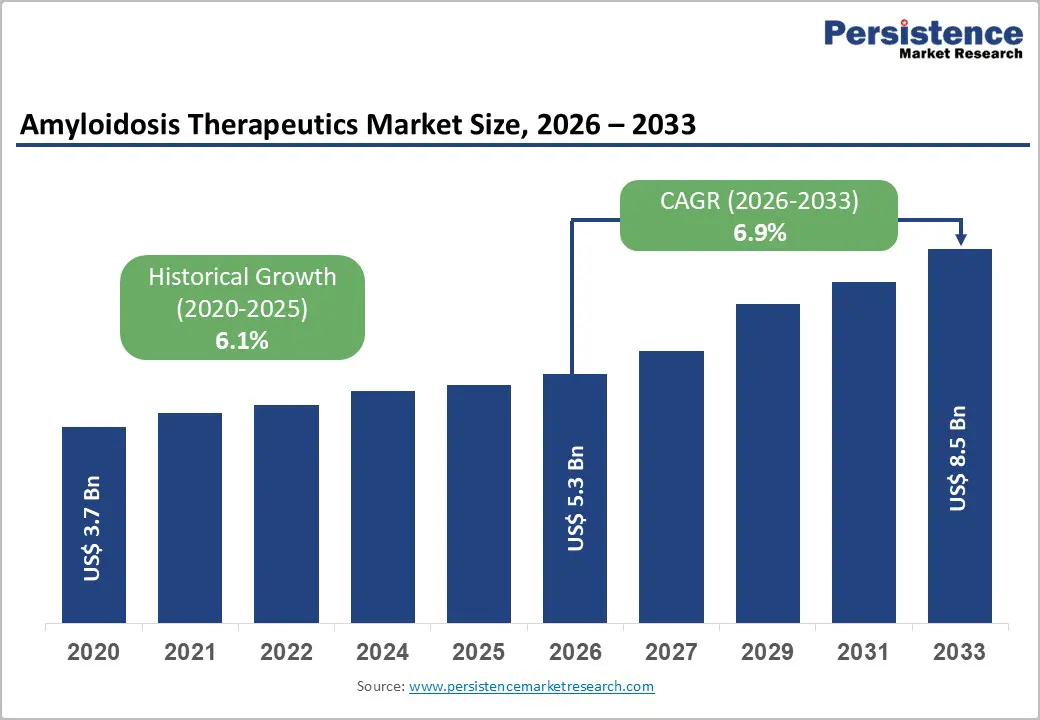

The global amyloidosis therapeutics market size is expected to be valued at US$ 5.3 billion in 2026 and projected to reach US$ 8.5 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033. It is growing steadily due to increasing recognition of rare protein misfolding disorders and advancements in targeted treatment approaches. Amyloidosis, including AL and ATTR types, leads to progressive organ dysfunction, driving demand for effective and early-stage therapies.

Rising awareness, improved diagnostic capabilities, and expanding availability of novel drugs such as monoclonal antibodies, RNA-based therapies, and supportive care treatments are strengthening market growth. Pharmaceutical companies are focusing on orphan drug development and precision medicine to address high unmet clinical needs. The increasing elderly population and ongoing clinical research are further supporting the global expansion of amyloidosis treatment options across healthcare systems.

Key Industry Highlights:

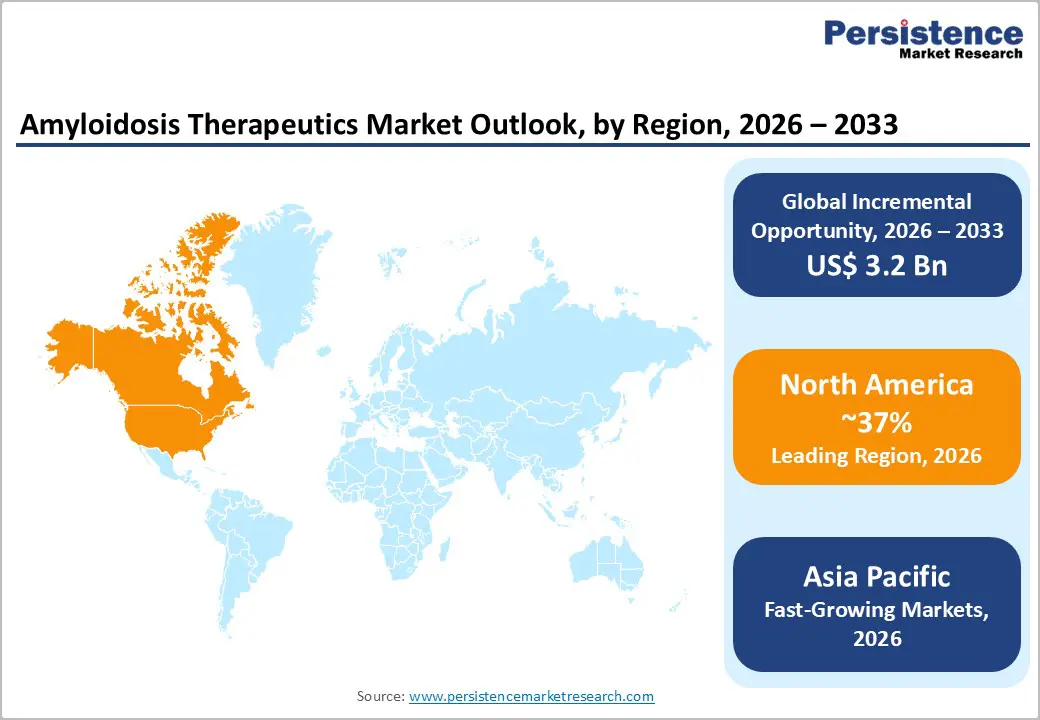

- Leading Region - North America commanded approximately 37% of the global amyloidosis therapeutics market share in 2025, driven by FDA-approved Amvuttra®, Onpattro®, and Vyndaqel®, Medicare Part D reimbursement, and concentration of specialist amyloidosis centers at Mayo Clinic and Boston Medical Center.

- Fast-Growing Market - Asia-Pacific is the fastest-growing market, driven by Japan's PMDA approval of three Alnylam/Pfizer therapies, China's NMPA tafamidis approval, and endemic Val30Met hATTR populations in Japan and India's CDSCO expanding access programs.

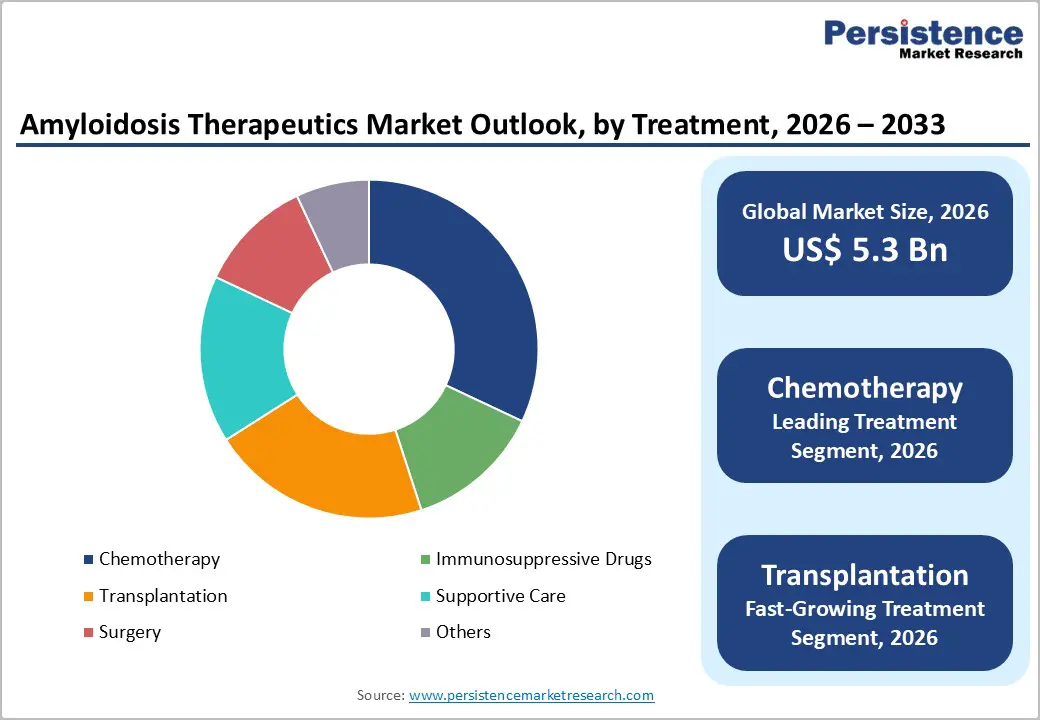

- Dominant Treatment- Chemotherapy held approximately 32% of the treatment segment market share in 2025, anchored by daratumumab (Darzalex®), achieving 40%+ hematologic complete response rates in AL amyloidosis, endorsed by International Society of Amyloidosis (ISA) guidelines.

- Fast-Growing Treatment - Transplantation is the fastest-growing treatment type, driven by expanding combined heart-liver transplant programs at Mayo Clinic, Cleveland Clinic, and Johns Hopkins, growing OPTN amyloidosis transplant listings, and domino transplantation protocol innovations.

- Key Opportunity - RNAi Expansion into Cardiomyopathy: Alnylam's HELIOS-B positive results for Amvuttra® in ATTR cardiomyopathy targeting an estimated 13% of hospitalized heart failure patients 60+ per JACC represent a US$ 3.2 billion incremental opportunity.

Market Dynamics

Drivers - FDA Approval of RNA Interference Therapies Transforming the Amyloidosis Treatment Landscape

The U.S. Food and Drug Administration (FDA)'s approval of RNA interference (RNAi) therapies has fundamentally transformed the amyloidosis treatment landscape, establishing a new generation of disease-modifying options that address the genetic root cause of hereditary transthyretin (hATTR) amyloidosis. Alnylam Pharmaceuticals' Onpattro® (patisiran) approved in 2018 as the first-ever RNAi therapeutic, was followed by Alnylam's Amvuttra® (vutrisiran), approved by the FDA in 2022 for hATTR amyloidosis with polyneuropathy.

Alnylam's HELIOS-B trial results, published in 2024, demonstrated Amvuttra's significant efficacy in cardiomyopathy, a broader indication signaling further market expansion. The European Medicines Agency (EMA) has granted similar approvals, expanding access across EU member states. These approvals are driving a paradigm shift from symptomatic management to disease modification, expanding the revenue potential of the therapeutics market substantially.

Improving Diagnostic Capabilities: Expanding the Identified Amyloidosis Patient Population

Historically, amyloidosis has been profoundly underdiagnosed due to its protean clinical manifestations and rarity, resulting in significant delays between symptom onset and diagnosis. The advent of technetium-99m pyrophosphate (Tc-99m PYP) cardiac scintigraphy, endorsed by the American College of Cardiology (ACC) for non-invasive ATTR cardiomyopathy diagnosis, has dramatically reduced the need for invasive biopsy and is expanding the diagnosed population.

A landmark study in JACC: Cardiovascular Imaging estimated that wild-type ATTR cardiomyopathy may affect 13% of hospitalized heart failure patients over 60, a population previously undetected. This growing diagnosed cohort is directly expanding the patient population eligible for novel amyloidosis therapeutics from Pfizer's Vyndaqel® (tafamidis) and Alnylam's Amvuttra®, sustaining strong new prescription uptake through the forecast period.

Restraints - Exceptionally High Drug Pricing and Payer Access Barriers Limiting Patient Reach

The amyloidosis therapeutics market faces significant access barriers driven by the exceptionally high pricing of approved RNA interference and TTR stabilizer therapies. Pfizer's Vyndaqel® (tafamidis) carries an annual list price of approximately US$ 225,000 in the United States, while Alnylam's Amvuttra® has an annual cost exceeding US$ 450,000. These extreme price points create substantial payer reimbursement barriers from insurers and government health programs, limiting eligible patient access particularly in middle-income countries and markets with strict NICE Health Technology Appraisal cost-effectiveness thresholds in the UK.

Diagnostic Delays and Physician Awareness Gaps Constraining Market Uptake

Despite improving diagnostic tools, the median time from symptom onset to amyloidosis diagnosis remains unacceptably long, estimated at approximately 3-4 years in published studies in the Amyloid: The International Journal of Experimental and Clinical Investigation. The condition's overlapping presentation with common cardiac and neurological conditions leads to frequent misdiagnosis, particularly in non-specialized centers. Limited training of primary care physicians and general cardiologists in recognizing amyloidosis red-flag symptoms directly restricts the pipeline of newly diagnosed patients entering treatment pathways, creating a structural barrier to full realization of the addressable therapeutic market.

Opportunities - Transplantation: Fastest-Growing Treatment Segment with Expanding Indications in hATTR Management

Transplantation, encompassing liver transplantation (the primary source organ for TTR protein) and increasingly combined heart-liver transplantation, represents the fastest-growing treatment segment within the amyloidosis therapeutics market, driven by rising transplant center capability and improving patient selection protocols. Liver transplantation remains the only curative option for Val30Met hereditary ATTR amyloidosis subtypes and has demonstrated decades of efficacy data.

The Organ Procurement and Transplantation Network (OPTN) in the U.S. documents growing amyloidosis-related transplant listings, while combined heart-liver procedures increasingly performed at centers including Mayo Clinic, Cleveland Clinic, and Johns Hopkins are expanding the treatment-eligible population for advanced cardiac amyloidosis. Domino transplantation innovations, where the amyloid-producing liver is re-implanted in older non-TTR patients, are further expanding transplant program viability.

Asia-Pacific: Fastest-Growing Regional Market Driven by Diagnostic Infrastructure and Novel Therapy Launches

Asia-Pacific represents the fastest-growing regional opportunity for amyloidosis therapeutics, driven by large and historically underdiagnosed patient populations in Japan, China, India, and South Korea, combined with increasing specialty healthcare investment and progressive regulatory approvals of novel therapies. Japan, which has a well-characterized endemic hATTR mutation population in Nagano Prefecture, has driven early adoption of Alnylam's Onpattro® and Vyndaqel®, both approved by Japan's Pharmaceuticals and Medical Devices Agency (PMDA).

China's National Medical Products Administration (NMPA) is progressively approving innovative amyloidosis therapies, with Pfizer's tafamidis gaining approval and Alnylam's pipeline under regulatory review, creating a significant near-term commercial opportunity as diagnostic awareness programs expand across Asian tertiary cardiac centers.

Category-wise Analysis

Treatment Insights

The chemotherapy segment led the amyloidosis therapeutics market by treatment type, accounting for approximately 32% of total market share in 2026. In the amyloidosis context, chemotherapy encompasses high-dose melphalan, cyclophosphamide, bortezomib (Velcade®), and daratumumab (Darzalex®) the backbone of AL amyloidosis treatment, which targets the underlying plasma cell dyscrasia producing amyloidogenic immunoglobulin light chains. AL amyloidosis is the most common form of systemic amyloidosis, with approximately 4,000-4,500 new U.S. cases annually per the National Organization for Rare Disorders (NORD). Janssen's daratumumab-based combinations endorsed by the International Society of Amyloidosis (ISA) as transformative in AL treatment have achieved hematologic complete response rates exceeding 40% in landmark trials, reinforcing chemotherapy's dominant treatment revenue position.

End-user Insights

Hospitals and clinics constituted the dominant end-user segment of the amyloidosis therapeutics market, representing approximately 68% of total end-user demand in 2026. The clinical complexity of amyloidosis requiring multidisciplinary specialist care from hematologists, cardiologists, nephrologists, and neurologists mandates hospital-based management settings where comprehensive diagnostic workup, infusion services, and transplant programs are available. Comprehensive amyloidosis treatment centers at institutions including Boston Medical Center, Mayo Clinic, MD Anderson Cancer Center, and University College London Hospital serve as primary prescription and treatment hubs for novel RNAi therapies and TTR stabilizers, which require hospital-level patient monitoring infrastructure. Infusion-administered therapies, including Onpattro® and daratumumab regimens, mandate clinical settings, reinforcing the hospital and clinic segment's dominant position in end-user revenue distribution.

Regional Insights

North America Amyloidosis Therapeutics Market Trends and Insights

North America dominated the global amyloidosis therapeutics market with approximately 37% market share in 2025, driven by FDA-facilitated early access to novel RNAi and TTR stabilizer therapies, the highest amyloidosis diagnostic rates globally, comprehensive disease registry infrastructure, and a concentration of specialized amyloidosis treatment centers at academic medical institutions.

U.S. Amyloidosis Therapeutics Market Size

The U.S. accounts for approximately 90% of North American amyloidosis therapeutics revenue, anchored by FDA approvals of Vyndaqel®, Onpattro®, and Amvuttra®, Medicare Part D coverage for approved therapies, and high prescription uptake through dedicated amyloidosis centers at Mayo Clinic, Cleveland Clinic, and Boston Medical Center.

Europe Amyloidosis Therapeutics Market Trends and Insights

Europe is the second-largest market, shaped by EMA-approved amyloidosis therapy portfolios, national reimbursement decisions in Germany, France, and Italy, and the long-standing European Network for Amyloidosis (ENA) clinical research infrastructure. Hereditary ATTR amyloidosis endemic foci in Sweden, Portugal, and Northern Italy sustain consistent specialist prescription volumes for approved therapies.

Germany Amyloidosis Therapeutics Market Size

Germany leads European amyloidosis therapeutics revenue, supported by GKV statutory insurance reimbursement for Vyndaqel® and Amvuttra®, and specialist centers at Heidelberg University Hospital and University Hospital Munich. Germany's AMNOG early benefit assessment framework has approved add-on reimbursement for vutrisiran, supporting premium pricing access in the German market.

UK Amyloidosis Therapeutics Market Size

Amyloidosis therapeutics market in the UK is shaped by NICE technology appraisals, with NICE TA921 recommending vutrisiran (Amvuttra®) for hATTR polyneuropathy in 2023. The National Amyloidosis Centre (NAC) at University College London Hospital is one of the world's foremost amyloidosis clinical and research centres, driving UK prescription leadership in specialist treatment protocols.

France Amyloidosis Therapeutics Market Size

France's amyloidosis therapeutics market benefits from Sécurité Sociale reimbursement for approved TTR therapies and autorisation temporaire d'utilisation (ATU) frameworks that provide early access. France has a notable hereditary ATTR endemic cluster in Val-de-Marne, and Hôpital Bicêtre (AP-HP) is a leading national amyloidosis diagnostic and treatment center, driving prescription volumes.

Asia Pacific Amyloidosis Therapeutics Market Trends and Insights

Asia-Pacific is the fastest-growing amyloidosis therapeutics region, driven by expanding specialist care networks, progressive PMDA and NMPA therapy approvals, and growing diagnostic awareness programs. Japan leads regional adoption with early PMDA approvals of Vyndaqel® and Onpattro®, while China's NMPA approvals of tafamidis and expanding Alnylam pipeline submissions are creating significant near-term market expansion.

India Amyloidosis Therapeutics Market Size

India's amyloidosis therapeutics market is in early growth, with diagnosis and treatment concentration at AIIMS New Delhi, Tata Medical Center Kolkata, and Christian Medical College Vellore. The Central Drugs Standard Control Organisation (CDSCO) has approved tafamidis for ATTR cardiomyopathy, and India's Rare Disease Policy framework is expanding institutional treatment access.

Competitive Landscape

The global amyloidosis therapeutics market is highly competitive and evolving, driven by advancements in targeted therapies and increasing focus on rare disease management. Market players are investing in innovative treatment approaches such as monoclonal antibodies, gene-silencing therapies, and next-generation small molecules to improve patient outcomes. Competition is shaped by strong clinical pipelines, regulatory approvals for orphan drugs, and expanding research collaborations between pharmaceutical companies and academic institutes. Companies are also focusing on improving early diagnosis and personalized treatment strategies to strengthen their market position.

Key Developments

- In March 2025, Alnylam Pharmaceuticals announced that the U.S. FDA approved AMVUTTRA® (vutrisiran) for the treatment of transthyretin amyloidosis with cardiomyopathy (ATTR-CM) in adults.

- In February 2025, the European Commission granted marketing authorization for acoramidis, branded as Beyonttra™, for the treatment of wild-type or variant transthyretin amyloidosis in adult patients with cardiomyopathy (ATTR-CM).

Companies Covered in Amyloidosis Therapeutics Market

- Pfizer Inc.

- Johnson & Johnson Services, Inc.

- GSK plc

- Takeda Pharmaceutical Company Limited

- Amgen Inc.

- Bristol-Myers Squibb Company

- Novartis AG

- F. Hoffmann-La Roche Ltd

- Merck KGaA

- Sanofi

- Alnylam Pharmaceuticals, Inc.

- Others

Frequently Asked Questions

The global amyloidosis therapeutics market is expected to be valued at US$ 5.3 billion in 2026.

The primary demand drivers for the Amyloidosis Therapeutics market include the rising global prevalence of amyloidosis, especially AL and ATTR types, and increasing awareness leading to earlier diagnosis.

North America leads with approximately 37% global market share in 2025, anchored by FDA-approved Vyndaqel®, Onpattro®, and Amvuttra®, Medicare Part D reimbursement, and world-leading specialized amyloidosis treatment programs at Mayo Clinic, MD Anderson, and Boston Medical Center.

The amyloidosis therapeutics market offers strong growth opportunities driven by expanding adoption of targeted and disease-modifying therapies, including gene-silencing drugs, monoclonal antibodies, and next-generation small molecules.

Leading companies include Alnylam Pharmaceuticals, Inc. (Amvuttra®/Onpattro®), Pfizer Inc. (Vyndaqel®), Johnson & Johnson (Janssen) (Darzalex®), Novartis AG, Bristol-Myers Squibb, Takeda Pharmaceutical, and Ionis Pharmaceuticals.