- Technology

- Deep Learning Market

Deep Learning Market Size, Share, and Growth Forecast 2026 - 2033

Deep Learning Market by Offering (Hardware – Processor, Memory, Network; Software – Solution, Platform/API; Services – Installation, Training, Support & Maintenance), by Application (Image Recognition, Signal Recognition, Data Mining, Others), by End-User (Healthcare, Manufacturing, Automotive, Agriculture, Retail, Security, Human Resources, Marketing, Law, Fintech), by Regional Analysis, 2026–2033

Deep Learning Market Size and Trend Analysis

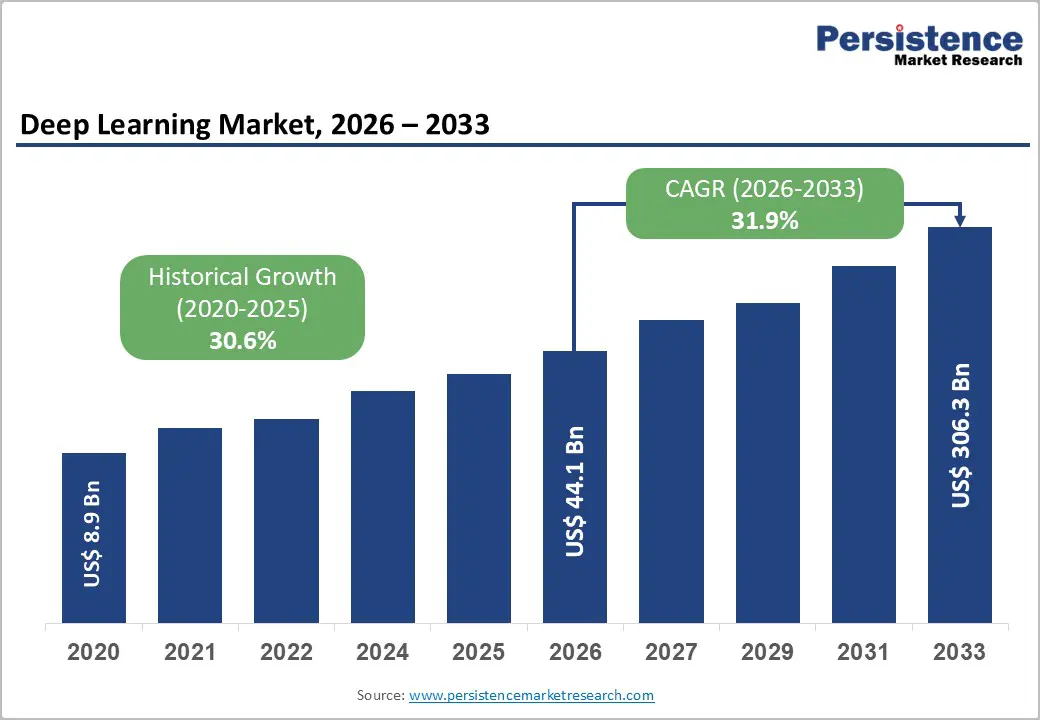

The global deep learning market size is likely to be valued at US$ 44.1 Billion in 2026 and is expected to reach US$ 306.3 Billion by 2033, growing at a CAGR of 31.9% during the forecast period from 2026 to 2033. The market has already expanded rapidly from about US$ 8.9 Billion in 2020, reflecting a historical CAGR of around 30.6% from 2020–2025. Strong demand for AI accelerators, cloud AI infrastructure, and deep learning software frameworks is being reinforced by broad enterprise AI adoption in sectors such as healthcare, automotive, retail, and financial services.

Key Market Highlights

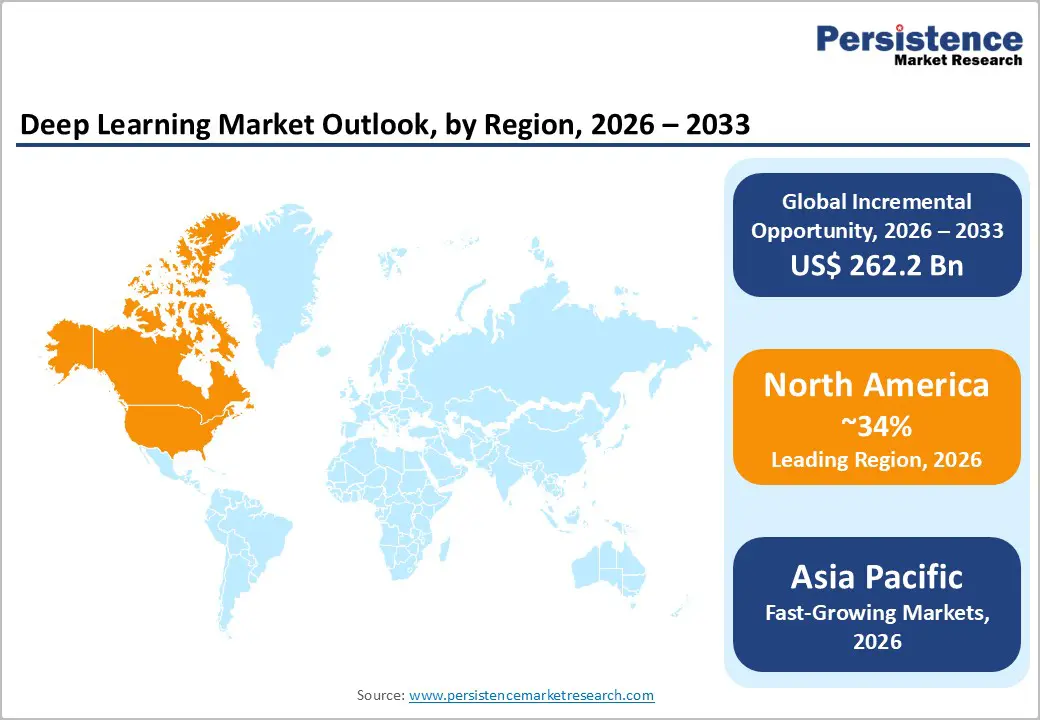

- Leading region: North America currently holds the largest share of the Deep Learning Market, with around 34% of global revenue, supported by hyperscaler investment, strong AI research ecosystems, and high adoption in healthcare, automotive, and retail.

- Fastest growing region: Asia Pacific is the fastest growing regional market, fuelled by China’s AI investment of about ¥890 Billion in 2025, expanding smart manufacturing, autonomous mobility pilots, and rapid adoption of AI in healthcare and financial services.

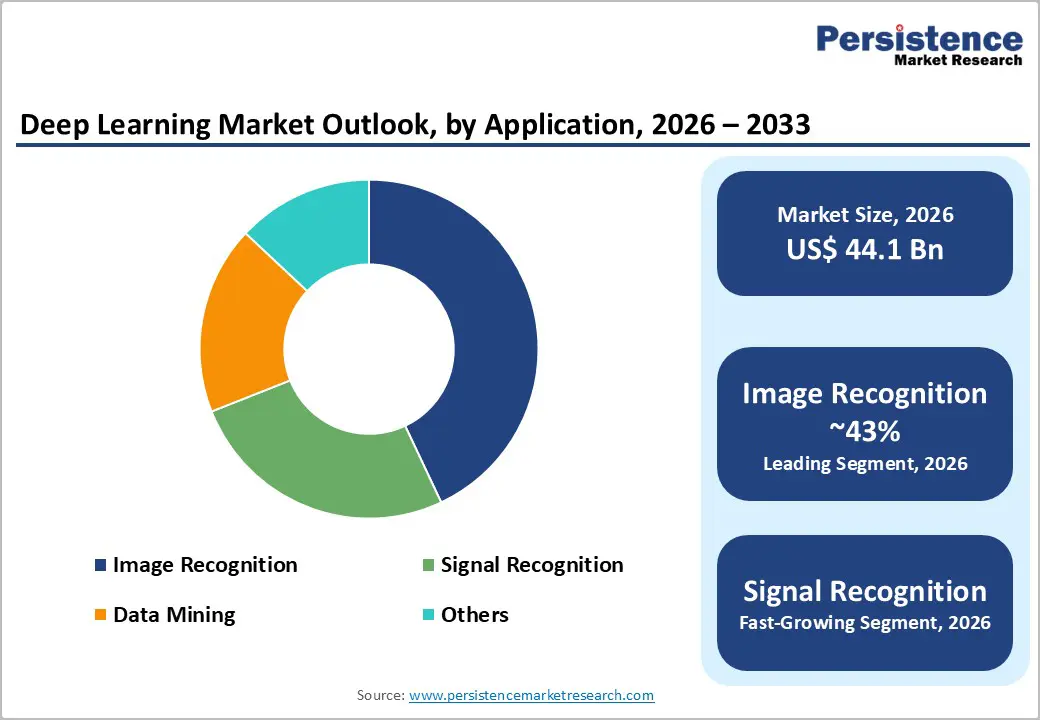

- Dominant segment: By application, Image Recognition leads with roughly 43% market share, driven by widespread use of deep learning computer vision in medical imaging, autonomous driving, industrial inspection, security, and retail store analytics.

- Fastest growing segment: Edge and embedded deep learning – including on device inference for IoT, robotics, and autonomous systems – is expanding at around 40% CAGR in related edge AI chips, reaching about US$ 70 Billion by 2030, creating new deployment opportunities.

- Key market opportunity: Generative and multimodal deep learning offers substantial upside, with McKinsey estimating US$ 240–390 billion in potential annual value for retail alone; similar productivity gains are expected across marketing, customer service, software development, and knowledge work.

| Report Attribute | Details |

|---|---|

|

Deep Learning Market Size (2026E) |

US$ 44.1 Billion |

|

Market Value Forecast (2033F) |

US$ 306.3 Billion |

|

Projected Growth CAGR (2026–2033) |

31.9% |

|

Historical Market Growth (2020–2025) |

30.6% |

Market Dynamics

Market Growth Drivers

Exploding AI compute investments and GPU-centric architectures

A primary growth driver is the surge in AI compute investments and purpose built accelerators optimized for deep learning. The global AI chip market reached roughly US$ 23.2 Billion in 2023 and is projected to more than quadruple by the late 2020s, at a CAGR above 30%, as GPUs, NPUs and other accelerators become the backbone of large scale training and inference.

In 2024, data center GPUs more than doubled year on year, with NVIDIA capturing about 92% of the data center GPU segment and generating over US$ 115 Billion in annual data center revenue in 2024, up more than 140% year over year. This unprecedented infrastructure build out – spanning cloud hyperscalers such as Microsoft Azure, AWS, and Google Cloud, and sovereign AI initiatives – dramatically lowers barriers for enterprises to deploy deep learning at scale, catalyzing demand for both hardware and software layers.

Proven performance gains in high value healthcare and safety-critical use cases

Deep learning has demonstrated superior performance to traditional algorithms and, in many settings, to human experts, creating strong pull from healthcare, security, and autonomous systems. Clinical studies show convolutional neural networks achieving around 95–97% sensitivity and 96–97% specificity in tasks such as chest radiograph classification, outperforming radiologists in some controlled trials. A review of AI in diagnostic imaging highlights that deep learning significantly reduces diagnostic errors, accelerates interpretation, and enables predictive analytics for early disease detection.

In radiology, about 90% of surveyed health systems reported at least partial deployment of AI tools for imaging by 2024, making it the most widely deployed clinical AI use case. Similar gains appear in cybersecurity, where Deep Instinct reports >99% zero day malware prevention with inference in under 20 milliseconds, 750× faster than typical ransomware encryption times. These quantifiable benefits justify sustained investment in deep learning models and platforms.

Market Restraints

Soaring compute, energy, and infrastructure costs

Despite strong demand, escalating compute and energy costs act as a structural restraint. Research indicates AI data centers are on track to consume around 2% of global electricity by 2025, raising both cost and sustainability concerns. The OECD notes that many countries have national AI strategies but lack robust plans for “AI compute capacity,” including GPUs, high bandwidth networks, and associated infrastructure, creating potential “compute divides” that limit diffusion of advanced deep learning systems. Enterprises face high upfront capital expenditure for specialized accelerators, networking, and cooling, while GPU shortages and long lead times can delay deployments. For smaller firms and public institutions, these barriers often slow adoption or confine them to narrow pilots rather than full scale production roll outs.

Regulatory complexity and trust deficits around high risk AI

Regulatory and ethical challenges also constrain market growth, especially in high risk applications such as healthcare, transportation, and biometrics. The EU AI Act defines “high risk AI systems” and imposes strict obligations around risk management, data quality, transparency, human oversight, and post market monitoring. Many deep learning systems for medical diagnosis, public space surveillance or credit scoring fall into these categories.

At the same time, McKinsey’s global AI survey shows that only around 21% of organizations with AI adoption had formal policies governing generative AI use in 2023, highlighting governance gaps that undermine trust. Complying with evolving regulations increases development time and costs, and uncertainty over future rules can delay investment decisions, particularly in regulated sectors and across borders.

Market Opportunities

Edge AI and industrial automation powered by deep learning

One of the most attractive opportunities lies at the intersection of deep learning and edge AI across manufacturing, robotics, and IoT. Demand for edge AI chips is projected to grow at about 40% CAGR, reaching roughly US$ 70 Billion by 2030, as devices such as drones, autonomous robots, and smart cameras embed local inference capabilities. Deep learning enables real time quality inspection, predictive maintenance, and autonomous navigation in factories and warehouses, reducing downtime and labor costs.

National AI strategies in countries such as China allocate tens of billions of yuan to “industrial AI modernization” and smart manufacturing initiatives, with industrial AI investment around ¥89 Billion (about US$ 12–13 Billion) in 2025 alone. Vendors that combine efficient deep learning models with optimized hardware (e.g., IPUs, FPGAs, ASICs) and toolchains for deployment on constrained devices are well positioned to capture high growth revenue pools in industrial and logistics verticals.

Generative and multimodal AI unlocking new value in retail, marketing, and customer experience

A second major opportunity arises from generative and multimodal deep learning models across retail, marketing, and customer interaction. McKinsey estimates that generative AI could unlock between US$ 390 Billion in annual value for the global retail sector alone, equivalent to an EBIT margin uplift of around 1.9 percentage points when combined with other AI and analytics. A 2023–2024 survey of retail and CPG executives commissioned by NVIDIA found that about 69% of respondents reported revenue increases attributable to AI, 72% saw operating cost reductions, and roughly 64% plan to expand AI infrastructure spending in the next 18 months; 86% aim to deploy generative AI to transform customer experiences.

Deep learning based computer vision platforms such as Clarifai already help retailers reduce bounce rates by about 12% and target a 2% uplift in revenue via better visual search and recommendations. Vendors that offer robust deep learning platforms for personalization, demand forecasting, and content generation can therefore tap rapidly growing budgets in retail, e commerce, and digital marketing.

Category-wise Insights

Offering Analysis

By offering, software currently leads the Deep Learning Market, supported by strong evidence that deep learning frameworks, platforms, and tools capture the largest share of value. Industry segmentation data indicate that software accounted for about 46.1% of global deep learning revenue in 2024, ahead of hardware and services. This dominance reflects the central role of frameworks such as TensorFlow, PyTorch, and Keras (all registered trademarks) and cloud-native AI platforms from Google, Microsoft, AWS, and IBM, which enable enterprises to design, train, and deploy neural networks at scale. Software layers abstract away hardware complexity, accelerate experimentation, and support MLOps, model monitoring, and security. At the same time, open-source ecosystems and managed services lower entry barriers for smaller firms and enable rapid reuse of pre-trained models. While hardware spending is surging, particularly for GPUs and specialized accelerators, software’s flexibility, recurring subscription models, and integration into broader digital platforms support its leading market share in the mix of offerings.

Application Analysis

By application, Image Recognition is the dominant segment in the Deep Learning Market. Multiple industry assessments suggest that image recognition captured roughly 43–43.5% of global deep learning revenue in 2024, significantly ahead of signal/voice recognition, video surveillance & diagnostics, and data mining applications. This leadership is underpinned by the rapid adoption of deep learning based computer vision across healthcare imaging, autonomous driving, retail analytics, and security. In medical imaging, deep learning has become the leading AI technology, delivering accuracies of around 98% for tasks such as tumor detection and COVID-19 classification, often surpassing radiologists in controlled studies.

End-User Analysis

By end -user, the Automotive sector holds the largest revenue share in the Deep Learning Market. Industry segmentation data indicate that automotive applications, spanning advanced driver assistance systems (ADAS), autonomous vehicles, in-cabin monitoring, and intelligent infotainment, account for nearly 39.6% of total deep learning demand in 2024. Autonomous vehicle and ADAS markets themselves are expanding rapidly; one forecast projects the autonomous vehicles market to add approximately US$ 624 Billion between 2024–2029, at a CAGR around 39.3%, with deep learning at the core of perception, path planning, and sensor fusion stacks.

Regional Insights

North America Deep Learning Market Trends

North America is currently the leading region in the Deep Learning Market, accounting for roughly 34% of global revenue in 2024 and expected to retain a dominant share through the forecast period. The region benefits from a dense concentration of AI hyperscalers (Google, Microsoft, AWS, Meta), leading chipmakers (NVIDIA, Intel, AMD), and top research universities, together creating a powerful innovation ecosystem for deep learning.

North American healthcare providers are early adopters: a survey of 43 health systems found that 90% had at least partially deployed AI in imaging and radiology by 2024, while other studies show healthcare organizations realizing returns of about US$ 3.20 for every US$ 1 invested in AI technologies. In retail, NVIDIA’s 2023–2024 surveys show that around 64% of large retailers plan to increase AI infrastructure investment, with 86% targeting generative AI to transform the customer experience.

Europe Deep Learning Market Trends

Europe represents a mature but heavily regulated Deep Learning Market, characterized by strong industrial, healthcare, and public-sector use cases alongside robust ethical and legal frameworks. While Europe’s absolute market share is smaller than North America’s and Asia’s, the region plays an outsized role in shaping AI governance via the EU AI Act, the first comprehensive horizontal legislation on AI worldwide.

The Act classifies many deep learning applications – such as medical diagnosis, critical infrastructure management, biometric identification, and credit scoring – as “high risk,” subjecting them to detailed obligations around risk management, training data quality, documentation, transparency, human oversight, and post-market monitoring. These rules will begin phasing in from 2026–2027, compelling providers and deployers to strengthen MLOps, model explainability, and auditing for deep learning systems.

Asia Pacific Deep Learning Market Trends

The Asia Pacific region is the fastest growing geography in the Deep Learning Market, driven by large-scale digitalization, massive data generation, and strong government support in China, Japan, South Korea, India, and ASEAN economies. Industry estimates suggest that Asia Pacific already accounts for more than a quarter of global deep learning revenue and is gaining share rapidly as domestic ecosystems scale.

China alone invested about ¥890 billion in AI in 2025, representing about 38% of global AI investment, with about 22% going to autonomous vehicles and 18% to computer vision. Government programs such as the National AI Development Plan and smart city initiatives allocate tens of billions of yuan to AI chips, intelligent computing centers, healthcare AI, and industrial automation, all of which heavily rely on deep learning.

Competitive Landscape

Market Structure Analysis

The Deep Learning Market exhibits a hybrid structure: highly concentrated in core hardware and cloud infrastructure, yet fragmented across application-level software and vertical solutions. On the hardware side, NVIDIA dominates data center and AI accelerators with an estimated 80–90% share of data center GPUs and discrete AI accelerators, supported by a rich software ecosystem (CUDA, cuDNN) and strong relationships with cloud providers. Competing chipmakers such as Intel, AMD, Qualcomm, Graphcore, Xilinx (now AMD), and specialized startups target niches in data center, edge, and vehicle compute with AI-optimized architectures. In cloud and platform services, Google, Microsoft, AWS, IBM, and Meta provide end-to-end deep learning stacks, integrating training, inference, data management, and MLOps.

Key Market Developments

- In June 2024, Deep Instinct publishes its fifth “Voice of SecOps” report, highlighting rising AI-powered cyber threats and demonstrating a deep learning based prevention platform with >99% zero day detection accuracy and sub-20 millisecond response times for unknown malware.

- In January 2024, NVIDIA releases its “State of AI in Retail and CPG” study; about 69% of surveyed retailers report revenue gains from AI, 72% report lower operating costs, and over 60% plan to increase AI infrastructure spending within 18 months, boosting demand for deep learning platforms.

- In January 2025, AWS and Deep Instinct announce integration of the DIANNA malware analysis assistant with Amazon Bedrock, combining generative AI with proprietary deep learning models to deliver real-time, explainable zero-day threat analysis for security operations teams.

Companies Covered in Deep Learning Market

- NVIDIA Corporation

- Intel Corporation

- General Vision

- Graphcore

- Xilinx

- Qualcomm Technologies, Inc.

- Google LLC

- Microsoft Corporation

- Amazon Web Services

- Sensory Inc.

- IBM Corporation

- Meta Platforms, Inc.

- Clarifai, Inc.

- Deep Instinct Ltd.

- Amazon.com, Inc.

Frequently Asked Questions

The global Deep Learning Market is projected to reach about US$ 306.3 Billion by 2033, up from approximately US$ 44.1 Billion in 2026 and about US$ 8.9 Billion in 2020, reflecting a robust forecast CAGR near 31.9% between 2026–2033.

Key demand drivers include rapid expansion of AI compute and GPUs, with AI chips valued around US$ 23.2 Billion in 2023 and growing above 30% CAGR, alongside strong adoption in high‑value use cases such as medical imaging, cybersecurity, and autonomous driving, where deep learning delivers 95–99%‑level accuracy and significant productivity gains.

Image Recognition is the leading application segment, accounting for roughly 43% of global deep learning revenue in 2024, supported by extensive use of computer vision in healthcare diagnostics, automotive perception, industrial inspection, security, and retail store analytics and loss prevention.

North America currently leads the Deep Learning Market, with an estimated 34% global revenue share, underpinned by hyperscaler investment, dominance in AI chips and data centers, and early adoption in sectors such as healthcare, retail, and autonomous vehicles.

A major opportunity lies in generative and multimodal deep learning across retail, marketing, software development, and knowledge work, where McKinsey projects US$ 240–390 Billion in annual value for retail alone, complemented by high‑growth edge AI deployments in industrial, robotics, and IoT environments.

Key players include hardware and platform leaders such as NVIDIA, Intel, AMD, Qualcomm, Graphcore, Xilinx, Google, Microsoft, AWS, IBM, and Meta Platforms, alongside specialized vendors like Clarifai, Deep Instinct, Sensory Inc., General Vision, and regional champions including Baidu, Tencent, Alibaba, Samsung Electronics, and Huawei.