- Biotechnology

- Autologous Cell Therapy Market

Autologous Cell Therapy Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Autologous Cell Therapy Market by Source (Autologous Cellular Immunotherapies, Autologous Stem Cell Therapy), Type (Bone Marrow, Epidermis, Mesenchymal stem cells, Haematopoietic stem cells, Chondrocytes, Others), Application (Cance, Neurodegenerative disorder, Cardiovascular disorder, Autoimmune disorder, Orthopedic, Wound healing, Others), End-user (Hospitals & Clinics, Ambulatory Centers, Academics & Research, Others), and Regional Analysis from 2026 to 2033

Autologous Cell Therapy Market Share and Trends Analysis

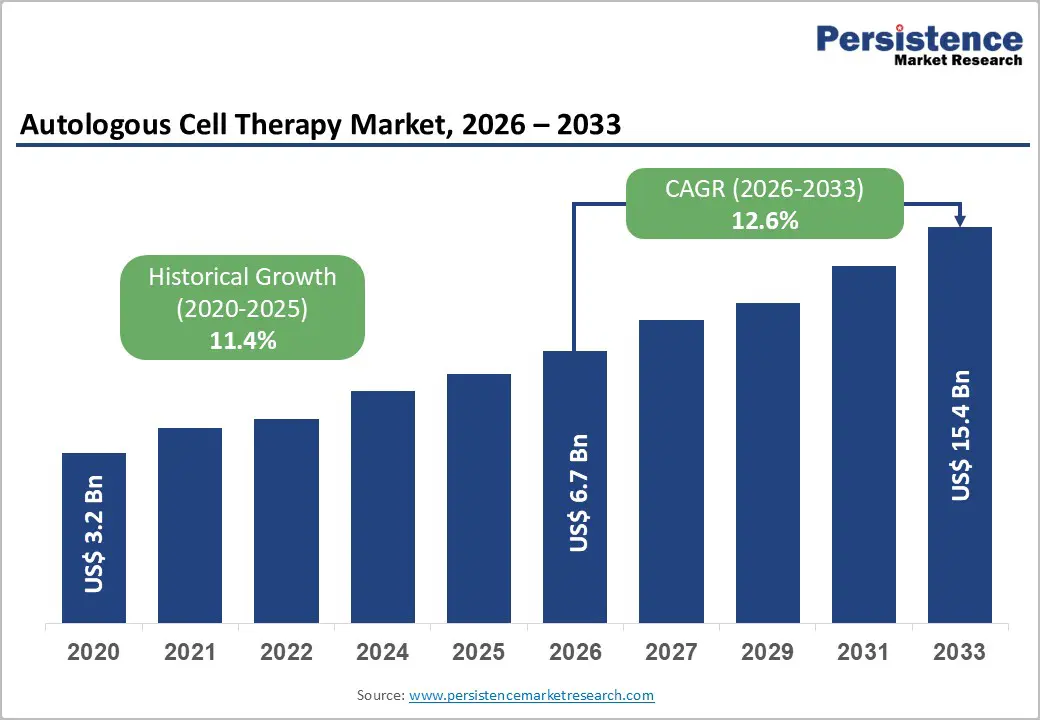

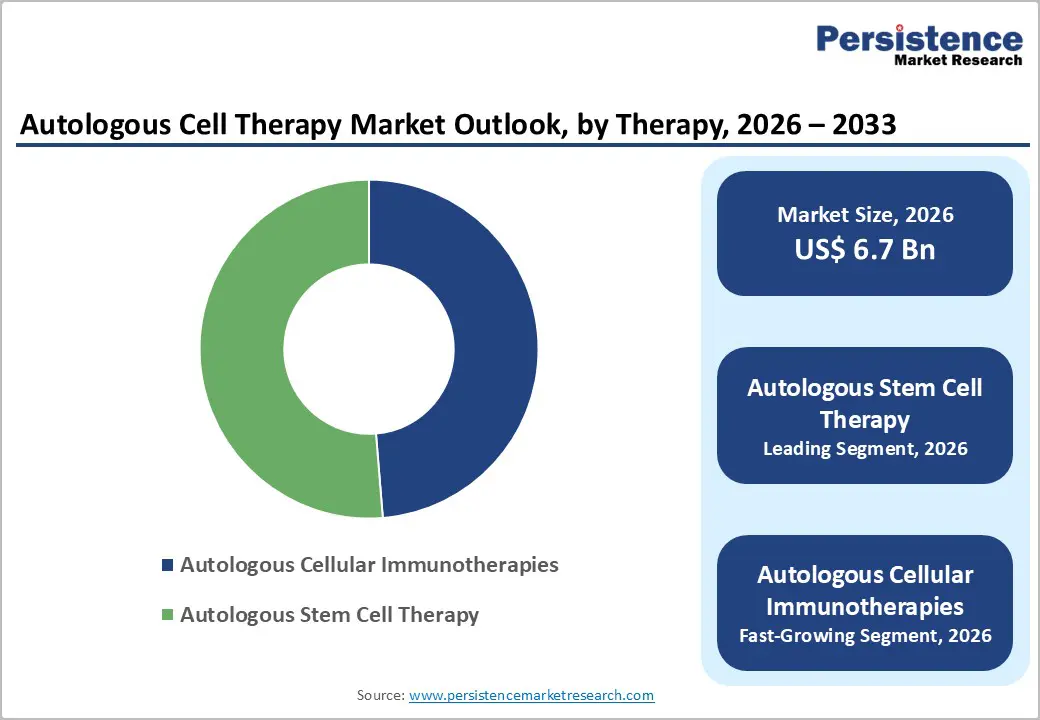

The global autologous cell therapy market is projected to reach US$6.7 billion in 2026 and increase to US$15.4 billion by 2033, with a CAGR of 12.6% over the forecast period.

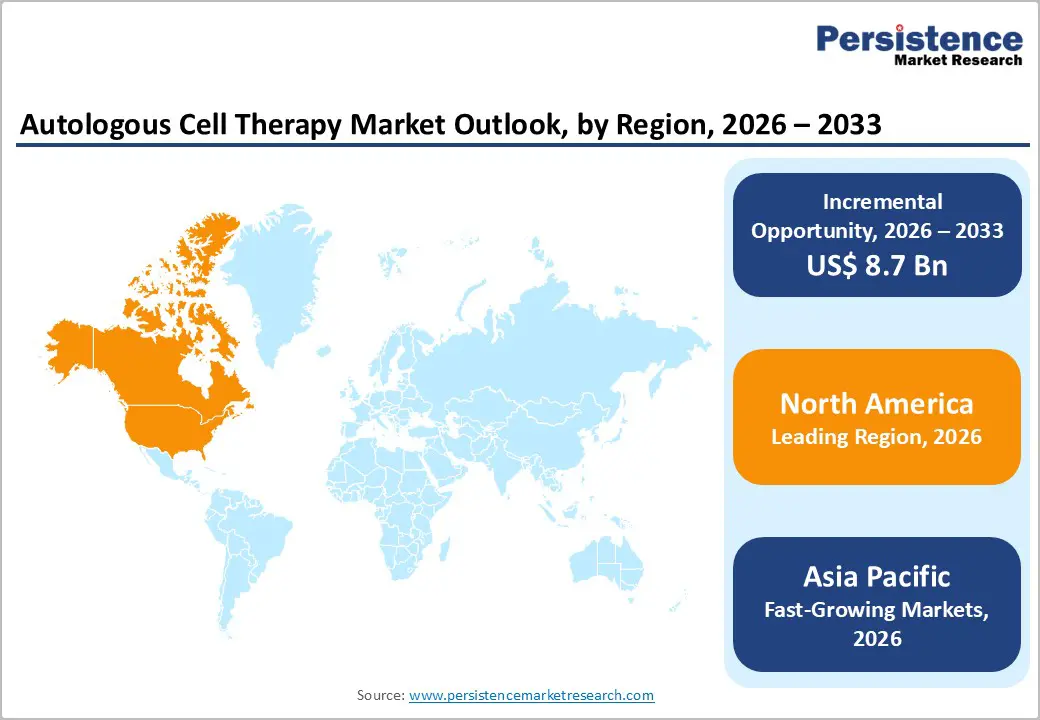

The autologous cell therapy market is growing rapidly, fueled by rising data security concerns, the digitization of health records, and demand for interoperability. North America leads in advanced healthcare IT infrastructure and early adoption, whereas Asia-Pacific is the fastest-growing market, driven by digital health initiatives, expanded healthcare access, and government-supported blockchain programs.

Key Industry Highlights:

- Dominant Segment: Autologous stem cell therapy dominated the Autologous cell therapy market in 2025, holding a 51.3% share due to its broad applications in regenerative medicine, tissue repair, and personalized treatment strategies. High adoption in orthopedic, cardiovascular, and hematological disorders, coupled with increasing clinical approvals and supportive research, drove widespread use across hospitals, specialty clinics, and biotech companies.

- Dominant Region: North America led the market in 2025, with a 55.1% share, supported by advanced healthcare infrastructure, early adoption of autologous therapies, and robust regulatory frameworks. Asia-Pacific emerged as the fastest-growing region due to expanding healthcare access, rising cancer incidence, and increasing government-backed regenerative medicine programs.

- Growth Indicator: Growth is driven by the rising prevalence of blood cancers, demand for personalized medicine, increasing clinical trial activity, advances in cell-processing technologies, and rising investments in autologous therapy development.

- Market Opportunity: Key opportunities include the expansion of CAR-T and MSC therapies, the development of all-in-one automated cell-processing systems, adoption in emerging healthcare markets, partnerships with pharmaceutical companies, and integration with telemedicine and digital health platforms.

| Key Insights | Details |

|---|---|

| Autologous Cell Therapy Market Size (2026E | US$ 6.7 Bn |

| Market Value Forecast (2033F) | US$ 15.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.4% |

Market Dynamics

Driver - Rising prevalence of blood cancers and chronic diseases

The autologous cell therapy market is strongly driven by the rising prevalence of blood cancers, which fuels demand for personalized treatments such as autologous approaches that leverage a patient’s own cells. In 2025, an estimated 187,740 new cases of leukemia, lymphoma, and myeloma are expected in the United States alone, representing 9.4 percent of all new cancer cases in the country, and globally over 1.39%. million blood cancer diagnoses are projected with 745,000 deaths from the three major types, underscoring a substantial therapeutic burden. This persistent and increasing incidence underscores the need for advanced cell therapies to improve outcomes in hematologic malignancies.

Similarly, chronic noncommunicable diseases (NCDs), including cancers, cardiovascular diseases, diabetes, and respiratory illnesses, account for approximately 71% of all deaths globally and represent a major long-term health challenge, increasing the pool of patients who may benefit from regenerative and personalized autologous cell therapies. The rising prevalence of chronic conditions elevates demand for innovative treatments that can manage complex, long-term disease processes more effectively than traditional modalities. Collectively, these disease burdens strengthen the case for the expanded adoption of autologous cell therapy.

Restraints - Complex manufacturing and logistical challenges

The autologous cell therapy market faces significant complex manufacturing challenges because each therapy batch is made for an individual patient, creating a “batch-of-one” production model with limited economies of scale. Autologous processes may require a bioreactor for approximately 14 days to produce a single therapy, limiting throughput and necessitating multiple reactors and highly trained staff to meet demand. The need to maintain strict quality standards and Good Manufacturing Practices (GMP) across every patient-specific lot increases costs and complexity compared with traditional pharmaceuticals. Moreover, variability in patient-derived starting material and multiple manual processing steps heighten the risk of product failure, complicating consistent commercial-scale production.

Logistical challenges further restrain the market because autologous cell therapies require sensitive cold-chain transport between collection sites, manufacturing facilities, and clinical centers within narrow time windows, often 40-50 hours or less, to maintain cell viability. Specialized cryogenic conditions and strict chain-of-identity protocols are essential to prevent errors and maintain patient safety, but these requirements strain existing pharmaceutical logistics infrastructure, which was not designed for individualized therapies. Limited infrastructure, temperature excursions that can reduce cell viability, and workforce shortages in specialized handling add substantial costs and risks to the delivery of autologous treatments.

Opportunity - Expansion of CAR-T and MSC therapies into new indications

The autologous cell therapy market benefits from the expanding use of CAR-T cell therapies in new indications, particularly beyond traditional blood cancers to broader patient populations. As of April 2024, approximately 1,580 CAR-T clinical trials are registered on ClinicalTrials.gov, with nearly 25% exploring solid tumor applications in addition to hematologic malignancies, indicating a widening of clinical interest and therapeutic scope. CAR-T products such as tisagenlecleucel (Kymriah) and axicabtagene ciloleucel (Yescarta) have already improved outcomes in conditions such as diffuse large B-cell lymphoma and acute lymphoblastic leukemia, providing a foundation for further expansion of indications.

Similarly, mesenchymal stem cell (MSC) therapies present substantial opportunity because they are being investigated across a broad range of immune and inflammatory diseases. The U.S. National Institutes of Health registry lists hundreds of MSC studies exploring safety and efficacy for conditions ranging from graft rejection to autoimmune disorders and inflammatory diseases, indicating a diversification of applications beyond traditional regenerative medicine uses. This increased clinical research interest in MSCs for systemic and chronic conditions can significantly expand the adoption of autologous stem cell therapy.

Category-wise Analysis

By Therapy Insights

Autologous stem cell therapy accounts for 51.3% of the global market in 2025, as it remains the most widely performed personalized cellular therapy worldwide, particularly in hematologic and regenerative applications. For example, autologous hematopoietic stem cell transplantation (auto-HSCT) continues to account for the majority of stem cell transplants worldwide; despite CAR-T growth, reports show hundreds of auto-HSCT procedures per center compared with smaller absolute numbers of CAR-T infusions, with one survey finding autologous cell collections (HSCT) of 341-400 annually versus 24-111 CAR-T infusions from 2018-2023, underscoring sustained use of stem cell therapy in clinical practice. This long-standing clinical foundation, established safety profile, and broad applicability across oncology, orthopedics, and autoimmune conditions anchor autologous stem cell therapy’s dominant position within the market’s therapy mix.

By Source Insights

Bone marrow-derived autologous therapies hold a dominant position within the autologous cell therapy market because bone marrow remains the most established and widely used source of stem cells for clinical transplantation, particularly in hematologic disorders. In Europe in 2022, 58.8% of all hematopoietic cell transplants were autologous, compared with allogeneic procedures, highlighting the prevalence of patient-derived bone marrow use in therapeutic practice. Autologous transplantation of bone marrow or peripheral blood stem cells is a standard treatment for lymphoid malignancies and multiple myeloma, with tens of thousands of procedures performed at major transplant centers each year. Autologous bone marrow therapies are supported by extensive clinical experience, established protocols, and documented survival benefits, which reinforce their dominant role in application.

Regional Insights

North America Autologous Cell Therapy Market Trends

North America dominates the autologous cell therapy market with 55.1% share in 2025, due to its advanced healthcare and research ecosystem, strong regulatory support, and concentration of clinical activity. The United States alone has administered over 22,000 CAR-T cell infusions since 2017, with more than 150-200 designated treatment centers, illustrating extensive real-world adoption of autologous therapies. FDA frameworks like the Regenerative Medicine Advanced Therapy (RMAT) designation accelerate the development and approvals of novel cell therapies, fostering innovation. ClinicalTrials.gov data indicate that North America hosts a significant portion of active cell and gene therapy trials, reflecting robust R&D investment and infrastructure. This combination of clinical adoption, regulatory facilitation, and research intensity positions North America at the forefront of the global autologous cell therapy market.

Europe Autologous Cell Therapy Market Trends

Europe is a key region in the autologous cell therapy market owing to its well-structured regulatory framework and substantial clinical activity. The European Union regulates cell-based therapies, including autologous products, under the Advanced Therapy Medicinal Products (ATMP) Regulation, with centralized marketing authorisation and expert evaluation by the European Medicines Agency’s Committee for Advanced Therapies, enabling broader access across member states. Clinical data reinforce Europe’s role: in 2022, 46,143 hematopoietic cell transplants were reported across 689 centers, with 27,132 (58.8%) autologous procedures, and over 4,300 advanced cellular therapies, including CAR-T, highlighting substantial clinical integration. Robust public funding, research infrastructure, and adoption of novel therapies further position Europe as an important market for autologous cell therapy development and delivery.

Asia-Pacific Autologous Cell Therapy Market Trends

Asia-Pacific’s rapid growth in the autologous cell therapy market is driven by its expanding clinical research ecosystem, large patient populations, and supportive regulatory environments. The region now accounts for a significant share of global cell and gene therapy clinical trials, with approximately 44 percent conducted in the Asia-Pacific region, led by China, Japan, and South Korea. China alone accounts for approximately 60% of global CAR-T trials, reflecting strong local innovation and trial activity. Additionally, governments across the region have increased funding, such as Japan’s over USD 1 billion investment in regenerative medicine research and streamlined regulatory pathways, accelerating the development, clinical adoption, and commercialization of autologous cell therapies.

Competitive Landscape

The competitive landscape in the autologous cell therapy market is defined by leading biopharma developers (Novartis, Bristol Myers Squibb, Autolus), regenerative specialists (Vericel, Caladrius), and contract manufacturing partners (Lonza, Catalent, Sartorius). Innovation in CAR-T, MSC, and automated manufacturing, strategic alliances, and expansion into new indications intensify competition and drive differentiation.

Key Industry Developments:

- In December 2025, Bristol Myers Squibb announced that the U.S. FDA approved Breyanzi (lisocabtagene maraleucel) as the first and only CAR-T cell therapy for adults with relapsed or refractory marginal zone lymphoma (MZL). The approval expanded Breyanzi’s indication based on clinical data demonstrating durable responses in heavily pretreated patients, strengthening the company’s CAR-T portfolio in hematologic malignancies.

- In August 2025, Excellos, Lonza, and Akadeum Life Sciences announced a collaboration to advance cell therapy manufacturing by improving the quality of starting materials. The partnership focused on integrating advanced cell processing, enrichment, and analytical technologies to enhance consistency, efficiency, and scalability in cell therapy production, supporting more reliable manufacturing outcomes for clinical and commercial applications.

Companies Covered in Autologous Cell Therapy Market

- BrainStorm Cell Therapeutics

- Holostem Terapie Avanzate S.R.L

- Pharmicell Co. Inc

- Opexa Therapeutics

- Lonza

- Bristol Myers Squibb

- Tego Science

- Corning Incorporated

- Bio Elpida

- Novartis

- Autolus therapeutics

- Vericel Corporation

- Catalent, Inc

- Sartorius AG

- Caladrius Biosciences Inc

- U.S. Stem Cell Inc

- Others

Frequently Asked Questions

The global autologous cell therapy market is projected to be valued at US$ 6.7 Bn in 2026.

Rising blood cancer incidence, demand for personalized therapies, clinical success of CAR-T, and advances in cell processing technologies.

The global autologous cell therapy market is poised to witness a CAGR of 12.6% between 2026 and 2033.

Expansion of CAR-T and MSC therapies, new indications, automated manufacturing, emerging markets, supportive regulatory pathways.

BrainStorm Cell Therapeutics, Holostem Terapie Avanzate S.R.L, Pharmicell Co. Inc, Opexa Therapeutics, Lonza, Bristol Myers Squibb.