- Specialty & Fine Chemicals

- Acrylates Copolymer Market

Acrylates Copolymer Market Size, Share and Growth Forecast, 2026 - 2033

Acrylates Copolymer Market by Application (Paints & Coatings, Adhesives & Sealants, Personal Care & Cosmetics), Product Type (Ethyl Acrylate Copolymers, Butyl Acrylate Copolymers, Styrene-Acrylate Copolymers), Product Form (Powder, Emulsion, Liquid, Beads), and Regional Analysis for 2026 - 2033

Acrylates Copolymer Market Share and Trends Analysis

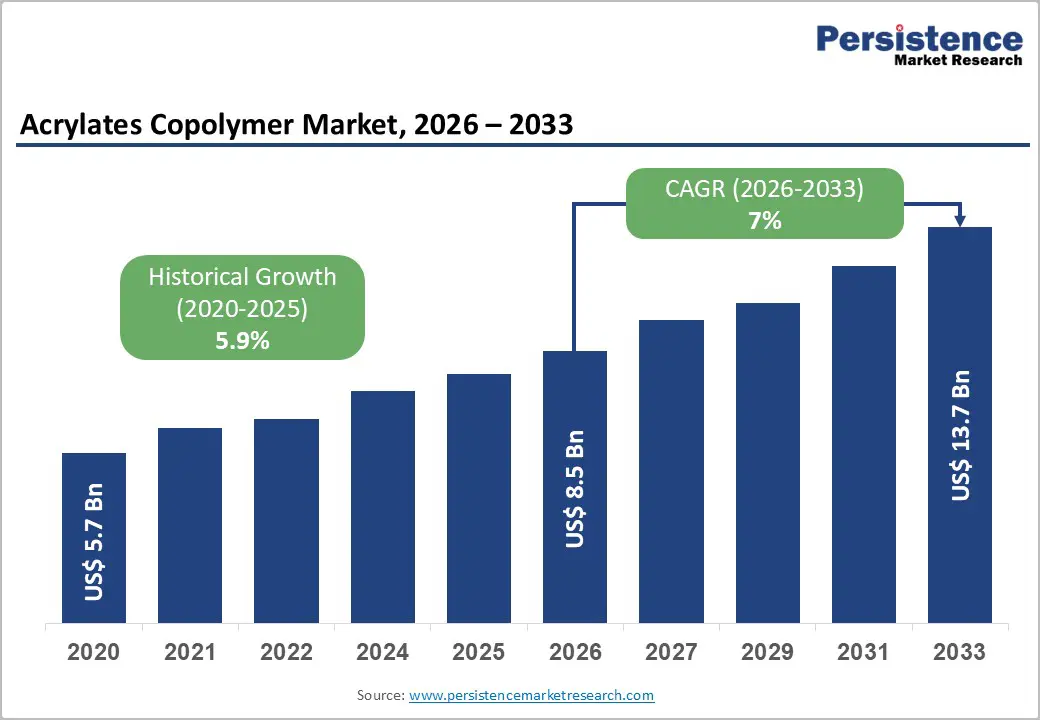

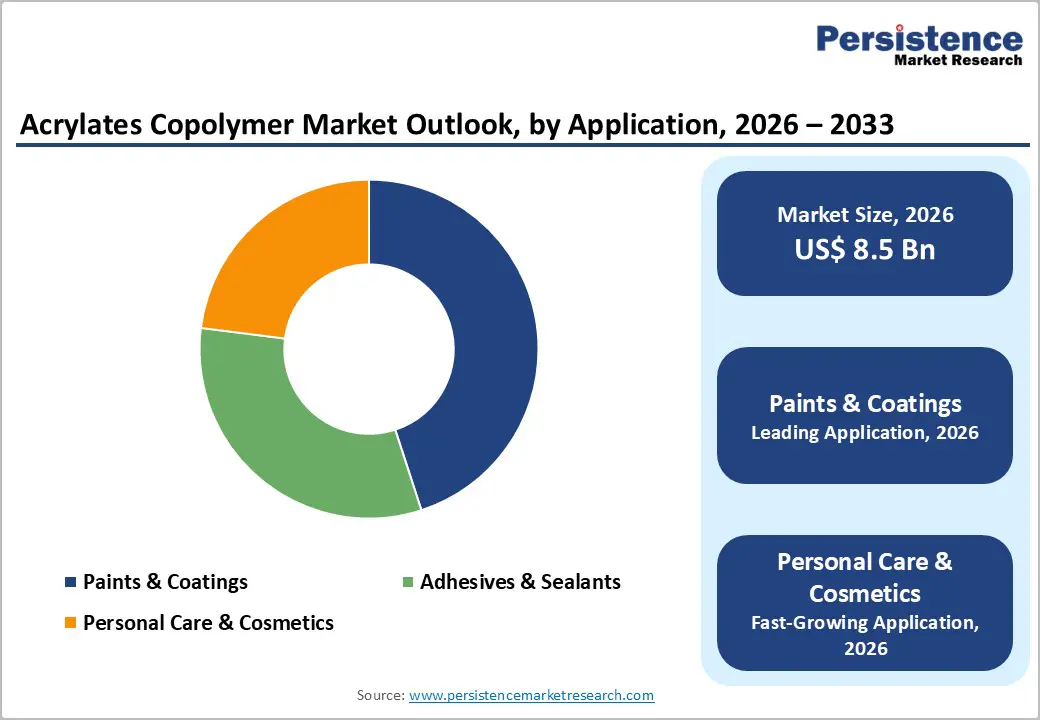

The global acrylates copolymer market size is likely to be valued at US$ 8.5 billion in 2026, and is projected to reach US$ 13.7 billion by 2033, growing at a CAGR of 7% during the forecast period 2026–2033. The expansion of the market is primarily driven by rising adoption across paints & coatings, adhesives & sealants, and personal care & cosmetics segments. These applications leverage the polymers’ superior adhesion, flexibility, film-forming ability, and chemical resistance, making them essential for both industrial and consumer products.

Macroeconomic factors, including rapid urbanization, industrial manufacturing growth, and increased infrastructure development, are significantly boosting polymer demand, especially in Asia Pacific and North America. Growing regulatory pressure on low-volatile organic compound (VOC) and environmentally friendly formulations is accelerating the transition to water-based acrylates copolymer systems, promoting sustainability and compliance in end-use industries.

Key Industry Highlights

- Dominant Applications: Paints & coatings are set to command around 45% revenue share in 2026, while personal care & cosmetics are likely to grow the fastest at about 9.2% CAGR through 2033, driven by multifunctional formulation trends.

- Leading Product Types: Ethyl acrylate copolymers are expected to lead with approximately 40% market share in 2026, while butyl acrylate copolymers are projected as the fastest-growing during 2026–2033, reflecting rising demand for flexible packaging.

- Dominant Product Form: Emulsion formulations are anticipated to hold the largest revenue share at 42% in 2026, while liquid acrylates are set to be the fastest-growing form from 2026 to 2033, driven by industrial processing efficiencies.

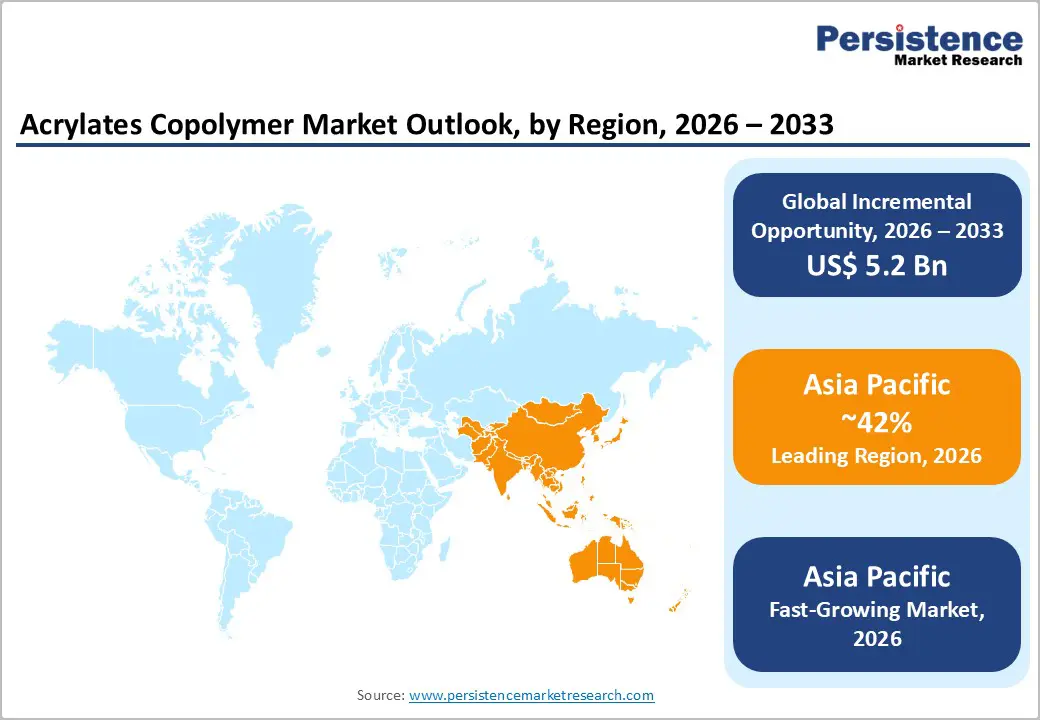

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 42% revenue share in 2026 and register around 7.5% CAGR through 2033, led by infrastructure growth and industrial expansion China, India, and ASEAN.

- Competitive Environment: Competitive dynamics include sustainable product launches, bio-based monomer innovations, strategic capacity expansions, and technology collaborations.

| Key Insights | Details |

|---|---|

|

Acrylates Copolymer Market Size (2026E) |

US$ 8.5 Bn |

|

Market Value Forecast (2033F) |

US$ 13.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

DRO Analysis

Rising Demand in Paints & Coatings and Industrial Applications

The paints & coatings segment continues to be a core driver for acrylates copolymer consumption, as real-world market activity demonstrates strong product demand. The Sherwin-Williams Company reported robust sales growth in protective, marine, commercial, and residential coatings in late 2025, driven by rebounds in U.S. home sales and renovation activity, reflecting heightened demand for high-performance coatings. Acrylic technologies, which frequently incorporate acrylates copolymers for film formation, weather resistance, and low-VOC performance, are central across these sub-segments.

In addition, recent mega-merger activity in the coatings sector, such as the proposed US$ 25 billion combination of AkzoNobel and Axalta, underscores the strategic importance of coatings portfolios to industry growth and future innovation. This consolidation signals confidence in long-term demand and expands capacity for advanced coatings formulations. Simultaneously, new downstream manufacturing capacity for acrylic intermediates, such as India’s inauguration of a large acrylic acid and butyl acrylate plant in Gujarat, highlights upstream supply strengthening that supports broader regional industrial growth.

Personal Care Expansion and Shift toward Eco-Friendly Polymer Formulations

The personal care and cosmetics sector is increasingly prioritising product sustainability alongside performance, shaping acrylates copolymer use in film-forming and stabilizing applications. Regulatory momentum, such as the European Union (EU)’s microplastics restriction under Regulation (EU) 2023/2055, which phases out intentionally added microplastics across cosmetics categories, is forcing industry reformulation strategies and prompting innovation toward biodegradable and compliant ingredients. This regulatory backdrop is influencing global personal care brands to rethink polymer use in formulations well ahead of compliance deadlines.

The consumer demand for sustainable, eco-friendly beauty products is accelerating, as evidenced by insights from industry reporting showing strong preference for biodegradable solutions among major consumer groups in the U.S. and Europe. This trend is reinforced by data showing that tighter ingredient transparency and environmental expectations are key purchase drivers. Combined regulatory pressure and shifting consumer behaviour are incentivising manufacturers to innovate formulations that balance high performance with sustainability, thereby expanding the role of compliant polymers in personal care product lines.

Volatility in Raw Material Pricing

Polymers derived from key acrylic monomers, such as acrylic acid, ethyl acrylate, and butyl acrylate, remain highly sensitive to feedstock price fluctuations, which are closely tied to broader petrochemical and energy market dynamics. This volatility directly impacts downstream producers, with approximately 35% of manufacturers reporting raw material cost swings as a major margin pressure point, constraining production scalability and elongating contract pricing negotiations. Price instability also complicates budgeting for end users in cost-sensitive sectors such as construction, industrial coatings, and packaging, affecting project timelines and supplier negotiations.

In early 2026, acrylic acid prices surged over 86% in parts of East China due to geopolitical tensions and supply disruptions, intensifying input cost pressures on polymer producers. Major chemical producers, including BASF, responded by raising prices for critical acrylic intermediates, citing persistent cost inflation across logistics, energy, and regulatory compliance pathways. These price shocks increase budget uncertainty for both producers and buyers, constraining expansion in price-sensitive applications and requiring careful supply chain management.

Regulatory Complexity and Product Compliance Challenges

While eco-friendly polymer formulations present growth potential, they also increase regulatory complexity for product compliance and market access, especially in multi-jurisdictional environments. Compliance with frameworks such as the EU’s REACH regulation and the Toxic Substances Control Act (TSCA) of the U.S. involves extensive documentation, hazard assessment, registration efforts, and ongoing monitoring, adding significant time and expense to product introductions. Smaller and emerging manufacturers without dedicated regulatory teams often face hurdles, including delayed launches, increased costs, and potential market exclusion.

The European Commission proposed a major REACH reform, described as one of the most significant updates in recent years, eliciting concern from industry groups about increased compliance burdens. The Candidate List for Substances of Very High Concern maintained by ECHA has also been expanded, adding regulatory obligations for chemicals used in coatings, adhesives, and polymers. These regulatory developments intensify administrative complexity, slow new product launches, and require significant investment in compliance infrastructure, reinforcing regulatory barriers as a structural restraint in the acrylates copolymer market.

Rapid Industrialization in Developing Economies

Economic expansion and large-scale infrastructure development in emerging regions are creating strong demand for acrylates copolymer-enhanced coatings, adhesives, and sealants. In India’s Union Budget 2026–27, the government allocated support for Chemical Parks and Plastic Parks, offering grants of up to 50% of project costs to attract investment and expand polymer manufacturing infrastructure. This policy direction strengthens local chemical ecosystems, broadens access to raw materials, and encourages domestic manufacturing of value-added polymer products.

The extended producer responsibility (EPR) regulations taking effect in India in 2026 mandate producers to manage packaging waste, prompting manufacturers to innovate with recyclable and high-performance polymers. With urbanization rising and industrial output expanding across ASEAN and Latin America, these combined policy initiatives are expanding industrial polymer demand. Regional trade agreements and cross-border production incentives further amplify growth potential, while foreign direct investment (FDI) in the chemical and manufacturing sectors strengthens supply chain integration, creating a robust environment for acrylates copolymer suppliers.

Innovation in Performance and Sustainable Polymer Solutions

Government incentives and legislative action in 2025–2026 are accelerating innovation in high-performance and sustainable polymers. The U.S. Renewable Chemicals Act of 2025 introduced tax credits for renewable chemicals and biopolymer production, including eco-friendly polymer technologies, to enhance domestic manufacturing competitiveness. These incentives lower production costs for sustainable acrylates and encourage R&D investments in next-generation materials for coatings, adhesives, and personal care applications.

In parallel, the U.S. Department of Energy (DOE) committed over US$ 27 million to advanced plastics recycling and design-for-recyclability projects, supporting innovation in circular and sustainable polymer technologies. Legislative discussions around TSCA modernization also aim to streamline chemical approvals, enabling faster commercialization of eco-friendly polymers. These policy and funding developments collectively create a strong innovation ecosystem, allowing manufacturers to differentiate products, capture premium markets, and accelerate the adoption of high-value sustainable acrylates copolymer solutions across multiple industries.

Category-wise Analysis

Application Insights

Paints & coatings is slated to remain the leading application in 2026, with an approximate 45% of the acrylates copolymer market revenue share, driven by use in architectural, automotive, and industrial coatings requiring durability, flexibility, and environmental resistance. Verified 2025 reports highlight a shift toward low-VOC and water-based coatings to meet U.S. and EU environmental mandates. Within this segment, eco-friendly high-performance protective coatings are the fastest-growing, as showcased at the 2025 European Coatings Show, where advanced water-based acrylic copolymers demonstrated superior durability and chemical resistance, reflecting rising adoption aligned with sustainability and regulatory compliance, and strong CAGR potential through 2033.

The personal care & cosmetics segment is projected to grow at an estimated CAGR of 9.2% through 2033, as acrylates copolymers enhance film-forming, water-resistant, and stabilizing properties in hair, skincare, and long-wear makeup products. Verified 2025 insights show a shift toward biobased and biodegradable polymer alternatives, aligning with consumer and regulatory demands for sustainable formulations. Within this category, sustainable and multifunctional cosmetics polymers are the fastest-growing, driven by ingredient safety regulations such as per- and polyfluoroalkyl substances (PFAS) bans and transparency mandates in the U.S. and EU, prompting brands to reformulate with high-performance copolymers that combine compliance with product efficacy.

Product Type Insights

Ethyl acrylate copolymers are projected to remain the largest product type in 2026, accounting for roughly 40% revenue share due to their versatile performance across coatings, adhesives, and sealants. Verified 2025 reports highlight stable supply chains and ongoing adoption in architectural and automotive coatings, where water-based emulsions and low-VOC formulations are increasingly used to meet U.S. and EU environmental mandates while maintaining durability. These copolymers provide a balanced combination of adhesion, flexibility, and weather resistance, supporting industrial and institutional applications. Growing demand for protective and decorative coatings, coupled with manufacturers’ shift toward environmentally compliant polymers, reinforces ethyl acrylate’s dominant position in multiple end-use sectors.

Butyl acrylate copolymers are anticipated to be the fastest-growing product type with a CAGR of 9.5%, driven by expanding use in pressure-sensitive adhesives, flexible packaging, and specialty sealants. Verified 2025 developments show manufacturers investing in eco-friendly feedstocks, sustainable polymerization processes, and low-VOC formulations to meet both regulatory requirements and consumer demand for green products. Their compatibility with water-based and solvent-based systems enhances adoption across industrial, packaging, and consumer applications. Rising demand in high-performance adhesives for electronics, automotive, and flexible packaging applications underscores the growth potential. Continued R&D into enhanced adhesion, flexibility, and durability further positions butyl acrylate copolymers as a critical growth driver in the global market through 2033.

Regional Insights

North America Acrylates Copolymer Market Trends

North America, led by the U.S., is a high-growth market for acrylates copolymers, driven by strong industrial and manufacturing demand in coatings, adhesives, and personal care. In 2025, the U.S. Environmental Protection Agency (EPA) finalized amendments to the National VOC Emission Standards for aerosol coatings, prompting a shift toward low-VOC, water-based polymer systems that meet regulatory and air quality standards. Verified examples show PPG Industries expanding low-VOC architectural coating portfolios to comply with these mandates while addressing rising sustainability expectations, reinforcing adoption across industrial and consumer applications.

The region’s growth is also fueled by robust R&D and strategic partnerships targeting sustainable and high-performance polymer solutions. U.S. polymer science clusters are advancing binder and resin technologies that improve durability and reduce emissions under EPA and TSCA guidelines. Collaborations between specialty chemical firms and original equipment manufacturers (OEMs) are accelerating commercialization of next-generation acrylates, positioning North America as a hub for environmentally compliant, high-performance polymer innovation through 2033.

Europe Acrylates Copolymer Market Trends

Europe holds a significant portion of the acrylates copolymer market share, driven by strict environmental regulations and sustainability mandates across construction, automotive, and personal care sectors. Key markets such as Germany, France, and the U.K. are adopting low-VOC, water-based coatings and adhesives to meet EU environmental and consumer safety requirements. Verified 2025 examples highlight updates to EU Cosmetics Regulation and chemical labeling rules, prompting formulators to innovate eco-friendly polymer solutions while ensuring compliance. These regulatory drivers encourage adoption of advanced acrylic and acrylate copolymers across industrial and consumer applications.

Growth is further supported by investments in sustainable polymer technologies and green chemistry initiatives. In 2025, European coatings manufacturers expanded production of bio-based and waterborne acrylic copolymers, aligning with EU sustainability targets. Strategic product launches and consolidation activities are reinforcing competitive positioning, with innovation focused on combining performance with environmental compliance. These developments are expected to sustain steady market growth through 2033 while promoting safer, eco-friendly polymer portfolios.

Asia Pacific Acrylates Copolymer Market Trends

Asia Pacific is expected to be the largest regional market for acrylates copolymer, capturing a share of roughly 42% in 2026, owing to rapid industrialization, infrastructure expansion, and growing automotive and personal care industries. Verified 2025 developments show strong adoption of low-VOC and high-performance coatings in China, India, and ASEAN countries, supported by urban housing projects and industrial growth. Leading manufacturers, including Nippon Paint and Asian Paints, scaled production of compliant acrylic copolymers to meet environmental standards while addressing increasing industrial and consumer demand.

The region’s fastest-growing subsegments include specialty coatings and pressure-sensitive adhesives for automotive, electronics, and packaging applications. The reports highlight regional manufacturers introducing water-based and antimicrobial coatings to satisfy sustainability requirements. Cost-competitive production, supportive government policies, and harmonized VOC regulations across Asia Pacific countries continue to reinforce the region’s leadership position and strong growth trajectory through 2033, making it a key driver of global acrylates copolymer demand.

Competitive Landscape

The global acrylates copolymer market structure is moderately consolidated, with leading chemical companies—including Dow, BASF, Arkema, Evonik, and Nippon Shokubai, together controlling over 50% of the market share. These established players leverage extensive customer relationships across coatings, adhesives, and personal care industries, while investing heavily in R&D for high-performance, low-VOC, and sustainable polymer formulations. Their integrated production capabilities and global distribution networks provide strong competitive advantages in meeting regional regulatory and environmental standards.

Regional and specialty manufacturers, such as Synthomer and Allnex, focus on niche applications or high-growth geographies, offering customized solutions for industrial coatings, adhesives, and multifunctional personal care products. Barriers such as raw material cost volatility, regulatory compliance, and technological complexity limit new entrants, but innovation in water-based, bio-based, and eco-friendly polymer systems enables smaller firms to participate. Market consolidation is expected to continue gradually, with leading players pursuing acquisitions, joint ventures, and partnerships to expand geographically and strengthen sustainable product portfolios.

Key Industry Developments

- In January 2026, researchers from Hebei University of Science and Technology developed a UV-induced peelable adhesive using castor oil-based urethane acrylate and modified acrylic copolymers, significantly improving peeling performance for semiconductor wafer dicing. The formulation enables strong adhesion with controlled debonding via UV-triggered crosslinking, enhancing process reliability and efficiency in advanced electronics manufacturing.

- In December 2025, Arkema announced plans to divest parts of its plastic additives business, including impact modifiers and processing aids, to Praana Group as part of a portfolio shift toward higher-value specialty materials. The divestment, covering select global and regional operations and a Netherlands facility, generated € 44 million in 2024 sales and is expected to close in Q1 2026.

- In October 2025, BASF sold a majority stake in its coatings unit, including automotive OEM and surface treatments, to Carlyle Group and Qatar Investment Authority for €7.7 billion while retaining a 40% stake. This strategic move provided BASF with ~€5.8 billion in pre-tax proceeds, enabling reinvestment into high-growth polymer segments and strengthening its balance sheet.

Companies Covered in Acrylates Copolymer Market

- BASF SE

- Dow Inc.

- Arkema Group

- Evonik Industries AG

- Nippon Shokubai

- Mitsubishi Chemical

- LG Chem

- Lubrizol Corporation

- DIC Corporation

- Allnex

- Formosa Plastics

- Synthomer plc

- Sasol Limited

- Nouryon

Frequently Asked Questions

The global acrylates copolymer market is projected to reach US$ 8.5 billion in 2026.

Rising demand in paints & coatings, adhesives, and personal care segments, coupled with regulatory shifts toward low-VOC and eco-friendly formulations, is driving the market.

The market is poised to witness a CAGR of 7% from 2026 to 2033.

Expansion in emerging industrial markets and innovation in high-performance, sustainable copolymer formulations are unlocking high-value opportunities.

Dow, BASF, Arkema, Evonik, and Nippon Shokubai are some of the leading companies in the market.