- Chipsets & Processors

- Wireless Charging Market

Wireless Charging Market Size, Share, and Growth Forecast 2026 - 2033

Wireless Charging Market by Charging Method (Charging Mat, Charging Stand, Charging Pads, Charging Stations), Technology (Inductive Charging, Resonant Charging, Radio Frequency Charging, Other), Power Range (Low, Medium, High), Charging Standard, End-use, and Regional Analysis for 2026-2033

Wireless Charging Market Size and Trend Analysis

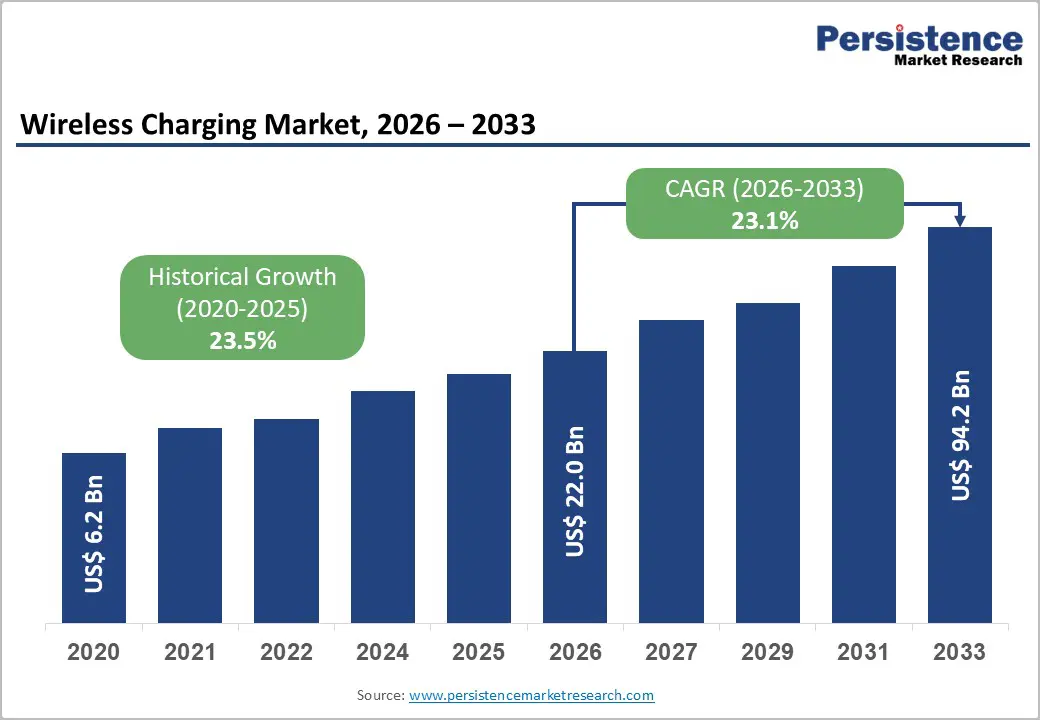

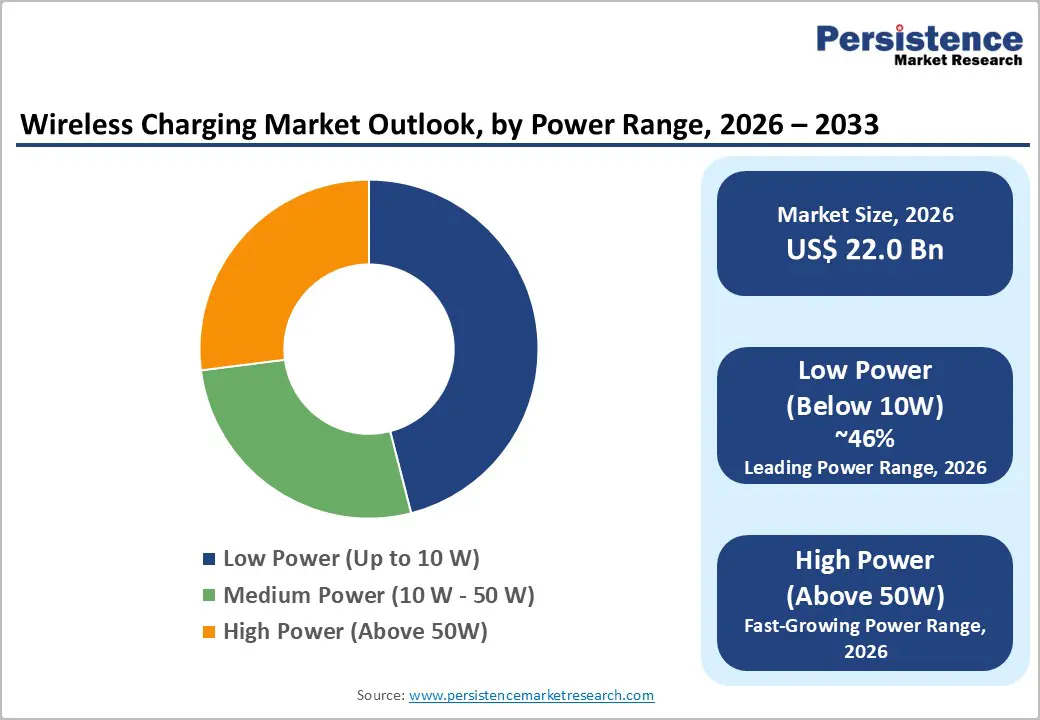

The global wireless charging market size is supposed to be valued at US$ 22.0 Bn in 2026 and is projected to reach US$ 94.2 Bn by 2033, growing at a CAGR of 23.1% between 2026 and 2033.

The market's transformation is evidenced by the adoption of Qi2 technology, which has achieved 1,200 new certified products in 2025 alone, demonstrating a 6-fold faster adoption rate compared to its predecessor. With smartphone penetration reaching critical mass, 88% of Qi2 users reporting satisfaction with wireless charging performance, and electric vehicle adoption surpassing 17 million units globally in 2024, the market is transitioning from a convenience feature to essential infrastructure across consumer electronics and mobility sectors. Strategic investments by major technology players, coupled with government incentives for sustainable transportation infrastructure, are positioning wireless charging as a foundational technology for the next decade of connected device ecosystems.

Key Market Highlights

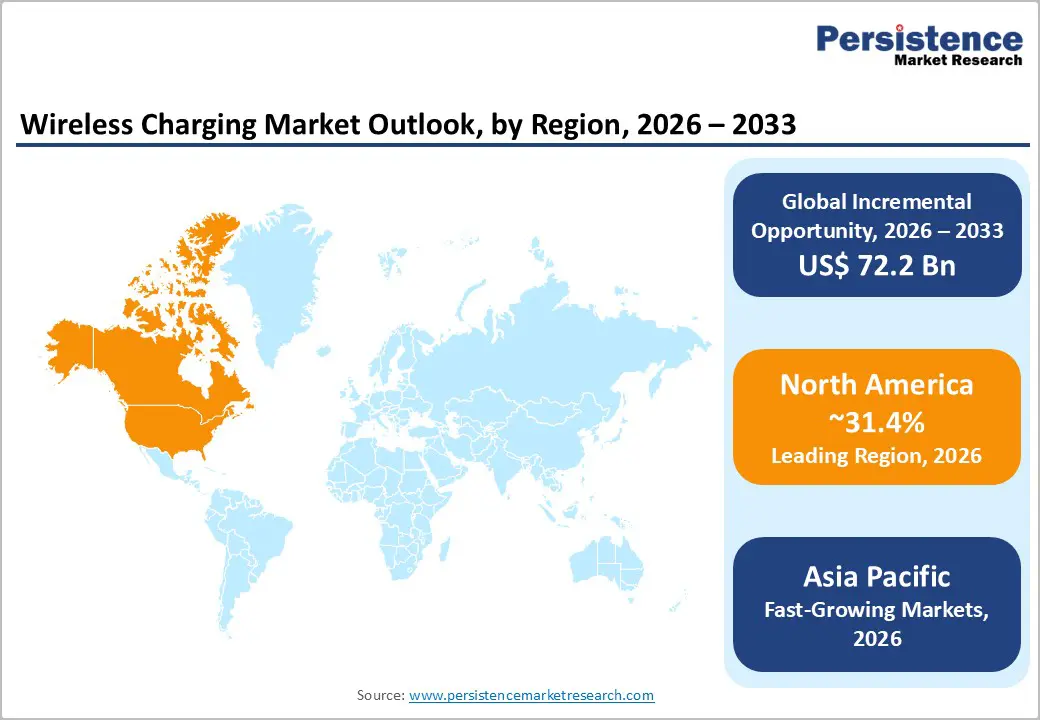

- Leading region: North America maintains the largest wireless charging market share at 31.4% in 2025, driven by Apple's dominant 57.39% smartphone market share in the United States and widespread consumer adoption of Qi2 technology among premium smartphone segments.

- Fastest Growing Region: Asia Pacific represents the fastest-growing region with 29.50% of global market share in 2025 and a projected CAGR of 24.36% through 2034, driven by China's manufacturing dominance, India's rising middle-class consumer adoption, and government-mandated electric vehicle charging infrastructure development across the region.

- Dominant Segment: Inductive charging technology dominates the market with 60% of global market share in 2025, reflecting proven reliability, electromagnetic efficiency, device manufacturer standardization support, and extensive patent portfolio coverage enabling seamless ecosystem integration across consumer electronics applications.

- Fastest Growing Segment: High Power (Above 50W) charging applications represent the fastest expanding segment, with Belkin's 200W GaN chargers and WPC's 2.2 kW power delivery capabilities opening industrial, electric vehicle, and professional workstation charging applications beyond traditional consumer electronics.

- Key Market Opportunity: Multi-device charging infrastructure integration into furniture, automotive consoles, and public spaces creates substantial growth opportunities, with projected unit shipments reaching 4,750 million wireless charging-enabled devices by 2030, driven by embedded receiver technology eliminating aftermarket accessory requirements.

| Report Attribute | Details |

|---|---|

|

Wireless Charging Market Size (2026E) |

US$ 22.0 Bn |

|

Market Value Forecast (2033F) |

US$ 94.2 Bn |

|

Projected Growth CAGR (2026-2033) |

23.1% |

|

Historical Market Growth (2020-2025) |

23.5% |

Market Dynamics

Market Growth Drivers

Rapid Adoption of Qi2 Standard and Enhanced Charging Speeds

The Wireless Power Consortium (WPC) introduced Qi v2.0 in 2023 and later launched Qi v2.2.1, branded as Qi2 25W, in July 2025, marking a major leap in wireless charging standards. This advancement allows certified devices to charge at 15 watts, with the latest version supporting speeds up to 25 watts and future capabilities projected to reach 50 watts. Samsung committed to integrating Qi2 across its Galaxy lineup in 2025, while Google contributed high-power wireless charging technology to support Qi v2.2 development.

A key feature, magnetic alignment, adapted from Apple’s MagSafe, ensures optimal efficiency and eliminates energy loss from misalignment, addressing a long-standing barrier to adoption. Leading accessory brands such as Belkin, Anker, Nomad, Mophie, and Baseus have rolled out Qi2-compatible chargers and power banks, including Belkin’s BoostCharge Pro 3-in-1 Magnetic Stand, which offers 15-watt charging along with Apple Watch fast-charging support.

Escalating Smartphone and Wearable Device Penetration in Emerging Economies

The global smartphone user base has surpassed 4.5 billion individuals, with particularly rapid growth in the Asia Pacific regions, including China, India, and Southeast Asia. The proliferation of wearable devices such as Apple Watch, smartwatches, and wireless earbuds creates complementary demand for multi-device wireless charging solutions. According to recent market analysis, consumer electronics applications account for 45% of the wireless charging market share in 2025, driven primarily by smartphone and accessories integration.

Inductive charging technology, which commands 60% market share due to its efficiency and compatibility with existing consumer electronics, has become the dominant transmission method. Rising disposable incomes in Asia Pacific markets, combined with tech-savvy consumer bases and robust manufacturing infrastructure in China, Japan, and South Korea, create sustained demand drivers that extend wireless charging adoption beyond developed markets into price-sensitive, high-volume segments.

Market Restraints

Consumer Skepticism and Limited Awareness Regarding Wireless Charging Benefits

Although wireless charging technology has advanced significantly, its adoption remains limited due to low consumer penetration. Current industry data shows that only 29% of smartphone users utilize wireless charging, highlighting both untapped potential and notable adoption challenges. Surveys reveal that around 45% of North American consumers are concerned about reliability and charging speed compared to traditional wired methods.

Persistent misconceptions, such as wireless charging being 10–20% slower than wired alternatives, continue to influence consumer perception. Additionally, issues like electromagnetic interference, thermal management in high-power applications, and potential cybersecurity risks in wireless power transfer systems contribute to hesitancy among individuals and enterprise buyers, particularly in security-sensitive sectors such as healthcare and financial services.

Higher Implementation Costs and Infrastructure Investment Requirements

Building wireless charging infrastructure, especially for medium and high-power applications, requires significantly higher upfront investment compared to traditional wired solutions. Electric vehicle wireless charging systems demand specialized components such as ground-mounted pads, in-vehicle receivers, and power transmission hardware, creating cost barriers for both developers and end-users. Public installations in smart cities and along highways involve civil engineering work, grid upgrades, and ongoing maintenance, all of which exceed the costs of conventional charging posts.

While consumer electronics wireless chargers are becoming more affordable, they still carry a premium over standard cable-based options, limiting adoption in price-sensitive markets. Additionally, the Wireless Power Consortium’s certification process adds further expense through testing fees and compliance requirements, particularly for Extended Power Profile (EPP) products supporting 5W to 30W, which must include authentication under Qi v1.3 standards.

Market Opportunities

Expansion of High-Power Wireless Charging for Gaming Laptops and Industrial Applications

The wireless charging market is rapidly evolving with significant opportunities in high-power applications exceeding 50W. Belkin’s BoostCharge Pro 4-Port USB-C GaN Charger exemplifies this trend, delivering a total output of 200W, including 140W per port for gaming laptops and professional workstations. The Medium Power standard set by the Wireless Power Consortium (WPC) currently supports 30W to 65W, with future capabilities expected to reach 200W for devices such as portable power tools, robotic vacuums, drones, and e-bikes.

Renesas Electronics has introduced the P9412 wireless power receiver, the industry’s first 30W receiver featuring a high-voltage integrated capacitor divider, achieving over 85% system efficiency while reducing solution size by 40% compared to conventional designs. This innovation frees up PCB space, enabling manufacturers to add more features. Furthermore, WPC’s upgrade of Qi technology to enable 2.2 kW wireless power delivery in 2024 opens new applications in industrial manufacturing, medical equipment, and commercial kitchen appliances. The integration of GaN (Gallium Nitride) technology with wireless charging is driving compact, efficient solutions that maintain high power output in smaller form factors.

Multi-Device Charging Solutions and Integration into Furniture and Infrastructure

The increasing number of wireless-enabled devices per user is driving demand for multi-device charging solutions. Belkin’s BoostCharge Pro 3-in-1 platform exemplifies this trend by enabling simultaneous charging for iPhone, AirPods, and Apple Watch on a single station. Renesas’s Wattshare technology further enhances functionality by allowing smartphones to act as power sources, wirelessly charging accessories such as earbuds and smartwatches, thereby introducing peer-to-peer charging capabilities.

The integration of Qi charging pads into furniture, automotive consoles, and public infrastructure, including desks, airport lounges, cafes, and transportation hubs, is gaining significant traction, with urban planners incorporating wireless charging into public transport facilities and parking lots as part of smart city initiatives. Qi v2.1 development specifically addresses automotive applications with moving charging coil designs that accommodate varying device sizes and awkward placement angles common in vehicle environments. This embedded approach enhances user experience and reduces the need for supplementary charging accessories, creating opportunities for component suppliers and semiconductor manufacturers.

Category-wise Insights

Charging Method Analysis

Charging pads lead the wireless charging method category, accounting for approximately 43% of market share due to their versatility, compact design, and seamless integration across residential, commercial, and automotive environments. Belkin’s BoostCharge Pro 3-in-1 Wireless Charging Pad with Qi2 illustrates this evolution, offering dual charging spots, 15W for iPhone and 5W for additional devices or AirPods, along with a detachable Apple Watch puck supporting fast charging.

Flat pad architecture enables integration into furniture such as office desks, nightstands, and conference tables, eliminating visible cables and enhancing aesthetics. Qi2 certification ensures consistent 15W charging with magnetic alignment, addressing efficiency concerns from device misplacement. Automotive manufacturers increasingly adopt pads as original equipment, supported by WPC’s Qi v2.1 standard featuring moving coil technology for varied smartphone sizes and positions.

Technology Analysis

Inductive charging technology holds the dominant position in the wireless charging market, accounting for 60% of global share in 2025. Its leadership is driven by proven reliability, compatibility with existing device ecosystems, and superior electromagnetic efficiency for short-to-medium range power transfer. Inductive systems use electromagnetic induction to transmit power between coils embedded in charging pads and receiver coils in devices, ensuring interoperability supported by extensive patent portfolios from companies such as Qualcomm, NXP Semiconductors, and Renesas Electronics.

Resonant inductive coupling, the second-largest segment with 28% share, offers greater tolerance to misalignment and air gaps, making it ideal for automotive applications. Radio frequency (RF) charging represents about 8% of the market, primarily serving low-power IoT devices and smart city infrastructure. Inductive dominance reflects efficiency, cost advantages, safety validation, and universal Qi standard adoption.

Power Range Analysis

Low-power wireless charging (up to 10W) accounts for approximately 46% of market volume, driven primarily by smartphones and wearable devices where power requirements typically range from 5W to 10W. The Baseline Power Profile (BPP) under Qi 1.2 supports up to 5W, while newer standards enable 10W through proprietary extensions, as seen in Samsung’s implementation under Qi 1.3. Flagship devices such as the iPhone 15 series, Samsung Galaxy S24 Ultra, and Google Pixel 8 utilize Qi-based charging within this range, reinforcing its role as a premium feature.

Wearables like Apple Watch and AirPods also operate within low-power specifications, with multi-device solutions allocating 5W for accessories. This segment benefits from the largest installed base, exceeding 1.2 billion annual smartphone shipments, and offers energy efficiency advantages that support consumer adoption and regulatory compliance.

Charging Standard Analysis

The Qi wireless charging standard, developed by the Wireless Power Consortium (WPC), dominates the global market with a 73% share, encompassing Qi v1.0, Qi v2.0, Qi2, and emerging Qi2 25W specifications. Its widespread adoption reflects strong industry support, particularly Apple’s integration of Qi2 in iPhone 12–16 series and Samsung’s commitment to Qi2 across Galaxy devices in 2025. Over 13,000 Qi-certified products are available globally, with certification numbers rising rapidly as new Qi2 and Qi2 25W categories launch.

In comparison, the Powermat standard holds approximately 15% market share, mainly in automotive applications and legacy installations, while proprietary and emerging standards account for the remaining 12%. Qi’s dominance is underpinned by robust WPC certification processes, extensive patent licensing, superior interoperability, and compliance with safety regulations across major global markets.

End-Use Analysis

Smartphone wireless charging constitutes the largest market segment, representing approximately 54% of total end-use applications. This dominance reflects widespread smartphone penetration in developed markets and rapid adoption in emerging economies. Leading manufacturers such as Apple and Samsung have standardized wireless charging across flagship and mid-range models, shaping consumer expectations and driving accessory ecosystem growth.

Wearable devices, including smartwatches, wireless earbuds, and fitness trackers, account for about 22% of market share, with strong growth in premium segments where integrated charging enhances convenience and portability. Tablets hold 12% share, primarily in high-end models, while laptops remain at 8%, limited to select premium devices but expanding as high-power wireless solutions advance. Smartphone leadership is supported by over 4.5 billion global users, ingrained charging habits, and robust third-party accessory ecosystems.

Regional Insights

North America Wireless Charging Trends

North America holds the largest regional market share at 31.4% in 2025, primarily driven by the U.S., which recorded a valuation of $5,277 million and is projected to grow at a CAGR of 18.7% during the forecast period. Apple’s dominant U.S. smartphone share of 57.39% has positioned Qi2 wireless charging as a standard feature in premium devices. The widespread adoption of iPhone 12–16 series with Qi2 support has accelerated ecosystem development, prompting accessory manufacturers such as Anker, Belkin, Nomad, and Mophie to launch comprehensive product lines.

Favorable regulatory policies, reduced certification timelines, and utility-backed infrastructure initiatives further support adoption. Rising EV penetration in states like California and Texas drives demand for SAE J2954-compliant wireless charging, while emerging opportunities include smart home integration, luxury automotive applications, and dynamic highway charging projects.

Europe Wireless Charging Trends

Europe is the second-largest regional market for wireless charging, with Germany accounting for approximately 28% of the share, supported by its strong automotive manufacturing base, consumer preference for premium electronics, and government incentives for EV adoption. France, the United Kingdom, and Spain also hold significant positions, with combined investments in wireless EV charging infrastructure exceeding $32 million in 2025 at a CAGR of 40.05%.

Nordic countries, Norway, Sweden, and Finland, represent the fastest-growing sub-region, projected to achieve a CAGR of 52.10% through 2030, driven by high EV penetration, regulatory mandates, and municipal fleet electrification programs. EU efforts to harmonize standards and electromagnetic field regulations create a favorable policy environment. Static wireless charging systems dominate current deployments, while dynamic in-road charging is emerging as a high-growth opportunity.

Asia Pacific Wireless Charging Trends

Asia Pacific is the fastest-growing regional market, holding 29.50% of global share in 2025 and projected to reach $70 billion by 2034, reflecting a sustained CAGR of 24.36%. China leads with 38.20% of regional share, driven by its extensive smartphone manufacturing ecosystem, robust consumer electronics retail infrastructure, and government mandates for 11 kW wireless EV charging stations in new residential projects.

Japan accounts for 19.60%, leveraging technological leadership in wireless power transmission and early Qi2 adoption in premium devices. India holds 11.50%, fueled by rising middle-class demand for premium smartphones and smart infrastructure development. South Korea maintains 12%, supported by Samsung’s manufacturing strength and dynamic charging technology validation. Cost advantages in China, Vietnam, and Bangladesh enable competitive supply chains, while emerging opportunities in India and Southeast Asia focus on affordable wireless charging solutions.

Competitive Landscape

Market Structure Analysis

The wireless charging market is moderately fragmented, with leadership concentrated among specialized accessory manufacturers and technology component suppliers rather than traditional electronics conglomerates. Anker Innovation Technology leads the market by leveraging extensive distribution networks, strong brand recognition, and rapid product development aligned with Qi2 25W standard adoption. Belkin International holds a second-tier position with $325.9 million in revenue, focusing on premium designs and Apple ecosystem integration, while Mophie, at $215.4 million, emphasizes portable power solutions and multi-device platforms. Major smartphone brands such as Apple, Samsung, and Google compete through integrated wireless charging features, while component suppliers like Qualcomm and NXP Semiconductors maintain an edge via patent portfolios and technology licensing. Market growth is driven by Qi and SAE J2954 standardization, enabling new entrants and fostering innovation.

Key Market Developments

- July 2025: Wireless Power Consortium introduced Qi2 25W standard, enabling charging speeds up to 25 watts with advanced magnetic alignment technology, establishing a new performance baseline for the industry and accelerating adoption across smartphone manufacturers, including future Apple and Google Pixel device generations.

- January 2025: Samsung Electronics announced Galaxy S25 series support for Qi 2.1 wireless charging standard, combining automatic alignment and magnetic phone case technology, expanding Qi2 ecosystem penetration among Android manufacturers, and establishing interoperability with premium charging accessories.

- November 2025: Nomad introduced 4th generation Stand One wireless chargers featuring Qi2 25W support at $119-$159 price points, demonstrating market validation of premium wireless charging accessories and expanding multi-device charging ecosystem to accommodate iPhone, Apple Watch, and compatible Android devices simultaneously.

Top Companies in the Wireless Charging Market

Anker Innovation Technology (China) dominates the wireless charging market, leveraging extensive distribution infrastructure across North America and the Asia Pacific, rapid product innovation cycles supporting Qi2 standards adoption, and strategic partnerships with device manufacturers. The company's diversified product portfolio spans charging pads, charging stands, and multi-device charging stations, addressing consumer segments from budget-conscious to premium market positions.

Belkin International Inc. (U.S.) maintains a second-tier market position, emphasizing premium product design, seamless integration with the Apple ecosystem through MagSafe compatibility, and retail distribution through major technology retailers, including Apple Store partnerships. Belkin's strength derives from brand heritage in mobile accessories, design-forward aesthetic approach to wireless charging solutions, and established relationships with consumer electronics retailers across developed markets.

Samsung Electronics Co. Ltd. (South Korea) integrates wireless charging as a standard smartphone feature across the Galaxy flagship lineup, commanding significant market influence through device ecosystem integration, investment in Qi2 standard adoption, and development of future high-power wireless charging technologies. Samsung's competitive position reflects vertical integration spanning semiconductor components, device manufacturing, and ecosystem software optimization, enabling rapid technology advancement and market-wide standardization advocacy.

Companies Covered in Wireless Charging Market

- Anker Innovation Technology

- Belkin International, Inc.

- Otter Products, LLC

- Nomad

- totallee

- ByteCable & Memory Range Technology co., Ltd

- Energizer

- Renesas Electronics Corporation

- Qualcomm Technologies, Inc.

- Samsung Electronics Co. Ltd.

- Apple Inc.

- NXP Semiconductors

- Mophie

- Powermat Technologies

- WiTricity Corporation

- Ossia Inc.

Frequently Asked Questions

The global wireless charging market is projected to reach US$ 94.2 billion by 2033, growing from US$ 22.0 billion in 2026 at a compound annual growth rate of 23.1%. This substantial growth reflects accelerating smartphone adoption, wearable device proliferation, electric vehicle infrastructure development, and standardization through Qi2 wireless charging technology across global markets.

The wireless charging market growth is fundamentally driven by rapid Qi2 standard adoption, enabling 25-watt charging speeds comparable to wired alternatives, escalating smartphone and wearable device penetration in emerging markets, substantial electric vehicle adoption requiring wireless charging infrastructure, and consumer preference for cable-free charging convenience.

Inductive Charging technology dominates with approximately 60% market share, supported by Wireless Power Consortium's Qi standardization, Renesas Electronics achieving over 85% system efficiency at 30W power levels, and widespread adoption across Apple, Samsung, Google, and Xiaomi device portfolios.

North America maintains the largest regional market share at 31.4% in 2025, driven by Apple's 57.39% smartphone market dominance in the U.S. and widespread consumer adoption of Qi2 standards in premium device segments.

Anker Innovation Technology dominates the market, followed by Belkin International and Mophie. Major smartphone manufacturers Apple Inc., Samsung Electronics, and Google drive market standardization through device ecosystem integration. Technology component suppliers, including Qualcomm Technologies, Inc., NXP Semiconductors, and Renesas Electronics Corporation, command a competitive advantage through wireless power transmission patent portfolios and chip supply relationships.