- Electric Mobility

- Wireless Electric Vehicle Charging Market

Wireless Electric Vehicle Charging Market Size, Share, and Growth Forecast, 2025 - 2032

Wireless Electric Vehicle Charging Market by Power Source Type (Below 11 KW, 11–50 KW, Above 50 KW), Vehicle (Passenger Cars, Commercial Vehicles), Distribution Channel (OEMs, Aftermarket), and Regional Analysis for 2025 - 2032

Wireless Electric Vehicle Charging Market Size and Trends Analysis

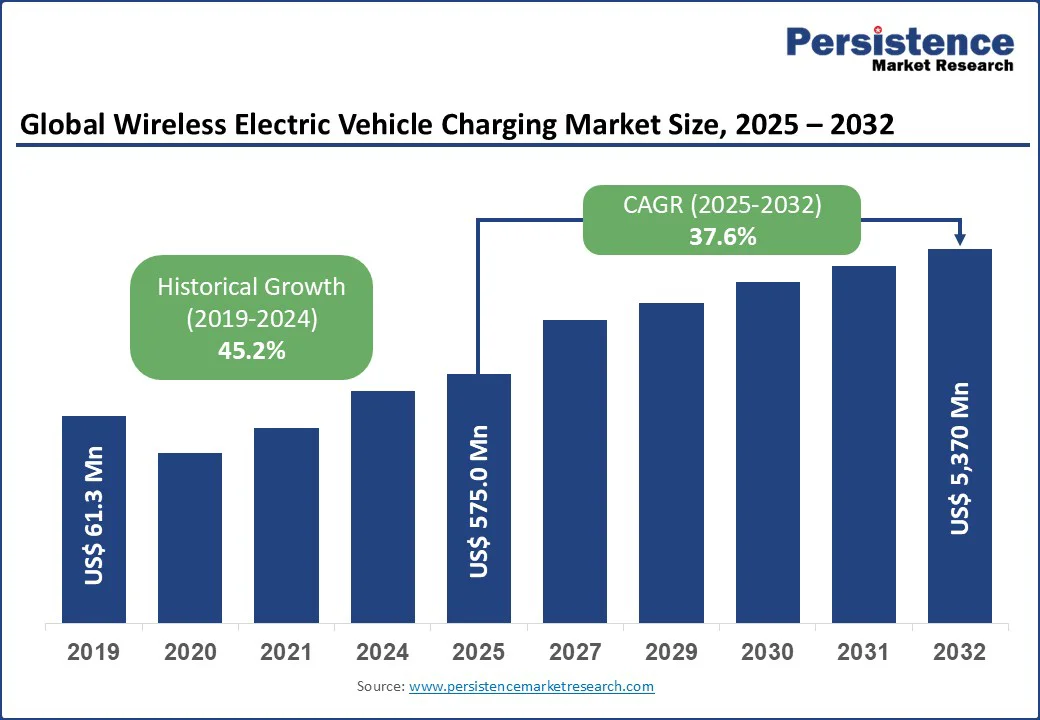

The global wireless electric vehicle (EV) charging market size is likely to reach US$575.0 Mn in 2025 and reach US$5,370 Mn by 2032, registering a CAGR of 37.6% during the forecast period from 2025 to 2032.

The market has witnessed strong growth driven by rising consumer awareness of sustainable mobility and the urgent shift toward reducing carbon emissions. Increasing demand for convenient, efficient, and wireless charging solutions is reshaping the electric vehicle ecosystem. Leading brands are introducing innovative technologies, enhancing performance, reliability, and adoption across global transportation networks.

Key Industry Highlights:

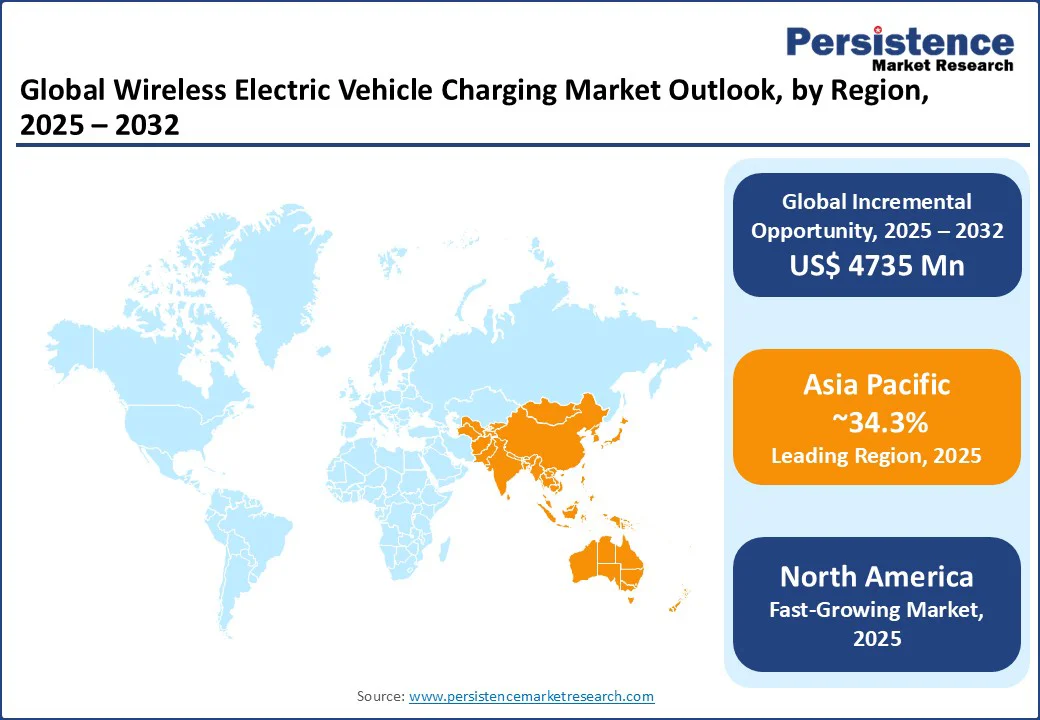

- Leading Region: Asia Pacific holds a 34.3% market share in 2025, driven by large-scale EV production, high population density, and increasing demand for efficient charging solutions in countries such as China and India.

- Fastest-growing Region: North America, fueled by rising consumer demand for advanced and convenient technologies, advanced infrastructure development, and strong adoption of eco-friendly transportation.

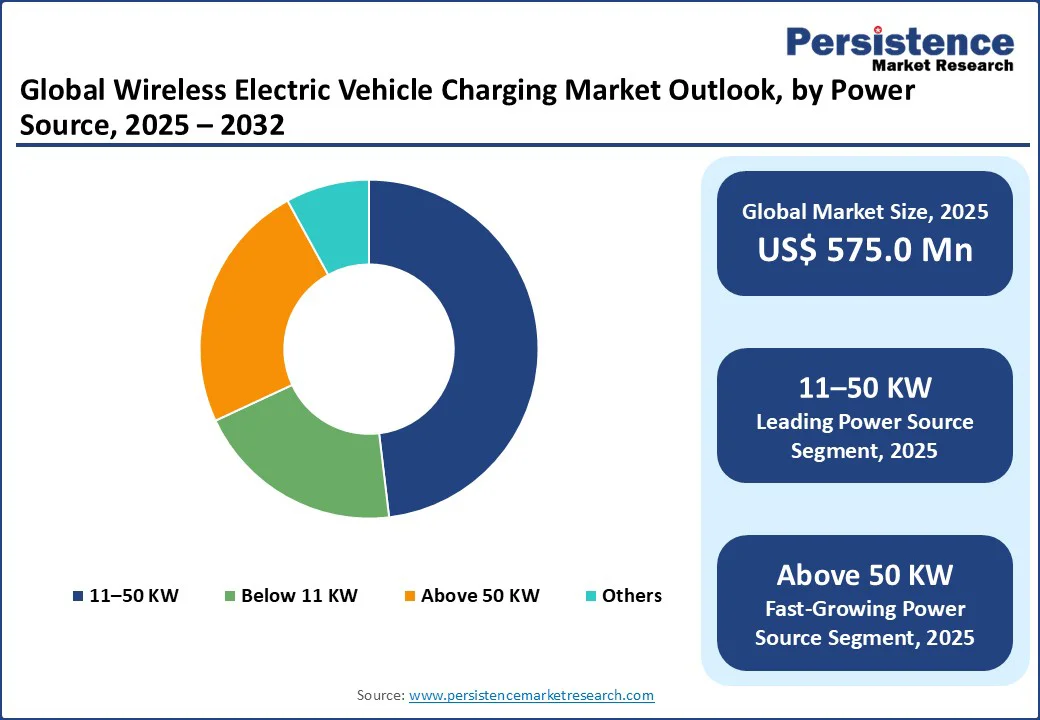

- Dominant Power Source Type in Wireless EV Charging Market: 11–50 KW accounts for nearly 48.2% of market share, driven by its versatility in supporting a wide range of vehicle types.

- Leading Vehicle Type: Passenger Cars lead with a 40% share, offering wide availability and competitive pricing.

- Leading Distribution Channel: OEMs dominate with a 65% share, driven by integration into new EV models.

- Projected Expansion: Opportunities in smart grid integration and sustainable infrastructure are expected to propel the wireless EV charging market to US$5370 Mn by 2032.

|

Global Market Attribute |

Key Insights |

|

Wireless EV Charging Market Size (2025E) |

US$575.0 Mn |

|

Market Value Forecast (2032F) |

US$5370 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

37.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

45.2% |

Market Dynamics

Driver - Rising Demand for Sustainable Mobility and Convenient Charging Solutions Pushes Demand

The wireless EV charging market is propelled by increasing demand for sustainable mobility and the growing adoption of convenient charging solutions. The global rise in electric vehicle adoption, driven by environmental concerns and government incentives, has boosted demand for innovative charging technologies such as wireless systems. Urbanization and fast-paced lifestyles continue to drive demand for seamless, cable-free charging solutions. Wireless EV charging is widely valued for its ability to enhance user convenience and support smart city infrastructure. In markets such as the U.S., consumers are increasingly opting for wireless charging over traditional plug-in systems, with surveys by the Electric Vehicle Association reporting a strong preference for cable-free solutions for home and public charging.

Government-backed sustainability programs further support market growth. In India, initiatives such as the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme have promoted EV infrastructure development, with wireless charging pilot projects launched in cities such as Delhi and Bangalore. These programs highlight the role of wireless charging in reducing carbon emissions and supporting clean energy goals.

The expansion of the EV industry has also driven demand, with global EV sales reaching 17 Mn units in 2024, creating a need for efficient charging infrastructure. Wireless charging systems, such as those developed by WiTricity Corporation, offer a cost-effective and scalable solution for urban and commercial applications.

Restraint - High Installation Costs and Infrastructure Challenges Limit Adoption

The industry faces challenges due to high installation costs and infrastructure limitations. The deployment of wireless EV charging systems requires significant investment in ground pads, power electronics, and grid integration, which increases upfront costs. Industry reports indicate that installing a single wireless charging station can cost considerably more than a traditional plug-in charger, deterring adoption in cost-sensitive markets such as rural India or Sub-Saharan Africa. Additionally, the lack of standardized infrastructure and interoperability across different systems poses a barrier, as consumers and manufacturers face compatibility issues.

Consumer concerns about efficiency and safety also hinder growth. Wireless charging systems currently have lower energy transfer efficiency than wired chargers, with noticeable transmission losses, according to industry studies. This inefficiency, combined with concerns about electromagnetic field exposure, restricts adoption among safety-conscious demographics, particularly in Europe and North America, where regulatory scrutiny remains high.

Opportunity - Innovation in Smart Grid Integration and Sustainable Infrastructure Boosts Consumption

The wireless EV charging market presents strong opportunities through innovation in smart grid integration and sustainable infrastructure. Growing demand for efficient, eco-friendly charging solutions aligns with consumer and industry preferences for clean energy technologies. Wireless charging systems integrated with smart grids and renewable energy sources are gaining traction, fueled by the global push for net-zero emissions.

Companies can capitalize by developing advanced systems that combine wireless charging with vehicle-to-grid (V2G) technology, catering to both environmentally conscious consumers and infrastructure developers. For example, in 2024, HEVO Inc. launched a smart grid-compatible wireless charging system, reporting a 20% increase in adoption among commercial fleets.

Sustainable infrastructure development is another growth avenue. With global efforts to reduce environmental impact, brands are investing in energy-efficient charging solutions. In 2024, Electreon introduced a dynamic wireless charging road in Europe, reducing reliance on fossil fuel-based grids and enhancing brand loyalty among eco-conscious stakeholders.

In the Asia Pacific, companies such as WiPowerOne are exploring scalable charging networks, reducing environmental footprints. The rise of e-commerce and digital platforms for EV accessories is also creating opportunities, with online marketplaces offering wireless charging solutions to fleet operators and individual consumers, expanding market reach through targeted digital marketing.

Category-wise Analysis

By Power Source Type

The wireless EV charging market is segmented into below 11 KW, 11–50 KW, and above 50 KW. The 11–50 KW segment dominates, expected to account for approximately 48.2% of the wireless EV charging market share in 2025, due to its versatility in supporting both passenger cars and light commercial vehicles. Brands such as WiTricity Corporation and HEVO Inc. have solidified their positions through advanced technology and widespread deployment capabilities. Its compatibility with urban charging infrastructure further drives adoption.

The segment above 50 KW is the fastest-growing, fueled by rising demand for high-power charging solutions for commercial vehicles and public transit systems. These systems appeal to fleet operators, particularly in urban areas, where fast charging is critical for operational efficiency. High-power wireless charging stations are gaining traction for their ability to support heavy-duty applications without compromising speed.

By Vehicle Type

Passenger Cars lead the vehicle segment, expected to account for 40% of the wireless EV charging market share in 2025. Their dominance stems from widespread adoption of electric passenger vehicles, competitive pricing, and consumer preference for convenient home and public charging solutions. Companies such as Induct EV Inc. and EVATRAN Group (Plugless) offer tailored wireless charging systems for passenger cars that meet the needs of urban consumers.

Commercial Vehicles are the fastest-growing segment, driven by the rise of electric buses and delivery fleets. The shift toward sustainable logistics, accelerated by government mandates for zero-emission transport, continues to boost this segment’s growth, with platforms expanding wireless charging offerings for commercial applications.

By Distribution Channel Type

OEMs lead the distribution channels, expected to account for 65% of the wireless EV charging market share in 2025. Their dominance is due to the integration of wireless charging systems into new EV models during manufacturing. Companies such as Toyota Motor Corporation and Continental AG offer proprietary wireless charging solutions, ensuring compatibility and reliability for end users.

The aftermarket is the fastest-growing segment, driven by rising consumer demand for retrofitting existing EVs with wireless charging capabilities. The rise of aftermarket solutions, particularly in urban markets, is fueled by the need for flexible and scalable charging options for older EV models.

Regional Insights

North America Wireless EV Charging Market Trends

In North America, the wireless EV charging market is the fastest-growing region, driven by rising consumer demand for advanced and convenient charging technologies and robust infrastructure development. The U.S. market is experiencing strong growth, supported by the increasing adoption of electric vehicles and government incentives for clean energy. The 11–50 KW and above 50 KW segments lead, fueled by their use in passenger cars and commercial fleets. Leading brands such as WiTricity Corporation and HEVO Inc. are expanding their offerings, while newer entrants gain traction with sustainable, high-efficiency systems.

Consumer trends in the U.S. strongly favor convenient and eco-friendly charging solutions, with brands such as EVATRAN Group (Plugless) seeing significant growth due to their user-friendly designs. Sustainability is a major focus, with companies introducing renewable energy-integrated charging systems. Regulatory support, such as the U.S. Department of Energy’s funding for wireless charging pilots, further contributes to market expansion.

Europe Wireless EV Charging Market Trends

Europe’s wireless EV charging market is led by Germany, the U.K., and France, driven by stringent regulations and increasing demand for sustainable infrastructure. Germany holds the largest market share, with a strong focus on 11–50 KW systems for passenger and commercial vehicles. The popularity of international brands such as Continental AG and Robert Bosch GmbH underscores this trend. The EU’s Green Deal Strategy promotes sustainable mobility, boosting the adoption of wireless charging across public and private sectors.

The U.K. market is driven by eco-conscious consumers and fleet operators favoring high-efficiency, low-impact charging solutions. Brands such as Wave Charging are expanding their offerings, emphasizing scalability and integration with smart grids. France witnessed steady growth in commercial vehicle applications, with high-power systems preferred. Regulatory incentives for zero-emission transport continue to support market growth across the region.

Asia Pacific Wireless EV Charging Market Trends

Asia Pacific dominates with a 34.3% market share in 2025, led by China, India, and Japan. In India, rising EV adoption and urbanization are driving demand for affordable 11–50 kW charging systems, with companies such as WiPowerOne and Dashdynamic leading the wireless EV charging market. India’s EV infrastructure is expanding, supported by government programs such as the FAME scheme, which promotes wireless charging pilots in urban centers.

China’s market is driven by large-scale EV production and rising demand for public charging infrastructure, with brands such as Electreon leading in dynamic charging solutions. Japan emphasizes premium wireless charging for passenger cars, with Toyota Motor Corporation’s systems gaining traction. The region’s rapid digital transformation and growth in B2B e-commerce further accelerate market expansion.

Competitive Landscape

The global wireless EV charging market is highly competitive, with global and regional players competing on technology innovation, pricing, and scalability. The rise of sustainable and high-efficiency charging systems intensifies competition, as consumers and industries demand eco-friendly solutions. Strategic partnerships, patents, and technological advancements are key differentiators.

Industry Developments:

- March 2025: InductEV partnered with ENC to introduce wirelessly charged next-generation battery-electric buses across North America. This collaboration enhances operational efficiency, reduces downtime, and supports sustainable transit by integrating advanced wireless charging technology into public transportation fleets.

- March 2025: ENRX launched ENRMOVE, a cutting-edge wireless charging platform designed for industrial vehicles such as AGVs, forklifts, and mobile robots. It enables seamless opportunity charging during regular operations, reducing downtime, improving productivity, and supporting sustainable, energy-efficient warehouse and logistics operations.

Companies Covered in Wireless Electric Vehicle Charging Market

- Electreon

- Induct EV Inc.

- Dashdynamic

- EVATRAN Group (Plugless)

- Continental AG

- WiPowerOne

- Toyota Motor Corporation

- HEVO Inc.

- Wave Charging

- Robert Bosch GmbH

- WiTricity Corporation

Frequently Asked Questions

The wireless EV charging market is projected to reach US$575.0 Mn in 2025.

Rising demand for sustainable mobility, convenient charging solutions, and government-backed EV infrastructure initiatives are the key market drivers.

The wireless EV charging market is poised to witness a CAGR of 37.6% from 2025 to 2032.

Innovation in smart grid integration and sustainable infrastructure are the key market opportunities.

WiTricity Corporation, Electreon, and HEVO Inc. are among the key market players.