- HVAC

- Ventilation Equipment Market

Ventilation Equipment Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Ventilation Equipment Market by Product Type (Ventilation Fans, Dehumidifiers and Humidifiers, Heat Recovery Ventilation Systems, Air Handling Units, Air Filters and Purifiers), Technology (Mechanical Ventilation, Natural Ventilation, Hybrid Ventilation), Application (Residential, Commercial, Industrial), Regional Analysis, 2025 - 2032

Ventilation Equipment Market Size and Trend Analysis

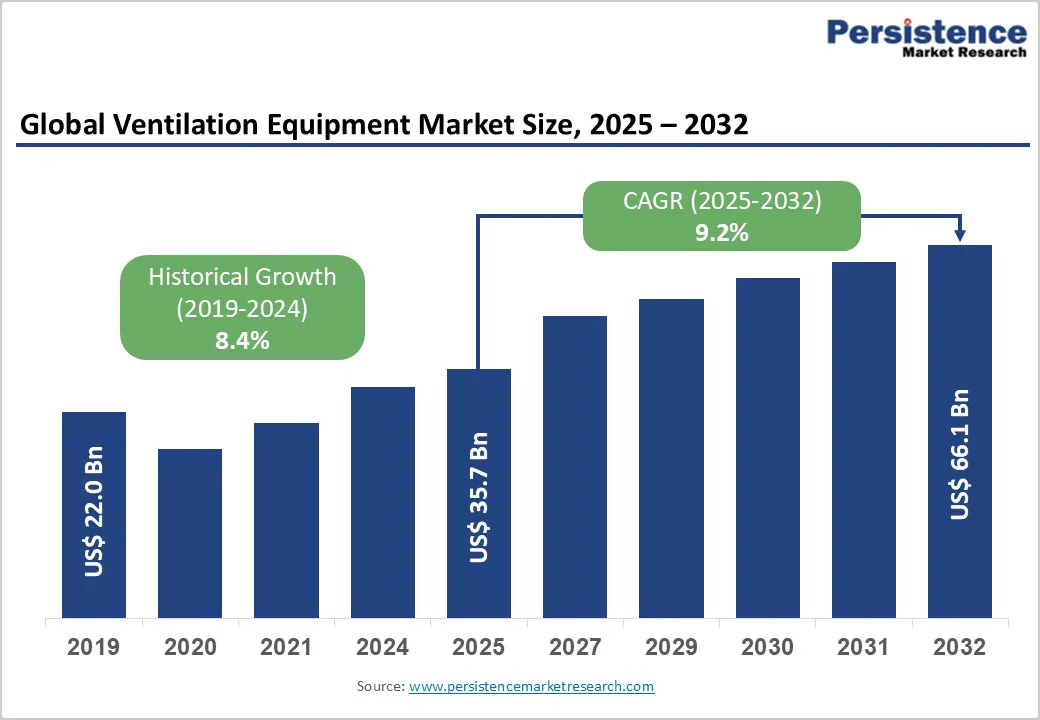

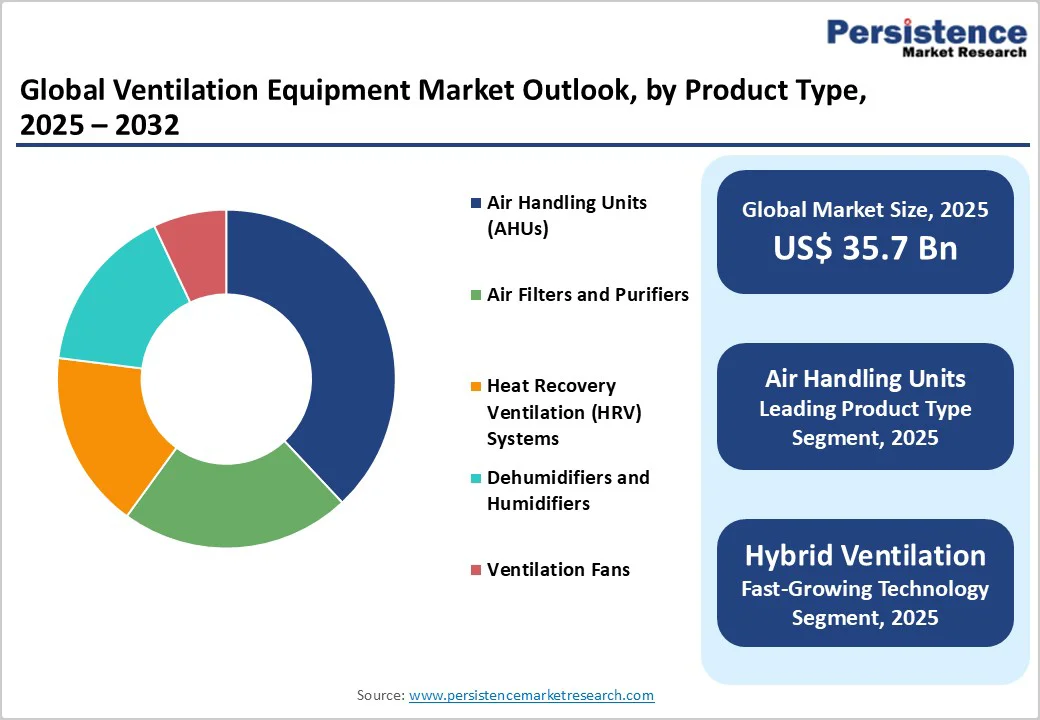

The global ventilation equipment market size is likely to value at US$ 35.7 billion in 2025 and is projected to reach US$ 66.1 billion, growing at a CAGR of 9.2% between 2025 and 2032.

The market expansion is primarily driven by increasing awareness of indoor air quality and stringent government regulations mandating proper ventilation systems across commercial and residential sectors.

Key Market Highlights:

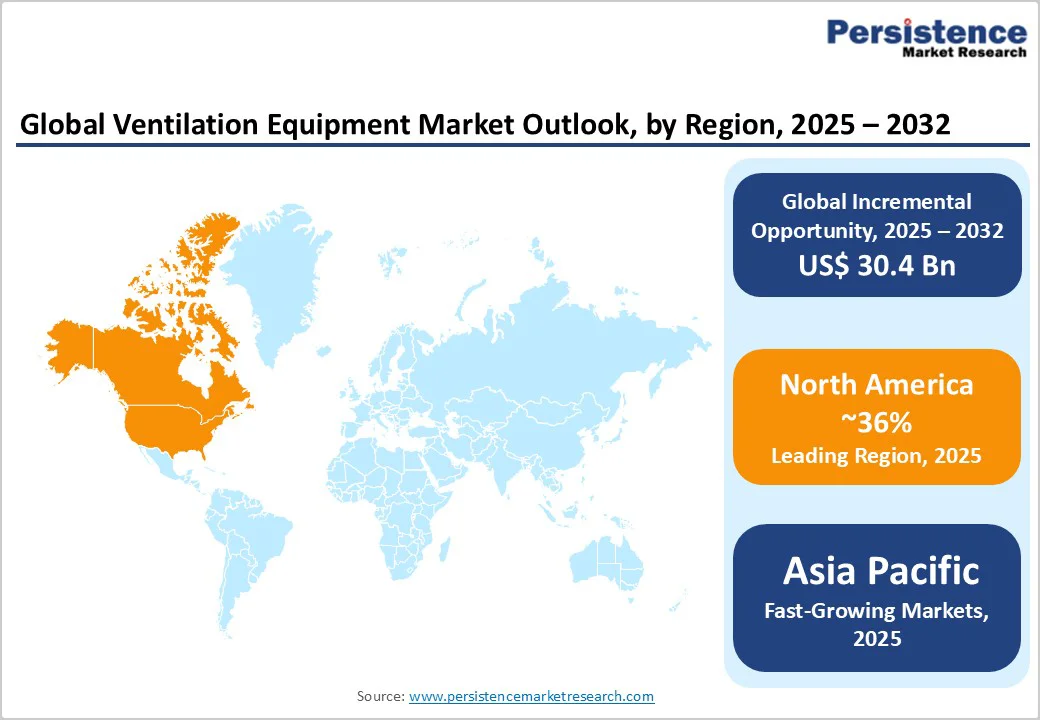

- Leading Region: North America dominates the global ventilation equipment market with approximately 36% share, driven by stringent OSHA workplace safety regulations.

- Fastest Growing Region: Asia Pacific exhibits the highest growth trajectory at 10.1% CAGR, fueled by China's industrial expansion, India's construction.

- Dominant Segment: Air Handling Units lead the product type category with approximately 38% market share, supported by comprehensive air quality management capabilities, advanced filtration technologies.

- Fastest Growing Segment: Hybrid Ventilation technology demonstrates accelerated adoption driven by energy efficiency mandates.

- Key Market Opportunity: The integration of smart, energy recovery ventilation systems with existing systems enables up to 95% heat recovery and 25-67% energy savings, supporting net-zero building goals and EU efficiency regulations.

| Key Insights | Details |

|---|---|

| Ventilation Equipment Market Size (2025E) | US$ 35.7 Bn |

| Market Value Forecast (2032F) | US$ 66.1 Bn |

| Projected Growth CAGR (2025 - 2032) | 9.2% |

| Historical Market Growth (2019 - 2024) | 8.4% |

Market Dynamics

Driver - Rising Indoor Air Quality Concerns and Regulatory Compliance

The growing focus on indoor air quality management has become a key driver for the ventilation equipment market, especially in the post-pandemic era. OSHA establishes permissible exposure limits for workplace pollutants, with a carbon monoxide limit of 25 ppm for an 8-hour workday, and NIOSH recommends a 35 ppm limit.

A 2023, Honeywell survey revealed that 72% of office workers are concerned about indoor air quality and seek regular updates on metrics. The EPA emphasizes proper ventilation and air filtration to reduce pollutants, while ASHRAE Standard 62.1 outlines necessary ventilation requirements. These regulations are prompting organizations to invest in advanced ventilation systems equipped with HEPA filters, activated carbon filters, UV-C light disinfection, and energy recovery systems to ensure compliance and protect occupant health.

Growth in Construction Industry and Infrastructure Development

The robust expansion of construction activities globally represents a significant growth catalyst for the ventilation equipment market, with commercial construction experiencing growth in Q2 2025 compared to Q1, led by data centers, healthcare facilities, and revitalized hotel and retail sectors.

The Infrastructure Investment and Jobs Act (IIJA), Inflation Reduction Act (IRA), and CHIPS Act are pumping substantial funding into manufacturing and energy-related commercial builds, creating sustained demand for sophisticated ventilation solutions.

Data center construction has experienced explosive growth, with spending increasing 45% in 2023 and 56% in 2024, and potentially reaching 40% growth for 2025. The U.S. Department of Energy projects that data center power demand could nearly triple in the next three years, consuming up to 12% of the country's electricity, necessitating advanced liquid cooling and ventilation technologies.

Restraint - High Costs and Labor Shortages Restrict Adoption of Advanced Ventilation Systems.

High initial investment and installation costs continue to hinder the widespread adoption of advanced ventilation systems. Energy-efficient and smart ventilation technologies often come with premium pricing due to their sophisticated components, such as IoT-enabled controls and high-performance filtration mechanisms.

The installation process further adds to expenses, demanding specialized technical skills and often involving complex retrofitting that can disrupt existing infrastructure.

The industry faces an acute shortage of skilled labor, particularly technicians and engineers trained to handle modern HVAC and ventilation systems. This expertise gap not only slows project execution but also raises concerns about long-term maintenance and system reliability.

For many organizations, especially small and medium enterprises, these financial and operational barriers make it challenging to justify investment in upgraded ventilation infrastructure, despite the clear benefits in energy efficiency and indoor air quality enhancement.

Opportunity - Energy Recovery Ventilation and Smart Technology Integration

The integration of energy recovery ventilation systems with smart technologies presents exceptional growth opportunities, particularly as buildings seek to achieve net-zero energy status and comply with increasingly stringent environmental regulations.

Heat recovery ventilation systems can recover 60-95% of heat in exhaust air, significantly improving building energy efficiency. European regulations mandate a minimum sensible recovery efficiency of 85% for HRVs and 75% for ERVs, with total recovery efficiency for ERVs reaching at least 80%.

Advanced European HRV and ERV equipment achieves whole-system efficacies ranging from 2-6 cfm/Watt, delivering Coefficient of Performance (COP) ratios of approximately 20 in cooling mode and 30 in heating mode. The EU27 expects electricity savings of 8 TWh in 2030 from improved ventilation measures, potentially increasing to 15 TWh by 2050.

Smart ventilation systems incorporating IoT sensors, AI-based control systems, and predictive maintenance capabilities can reduce building energy usage by 25% to 67% through optimal operational adjustments.

Category-wise Insights

Product Type Analysis

Air Handling Units (AHUs) dominate the product type segment with an estimated market share of approximately 38%, driven by their critical role in comprehensive indoor air quality management across commercial, industrial, and residential applications. These units are particularly popular in large commercial and industrial applications where efficient heating, cooling, and ventilation are critical for maintaining optimal indoor environments.

AHUs incorporate advanced filtration technologies, with the filters segment exceeding USD 4.1 billion in 2024, featuring MERV 13 or higher ratings capable of capturing approximately 85% of airborne respiratory particles. The commercial segment reflects robust demand for AHU, amid rising demand from office buildings, shopping malls, healthcare facilities, and educational institutions requiring sophisticated air treatment solutions.

Technology Analysis

Mechanical Ventilation technology commands the leading position in the technology segment with approximately 52% market share, reflecting its reliability, controllability, and ability to provide consistent indoor air quality regardless of external weather conditions.

These ventilation systems use fans and ducts to control airflow within buildings, offering precise environmental control essential for commercial and industrial applications where air quality standards are strictly regulated. The technology's dominance is further reinforced by IoT integration capabilities, enabling real-time monitoring and automated adjustments based on occupancy patterns, CO2 levels, and air quality metrics.

Hybrid Ventilation systems are gaining significant traction, combining natural and mechanical ventilation methods to enhance efficiency and adaptability based on weather conditions, occupancy levels, and indoor air quality requirements.

Research indicates that hybrid ventilation systems can reduce cooling energy consumption significantly, particularly in hot climates, with studies showing 25% to 67% energy usage reductions through optimal system design and control strategies.

Application Analysis

Commercial applications represent the dominant application segment with an estimated market share of 45%, driven by stringent regulatory requirements, increasing awareness of workplace health and safety, and substantial investments in modern building infrastructure.

The commercial segment's leadership is supported by OSHA workplace air quality mandates and growing recognition that poor indoor air quality costs businesses up to $15 billion annually in lost productivity. Office buildings, shopping malls, hospitals, and educational institutions constitute primary demand drivers, with 72% of office workers expressing concerns about workplace air quality and seeking regular air quality metric updates.

Regional Insights

North America Ventilation Equipment Market Trends

North America maintains market leadership with approximately 36% global market share, driven by stringent regulatory frameworks, advanced building codes, and substantial government infrastructure investments.

The United States contributed significantly with 78.2% share in the North American region during 2024, supported by OSHA workplace safety mandates and EPA indoor air quality guidelines. The region's innovation ecosystem centers on energy efficiency and smart technology integration, with manufacturers focusing on IoT-enabled systems, predictive maintenance capabilities, and advanced filtration technologies.

Europe Ventilation Equipment Market Trends

Europe demonstrates strong market performance driven by comprehensive regulatory harmonization under the Energy Performance of Buildings Directive (EPBD) and ambitious carbon neutrality goals targeting net-zero emissions by 2050.

The EPBD mandate requires all new buildings to be emission-free by 2030, compelling investment in advanced ventilation systems featuring energy recovery capabilities and smart controls. European countries including Germany, United Kingdom, France, and Spain lead in implementing stringent energy efficiency standards, with the EU27 spending €18 billion on ventilation units in 2015 and projections reaching €21 billion by 2030.

The region prioritizes energy recovery ventilation systems achieving 85% sensible recovery efficiency for HRVs and 75% for ERVs, with fan efficacies ranging 2-6 cfm/Watt significantly exceeding global averages.

Nordic countries including Finland, Sweden, and Norway maintain particularly precise ventilation regulations, with Finland requiring interior temperatures between 18-32°C and comprehensive air quality monitoring systems. The European Green Deal and circular economy principles drive innovation toward bio-based materials and recyclable ventilation system components, creating opportunities for sustainable technology manufacturers.

Asia Pacific Ventilation Equipment Market Trends

Asia Pacific emerges as the fastest-growing regional market, expected to expand at 10.1% CAGR during the forecast period, driven by rapid urbanization, industrial expansion, and substantial government infrastructure investments. China dominates with an anticipated market value of USD 5.72 billion for 2025, supported by disposable income growth of approximately 9.3% from 2022 to 2024 and government megaproject investments exceeding USD 1,000 billion.

India represents exceptional growth potential with construction market projections reaching INR 25.31 trillion by 2025, driven by the "Make in India" initiative and Pradhan Mantri Awas Yojana housing programs. The Indian government allocated USD 6,443.5 million in June 2022 for affordable housing development, creating substantial ventilation system demand.

Japan and South Korea anchor the premium technology segment, with Japan's METI providing USD 2.8 billion in heat-pump subsidies during 2024 catalyzing domestic demand and global exports. Manufacturing advantages including competitive labor costs, integrated supply chains, and proximity to raw materials position Asia Pacific manufacturers favorably for global market expansion.

Competitive Landscape

The global ventilation equipment market exhibits a moderately fragmented competitive structure with established global manufacturers competing alongside regional specialists and emerging technology innovators.

Major players including Daikin Industries, Lennox International, Greenheck Fan Corporation, Systemair AB, and Gree Electric Appliances maintain substantial market positions through diversified product portfolios, extensive distribution networks, and continuous innovation investments.

Companies are pursuing expansion strategies centered on technological advancement, geographic diversification, and strategic acquisitions to capture growth opportunities in high-potential emerging markets. Private equity firms remain active, often acquiring platform companies for add-on acquisitions, while emphasizing talent acquisition and employee retention strategies to address persistent skilled labor shortages affecting the industry.

Key Market Developments:

- In August 2025: Paloma Rheem Holdings announced the take-private acquisition of Fujitsu General for an enterprise value of $1.8 billion, enhancing their combined capabilities in air conditioning and water heating markets while accelerating decarbonization initiatives

- In July 2024: Robert Bosch acquired the global HVAC solutions business from the Johnson Controls-Hitachi Air Conditioning joint venture, expanding their portfolio to include York and Coleman brands in residential and light commercial applications.

- In March 2022: SI Group expanded production capacity for phenolic ester antioxidants at its Jinshan, China facility to meet growing Asia Pacific demand, demonstrating a strategic commitment to serving rapidly expanding Asian automotive and plastics markets requiring advanced ventilation filtration systems.

Companies Covered in Ventilation Equipment Market

- Manrose Manufacturing Ltd.

- Stamm International Corporation

- Zibo Lihua Ventilation Equipment Co. Ltd.

- VES Andover Ltd.

- Daikin Industries, Ltd.

- Lennox International Inc.

- Takasago Thermal Engineering Co. Ltd.

- Systemair AB

- Totech Corporation Inc.

- Greenheck Fan Corporation

- Air System Components Inc.

- Gree Electric Appliances Inc.

- Crompton Greaves Consumer Electricals Ltd.

- Airflow Developments Limited

- Maico Elektroapparate-Fabrik GmbH

- Schaefer Ventilation Equipment

- Carrier Corporation

- Trane Technologies

- Johnson Controls

- Mitsubishi Electric Corporation

Frequently Asked Questions

The global ventilation equipment market is projected to reach US$ 66.1 billion by 2032, growing at a CAGR of 9.2% from 2025.

Market growth is driven by rising indoor air quality concerns, stringent OSHA regulations, and expanding construction activities.

Air Handling Units (AHUs) dominate the market with around 38% share, owing to advanced filtration and strong commercial adoption.

North America leads the global market with a 36% share, supported by strict safety regulations and major infrastructure investments.

Energy Recovery Ventilation systems offer key growth opportunities through enhanced efficiency and support for net-zero energy buildings.

Major players include Daikin, Lennox, Greenheck, Systemair, Gree, Carrier, Trane Technologies, and Johnson Controls.