- HVAC

- Commercial Kitchen Ventilation System Market

Commercial Kitchen Ventilation System Market Size, Share, and Growth Forecast, 2026 – 2033

Commercial Kitchen Ventilation System Market by Technology (DCKV Systems, Constant-Airflow, Heat-Recovery & Energy-Recovery Integrated Systems, Smart Controls & IoT Monitoring), Component (Hoods, Exhaust Fans & Roof Curbs, Ducting & Dampers, Filters, Air Handling Systems, Controls, Sensors & BMS Integration, Fire Suppression Systems & Mounting Accessories), Application (Restaurants, Hotels & Resorts, Institutional Kitchens, Catering & Events, Food Processing & Manufacturing Kitchens, Cloud Kitchen), and Regional Analysis for 2026–2033

Commercial Kitchen Ventilation System Market Share and Trends Analysis

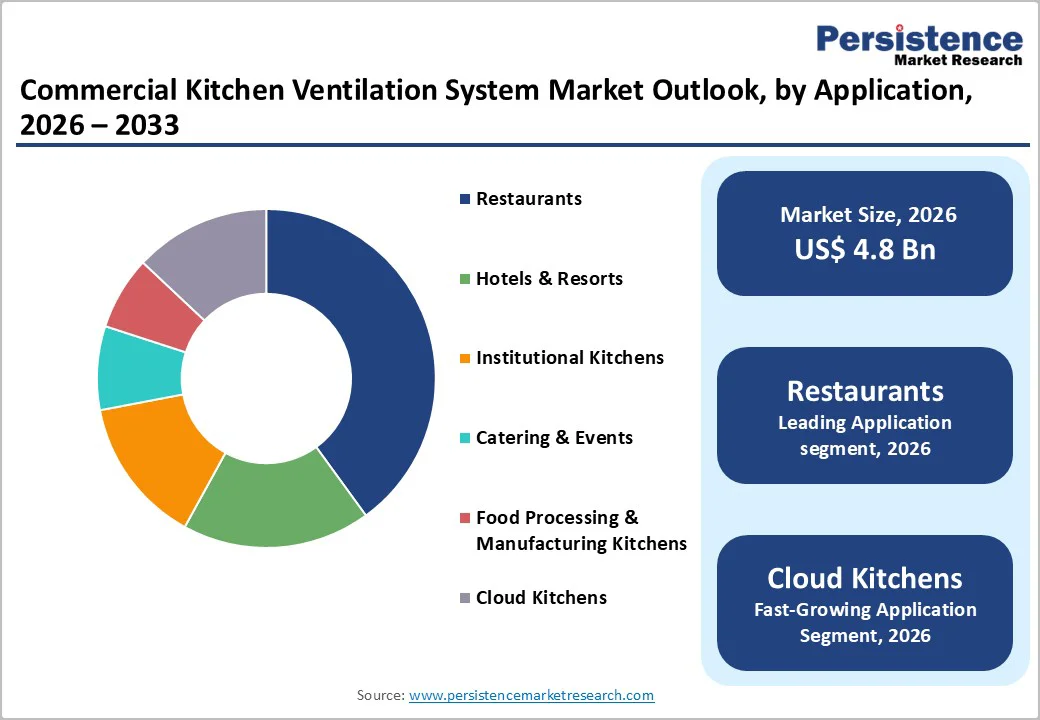

The global commercial kitchen ventilation system market size is likely to be valued at US$ 4.8 billion in 2026, and is projected to reach US$ 7.1 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026-2033. Market growth is supported by stricter indoor air quality standards, greater investment in foodservice infrastructure, and the gradual shift toward energy-efficient ventilation technologies. The increasing adoption of demand-controlled kitchen ventilation (DCKV) systems, rising institutional kitchen expansions, and the continued growth of cloud kitchens contribute to sustained demand. Regulatory frameworks across developed markets also reinforce ventilation upgrades in commercial foodservice facilities.

Key Industry Highlights

- Dominant Technology: DCKV systems are expected to lead in 2026 with about 45% revenue share, driven by increasingly stringent energy-efficiency mandates.

- Fastest-Growing Technology: Smart IoT ventilation is likely to grow the fastest at around 10.8% CAGR through 2033, supported by digital automation of everyday appliances.

- Leading Component: Hoods are projected to dominate with an estimated 46% revenue share in 2026, due to universal kitchen usage.

- Fastest-Growing Component: Controls & sensors are expected to grow the fastest at around 11.5% CAGR from 2026 to 2033, driven by expanding adoption of smart building solutions.

- Dominant Application: Restaurants are likely to lead with approximately 40% revenue share in 2026, supported by high installation needs.

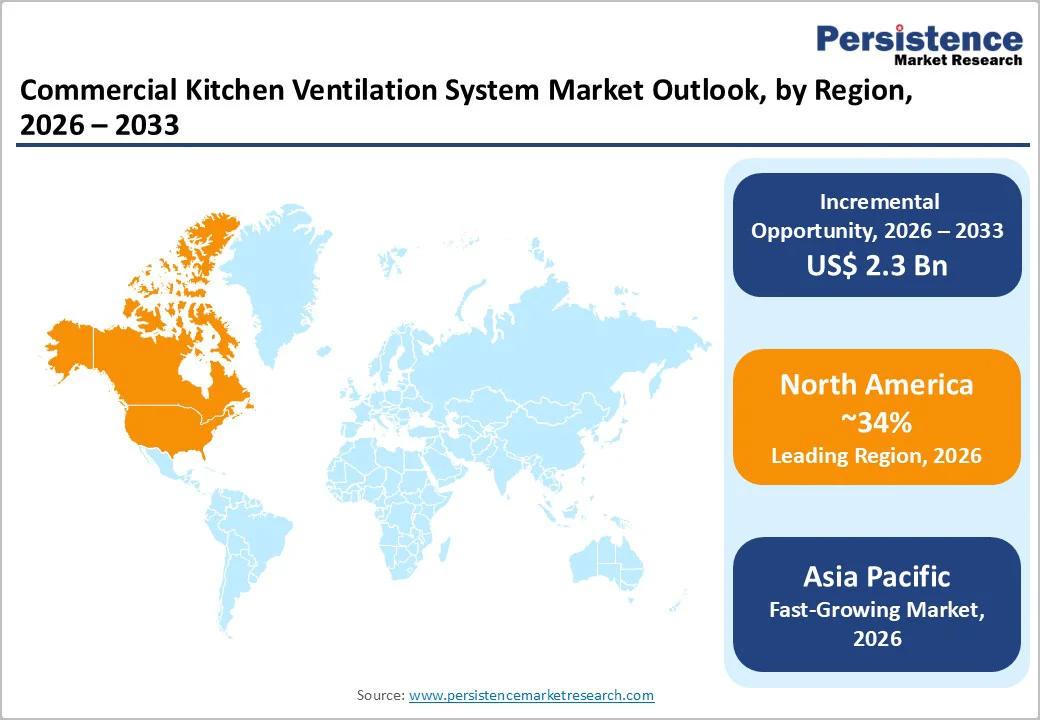

- Leading Region: North America is expected to lead with market share of about 34% in 2026, backed by strict ventilation regulations.

| Report Attribute | Details |

|---|---|

|

Commercial Kitchen Ventilation System Market Size (2026E) |

US$ 4.8 Bn |

|

Market Value Forecast (2033F) |

US$ 7.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Strengthening Regulations for Energy-Efficient Smart Ventilation

Stricter global regulations governing indoor air quality, fire safety, and emission control are compelling commercial kitchens to implement compliant, high-performance ventilation systems and equipment. Regulatory bodies enforce rigorous standards for airflow management, grease capture efficiency, particulate emissions reduction, and thermal comfort maintenance, necessitating equipment upgrades across both new facility construction and existing installations. This compliance imperative intersects with rapid expansion in restaurants, hotels, institutional kitchens, and cloud kitchen operations, substantially increasing demand for advanced exhaust hoods, sophisticated filtration units, and high-capacity ventilation solutions. Modular and compact units are increasingly favored in space-constrained environments such as delivery-only establishments, reflecting modern kitchen design practices and operational flexibility requirements.

Energy efficiency improvements and smart building integration are accelerating market adoption of next-generation ventilation technologies. DCKV systems, heat-recovery equipment, and IoT-enabled monitoring capabilities are progressively displacing traditional constant-airflow installations by delivering measurable energy savings and operational cost reduction. Integration with centralized building management systems enables predictive maintenance protocols, real-time performance monitoring, and enhanced system reliability across multi-unit operations. As energy conservation regulations become more stringent and digital facility management evolves into standard practice, global foodservice operators are increasingly prioritizing intelligent, energy-efficient, and fully compliant ventilation solutions to optimize both capital expenditure and long-term operating expenses.

High Capital Costs and Ongoing Maintenance Burden Limiting Adoption

High initial investment costs present a significant barrier to the adoption of advanced commercial kitchen ventilation systems. Innovations such as demand-controlled ventilation, heat-recovery units, and sensor-based controls require specialized installation, customized ductwork, and seamless integration with existing infrastructure, all of which substantially increase upfront capital expenditure. This cost hurdle is particularly challenging for small restaurants and businesses operating in markets with tight budget constraints. Installation complexity also prolongs project timelines, adding to total ownership costs and discouraging timely upgrades to more efficient or compliant ventilation solutions.

Beyond the initial outlay, the operational maintenance requirements of advanced systems further limit adoption. Commercial kitchens produce heavy grease loads, necessitating regular cleaning of filters, ducts, and hoods to comply with fire safety regulations. Consistent maintenance is vital to prevent equipment breakdowns and avoid regulatory penalties, but it demands skilled technicians and scheduled downtime. For busy kitchens, even brief disruptions in ventilation can affect productivity and profitability. These ongoing maintenance costs and operational risks make some operators reluctant to invest in advanced ventilation systems, thereby constraining broader market expansion and technology uptake in the foodservice sector.

Growing Demand for Smart, Energy-Efficient, and Modular Ventilation Solutions

Automated and sensor-driven ventilation systems represent substantial growth potential across commercial kitchen operations. Demand-controlled kitchen ventilation and IoT-integrated platforms deliver measurable energy conservation and operational efficiency improvements, particularly in hotels, institutional kitchens, and large-scale restaurants. Integration with centralized building management systems enables predictive maintenance scheduling, remote performance monitoring, and optimized airflow distribution that significantly enhance return on investment (ROI). Given that many kitchens continue operating legacy constant-airflow installations, retrofit opportunities for energy-efficient system replacements will remain considerable throughout the coming decade.

Cloud kitchens and delivery-centric foodservice business models are accelerating demand for compact, modular ventilation solutions. Space-constrained facilities require efficient exhaust, advanced filtration, and integrated air-handling systems to manage continuous high-frequency cooking operations while maintaining regulatory compliance. In June 2025, Greenheck introduced its Indoor Ventilation Efficiency (IVE) energy-recovery ventilator, engineered for indoor mounting and delivering 100% outdoor air with integrated heating capabilities to support sustainability objectives and energy performance in confined kitchen environments. Escalating energy expenses and strengthening environmental regulations worldwide are intensifying adoption of intelligent, heat-recovery, and modular ventilation solutions, thereby creating sustained growth opportunities for manufacturers and system integrators serving the global foodservice market.

Category-wise Insights

Technology Insights

DCKV systems are positioned to capture approximately 45% of the commercial kitchen ventilation system market revenue share in 2026, fueled by stringent energy-efficiency regulations and widespread compliance mandates. These systems dynamically adjust airflow in response to cooking activity levels, minimizing fan energy use and reducing heating, ventilation, & air conditioning (HVAC) demands, which proves ideal for restaurants, hotels, and institutional kitchens. North America and Europe lead in adoption, where regulatory frameworks accelerate retrofits and new deployments. Operators benefit from verified efficiency gains and reduced operating expenses, solidifying DCKV dominance and offering converters a stable foundation for market expansion.

Smart and IoT-connected ventilation systems are forecast to achieve the highest growth trajectory at an estimated 10.8% CAGR from 2026 to 2033, propelled by digital monitoring capabilities, predictive maintenance features, and seamless integration with building management systems. CaptiveAire Systems' CAPLink platform illustrates this momentum, combining exhaust hoods, fans, and fire suppression equipment with AI-driven IoT analytics to optimize airflow, slash energy consumption by 40-60%, and enable remote oversight of HVAC and utility functions. Advanced fire safeguards and cloud diagnostics further boost system uptime and return on investment [ROI]. Foodservice providers can leverage these solutions to enhance reliability, comply with evolving standards, and unlock operational efficiencies in increasingly digitized kitchen environments.

Component Insights

Hoods are positioned to dominate the market with approximately 46% market share in 2026, driven by their essential role in grease capture, exhaust regulation, and fire safety compliance. Every commercial kitchen requires a properly sized hood system to maintain safe and efficient operations, establishing this segment as the largest revenue contributor. High installation volumes across restaurants, hotels, and institutional kitchens, combined with strict regulatory adherence, reinforce the market leadership of hoods and canopies. In May 2025, for instance, Greenheck introduced "optics-driven hood controls" that enhance ventilation safety and operational efficiency, exemplifying ongoing innovation in this critical component segment.

Controls, sensors, and building management system (BMS) integration are projected to achieve the highest growth rate at an estimated 11.5% CAGR from 2026 to 2033. Energy-efficient, digitally connected buildings are becoming standard, prompting adoption of advanced sensor systems that enable continuous airflow monitoring, predictive maintenance scheduling, and safety alerts to improve operational reliability. Halton's 2025 integrated IoT ecosystem demonstrates the market shift toward smart, sensor-driven ventilation, supporting energy optimization and real-time monitoring across institutional kitchens and multi-unit restaurant chains. This technological transformation is accelerating growth in the controls and sensors segment throughout the forecast period.

Application Insights

Restaurants, including quick-service restaurants (QSR]), fast-casual, and full-service establishments, are expected to represent approximately 40% of the commercial kitchen ventilation market share in 2026, reflecting the substantial global concentration of dining operations. Ongoing expansion of restaurant chains, modernization initiatives, and regulatory compliance mandates collectively fuel demand for energy-efficient and safety-compliant ventilation systems. High-frequency cooking operations, diverse menu preparation requirements, and elevated customer throughput generate intensive exhaust and air-handling needs, establishing restaurants as the largest end-use segment. For ventilation system suppliers, this segment offers sustained baseline demand and opportunities to support compliance-driven retrofits alongside new installations.

Cloud kitchens are forecast to expand at an estimated 12.6% CAGR from 2026 to 2033, propelled by the accelerating adoption of delivery-only foodservice models across Asia Pacific, North America, and select European markets. These compact, high-output facilities require specialized ventilation solutions capable of managing frequent cooking cycles within constrained floor spaces while maintaining air quality and safety standards. The operational model demands modular, energy-efficient, and digitally enabled ventilation systems that can optimize performance without extensive infrastructure. This rapid evolution makes cloud kitchens the fastest-growing segment in the market, presenting manufacturers and system integrators with differentiated opportunities to develop tailored solutions that address space limitations, energy efficiency targets, and rapid deployment timelines specific to this emerging foodservice format.

Regional Insights

North America Commercial Kitchen Ventilation System Market Trends

North America is projected to remain the largest regional market for commercial kitchen ventilation systems, holding an estimated 34% market share in 2026, underpinned by strict regulatory frameworks, a mature foodservice ecosystem, and broad-based adoption of energy-efficient technologies. The United States generates most of this demand, as indoor air quality rules, National Fire Protection Association (NFPA) fire safety standards, and advanced DCKV adoption in restaurants, hotels, and institutional kitchens drive continuous investment in compliant, high-performance systems. Canada contributes a steady share through ongoing expansion and refurbishment of foodservice infrastructure and adherence to energy-performance and safety requirements in commercial buildings.

Regional growth is further supported by large-scale modernization of aging kitchen facilities and rapid penetration of cloud and multi-unit kitchen networks that require standardized, efficient ventilation designs. Equipment manufacturers increasingly prioritize smart, connected solutions and tight integration with building management systems to improve energy performance, monitoring, and lifecycle cost control. Strong enforcement of health, safety, and energy codes, reinforced by incentives for high-efficiency systems, sustains procurement of advanced exhaust equipment, hoods, and IoT-enabled monitoring platforms, making North America both a stable revenue base and a prime market for technology-driven upgrades across diverse foodservice formats.

Europe Commercial Kitchen Ventilation System Market Trends

Europe maintains a significant market presence, expected to capture an estimated 28% of the commercial kitchen ventilation system market share in 2026, backed by harmonized regulatory frameworks governing energy performance and fire safety. Leading markets such as Germany, the United Kingdom, France, and Spain operate extensive foodservice infrastructures that require modern, compliant ventilation systems. European kitchens have been early adopters of heat-recovery and energy-efficient ventilation technologies, motivated by high energy costs and stringent sustainability mandates imposed by European Union (EU) policies and national legislation.

Market growth is further enhanced by rising adoption of IoT-enabled and digitally connected ventilation solutions in hotels, institutional kitchens, and restaurant chains. Green building retrofits and compliance with EU energy performance standards drive demand for advanced exhaust, filtration, and control equipment. Manufacturers respond by focusing on technological innovation, offering solutions that align with regulatory and environmental goals. The persistent emphasis on energy efficiency and indoor air quality ensures sustained demand for modern, high-performance kitchen ventilation systems, positioning Europe as a stable and innovation-driven market segment.

Asia Pacific Commercial Kitchen Ventilation System Market Trends

The Asia Pacific market is projected to record the highest growth at an estimated 9.2% CAGR from 2026 to 2033, supported by rapid urbanization, expansion of restaurant chains, and rising development of institutional and cloud kitchens across China, India, Japan, and ASEAN countries. China serves as the largest national market in the region, with extensive foodservice networks and progressive upgrades to kitchen safety and ventilation standards. India and Southeast Asian economies are also adopting delivery-only and high-output kitchen formats at pace, which creates sustained demand for compact, efficient, and compliant ventilation solutions designed for intensive cooking in constrained spaces. Industry analyses consistently highlight Asia Pacific as a key growth engine for commercial kitchen ventilation equipment because of this combination of demographic expansion, urban infrastructure build-out, and rising foodservice penetration. ?

Japan and South Korea lead regional progress in advanced air quality management and energy performance, which accelerates uptake of heat-recovery units and digitally integrated ventilation platforms. Competitive manufacturing ecosystems, together with rising investment in commercial real estate, hospitality assets, and food processing facilities, further reinforce system demand across the region. The convergence of dense urban populations, sustained restaurant and hospitality growth, and a strong focus on energy-efficient, smart, and automated kitchens positions Asia Pacific as the fastest-growing and strategically critical regional market for commercial kitchen ventilation systems, offering long-term opportunities for manufacturers, integrators, and investors that tailor solutions to local regulatory and operational requirements.

Competitive Landscape

The global commercial kitchen ventilation system market structure is moderately consolidated, with leadership centered on major players such as CaptiveAire, Halton Group, and Greenheck. These established companies prioritize the development of energy-efficient hoods, advanced DCKV systems, and IoT-integrated solutions tailored for restaurants, hotels, and institutional facilities. Their engineering expertise ensures robust compliance with stringent air quality, fire safety, and energy performance regulations. Strategic investment in smart controls and predictive maintenance technologies enhances operational efficiency and significantly reduces energy expenditures for end-users. Furthermore, extensive distribution networks combined with comprehensive after-sales support reinforce customer loyalty and market reach, while integrated supply chains guarantee high component quality, securing their long-term dominance in high-volume and technologically advanced market segments.

Emerging regional players are also steadily enlarging their market share by offering compact, modular, and cost-effective ventilation systems specifically designed for cloud kitchens and delivery-centric foodservice models. Their flexible manufacturing and installation capabilities facilitate rapid deployment across diverse and often constrained kitchen layouts. The adoption of IoT-based monitoring, energy optimization tools, and specialized retrofitting solutions is a key driver of their growth. By focusing on affordability, seamless digital integration, and strict adherence to local safety and energy codes, these companies are enhancing their competitiveness. Targeted product offerings for emerging economies enable them to capture high-growth opportunities, with their influence expanding notably across Asia Pacific and other rapidly developing markets where cost-efficiency and adaptability are paramount.

Key Industry Developments

- In December 2025, Master Fire Mechanical expanded its commercial kitchen build-out operations in Brooklyn, enhancing service capacity for New York City restaurants through integrated fire suppression, mechanical systems, and kitchen equipment installation offerings. The expansion strengthens the company's ability to support rapid kitchen modernization and compliance requirements across the competitive NYC foodservice market.

- In November?2025, Greenheck added HCDR?051 light-duty round control damper to its industrial control damper line. The new model provides tight airflow control with low leakage, supporting pressures up to 6 in.?wg and velocities up to 3000?fpm, enhancing flexibility and efficiency for ventilation and HVAC installations.

- In July?2025, Halton published the updated Environmental Product Declarations (EPDs) for its commercial kitchen ventilation systems. This milestone marks its commitment to environmental transparency by providing independently verified lifecycle impact data, helping clients meet sustainability and green?building certification requirements.

Companies Covered in Commercial Kitchen Ventilation System Market

- Halton Group

- Greenheck Fan Corporation

- CaptiveAire Systems Inc.

- Systemair AB

- Rational AG

- Vent-A-Hood

- Fantech

- Munters Group

- Addison HVAC

- Daikin Industries

- Fujitsu General

Frequently Asked Questions

The global commercial kitchen ventilation system market is projected to reach US$ 4.8 billion in 2026.

Regulatory mandates for indoor air quality and fire safety, expansion of foodservice and institutional kitchens, rising energy costs, and adoption of DCKV and IoT-enabled ventilation systems for operational efficiency are driving the market.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Opportunities include the adoption of DCKV and smart/IoT ventilation systems, cloud kitchen expansion, heat- and energy-recovery technologies, retrofitting of aging kitchens, and growth in Asia Pacific and Middle East markets.

CaptiveAire, Halton Group, Greenheck, Lakeside Manufacturing, and Faber Ventilation are few of the key players in the market.