- Specialty & Fine Chemicals

- Vapor Recovery Services Market

Vapor Recovery Services Market Size, Share, and Growth Forecast 2026 - 2033

Vapor Recovery Services Market by Service Type (Installation & Commissioning Services, Operation & Maintenance Services, Testing & Certification Services, Consulting & Compliance Services, Others), by Technology Serviced (Carbon Adsorption Systems, Compression-Based Vapor Recovery Units, Absorption Systems, Hybrid Systems, Others), Industry, and Regional Analysis, 2026-2033

Vapor Recovery Services Market Size and Trend Analysis

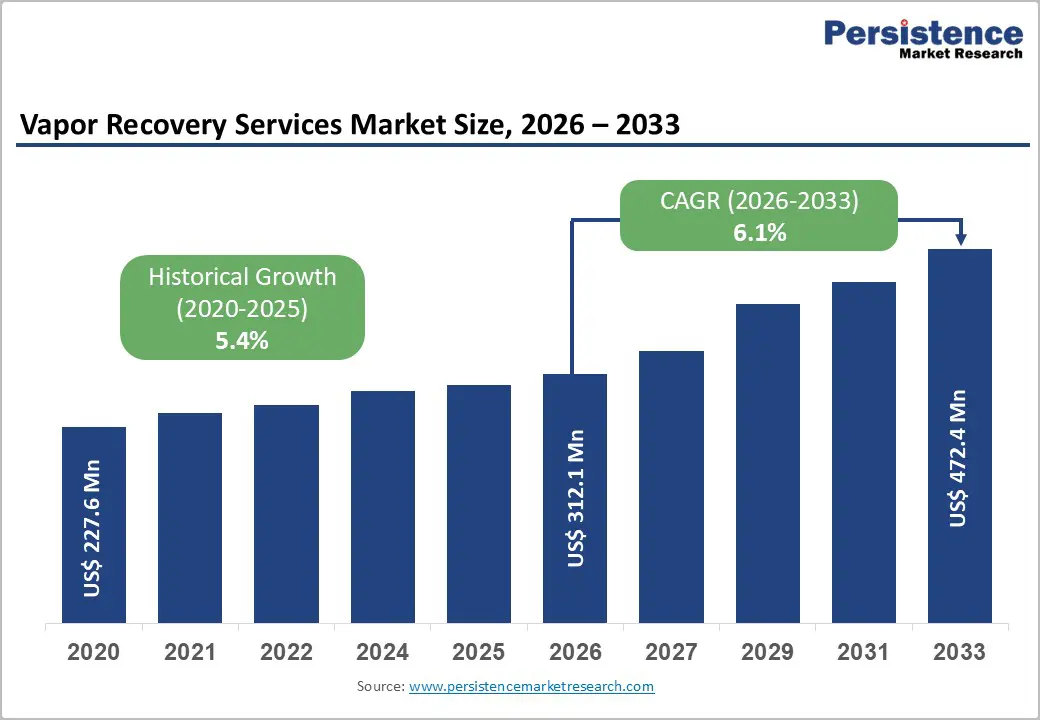

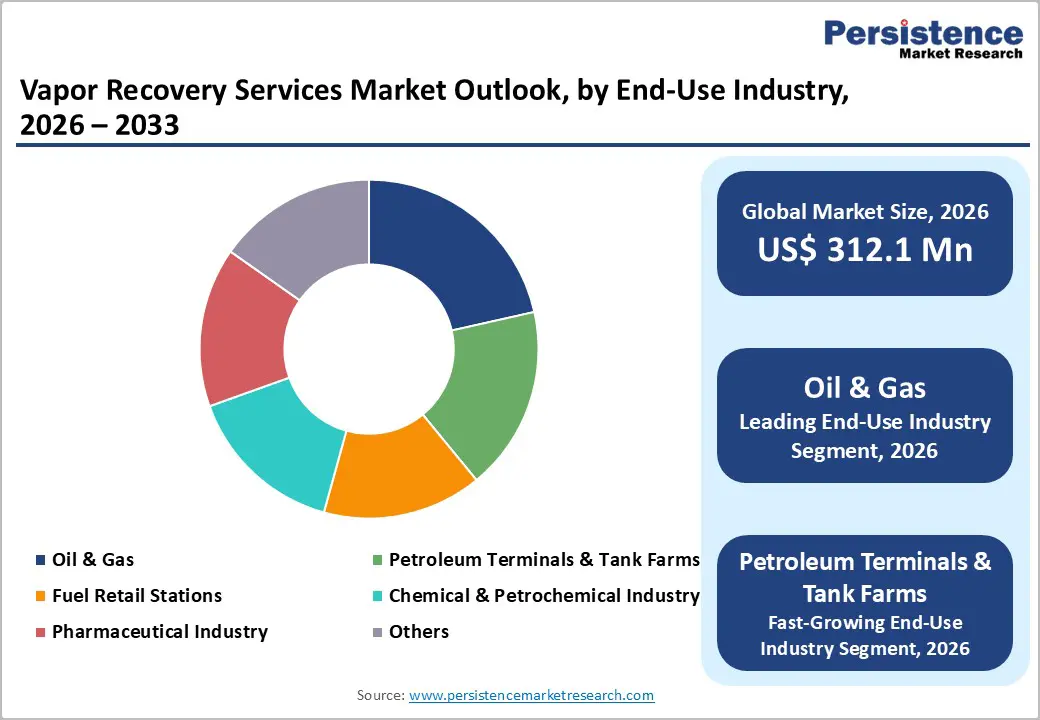

The global vapor recovery services market size is expected to be valued at US$ 312.1 million in 2026 and projected to reach US$ 472.4 million by 2033, growing at a CAGR of 6.1% between 2026 and 2033. Market growth is driven by stringent environmental regulations mandating control of volatile organic compound (VOC) emissions across industrial operations.

Regulatory enforcement by agencies such as the U.S. Environmental Protection Agency (EPA) compels industries to adopt compliant vapor recovery solutions. Oil & gas facilities, petroleum terminals, and chemical plants increasingly invest in vapor recovery services to minimize emissions, prevent product losses, improve operational safety, and support long-term sustainability and environmental compliance objectives.

Key Industry Highlights:

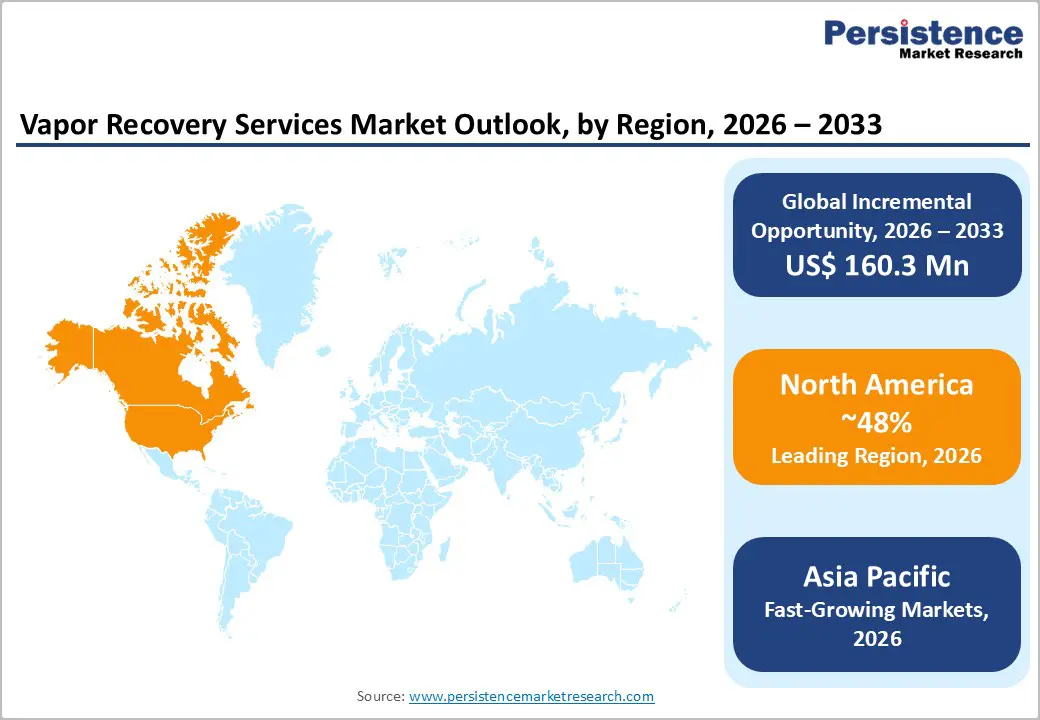

- Leading Region: North America leads the global Vapor Recovery Services market with 48% share in 2025, supported by stringent EPA regulations, mature compliance infrastructure, and high service demand across refineries, terminals, and fuel retail networks.

- Fastest-Growing Region: Asia Pacific holds approximately 32% market share and represents the fastest-growing region, driven by rapid industrialization, expanding refinery capacity, and tightening emission control regulations across China, India, and ASEAN economies.

- Leading Category: Operation & Maintenance Services dominate the market with a 38% share, fueled by recurring requirements for inspections, system optimization, adsorbent replacement, and compliance-driven performance monitoring.

- Fastest-Growing Category: Carbon Adsorption Systems lead the technology landscape with a 42% share, benefiting from proven VOC recovery efficiency, operational reliability, and widespread adoption across petroleum and chemical facilities.

- Key Market Opportunity: Hydrogen economy integration and carbon capture convergence present a key long-term opportunity, enabling hybrid vapor recovery solutions that support decarbonization goals, regulatory alignment, and carbon credit monetization.

| Report Attribute | Details |

|---|---|

|

Vapor Recovery Services Market Size (2026E) |

US$ 312.1 million |

|

Market Value Forecast (2033F) |

US$ 472.4 million |

|

Projected Growth CAGR(2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

5.4% |

Market Dynamics

Drivers - Regulatory Mandate for VOC Emission Control

Environmental compliance remains the primary driver accelerating adoption of vapor recovery services worldwide. Regulatory frameworks such as the U.S. EPA’s NSPS OOOOb, along with comparable standards across Europe and the Asia Pacific, mandate vapor collection efficiencies ranging from 90% to 98% for storage tanks, loading terminals, and processing facilities. Failure to comply can result in penalties exceeding US$ 25,000 per day, pushing operators toward reliable service providers.

Petroleum terminals, chemical manufacturing facilities, and fuel retail stations are subject to particularly strict monitoring and reporting requirements. As regulations evolve and enforcement intensifies, operators increasingly rely on professional vapor recovery services for system installation, commissioning, periodic testing, and certification. Continuous compliance has become critical for maintaining operating permits, driving sustained demand for specialized vapor recovery expertise.

Energy Efficiency and Economic Recovery Benefits

Beyond regulatory compliance, vapor recovery services offer compelling economic advantages by capturing hydrocarbon vapors that would otherwise be lost. Advanced solutions using carbon adsorption, compression-based units, and hybrid technologies enable recovery of valuable fuel products, often generating annual savings of US$ 8,000 to US$ 15,000 per mid-sized terminal. These recovered vapors directly improve operational efficiency and reduce product losses.

Integrated operation and maintenance services further enhance system performance by minimizing downtime, optimizing energy usage, and ensuring consistent recovery rates. Many industrial operators now view vapor recovery as a high-return investment, with payback periods of 18 to 36 months. The combined financial and sustainability benefits strengthen corporate environmental credentials while improving long-term cost efficiency.

Restraints - High Capital Investment and Complex Installation Requirements

Deployment of vapor recovery systems requires significant upfront capital investment, typically ranging from US$50,000 to over US$200,000, depending on facility scale, vapor volumes, and selected technology. This cost burden poses a major restraint for small and mid-sized operators, particularly independent fuel stations and regional chemical processors with limited financial flexibility.

In addition to equipment costs, installation involves complex engineering requirements, facility retrofitting, and temporary operational downtime during commissioning. Integration of pipelines, control systems, and safety infrastructure further increases project complexity. These challenges are especially pronounced in emerging markets, where capital constraints and limited technical infrastructure slow adoption despite increasing regulatory pressure.

Technical Complexity and Service Provider Shortage

The vapor recovery services market is constrained by a shortage of skilled service providers capable of handling advanced system design, installation, and maintenance. Technologies such as carbon adsorption optimization, compression-based unit calibration, and hybrid system diagnostics require specialized expertise typically concentrated among a limited number of global suppliers and authorized partners.

This imbalance leads to longer project timelines and higher service costs, particularly in the Asia Pacific, Latin America, and the Middle East & Africa. Many operators must depend on international service teams or long-term contracts, increasing operational expenses and limiting widespread market penetration in remote or underdeveloped regions.

Opportunity - Rapid Industrialization in the Asia Pacific and Emerging Market Expansion

Rapid industrial growth across the Asia Pacific presents a major opportunity for vapor recovery service providers. China’s continued expansion of refining, petrochemical, and storage infrastructure, supported by national emission reduction mandates, is accelerating adoption of advanced vapor recovery solutions. Government-led industrial policies increasingly emphasize compliance with emissions regulations, thereby driving demand for installation, commissioning, and maintenance services.

Similarly, India, Vietnam, Indonesia, and other ASEAN countries are witnessing refinery construction and petroleum storage expansion to meet rising energy demand. These underpenetrated markets offer strong opportunities for service providers to establish regional footprints, train local technicians, form strategic partnerships, and benefit from first-mover advantages as emission standards tighten.

Hydrogen Economy Development and Carbon Capture Integration

The transition toward a hydrogen-based energy ecosystem and the integration of carbon capture create new growth avenues for vapor recovery services. Advanced hybrid systems capable of recovering hydrocarbon vapors while simultaneously reducing CO emissions align closely with industrial decarbonization strategies. Energy companies increasingly seek integrated solutions that improve efficiency and support long-term carbon reduction goals.

Leading technology providers are developing combined vapor recovery and carbon management systems, enabling operators to optimize emissions control and participate in carbon credit programs. Government incentives, carbon taxation frameworks, and sustainability-linked financing further enhance adoption, driving demand for specialized consulting, system integration, and performance certification services.

Category-wise Analysis

Service Type Insights

Operation & maintenance services represent the leading category within the vapor recovery services market, accounting for approximately 38% share in 2025. The dominance of this segment is supported by continuous operational needs, including routine inspections, compressor servicing, adsorbent media replacement, and system performance monitoring to maintain recovery efficiencies above regulatory thresholds. Recurring service contracts generate stable revenues that often exceed initial installation costs, strengthening long-term service demand.

Installation & commissioning services emerge as the fastest-growing category, driven by infrastructure expansion in emerging markets and first-time regulatory compliance requirements. New terminal construction, refinery upgrades, and fuel station retrofits increase demand for specialized engineering, system integration, and start-up validation services across diverse industrial environments.

Technology Serviced Insights

Carbon adsorption systems are expected to account for approximately 42% of the market in 2026, given their proven effectiveness in achieving high VOC recovery rates. Activated carbon technology benefits from operational reliability, established supply chains, and cost-efficient service requirements, making it widely adopted across petroleum terminals, refineries, and chemical facilities. Standardized service protocols further support large-scale deployment and consistent system performance.

Compression-based vapor recovery units are the fastest-growing technology segment, driven by advances in compressor efficiency, system flexibility, and digital monitoring capabilities. Operators increasingly adopt these systems to modernize aging infrastructure, reduce energy consumption, and enhance operational control while meeting evolving environmental and sustainability objectives.

Industry Insights

The oil & gas industry dominates the vapor recovery services market, accounting for approximately 44% share due to extensive vapor generation across upstream storage, midstream transportation, and downstream refining operations. Stringent regulatory frameworks, methane-reduction initiatives, and corporate sustainability targets drive consistent demand for professional vapor-recovery services across integrated petroleum value chains.

Petroleum terminals & tank farms are the fastest-growing end-use segment as global fuel logistics infrastructure modernizes. Increasing throughput volumes, expanded storage capacity, and tighter emission monitoring requirements drive the adoption of advanced vapor recovery solutions tailored to terminal-specific operational and compliance needs.

Regional Insights

North America Vapor Recovery Services Market Trends and Insights

North America leads the global vapor recovery services market, accounting for approximately 48% market share, supported by mature regulatory frameworks and strong enforcement mechanisms. The United States maintains regional dominance through EPA regulations, such as NSPS and gasoline dispensing standards that mandate high vapor recovery efficiency. Petroleum terminals, refineries, and fuel distribution facilities rely heavily on certified installation, testing, and maintenance services to ensure compliance and operational continuity.

Canada complements regional growth through comparable emission standards enforced by Environment and Climate Change Canada (ECCC). The increasing emphasis on methane reduction, sustainability reporting, and corporate environmental accountability continues to drive demand for advanced vapor recovery services across both upstream and downstream petroleum operations.

Europe Vapor Recovery Services Market Trends and Insights

Europe represents a mature and compliance-driven market, supported by stringent EU environmental directives governing industrial emissions and air quality standards. Countries including Germany, France, the United Kingdom, and Spain maintain strict vapor recovery requirements across petroleum terminals, chemical plants, and fuel distribution networks. Established service providers benefit from long-term contracts focused on system optimization and regulatory adherence.

The European Vapor Recovery Services market is projected to grow at a moderate CAGR of around 6%, driven by regulatory updates, sustainability mandates, and circular economy initiatives. Increasing monetization of recovered vapors and energy efficiency improvements are expanding service demand beyond compliance toward value-added operational enhancements.

Asia Pacific Vapor Recovery Services Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, holding an estimated 32% global market share, driven by rapid industrialization and expanding refinery infrastructure. China dominates regional demand through large-scale petrochemical expansion and emission-control mandates under its national air-quality initiatives. Regulatory alignment with international standards accelerates the adoption of modern vapor recovery services.

India, Southeast Asia, and select ASEAN economies present strong growth potential as environmental governance strengthens and fuel consumption rises. New refinery projects, storage terminal expansion, and tightening emission regulations create opportunities for service providers to establish regional networks and capture early-stage market demand.

Competitive Landscape

The vapor recovery services market is moderately consolidated, with leading service providers collectively accounting for approximately 52% of total market share. Market leadership is driven by strong technological capabilities, deep regulatory expertise, and long-standing relationships with large industrial clients. High capital requirements, specialized engineering skills, and compliance-driven service models create entry barriers, favoring established players with scalable operations and multi-technology service portfolios.

Smaller regional and niche providers remain competitive by offering localized knowledge, faster response times, and cost-efficient solutions tailored to specific facility needs. Competitive differentiation increasingly centers on digital monitoring, predictive maintenance, emissions analytics, and integration of sustainability and carbon management services, expanding market competition beyond traditional vapor recovery operations.

Key Developments:

- In June 2024, Ingersoll Rand introduced enhanced compression-based vapor recovery systems incorporating variable frequency drive technology, reducing energy consumption by 15-18% while expanding operational flexibility across diverse vapor flow rate conditions in petroleum and chemical applications.

- In March 2024, John Zink Hamworthy launched AI-driven vapor recovery units with real-time emissions tracking and predictive maintenance, improving system efficiency by 20% and reducing unplanned downtime across refinery and petroleum terminal operations.

- In October 2023, Flogistix announced its expanded participation in the Abu Dhabi International Petroleum Exhibition and Conference (ADIPEC), showcasing advanced vapor recovery and methane-reduction solutions to Middle East & Africa petroleum operators and regional service providers.

Companies Covered in Vapor Recovery Services Market

- John Zink Hamworthy Combustion

- Dover Corporation (PSG/Blackmer)

- Cimarron Energy

- AEREON

- Zeeco

- Hy-Bon/EDI

- Petrogas Systems

- Ingersoll Rand

- Evonik Industries

- BORSIG GmbH

- Cool Sorption

- Flogistix

- VOCZero

- KAPPA GI

- Kilburn Engineering

- Dürr AG

- Zeppelin Systems

- Whirlwind Methane Recovery Systems

Frequently Asked Questions

The global Vapor Recovery Services market is expected to reach US$ 312.1 million in 2026, up from US$ 227.6 million in 2020, reflecting growing adoption across petroleum, chemical, and manufacturing sectors.

Primary growth drivers include stringent VOC regulations (EPA NSPS OOOOb, EU Directive 2010/75/EU) and economic returns from recovered hydrocarbons

North America leads with 48% global share in 2025, supported by mature regulations, dense petroleum infrastructure, and established service provider networks.

Fastest growth opportunity lies in integration with hydrogen economy and carbon capture, enabling hybrid systems capturing hydrocarbon vapors and CO₂, supported by carbon credit incentives.

Market key leaders for Vapor Recovery Services market are John Zink Hamworthy Combustion, Dover Corporation (PSG/Blackmer), Cimarron Energy, AEREON, and Zeeco.