- Home Appliances

- Europe UK, and Australia Electric Blanket Market

Europe UK, and Australia Electric Blanket Market Size, Share, and Growth Forecast, 2026 - 2033

Europe UK, and Australia Electric Blanket Market by Product Type (Under Blankets, Over Blankets, Misc.), Material Type (Wool, Cotton, Polyester, Acrylic, Misc.), Size (Single Size, Double Size, King Size.), End-user (Commercial, Residential.), Distribution Channel (Supermarkets and Hypermarkets, Specialty Stores, Online Stores, Misc.), and Regional Analysis for 2026 - 2033

Europe UK, and Australia Electric Blanket Market Size and Trends Analysis

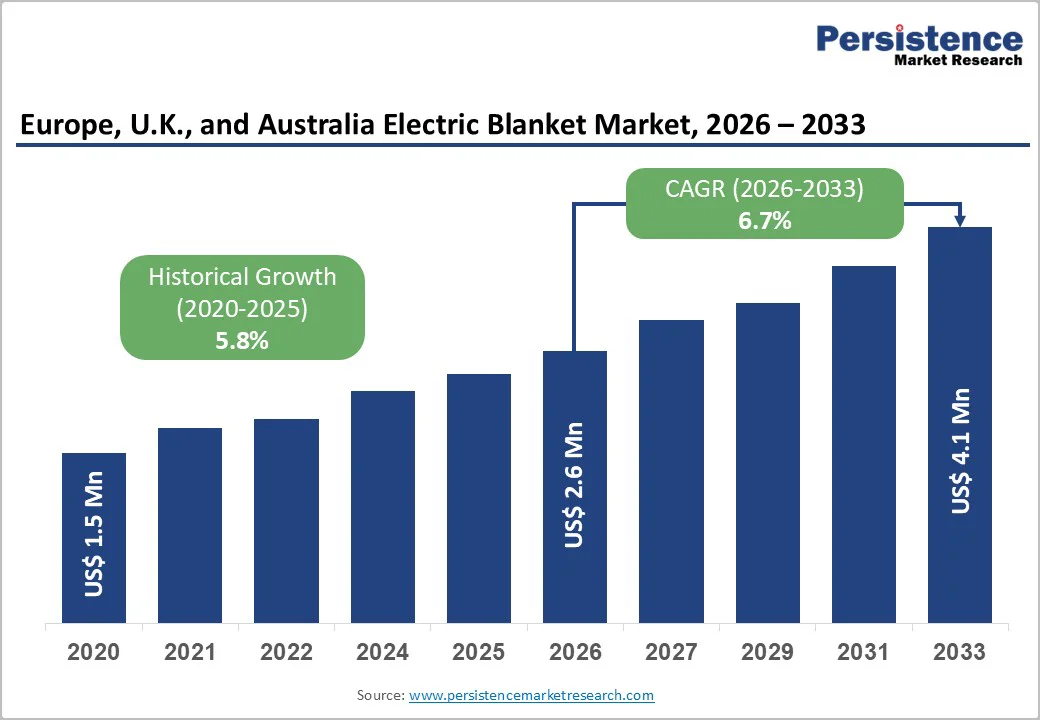

Europe, U.K., and Australia electric blanket market size is likely to value at US$ 2.6 billion in 2026 and is projected to reach US$ 4.1 billion by 2033, growing at a CAGR of 6.7% between 2026 and 2033.

Market expansion is driven by rising energy costs compelling households to adopt cost-efficient heating solutions, increased consumer awareness validated through multinational preference studies, and heightened regulatory initiatives promoting product safety and certification.

Economic pressures across Europe and the U.K., combined with demographic shifts toward aging populations requiring accessible heating alternatives, reinforce sustained market momentum. Government-backed distribution programs targeting vulnerable households further accelerate adoption, positioning electric blankets as a mainstream residential heating solution across the three regions.

Key Industry Highlights:

- Energy-cost concerns continue to accelerate adoption, with low operating costs (2-4p/hour) driving mass consumer shift toward electric blankets across Europe, the U.K., and Australia.

- Over-blankets retain dominant product leadership with a 51% market share in 2025, supported by strong consumer familiarity and extensive retail distribution.

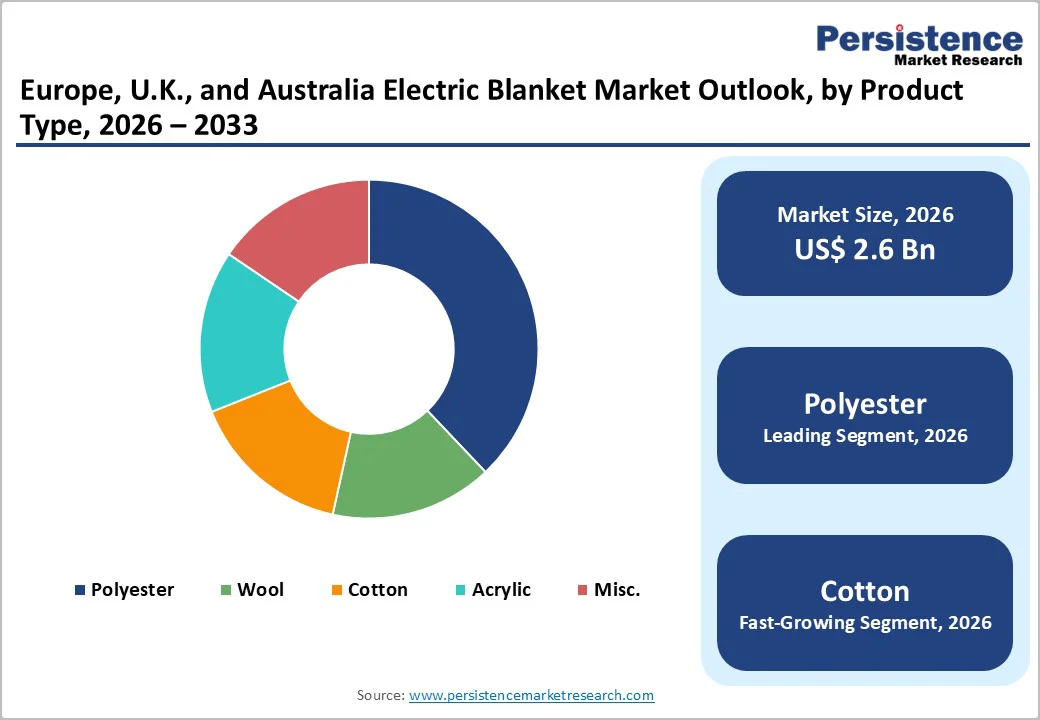

- Polyester-based electric blankets hold 58% material share, driven by durability, washability, and cost-efficient production aligned with hygiene-focused consumer behavior.

- Residential use remains the largest end-use category with a 78% market share, reinforced by utility-backed distribution initiatives and household affordability pressures.

- Safety-compliance enforcement remains a critical market driver, with inspection failure rates of 17-38% pushing consumers toward certified, high-quality branded products.

- Hygiene-enhanced electric blankets emerge as a key opportunity, with rising demand for washable and antimicrobial designs following documented bacterial and dust-mite risks.

- Institutional partnerships with councils and energy suppliers create strong volume opportunities, as large-scale programs from OVO and Octopus Energy distribute tens of thousands of units.

- Under-blankets represent the fastest-growing product trend as consumers increasingly prioritize lightweight designs, enhanced comfort, and premium easy-care fabric technologies.

| Europe, U.K., and Australia Market Attribute | Key Insights |

|---|---|

| Electric Blanket Market Size (2025E) | US$ 2.6 Bn |

| Market Value Forecast (2033F) | US$ 4.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.8% |

Market Dynamics

Drivers - Energy Cost Inflation and Consumer Affordability Pressures

The primary catalyst for market expansion within the Europe, U.K., and Australia Electric Blanket Market stems from sustained energy price escalation and household budget constraints.

Modern electric blankets operate at exceptionally low operating costs approximately 2-4 pence per hour, translating to estimated annual savings of up to £300 per household when deployed as alternatives to whole-home heating systems. During 2022, retailers and market analysts documented an 8% year-on-year surge in electric blanket sales across the U.K., directly attributable to record-high energy bills and inflationary pressures on consumer spending.

Major energy suppliers, including Octopus Energy and OVO, subsequently launched large-scale distribution initiatives providing tens of thousands of free electric blankets to vulnerable populations, validating market expansion through corporate-backed adoption programs. This affordability advantage transforms electric blankets from seasonal novelties into essential household utilities, particularly for fixed-income populations, elderly residents, and families managing constrained winter budgets.

Regulatory Safety Standards and Certification Compliance

Regulatory oversight and consumer safety initiatives have emerged as critical market accelerators within the Europe, U.K., and Australia Electric Blanket Market. Oxfordshire County Council's 2020 safety campaign identified a 17% failure rate among electric blankets, prompting widespread testing infrastructure and contactless inspection programs designed to reduce fire risks and product deterioration hazards.

Milton Keynes City Council documented that 38% of electric blankets failed electrical safety standards during inspection events, triggering coordinated initiatives to replace unsafe units with certified alternatives. These regulatory interventions, supported by fire rescue services and trading standards bodies, have intensified consumer demand for quality-assured products that comply with established safety protocols.

The enforcement environment creates sustained competitive advantage for manufacturers producing certified electric blankets with verifiable safety standards, while simultaneously driving consumer preference away from informal sellers and low-cost non-compliant products.

The widespread regional adoption patterns validate market legitimacy and create psychological confidence among hesitant consumers, directly supporting market expansion and penetration across the Europe, U.K., and Australia region.

Consumer Awareness and Behavioral Adoption Trends

Consumer acceptance and preference validation have accelerated market penetration across the Europe, U.K., and Australia Electric Blanket Market. A February 2018 E.ON multinational consumer study, conducted in collaboration with Kantar EMNID across ten European countries, revealed that electric blankets and heat cushions ranked as the second-most preferred solution for combating cold feet, selected by 29% of respondents.

Regional analysis demonstrated pronounced adoption in countries including Sweden and Germany, where heated blankets established themselves as viable alternatives to traditional hot water bottles. This validation of consumer preference, combined with heightened visibility during seasonal winter transitions and extreme weather events, has normalized electric blanket usage within mainstream household heating portfolios.

Behavioral adoption accelerates through institutional endorsements from energy suppliers, fire services, and municipal councils that collectively communicate product safety and value proposition to target demographics.

Restraints - Safety Compliance Burdens and Product Quality Variability

The electric blanket market faces persistent headwinds from inconsistent product quality standards and compliance complexities. Inspection campaigns consistently reveal failure rates between 17-38% among existing units, indicating widespread distribution of non-compliant or deteriorating products.

Manufacturers must navigate divergent regulatory frameworks across Europe, the U.K., and Australia, requiring substantial investment in certification, testing, and documentation to maintain market access. Supply chain vulnerabilities associated with component sourcing and production quality create competitive pressure for established manufacturers, while simultaneously erecting barriers against rapid market entry.

Warranty obligations, liability exposure, and recall risks associated with safety failures impose significant cost burdens, particularly for smaller producers lacking economies of scale.

Key Market Opportunities

Advanced Safety Technology Integration and Certification Excellence

Emerging consumer health consciousness presents actionable market expansion potential within the Europe, U.K., and Australia Electric Blanket Market. A November 2025 advisory from Homeaglow's hygiene experts highlighted health risks linked to bacteria accumulation, dust mites, and pathogenic contamination resulting from improper cleaning and extended electric blanket usage.

This development catalyzed demand for washable, antimicrobial, and easy-care electric blanket designs that address documented health concerns while commanding premium pricing strategies.

Manufacturers possess clear differentiation opportunities through antimicrobial fabric technologies, enhanced washability protocols, and hygiene-certified product specifications. Premium positioning enables margin expansion and customer loyalty development among health-conscious consumer segments, particularly elderly populations and individuals with respiratory or immunological vulnerabilities.

Market research data from regulatory initiatives and consumer health campaigns directly validates unmet demand for hygiene-enhanced electric blankets, providing strategic justification for innovative investments and product line extensions targeting wellness-focused market segments.

Distribution through Vulnerable Population Support Programs and Public Health Initiatives

Large-scale corporate and municipal distribution initiatives have established proven channels for market expansion across the Europe, U.K., and Australia Electric Blanket Market.

Octopus Energy and OVO's distribution of tens of thousands of complimentary units to vulnerable households, combined with Milton Keynes City Council's replacement programs for non-compliant products, demonstrate institutional purchasing power and recurring demand generation mechanisms.

Fire services, trading standards bodies, and municipal councils have emerged as strategic distribution partners capable of reaching underserved demographics while simultaneously legitimizing product safety and quality standards.

These institutional partnerships create sustained procurement opportunities extending beyond one-time distributions into recurring replacement cycles, maintenance programs, and educational initiatives. Strategic positioning with energy suppliers, healthcare providers, and local authorities enables manufacturers to access captive customer bases while building brand recognition and establishing long-term contractual relationships.

The public-health-anchored distribution model transforms electric blankets from consumer discretionary purchases into subsidized or mandated safety interventions, fundamentally altering market dynamics and creating scalable revenue streams for manufacturers capable of meeting institutional quality and certification requirements.

Geographic Expansion and Cold-Weather Climate Adaptation Strategies

Climate variability and extreme weather intensification present geographic expansion opportunities within the Europe, U.K., and Australia Electric Blanket Market. The November 2025 Met Office forecast of severe freezing temperatures and widespread winter hazards triggered public safety advisories and heightened regulatory scrutiny across the U.K., validating electric blankets as critical seasonal heating solutions during extreme weather events.

Historical climate data and meteorological trends suggest prolonged cold seasons and intensified winter severity across Northern Europe, the U.K., and parts of Australia, supporting sustained demand for heating alternatives.

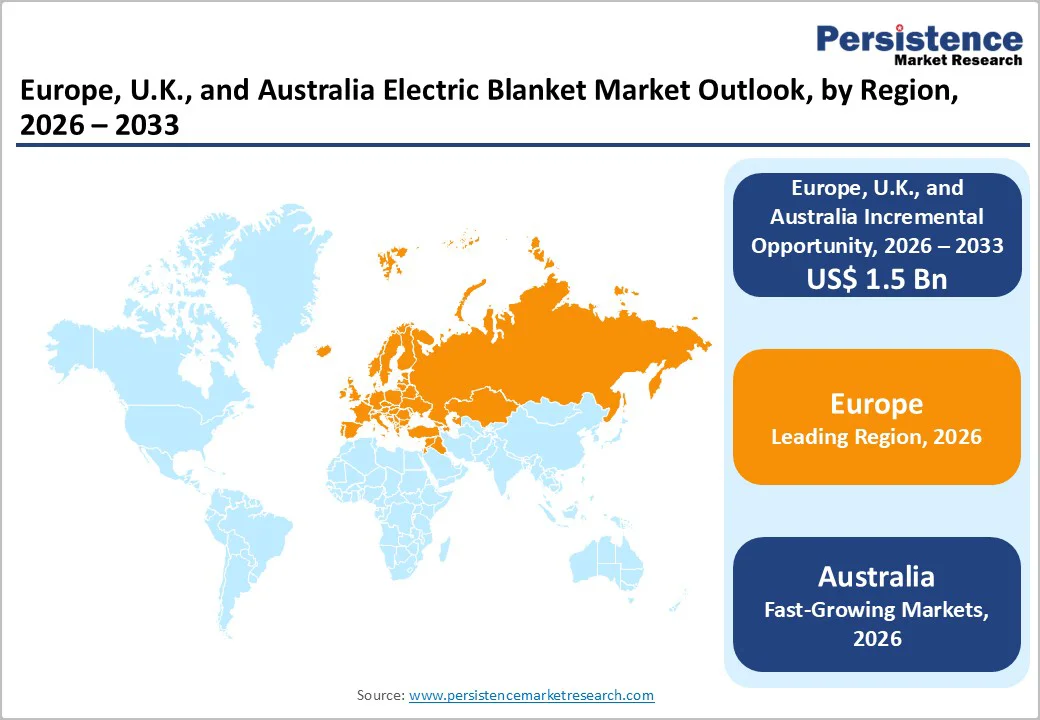

Geographic markets with historically moderate winters including Southern Europe, Northern Australia, and Mediterranean regions present untapped expansion potential as climate volatility drives seasonal heating demand expansion.

Strategic market entry initiatives targeting regions with limited central heating infrastructure, developing economies transitioning toward consumer durables adoption, and seasonally constrained heating markets enable manufacturers to diversify geographic revenue streams.

Regulatory harmonization efforts across European nations and Commonwealth markets create standardized certification frameworks that reduce market-entry barriers and facilitate cross-border product distribution strategies.

Category-wise Analysis

Product Type Insights

Over-blankets maintain dominant market positioning within the Europe, U.K., and Australia Electric Blanket Market, accounting for 51% of product-type segmentation in 2025. This leadership reflects established consumer preference for blankets deployed atop conventional bedding arrangements, offering superior temperature distribution, ease of use, and compatibility with existing sleep environments.

Over-blankets address primary consumer use-cases including supplementary warmth during winter months, reduction of central heating reliance, and thermal comfort optimization for elderly populations and cold-sensitive demographics. Established distribution channels through major retailers, healthcare providers, and institutional procurement processes have solidified over-blanket market penetration across residential and commercial properties.

Market leadership correlates directly with consumer familiarity, regulatory acceptance, and manufacturer product depth. Over-blankets benefit from extensive product differentiation through material composition, size specifications, and technological features including automatic shut-off, timer functions, and dual-temperature controls.

Pricing accessibility and compatibility with diverse bedroom configurations reinforce market incumbency, though commodity price competition constrains margins and limits profitability expansion within the established segment.

Under-blankets represent the fastest-expanding product category within the Europe, U.K., and Australia Electric Blanket Market, driven by consumer preference for under-blanket deployment that eliminates top-layer weight while maximizing thermal efficiency and bedding compatibility.

Under-blankets address user comfort concerns associated with blanket weight, material contact sensitivity, and sleeping position limitations inherent to over-blanket design. Innovative product features, including waterproof materials, machine-washability specifications, and hypoallergenic fabric compositions, position under-blankets as premium alternatives appealing to consumers prioritizing health consciousness and product convenience.

Material Type Insights

Polyester-based electric blankets command 58% material-type market share within the Europe, U.K., and Australia Electric Blanket Market, reflecting established manufacturing infrastructure, cost efficiency, and consumer acceptance.

Polyester composition enables consistent thermal performance, durability across extended use cycles, and machine-washability specifications aligned with emerging hygiene preferences. Manufacturing scalability and established supply chains for polyester textiles facilitate cost-competitive production, supporting price accessibility across consumer income segments and institutional procurement budgets.

Market leadership reflects practical performance characteristics and regulatory compliance alignment. Polyester blankets demonstrate thermal retention properties suitable for European and U.K. winter conditions, while enabling easy-care maintenance protocols addressing documented hygiene concerns.

Commercial viability of polyester-based products has established established manufacturer depth and product diversity, creating barriers against material substitution despite emerging consumer preferences for alternative fiber compositions.

Cotton-based electric blankets represent the fastest-growing material segment within the Europe, U.K., and Australia Electric Blanket Market, driven by consumer perception of cotton as natural, breathable, and hypoallergenic.

Cotton composition aligns directly with health-conscious consumer segments prioritizing antimicrobial properties, reduced chemical exposure, and sustainable material sourcing. Recent hygiene advisories and health-risk warnings have catalyzed demand migration toward cotton alternatives perceived as inherently cleaner and safer than synthetic materials.

End-user Insights

Residential applications dominate the Europe, U.K., and Australia Electric Blanket Market with 78% market share in 2025, reflecting primary consumer usage in private household settings.

Household adoption accelerated substantially through government-backed distribution initiatives and utility company programs targeting residential consumers. Consumer awareness campaigns and safety advisories from fire services have established electric blankets as legitimate residential heating infrastructure rather than supplementary comfort products.

Commercial applications represent the fastest-growing segment within the Europe, U.K., and Australia Electric Blanket Market, driven by adoption in healthcare facilities, hospitality establishments, aged care institutions, and emergency shelters.

Healthcare sector utilization for patient comfort and therapeutic applications creates substantial institutional demand, while hospitality applications address guest comfort requirements during seasonal heating periods. Regulatory safety initiatives and large-scale institutional procurement by government agencies and healthcare systems create structural demand growth pathways for commercially oriented electric blanket variants.

Competitive Landscape

Europe, U.K., and Australia electric blanket market is largely fragmented, with numerous regional brands, private-label offerings from large retailers, and specialist manufacturers competing alongside a handful of well-established companies that command significant retail presence and brand recognition.

Major players shaping the competitive landscape include Beurer GmbH, Glen Dimplex Group, Morphy Richards Ltd., Jarden Corporation, Silentnight Group Ltd., and Biddeford Blankets, LLC, each leveraging differentiated portfolios, retail partnerships, or distribution strength to capture share.

Competition is driven by product innovation (washable and antimicrobial fabrics, multi-zone heating), price promotions through supermarkets and online channels, and increasing retailer private-label penetration.

Regulatory scrutiny and safety-testing initiatives have raised barriers for low-cost entrants, benefiting established companies with compliance capabilities. While many small players persist, the market rewards scale, proven safety credentials, and wide distribution, keeping it fragmented but with clear advantages for the leading companies.

Key Industry Developments

- On 23 October 2025, Octopus Energy and OVO announced major winter support programs to distribute tens of thousands of free electric blankets to vulnerable households. The initiative aims to help elderly and mobility-challenged residents reduce heating expenses, as electric blankets cost only 2-4p per hour to operate. This development strengthens the role of electric blankets as an affordable heating solution across Europe, the U.K., and Australia.

- On 11 October 2022, Kantar and the BRC-KPMG Retail Sales Monitor reported a significant rise in electric blanket sales as households turned to low-cost heating alternatives amid soaring energy bills. Sales of duvets and electric blankets grew 8% year-on-year, reflecting a strong consumer shift toward energy-efficient warming products. This trend accelerated market adoption of electric blankets across Europe, the U.K., and Australia.

Companies Covered in Europe UK, and Australia Electric Blanket Market

- Jarden Corporation

- Beurer GmbH

- Morphy Richards Ltd.

- Glen Dimplex Group

- Biddeford Blankets, LLC

- Snugnights UK LLP

- Odessey Products

- Slumberdown Company

- PIFCO

- Shavel Associates Inc.

- Silentnight Group Ltd.

- CDB Goldair Australia Pty LTD

- ECD Germany

- Dr. Madley

- MAXSA Innovations

- E&E Co. Ltd.

Frequently Asked Questions

Europe, U.K., and Australia Electric Blanket Market is projected to be valued at US$ 2.6 Bn in 2025.

The Polyester segment is expected to account for approximately 58% of the Europe, U.K., and Australia Electric Blanket Market by Material Type Industry in 2025.

Europe UK, and Australia Electric blanket market is expected to witness a CAGR of 6.7% from 2026 to 2033.

The Europe, U.K., and Australia Electric Blanket Market is driven by rising energy costs and affordability pressures, regulatory safety enforcement that pushes demand toward certified products, and growing consumer awareness supported by institutional endorsements and behavioural adoption trends.

Key market opportunities include rising demand for antimicrobial, washable, and hygiene-certified electric blankets, large-scale procurement through energy suppliers and public-health support programs, and geographic expansion driven by colder winters, climate volatility, and emerging regions with limited heating infrastructure.

The key players in Europe, U.K., and Australia Electric Blanket include Beurer GmbH, Glen Dimplex Group, Morphy Richards Ltd., Jarden Corporation, Silentnight Group Ltd., and Biddeford Blankets, LLC,.