- Home Care & Utilities

- Udder Hygiene Market

Udder Hygiene Market Size, Share, and Growth Forecast, 2026 - 2033

Udder Hygiene Market by Chemical Base (Iodine-based, Lactic Acid, Chlorhexidine/Others), by Product Type (Film-forming, Non-film-forming, Udder Creams/Cloth), by End-user (Large Scale Dairy, Scale/Family Farms), and Regional Analysis 2026 - 2033

Udder Hygiene Market Size and Trends Analysis

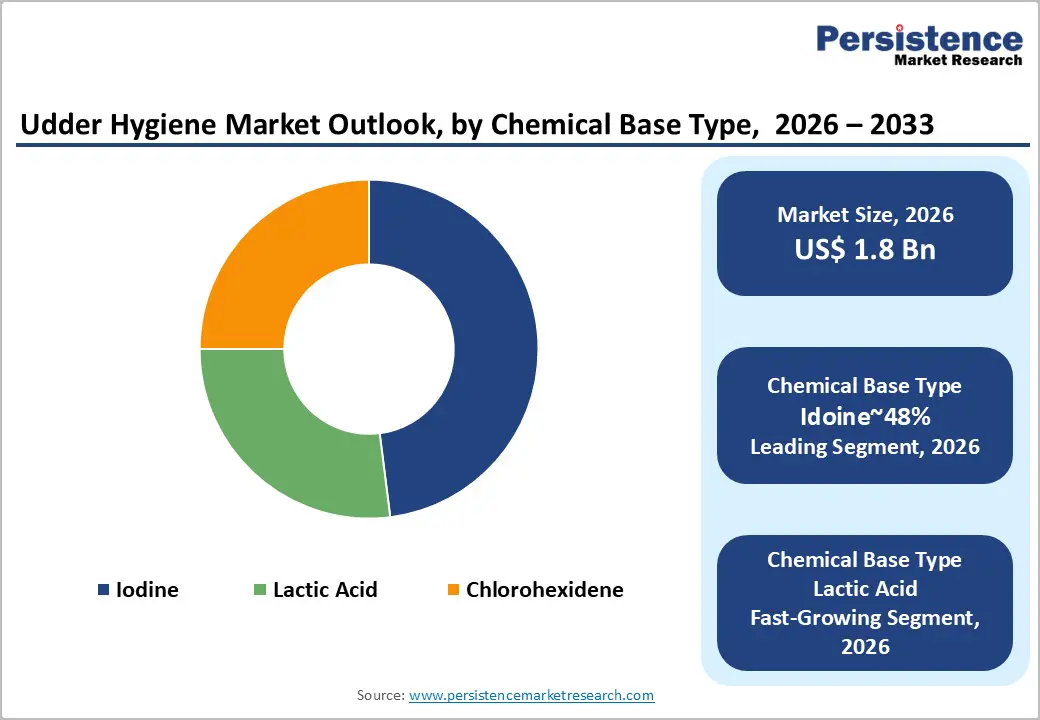

The global udder hygiene market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 6% during the forecast period from 2026 to 2033, driven by the global dairy production expansion, with milk output rising in key markets, including India, necessitating hygiene to curb mastitis.

Growth is further accelerated by the rapid industrialization of dairy farming in emerging economies, necessitating rigorous biosecurity protocols to maintain milk quality standards. The transition toward automated milking systems (AMS) is catalyzing demand for specialized, high-efficiency hygiene formulations compatible with robotics.

Key Industry Highlights:

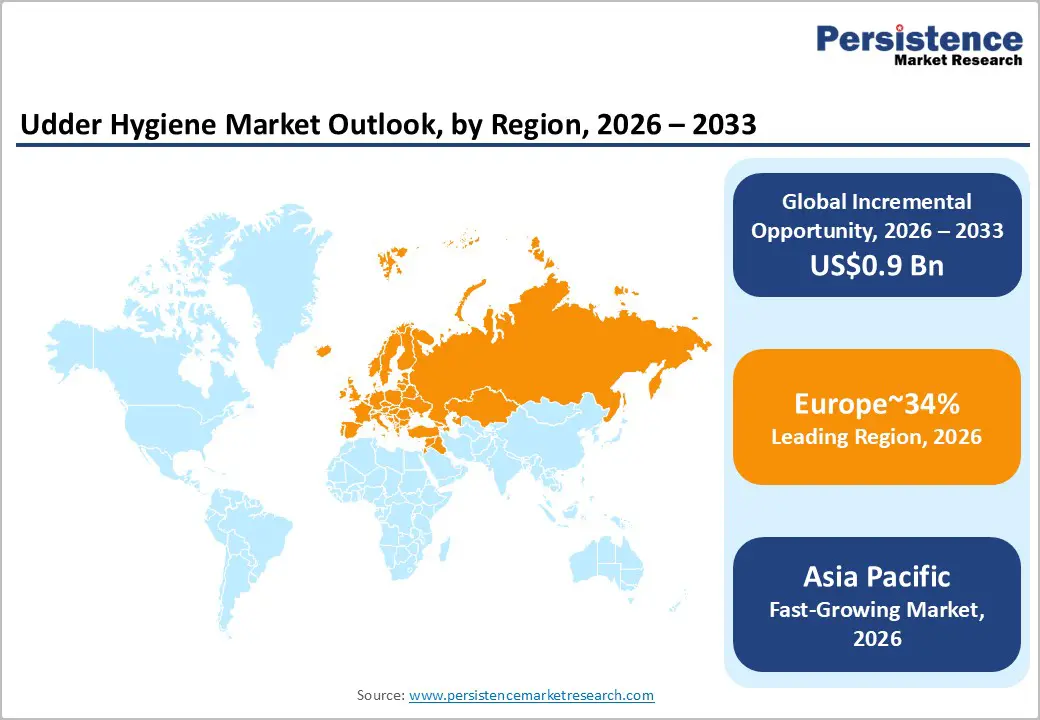

- Leading Region: Europe is projected to lead due to stringent animal welfare regulations, advanced dairy farm management systems, and strong veterinary oversight frameworks, accounting for approximately 34% of the market share.

- Fastest-Growing Region: Asia Pacific is anticipated to grow the fastest, due to rapid dairy sector expansion, policy support for milk productivity improvement, and modernization of farm hygiene practices.

- Leading Chemical Base: Iodine-based formulations are expected to lead with approximately 48%, reflecting broad-spectrum antimicrobial effectiveness, regulatory acceptance, and established industry trust.

- Leading Product Type Segment: Film-forming products are expected to lead, accounting for approximately 55%, driven by superior barrier protection, prolonged antimicrobial efficacy, and compatibility with automated teat-dipping systems.

| Key Insights | Details |

|---|---|

|

Udder Hygiene Market Size (2026E) |

US$1.8 Bn |

|

Market Value Forecast (2033F) |

US$2.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Escalating Milk Quality and Safety Compliance Standards

Stringent milk quality regulations structurally elevate hygiene requirements across dairy systems. Regulators impose residue thresholds and microbial limits within procurement frameworks. Processors enforce compliance through supplier audits and traceability mandates. Failure to meet standards results in shipment rejection and financial penalties. These enforcement mechanisms formalize hygiene as a non-negotiable operational input. Quality certification schemes further institutionalize standardized sanitation protocols. Export-oriented producers face heightened scrutiny across cross-border trade channels. Consequently, preventive udder hygiene becomes embedded within risk mitigation structures.

Safety compliance reshapes procurement and cost allocation. Dairy processors integrate hygiene verification into contractual sourcing arrangements. Advanced testing technologies accelerate the detection of contamination risks. Rapid diagnostics shorten response cycles and limit downstream spoilage exposure. Heightened surveillance increases recurring expenditure on sanitation consumables. Stabilized product quality supports premium pricing and brand integrity. Regulatory harmonization across regions amplifies uniform hygiene benchmarks. This systemic compliance pressure sustains durable demand for udder hygiene solutions.

Persistent Mastitis Burden in Dairy Herds

Sustained mastitis prevalence exerts structural pressure on dairy production economics. The infection reduces milk yield and degrades compositional quality parameters. Elevated somatic cell counts trigger processor penalties and supply rejections. Veterinary treatment and discarded output inflate farm-level operating expenditures. These recurring losses reclassify hygiene inputs as risk management essentials. Preventive sanitation becomes embedded within standardized milking protocols. Producers increasingly institutionalize pre- and post-milking disinfection routines. Such practices reduce pathogen transmission across high-density herd environments.

Mastitis risk reshapes procurement and compliance systems. Processors integrate herd health monitoring within quality assurance frameworks. Digital milking platforms deploy sensors detecting inflammatory biomarkers early. Data integration strengthens the linkage between hygiene inputs and yield stabilization. Regulatory pressure to limit reliance on antibiotics reinforces preventive strategies. Reduced antimicrobial exposure aligns with residue compliance and export mandates. Consequently, hygiene expenditure supports margin protection by preserving quality. This structural burden sustains recurring demand for udder sanitation solutions.

Barrier Analysis - Persistent Reliance on Blanket Antibiotic Protocols

Continued dependence on blanket dry cow therapy constrains preventive hygiene penetration. Producers perceive routine antibiotic administration as operational risk insurance. This practice dampens urgency for investment in advanced sanitation systems. Immediate infection suppression appears more predictable than preventive infrastructure upgrades. Consequently, hygiene inputs remain secondary within certain herd management budgets. The substitution effect limits the adoption of premium products among cost-sensitive farms. Procurement decisions, therefore, prioritize therapeutic expenditure over preventive allocation. This behavioral inertia slows the expansion of structural demand for hygiene solutions.

Antibiotic reliance distorts cost visibility frameworks. Short-term therapeutic spending masks longer-term hygiene investment benefits. Regulatory tightening around antimicrobial stewardship is reshaping compliance expectations. However, uneven enforcement sustains regional inconsistencies in the transition. Milk buyers are increasingly scrutinizing residue management and antibiotic-use disclosures. Elevated compliance risk gradually rebalances economic evaluation models. Technology-enabled infection monitoring challenges indiscriminate treatment protocols. Nevertheless, entrenched operational habits continue to moderate the momentum of preventive hygiene demand.

Scarcity of Veterinary Support Infrastructure

Limited access to qualified veterinary professionals impedes the adoption of preventive hygiene practices. Many dairy regions lack sufficient clinical advisory capacity. Farmers lack structured guidance on mastitis diagnostics and on optimizing protocols. This gap weakens confidence in targeted hygiene and monitoring systems. Reactive treatment, therefore, substitutes for preventive herd health planning. Knowledge asymmetry slows the diffusion of evidence-based sanitation standards. Supply chains face uneven demand signals across underserved geographies. Consequently, hygiene product penetration remains structurally fragmented within rural markets.

Advisory scarcity distorts decision-making frameworks. Without professional oversight, infection identification relies on observable symptoms. Delayed detection increases the severity and the intensity of required treatment. Preventive expenditure appears discretionary without quantified risk assessments. Regulatory compliance also weakens when access to veterinary certification remains limited. Milk quality assurance mechanisms become inconsistent across fragmented production bases. Technology-enabled remote diagnostics partially offset advisory shortages. Nevertheless, constrained institutional support continues to moderate structured hygiene investment.

Opportunity Analysis - Transition toward Green and Bio-Based Hygiene Formulations

Rising environmental scrutiny is reshaping formulation standards across dairy inputs. Concerns about chemical residues influence procurement decisions in regulated milk supply chains. Bio-based teat dips align with evolving sustainability compliance frameworks. Retailers increasingly prioritize traceability and disclosures of low-impact inputs. This shift elevates demand for biodegradable and residue-minimizing solutions. Regulatory pressure on effluent discharge strengthens the adoption of eco-compatible chemistries. Formulation innovation reduces toxicity while preserving antimicrobial efficacy. Consequently, green hygiene products integrate environmental compliance with herd health management.

At the value chain level, bio-based inputs recalibrate cost structures. Raw material sourcing shifts toward renewable feedstocks and certified supply streams. Manufacturers invest in formulation science to maintain performance equivalence. Certification and labeling standards create differentiation within procurement contracts. Processors leverage sustainable inputs to reinforce brand positioning. Export markets reward transparency into residues and environmental stewardship credentials. Technology-enabled formulation stability enhances shelf life viability. These structural dynamics expand addressable demand for sustainable udder hygiene solutions.

Automation Integration for Operational Efficiency

The integration of automation into dairy operations is reshaping hygiene execution frameworks. Robotic milking systems standardize teat preparation and post-milking sanitation cycles. Automated dosing mechanisms reduce variability associated with manual application practices. Consistent hygiene protocols improve compliance with processor quality benchmarks. Labor scarcity further accelerates the transition toward mechanized sanitation processes. Data capture capabilities embed hygiene events within traceability systems. This convergence strengthens accountability across herd health management structures. Consequently, automation elevates hygiene from task execution to systemized control architecture.

Automation reconfigures cost allocation and margin stability. Capital expenditure shifts toward integrated equipment and toward compatibility with consumables. Hygiene product manufacturers adapt formulations for robotic dispensing systems. Sensor-enabled platforms support predictive analytics for mastitis risk detection. Early intervention reduces downstream treatment intensity and milk discard exposure. Regulatory audit readiness improves through digitally recorded sanitation logs. Standardized execution enhances milk quality consistency across large herds. These efficiencies structurally reinforce recurring demand for automation-compatible hygiene inputs.

Category-wise Analysis

Chemical Base Insights

Iodine-based solutions are expected to lead, accounting for approximately 48% share in 2026, underpinned by proven broad-spectrum antimicrobial efficacy across commercial dairy operations. Their effectiveness against contagious and environmental mastitis pathogens supports entrenched use in large herd environments. Established regulatory approvals across major food safety jurisdictions reinforce procurement confidence and qualification continuity. Visible post-application staining enables treatment verification within high-throughput milking workflows. Laboratory-validated kill performance supports somatic cell count management and milk quality stabilization. Mature dairy markets prioritize reliability, volume scalability, and predictable input performance. This combination of regulatory familiarity, validated efficacy, and operational integration sustains iodine-based dominance.

Lactic acid formulations are expected to be the fastest-growing segment, driven by accelerating demand for bio-based and skin-compatible chemistries. Sustainability positioning aligns with environmental compliance pressures and organic milk production standards. Unlike harsher antiseptics, lactic acid supports teat skin conditioning while delivering antimicrobial action. Improved dermal tolerance reduces the risk of hyperkeratosis during intensive milking cycles. Converging efficacy data strengthens substitution potential against conventional iodine systems. Premiumization trends in dairy sourcing incentivize residue-conscious sanitation inputs. Technological refinement in formulation stability enhances shelf life and dispensing compatibility. These dynamics collectively position lactic acid solutions for accelerated adoption across progressive dairy systems.

Product Type Insights

Film-forming products are expected to lead, accounting for approximately 55% share in 2026, underpinned by durable post-milking barrier protection across large commercial dairies. Their polymer-based sealing mechanism prevents bacterial ingress during vulnerable periods of teat canal exposure. Comparative field trials demonstrate superior infection reduction relative to conventional spray formulations. Persistence on teat surfaces enhances compliance within automated milking environments. Large-scale operators prioritize barrier integrity to manage environmental pathogen loads. Integration with robotic systems reinforces consistent application and coverage verification. This combination of physical protection, workflow compatibility, and validated performance sustains film-forming dominance.

Film-forming products are expected to be the fastest-growing segment, driven by continuous innovation in barrier chemistry and application precision. Advanced non-iodine variants address residue concerns while preserving antimicrobial efficacy. Enhanced film elasticity improves breathability without compromising protective durability. Reduced dripping characteristics minimize product wastage and optimize input utilization. Expanding herd sizes intensifies cross-contamination risk within confined housing systems. Automated dispensing technologies further strengthen adoption across modern dairy facilities. Ongoing materials science refinements position film-forming solutions for accelerated uptake within safety-focused production models.

Regional Insights

Europe Udder Hygiene Market Trends

Europe is expected to remain the leading regional market, accounting for approximately 34% in 2026, supported by harmonized regulatory frameworks and structurally embedded animal welfare standards. Regional demand is projected to be reinforced by stringent residue controls, antibiotic stewardship mandates, and cross-border compliance alignment under unified food safety governance. Innovation leadership is likely to be concentrated around DeLaval’s hygiene management platforms, GEA Group’s automated teat spray technologies, Lely’s Astronaut robotic milking systems, and BouMatic’s barrier dip solutions, embedding chemistry within precision equipment ecosystems. Parallel expansion of iodine-alternative and lactic-acid-based portfolios across these platforms is projected to reinforce Europe’s structural leadership in compliance-driven dairy sanitation.

Germany is expected to anchor regional momentum, shaping adoption patterns through precision farming integration and advanced dairy digitization frameworks. National emphasis on data-driven herd management is projected to strengthen interoperability between automated milking systems and hygiene dosing platforms. Environmental policy alignment is anticipated to accelerate the transition toward lactic acid and iodine-alternative formulations within large cooperatives. Precision analytics embedded within farm management software are expected to reinforce preventive hygiene scheduling and compliance documentation. As sustainable dairy positioning deepens within export-oriented supply chains, Germany is positioned to influence broader European procurement standards and innovation pathways.

Asia Pacific Udder Hygiene Market Trends

Asia Pacific is expected to be the fastest-growing region, supported by structural dairy expansion and supply chain modernization. Accelerating milk output across China, India, Japan, and ASEAN economies is anticipated to intensify focus on raw milk quality compliance. Organized dairy consolidation is projected to replace fragmented backyard production with cooperative and commercial herd models. Cost-competitive regional manufacturing is likely to enhance accessibility of iodine and bio-based formulations. Foreign direct investment into dairy technologies is expected to strengthen automation and hygiene system integration. Expanding cold-chain infrastructure is positioned to shift value emphasis toward upstream contamination control and standardized sanitation inputs.

India is expected to anchor regional acceleration through cooperative-led scaling and regulatory hygiene enforcement. National clean milk initiatives are anticipated to institutionalize pre- and post-milking sanitation protocols across organized dairies. Deployment of lactic-based and barrier formulations within expanding herd clusters is projected to enhance consistency in infection control. Investment flows into dairy digitization are likely to integrate hygiene monitoring with yield optimization platforms. As cooperative networks professionalize procurement standards, structured hygiene systems are positioned to outpace global growth trajectories across the region.

North America Udder Hygiene Market Trends

North America is expected to remain a mature and structurally stable market, supported by large-scale herd consolidation and advanced operational infrastructure. Demand is anticipated to be anchored in replacement cycles, compliance-driven upgrades, and automation-linked procurement rather than greenfield dairy expansion. Enterprise-scale dairies are positioned to prioritize efficiency optimization, integrating robotic milking platforms with standardized hygiene dispensing systems. The region’s technology ecosystem, supported by equipment innovators such as DeLaval and GEA, is expected to reinforce compatibility-driven purchasing decisions. Consolidated supplier concentration is likely to maintain disciplined pricing structures and contract-based supply models across high-volume operations.

The U.S. is expected to anchor regional momentum, shaping procurement standards through herd scale, regulatory enforcement, and capital allocation patterns. Federal oversight of antibiotic stewardship is expected to accelerate the adoption of preventive hygiene practices in large commercial dairies. The expanding deployment of automated film-forming systems is projected to integrate sanitation data into herd management analytics platforms. Investment in connected dairy technologies is likely to enhance IoT-enabled hygiene-monitoring architectures. As automation deepens across high-output states such as California, structured hygiene platforms are positioned to reinforce yield stability and operational consistency.

Competitive Landscape

The global udder hygiene market is moderately consolidated, with leadership concentrated among multinational suppliers including DeLaval, Ecolab, GEA Group, Diversey, and CID Lines, which collectively account for a substantial share of global revenues. While chemical-based manufacturing, particularly iodine sourcing and primary biocide inputs, exhibits relatively high upstream concentration, downstream formulation, branding, and distribution remain fragmented across regional compounders and dealer networks. Mid-tier participants such as BouMatic and Kersia operate within this intermediate tier, reinforcing competitive dispersion in localized markets despite top-tier dominance in integrated systems.

Competitive positioning increasingly reflects a shift from standalone chemical supply toward bundled “udder health” platforms. Market leaders differentiate through integration of hygiene consumables with milking equipment, diagnostics, and service contracts, embedding products within automated workflows and creating structural switching costs for dairy operators. In contrast, challenger brands and regional formulators compete on price-per-liter efficiency, flexible distribution, and rapid customization to local herd conditions. This dual structure platform-led integration at the top and cost-driven agility at the base defines current market behavior and supports gradual consolidation around technology-enabled, service-oriented ecosystems.

Key Industry Highlights:

- In June 2025, Zoetis launched strategic partnerships to address sustainability needs for dairy and beef producers. These collaborations focus on genetic selection and health protocols to reduce the environmental footprint of milk production.

- In March 2025, DeLaval launched a new non-iodine film-forming teat dip targeting sustainable dairy practices. The product addresses increasing regulatory restrictions on iodine residues while providing long-lasting barrier protection.

- In November 2024, GEA Group introduced automated sanitization technology to boost dairy farm efficiency. This development enhances operational speed and reduces labor reliance through advanced robotic cleaning systems.

Companies Covered in Udder Hygiene Market

- DeLaval

- Ecolab

- GEA Group

- Zoetis

- Boehringer Ingelheim

- Kersia

- Merck Animal Health (MSD)

- Elanco Animal Health

- Neogen Corporation

- BouMatic

- Diversey

- CID LINES

- Roullier Group

- Westfalia Surge

- AgroChem

- Milkrite

- InterPuls

Frequently Asked Questions

The global udder hygiene market is projected to be valued at US$1.8 billion in 2026 and is expected to reach US$2.7 billion by 2033, driven by global dairy production expansion, the persistent burden of mastitis, and the need to meet stringent milk quality and safety standards.

Mastitis remains the most costly disease for dairy farmers, reducing milk yield, degrading quality, and incurring treatment expenses. This persistent economic pressure reclassifies preventive udder hygiene from a discretionary input to a risk management essential, institutionalizing pre- and post-milking disinfection within standard operating protocols.

The udder hygiene market is forecast to grow at a CAGR of 6% from 2026 to 2033, reflecting steady demand from expanding dairy herds and the intensification of hygiene protocols in both established and emerging dairy regions.

Europe is the leading regional market, accounting for approximately 34% share, underpinned by stringent animal welfare regulations and advanced farm management systems. Asia Pacific is the fastest-growing region, driven by rapid dairy sector expansion, policy support for productivity improvement, and the modernization of farm hygiene practices in countries such as India and China.

The market is moderately consolidated, with leadership concentrated among multinational suppliers such as DeLaval, Ecolab, GEA Group, and Kersia. These companies compete through integrated "udder health" platforms that combine hygiene consumables with milking equipment, diagnostics, and service contracts, creating structural switching costs for dairy operators.