- Automation & Robotics

- Tunnel Detection System Market

Tunnel Detection System Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Tunnel Detection System Market by Technology (Ground Penetrating Radar (GPR), In-tunnel Scouting Robots, Ground Robots, Surface Seismic Systems, Microgravity Detection Systems (MDSs), UGV-based Systems, Resistive & Tomography, Electromagnetic Systems (excluding GPR), Others), Application, and Regional Analysis for 2025 - 2032

Tunnel Detection System Market Share and Trends Analysis

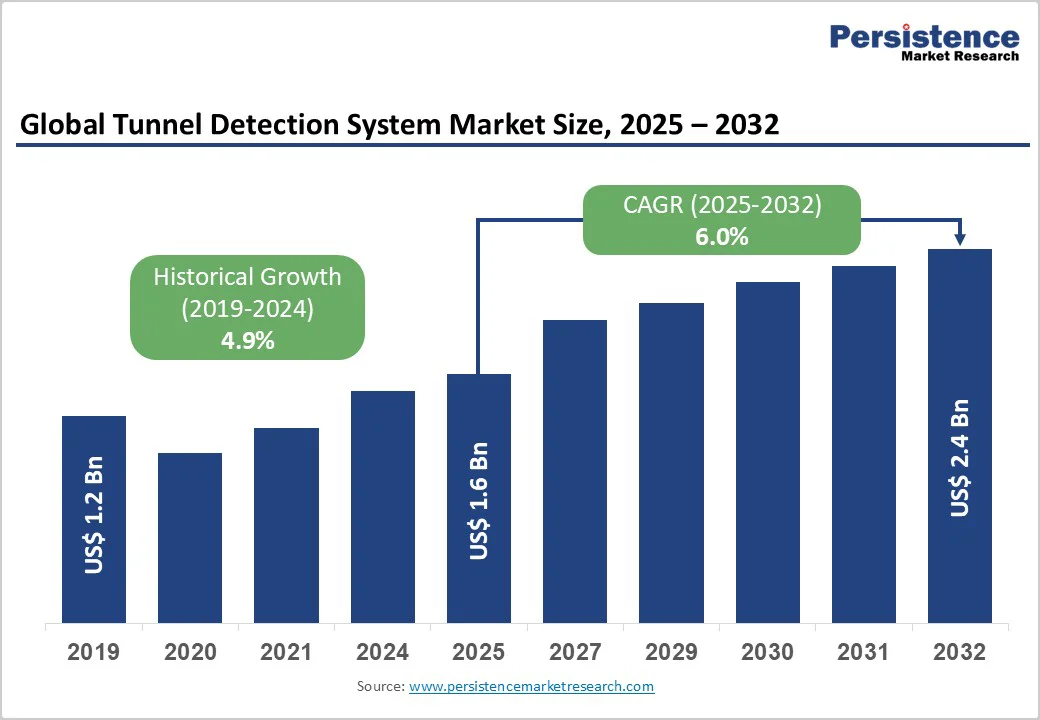

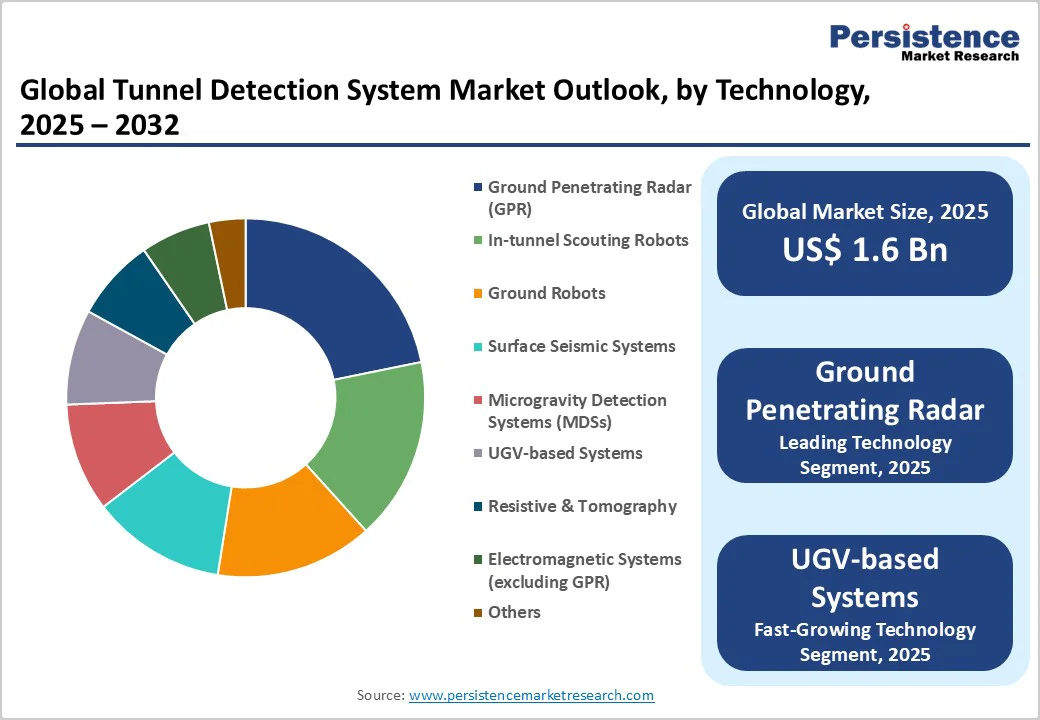

The global tunnel detection system market is expected to reach US$1.6 billion in 2025. It is projected to reach US$2.4 billion by 2032, growing at a CAGR of 6% during the forecast period 2025-2032. The rising need for advanced subterranean surveillance in border security, defense, transportation infrastructure, and critical asset protection underpins this expansion.

The demand surge is fueled by increasing geopolitical tensions, heightened security requirements, rapid infrastructure growth, and ongoing technological advancements in ground robotics, radar, and sensor-driven detection platforms. Strategic investments in innovation and cross-sector partnerships continue to accelerate deployment, making tunnel detection systems a core component of risk-mitigation and operational-safety frameworks worldwide.

Key Industry Highlights:

- GPR Dominance: Ground-penetrating radar (GPR) is expected to lead technology adoption, with an approximate 21.8% market share in 2025, while UGV-based systems are the fastest-growing segment, with about a 7% CAGR from 2025 to 2032.

- End-User Dynamics: Government agencies hold the largest share at around 28.7% in 2025, whereas defense & military applications show the highest growth at an estimated 6.5% CAGR through 2032.

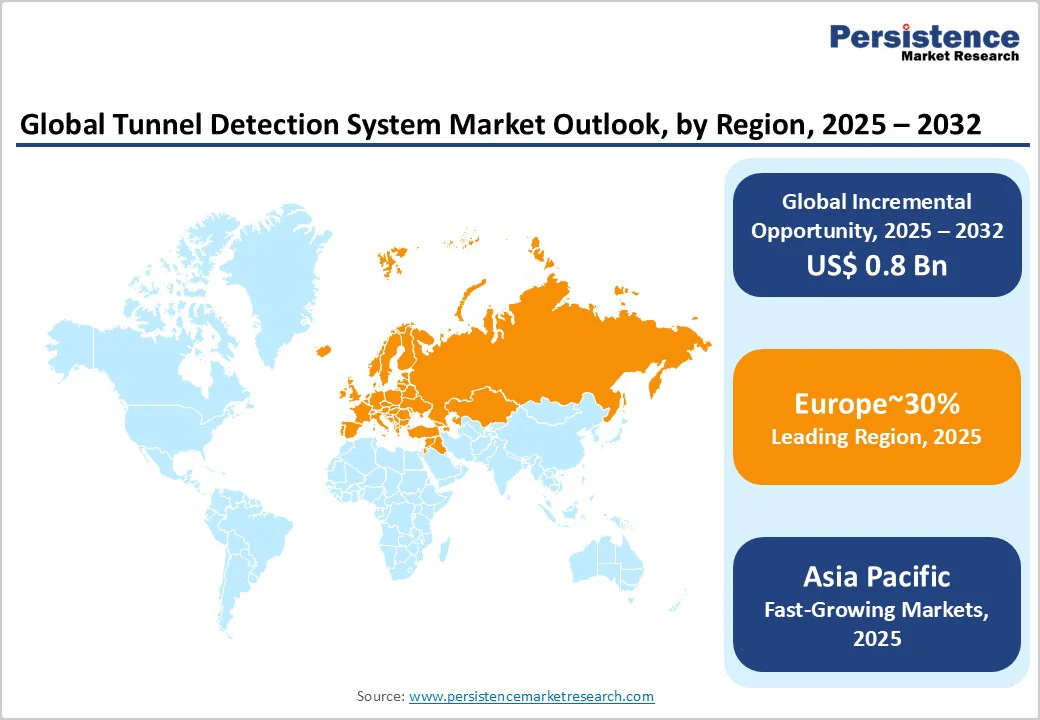

- Regional Insights: North America, with 28% and Europe, with 30% dominate demand on the back of strict security and infrastructure mandates, with Asia Pacific being positioned as the fastest-growing regional market at 6.9% CAGR during 2025-2032.

- Strategic Moves: Recent developments include Hexagon’s acquisition of Rocscience, MST Global–Keller Group partnerships, and STRABAG’s €110 million tunnel contract, reinforcing market consolidation.

- Business Focus: Leading players emphasize multi-modal sensing, AI-driven analytics, sustainability, and global expansion as their key competitive strategies.

| Key Insights | Details |

|---|---|

|

Tunnel Detection System Market Size (2025E) |

US$1.6 Bn |

|

Market Value Forecast (2032F) |

US$2.4 Bn |

|

Projected Growth CAGR (2025-2032) |

6% |

|

Historical Market Growth (2019-2024) |

4.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Driver - Border Security, Counter-terrorism, and Illicit Activity Prevention

Tunnel detection systems are essential to modern border and homeland security, as many countries worldwide face escalating threats from tunnel-based smuggling and covert infiltration. The U.S. Department of Homeland Security (DHS), for example, has dedicated over US$100 million to advanced tunnel-detection contracts to secure the U.S.–Mexico border. The demand for persistent, real-time underground surveillance stems from the need to detect sophisticated cross-border tunnels used for illegal trafficking, arms smuggling, and unauthorized migration. Similar imperatives are seen in Israel, India, and the European Union (EU), where border tunnel detection is integral to counter-terrorism operations.

In addition, global urbanization and multi-billion-dollar investments in transportation infrastructure are driving the deployment of tunnel detection solutions for railways, highways, metros, and utilities. Tunnel detection technologies are employed to monitor existing structures for collapse risks, water ingress, and subsurface anomalies, ensuring uninterrupted service and passenger safety. Projects such as the € 110 million Karawanks Tunnel contract and smart transit expansions in the Asia Pacific underscore the commercial value of detection systems in public and private sectors. Transport authorities and infrastructure owners require high-fidelity monitoring, making GPR, surface seismic, and Tomography methods pivotal for asset preservation amid swelling passenger numbers and utility demand.

Challenges - High Capital Costs and Technical Complexity

A major restraining factor for the market is the high capital investment required to acquire and operate advanced detection systems. The cost burden is significant for smaller agencies, municipalities, and developing nations, deterring market adoption despite pressing security and infrastructure needs. GPR, seismic, and microgravity platforms often require specialized hardware, ongoing maintenance, and technical expertise for data interpretation, resulting in higher training and operational costs. Regulatory compliance requirements may further increase costs by mandating system certifications and interoperability standards across critical sites. Risk quantification indicates that initial capital outlays can range from US$250,000 to several million dollars per deployment, with recurring costs for periodic upgrades and skilled personnel.

Another hurdle is that tunnel detection systems may be limited by soil conductivity, moisture variation, and urban electromagnetic noise, which can impact detection accuracy and reliability. In clay-rich or highly conductive ground, GPR signal penetration and seismic wave propagation are restricted, leading to potential misidentification and operational delays. These technical challenges can generate false positives, requiring secondary validation and potentially jeopardizing system credibility. Moreover, regulatory rules regarding electromagnetic frequency usage or seismic data acquisition in sensitive zones restrict broader deployment, particularly near defense installations or populated areas.

Opportunity - Infrastructure Modernization in Emerging Economies

Governments across developing economies in the Asia Pacific, Latin America, and Africa are channeling funds into urban transit networks, border modernization, and energy grid expansions, presenting addressable market opportunities exceeding US$300 million per year for detection technologies. Policies favoring smart city development and security upgrades underpin the growth of the tunnel detection system market, complemented by private-sector participation in utilities, mining, and large-scale construction. Collaborations between technology providers, construction firms, and defense agencies are expected to accelerate further the deployment of advanced sensing and autonomous detection systems, strengthening regional resilience and supporting long-term infrastructure modernization goals.

Technological convergence encompassing robotics, AI, and multi-modal sensing is reconfiguring the tunnel detection system market landscape. UGV-based systems and autonomous scouting robots, forecasted to be the fastest growing segment, deliver continuous, high-resolution analysis even in hazardous or remote settings. Their deployment is accelerating across the mining, energy, defense, and transportation sectors, fostering new applications and expanding the overall market. Integration with IoT platforms, drone-assisted inspections, and cloud-based analytics further elevates demand for real-time, predictive subterranean threat management.

Category-wise Analysis

Technology Insights

GPR technology is poised to dominate with approximately 21.8% of the tunnel detection system market revenue share in 2025, as it is the most widely adopted detection method for tunnels, utilities, and underground anomalies. Recognized for its non-destructive, real-time imaging capabilities and cost-effective deployment, GPR is preferred in government, defense, urban transit, and energy grid sectors. Recent procurement surges by military and municipal buyers underscore the rising demand for multi-frequency units offering enhanced accuracy and operational range, positioning GPR as the reference standard for quick, reliable tunnel mapping.

Unmanned ground vehicle (UGV)-based systems are forecasted to expand at about 7% CAGR through 2032. These systems offer autonomous deployment, remote operation, and adaptability in hazardous or complex terrain that is not easily accessible to manual teams. They are increasingly deployed in urban environments, border surveillance, mining operations, and critical infrastructure, providing high-resolution, multi-sensor data and reducing personnel risk. The convergence of technology with AI-powered analytics and advanced sensor payloads has driven rapid adoption, with several UGV developers reporting year-on-year revenue growth, particularly in Asia Pacific, Europe, and North America.

End-User Insights

Government agencies represent the largest end-user share with 28.7% of the global market value. Primary drivers are legislative commitment to addressing border threats, illicit tunneling, and national security imperatives. The U.S. Border Patrol spends more than US$ 100 million annually on tunnel detection and Persistent Surveillance and Detection (PSD) systems, with similar investments observed in the U.K., EU, Israel, and India. These agencies require multilayered detection strategies, integrating seismic, electromagnetic, GPR, and robotic techniques. Nearly 95% of major government contracts specify compliance with international standards and interoperability for joint operations, reinforcing market leadership.

Defense and military entities are the fastest-growing end users, expanding at approximately 6.5% CAGR from 2025 to 2032. The demand spike results from asymmetric warfare, evolving combat tactics, and the urgent need to detect underground threats (tunnels, bunkers, mines) near installations and active theaters. Increasing technological sophistication, such as AI-enabled seismic arrays, microgravity sensors, and specialized robotics, has made tunnel detection a critical component of national defense.

Regional Insights

North America Tunnel Detection System Market Trends

North America is slated to hold a prominent 28% of the tunnel detection system market share in 2025, led by the United States’ massive investments in security, defense, and critical infrastructure monitoring. The region is known for deploying advanced detection systems in customs, military, urban transportation, utilities, and correctional sectors. The U.S. Border Patrol utilizes persistent seismic-acoustic sensor arrays, predictive mapping, and real-time monitoring solutions to counter underground threats. Canada is also experiencing rapid market expansion supported by investments in subway, rail, and highway tunnel integrity management.

Market players across North America are maintaining a competitive edge through public–private innovation partnerships and compliance with strict regulatory standards, such as those set by the DHS and ASTM. Furthermore, the rising emphasis on AI-enabled analytics, field operations automation, and the interoperability of detection systems across agencies is reinforcing long-term growth prospects, while cross-border technology collaborations continue to enhance regional system reliability and scalability.

Europe Tunnel Detection System Market Trends

Europe is anticipated to account for an estimated 30.1% market share in 2025, underpinned by substantial public infrastructure development, defense spending, and rigorous adoption of detection innovations. Germany, the U.K., France, and Spain are market leaders, leveraging harmonized regulatory practices and long-term transit expansion projects, such as the Karawanks Tunnel, London Crossrail, and Paris Metro extensions. Regional policy mandates robust tunnel detection integration into urban transit and utilities. The EU’s commitment to border security, modernizing law enforcement, and coordinated funding programs accelerates deployment.

The competitive landscape of the European market is characterized by the presence of multinational system integrators, research-driven consortia, and specialized engineering partnerships fostering innovation in automation, sensor calibration, and data interoperability. Apart from this, the growing focus on climate-neutral construction and sustainable infrastructure practices is strengthening the adoption of eco-efficient and energy-optimized detection solutions across the region.

Asia Pacific Tunnel Detection System Market Trends

Asia Pacific is the fastest-growing region, projected to record a CAGR of 6.9% between 2025 and 2032. China, Japan, India, and major ASEAN economies fuel expansion through rapid urban transit buildouts, smart city initiatives, border modernization, and energy infrastructure upgrades. Market demand is amplified by government-led investments in metro tunneling, utility grid integrity, and defense requirements for counter-insurgency operations. Technology firms and state agencies are actively collaborating on robotics, microgravity detection, and autonomous system deployment, as market players establish local R&D and production hubs to support high-volume projects.

Asia Pacific’s competitive edge is reinforced by manufacturing cost advantages, policy-driven adoption, and escalating infrastructure budgets anticipated to exceed US$ 200 billion by 2030. Furthermore, the region is witnessing increased participation from private technology innovators, strategic foreign collaborations, and emerging standards for cross-border infrastructure safety, driving long-term adoption of smart, data-centric, and energy-efficient tunnel detection systems.

Competitive Landscape

The global tunnel detection system market structure is moderately concentrated, featuring a blend of established technology firms and niche solution providers. Leading players command 45–60% of segment revenues, with fragmented market share beyond the top 12 global vendors. Market concentration is shaped by government procurement policies, defense alliances, and infrastructure project cycles. Major manufacturers and integrators differentiate through proprietary sensing technologies, data analytics platforms, and cross-sector partnerships, forming complex competitive networks in North America, Europe, and Asia Pacific.

Key Industry Developments

- In November 2025, BTG Positioning Systems acquired U.S.-based GPR, Inc., a company specializing in radar-based underground mapping technology, to enhance its port automation capabilities. This strategic move allows BTG to integrate GPR’s patented ground-penetrating radar, which provides highly accurate underground positioning even in GPS-restricted environments. The acquisition supports the development of new autonomous solutions, including the upcoming Ground Sensing Localization (GSL) system, promising accuracy within 2 centimeters without needing above-ground reference points.

- In July 2025, Exodigo, an Israeli startup, secured US$ 96 million in Series B funding for its advanced underground mapping technology. The company's system enables detailed visualization of subterranean infrastructure, aiding military and security operations, including efforts to detect Hamas and Hezbollah tunnels. The technology is a crucial tool for underground warfare tactics developed by the IDF, enhancing situational awareness and operational effectiveness in complex underground environments.

- In February 2025, The Boring Company was contracted to build the Dubai Loop, a cutting-edge tunnel transportation system designed to revolutionize urban mobility in Dubai. This system will utilize high-speed autonomous vehicles traveling through underground tunnels, significantly reducing surface traffic congestion and travel times. The Dubai Loop aims to integrate with existing public transit for seamless connectivity and low environmental impact.

Companies Covered in Tunnel Detection System Market

- Hexagon AB

- Rocscience

- STRABAG

- MST Global

- Keller Group

- IBAK Helmut Hunger

- Geospace Technologies

- GeoRadar

- GEOInstruments

- Minova

- OCTX

- SENNING GmbH

- FLIR Systems

- Hitachi High-Technologies

- Nova Metrix

Frequently Asked Questions

The global tunnel detection system market is projected to reach US$ 1.6 billion in 2025.

Market growth is driven by a surging demand for border and homeland security, rising infrastructure expansion, and advancements in GPR and UGV technologies.

The market is poised to witness a CAGR of 6% from 2025 to 2032.

Key market opportunities include rapid adoption in Asia Pacific, autonomous robotics integration, and new deployments in correctional and private security sectors.

Hexagon, STRABAG, MST Global, and Keller Group are some of the key players in the market.