- Pharmaceuticals

- Global Tumour-Induced Osteomalacia Market

Global Tumour-Induced Osteomalacia Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Tumour-Induced Osteomalacia Market by Treatment (Drugs and Supplements and Surgery), by Diagnosis (Biochemical testing, Imaging techniques, Differential diagnosis, and Others) by End User (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, and Others), and Regional Analysis from 2026 to 2033.

Tumour-Induced Osteomalacia Market Share and Trends Analysis

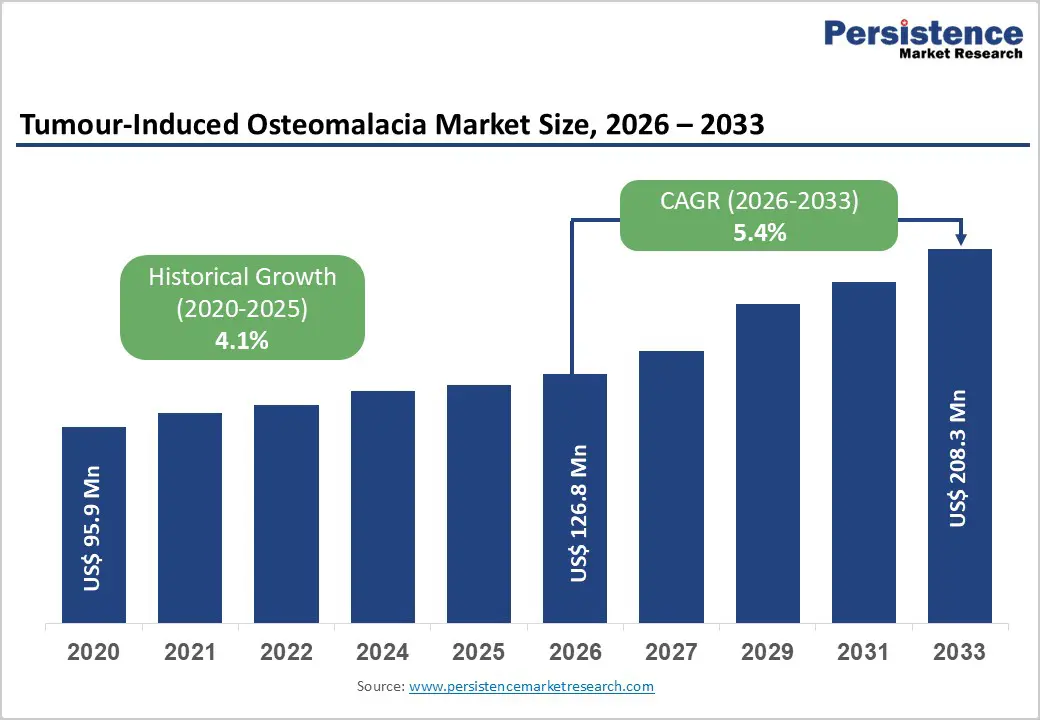

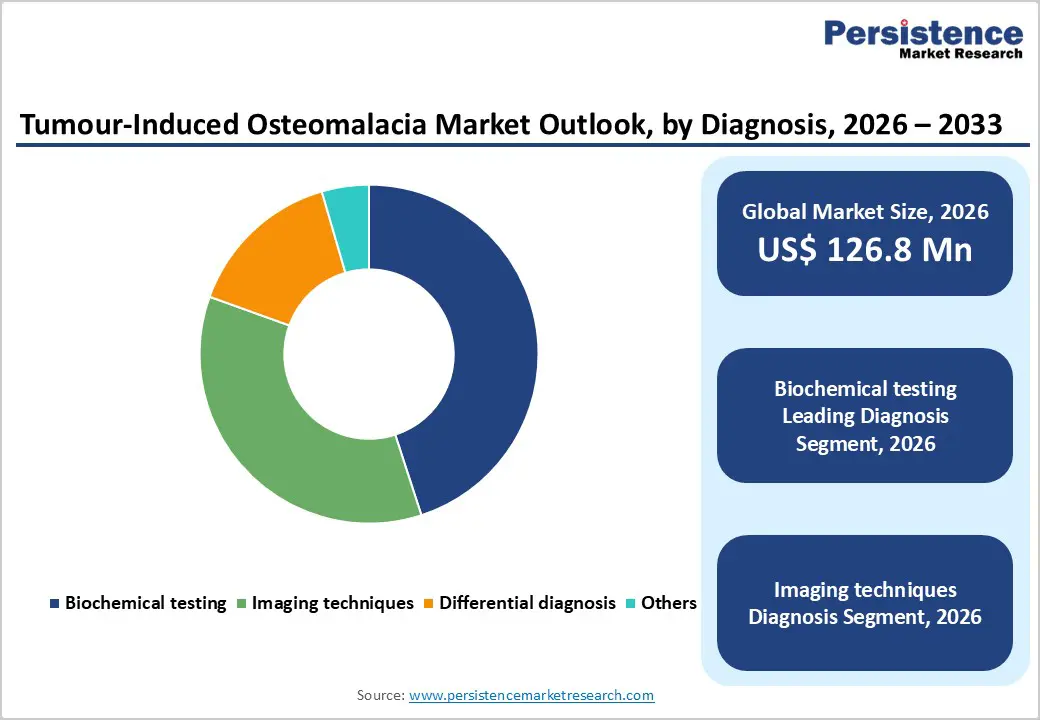

The global tumour-induced osteomalacia market size is estimated to grow from US$ 126.8 Mn in 2026 to US$ 208.3 Mn by Mn 2033. The market is projected to record a CAGR of 5.4% during the forecast period from 2026 to 2033.

Global demand for tumour-induced osteomalacia treatments is rising steadily, driven by increasing awareness of rare phosphate-wasting disorders, improved clinical recognition of FGF23-mediated pathophysiology, and advances in diagnostic and therapeutic approaches. Rising diagnosis rates among patients presenting with unexplained bone pain, muscle weakness, fractures, and impaired mobility are increasing demand for biochemical testing, advanced imaging, and long-term disease management across tertiary care hospitals and specialty clinics. Greater understanding of the severe skeletal and functional consequences associated with delayed diagnosis is reinforcing the need for early detection and sustained treatment. Pharmacological therapies, including phosphate supplements, active vitamin D analogs, and targeted FGF23 inhibitors, are gaining preference due to their effectiveness in symptom control, particularly in cases where tumors are unresectable or difficult to localize. Additionally, growing inclusion of TIO within rare disease frameworks, supportive regulatory pathways for orphan drugs, and expanding clinical research are sustaining consistent market demand. Improvements in diagnostic accuracy, expansion of specialist care infrastructure, and rising healthcare expenditure in emerging economies are further supporting long-term global market growth.

Key Industry Highlights

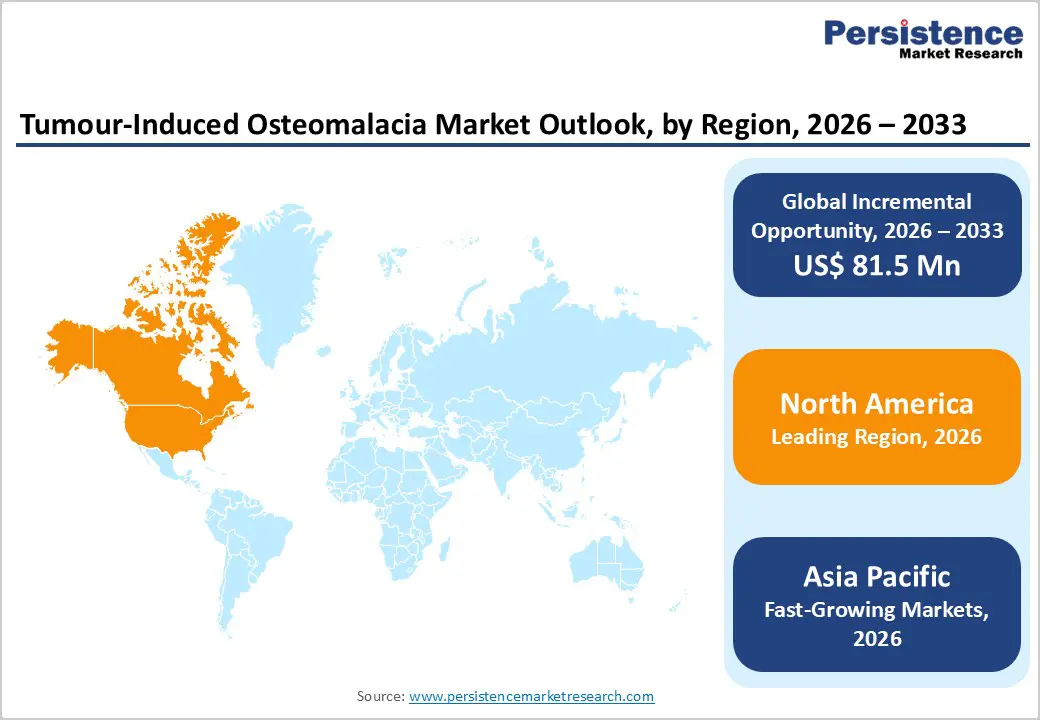

- Leading Region: North America holds the largest market share at 48.5%, supported by advanced healthcare systems, strong rare disease awareness, early adoption of targeted therapies, and well-established referral networks for metabolic bone disorders.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to increasing healthcare investments, improving diagnostic infrastructure, rising specialist availability, and growing awareness of rare endocrine and skeletal diseases.

- Leading Treatment Segment: Drugs and supplements dominate the market due to their central role in long-term disease management, recurring treatment requirements, and broad applicability across resectable and unresectable TIO cases.

- Fastest-Growing Treatment Segment: Surgery is witnessing faster growth as advances in imaging and tumor localization improve resection success rates and curative outcomes.

- Leading Diagnosis Segment: Surgery is witnessing faster growth as advances in imaging and tumor localization improve resection success rates and curative outcomes.

- Fastest-Growing Diagnosis Segment: Imaging techniques are expanding rapidly, driven by increasing reliance on advanced functional and hybrid imaging modalities to accurately localize small, elusive phosphaturic tumors responsible for tumour-induced osteomalacia.

| Key Insights | Details |

|---|---|

| Tumour-Induced Osteomalacia Market Size (2026E) | US$ 126.8 Mn |

| Market Value Forecast (2033F) | US$ 208.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Rising Awareness of Rare Phosphate-Wasting Disorders and Advancements in Targeted Therapies Driving Market Growth

The global tumour-induced osteomalacia market is primarily driven by increasing clinical awareness of rare phosphate-wasting disorders and improved understanding of fibroblast growth factor 23 (FGF23)–mediated pathophysiology. Historically underdiagnosed due to nonspecific symptoms such as bone pain, muscle weakness, and fractures, TIO is now being recognized more frequently as diagnostic capabilities improve. Greater awareness among endocrinologists, nephrologists, and orthopedic specialists is leading to earlier suspicion and confirmatory testing. Advances in biochemical diagnostics, including serum phosphate and FGF23 assays, are reducing diagnostic delays and enabling timely treatment initiation.

Additionally, the introduction and expanding clinical use of targeted therapies, particularly FGF23 inhibitors, have significantly transformed disease management. These therapies offer improved symptom control and quality of life for patients with unresectable or unlocalized tumors. Growing adoption of standardized treatment protocols and inclusion of TIO within rare disease frameworks are further strengthening demand. Increased investment in rare disease research, coupled with supportive regulatory pathways for orphan drugs, continues to accelerate therapeutic development. Collectively, improved disease recognition, diagnostic precision, and availability of effective long-term treatments are sustaining steady growth in the tumour-induced osteomalacia market.

Restraints – Diagnostic Complexity, Delayed Tumor Localization, and High Treatment Costs Limiting Market Expansion

The tumour-induced osteomalacia market faces several structural and clinical challenges that restrain wider adoption and timely treatment. One of the most significant limitations is the complexity of diagnosis, as TIO symptoms often mimic more common musculoskeletal or metabolic conditions. Prolonged diagnostic journeys are common, with patients undergoing multiple evaluations before correct identification, delaying treatment initiation. Tumor localization remains particularly challenging, as phosphaturic mesenchymal tumors are often small, slow-growing, and difficult to detect even with advanced imaging modalities.

Treatment-related cost burdens further constrain market growth. Long-term pharmacological management, especially with targeted biologic therapies, can be expensive and may not be universally reimbursed, particularly in low- and middle-income regions. Surgical intervention, while potentially curative, requires specialized imaging, experienced surgical teams, and tertiary care infrastructure, limiting accessibility. Regulatory and reimbursement variability across regions also affects therapy adoption. Additionally, limited availability of specialized diagnostic assays and trained clinicians in emerging markets restricts early detection. These combined factors contribute to underdiagnosis, delayed care, and uneven market penetration, moderating overall growth despite rising clinical recognition.

Opportunity – Expansion of Rare Disease Programs, Advanced Imaging, and Emerging Market Healthcare Infrastructure Creating Growth Potential

The tumour-induced osteomalacia market presents significant growth opportunities driven by expanding rare disease initiatives, advancements in diagnostic imaging, and improving healthcare infrastructure in emerging economies. Increasing inclusion of rare metabolic bone disorders within national healthcare strategies is improving patient identification, referral pathways, and treatment access. Development of advanced functional imaging techniques and hybrid modalities is enhancing tumor localization accuracy, increasing the likelihood of curative surgical intervention. These diagnostic improvements are expected to shorten disease timelines and increase procedural volumes.

Emerging regions across Asia Pacific, Latin America, and the Middle East offer substantial untapped potential. Rising healthcare expenditure, growing tertiary care capacity, and expanding specialist training programs are improving access to endocrinology and diagnostic services. Governments are gradually strengthening orphan drug policies and reimbursement mechanisms, encouraging adoption of targeted therapies. Additionally, expanding academic research into phosphate metabolism and bone biology is supporting innovation and pipeline development. Strategic collaborations between pharmaceutical companies, diagnostic providers, and research institutions are facilitating clinical trials, real-world evidence generation, and regional market entry. Together, these trends position tumour-induced osteomalacia as a niche but steadily expanding market with strong long-term growth potential.

Category-wise Analysis

By Treatment, Drugs and Supplements Lead Due to Chronic Disease Management and Long-Term Therapy Needs

The drugs and supplements segment is projected to dominate the global tumour-induced osteomalacia market in 2026, accounting for a revenue share of 82.0%. Segment leadership is primarily driven by the chronic nature of TIO, which necessitates long-term management using phosphate supplements, active vitamin D analogs, and targeted therapies such as FGF23 inhibitors. Unlike surgical intervention, which is applicable only when tumors are localized and resectable, pharmacological therapy remains essential for symptom control in unresectable or undetected tumors.

Continuous dosing requirements ensure recurring demand and sustained revenue generation. Broad clinical utility across different stages of disease progression further strengthens adoption. Increasing availability of standardized treatment protocols, improved physician awareness, and expanding access to rare disease therapies support segment growth. Ongoing clinical research aimed at improving dosing convenience, safety, and patient compliance continues to reinforce the dominant position of drugs and supplements within the treatment landscape.

By Diagnosis, Biochemical Testing Leads Due to Early Detection and Clinical Standardization

The biochemical testing segment is expected to lead the global tumour-induced osteomalacia market in 2026, capturing a revenue share of 45.0%. Leadership is supported by the central role of laboratory testing in confirming hypophosphatemia, elevated FGF23 levels, and associated metabolic abnormalities characteristic of TIO. Biochemical assays are widely used as first-line diagnostic tools due to their accuracy, reproducibility, and integration into routine clinical workflows. These tests enable early disease suspicion before advanced imaging is pursued, making them critical in reducing diagnostic delays common in rare bone disorders.

Strong clinical guideline support and widespread availability across hospital and reference laboratories enhance adoption. Compatibility with automated analyzers improves efficiency and scalability, particularly in tertiary care settings. Growing awareness among endocrinologists and nephrologists, along with improved access to specialized testing, continues to drive demand for biochemical diagnostics.

By End User, Hospitals Lead Due to Multidisciplinary Care and High Patient Footfall

The hospitals segment is projected to dominate the tumour-induced osteomalacia market in 2026, accounting for a revenue share of 55.0%. Leadership is driven by the concentration of multidisciplinary expertise required for managing TIO, including endocrinology, orthopedics, radiology, and surgical care. Hospitals serve as the primary centers for diagnosis, treatment initiation, and long-term disease monitoring. High patient inflow, especially referrals for unexplained fractures, bone pain, and muscle weakness, sustains demand for diagnostic testing and pharmacological treatment.

Advanced laboratory infrastructure and access to imaging modalities support comprehensive disease evaluation. Hospitals also function as referral hubs for complex and rare metabolic bone disorders, handling cases transferred from specialty clinics and ambulatory centers. Increasing emphasis on early diagnosis, rare disease management programs, and integrated care pathways further reinforces hospital dominance in the market.

Region-wise Insights

North America Tumour-Induced Osteomalacia Market Trends

The North America tumour-induced osteomalacia market is expected to dominate globally with a value share of 48.5% in 2026, led primarily by the United States. Regional leadership is underpinned by advanced healthcare infrastructure, strong rare disease awareness, and early adoption of specialized diagnostic and therapeutic solutions. Well-established referral networks and access to endocrinology specialists facilitate timely diagnosis and management of TIO.

The presence of robust laboratory capabilities enables widespread use of biochemical testing and advanced imaging for tumor localization. Regulatory support for orphan drugs and favorable reimbursement frameworks improve patient access to long-term pharmacological therapies. The region also benefits from strong clinical research activity and ongoing trials evaluating targeted treatments for phosphate-wasting disorders. Academic medical centers play a key role in advancing diagnostic accuracy and treatment protocols. High healthcare spending, established patient registries, and continued innovation collectively sustain North America’s dominant market position.

Europe Tumour-Induced Osteomalacia Market Trends

The Europe tumour-induced osteomalacia market is expected to grow steadily, supported by strong healthcare systems, structured referral pathways, and increasing recognition of rare metabolic bone diseases. Countries such as Germany, the U.K., France, Italy, and the Nordic nations contribute significantly due to well-developed hospital networks and specialized endocrinology services. European healthcare providers emphasize evidence-based diagnostics, supporting consistent use of biochemical testing and imaging for disease confirmation.

Regulatory frameworks promoting orphan drug development and cross-border healthcare collaboration enhance treatment accessibility. Growing academic research in bone metabolism and rare disease registries improves clinical understanding and early diagnosis. Expansion of centralized laboratory services and integration of advanced imaging technologies improve diagnostic efficiency. Increased clinician education and patient advocacy initiatives are reducing diagnostic delays. These factors, combined with stable healthcare funding and structured disease management programs, support sustained market growth across Europe.

Asia Pacific Tumour-Induced Osteomalacia Market Trends

The Asia Pacific tumour-induced osteomalacia market is expected to register a relatively higher CAGR of around 7.1% between 2026 and 2033, driven by expanding healthcare infrastructure, improving diagnostic capabilities, and rising awareness of rare diseases. Countries including China, India, Japan, South Korea, and several Southeast Asian nations are investing heavily in hospital development and laboratory modernization. Improved access to biochemical testing and imaging services is enabling earlier identification of metabolic bone disorders. Growing medical education initiatives and international clinical collaborations are strengthening physician awareness of TIO.

The region also benefits from expanding pharmaceutical manufacturing and increased availability of essential supplements and targeted therapies. Gradual alignment of regulatory policies with global orphan drug frameworks is improving treatment access. Government focus on strengthening tertiary care and rare disease programs is expected to further accelerate market growth, positioning Asia Pacific as the fastest-growing regional market.

Market Competitive Landscape

The global tumour-induced osteomalacia market is characterized by moderate to high competition, with established players such as Teva Pharmaceuticals, Glenmark Pharmaceuticals, Lupin Pharmaceuticals, Glenmark Pharmaceuticals, and Intas Pharmaceuticals Ltd holding strong market positions. These companies benefit from extensive pharmaceutical portfolios, expertise in metabolic and rare bone disorders, and well-established distribution networks serving hospitals, specialty clinics, and diagnostic centers.

Competitive strategies focus on expanding therapeutic offerings, including phosphate supplements and targeted therapies, strengthening clinical evidence through R&D, and improving treatment accessibility. Market participants are also emphasizing geographic expansion in emerging economies, regulatory compliance, and strategic collaborations to enhance market penetration and support long-term growth.

Key Industry Developments:

In April 2022, the European Commission approved Kyowa Kirin’s CRYSVITA® (burosumab) for treating FGF23-related hypophosphataemia in tumour-induced osteomalacia patients with non-resectable or unlocalized tumors, in both children (1–17 years) and adults; the drug was already approved in the EU for X-linked hypophosphataemia.

Companies Covered in Global Tumour-Induced Osteomalacia Market

- Teva Pharmaceuticals

- Glenmark Pharmaceuticals

- Lupin Pharmaceuticals

- Glenmark Pharmaceuticals

- Intas Pharmaceuticals Ltd

- Ultragenyx Pharmaceutical Inc.

- Kyowa Kirin Co., Ltd.

- Eli Lilly and Company

- Amgen Inc.

- Novartis AG

- Sanofi S.A.

- Pfizer Inc.

- AbbVie Inc.

- Horizon Therapeutics

- Others

Frequently Asked Questions

The global tumour-induced osteomalacia market is projected to be valued at US$ 126.8 Mn in 2026.

Increasing clinical awareness and early diagnosis of this rare metabolic bone disorder, combined with advancements in diagnostic technologies and the introduction of targeted therapies such as FGF23 inhibitors like burosumab, drive market grow.

The global tumour-induced osteomalacia market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Expansion lies in developing advanced biologics and precision diagnostics and growing treatment accessibility in emerging regions with rising healthcare infrastructure.

Teva Pharmaceuticals, Glenmark Pharmaceuticals, Lupin Pharmaceuticals, Glenmark Pharmaceuticals, and Intas Pharmaceuticals Ltd are some of the key players in the tumour-induced osteomalacia market.