- Automation & Robotics

- Rupture Disc Market

Rupture Disc Market Size, Share, Trends, Growth Forecasts 2025 - 2032

Rupture Disc Market By Material (Graphite Rupture Discs, Metallic Rupture Discs), Product Type (Positive Arch Rupture Discs, Anti-Arch Rupture Discs, Flat Type Rupture Discs), Application (Standalone, Rupture Discs in Combination with Relief Valves), End-user and Regional Analysis 2025 - 2032

Rupture Disc Market Share and Trends Analysis

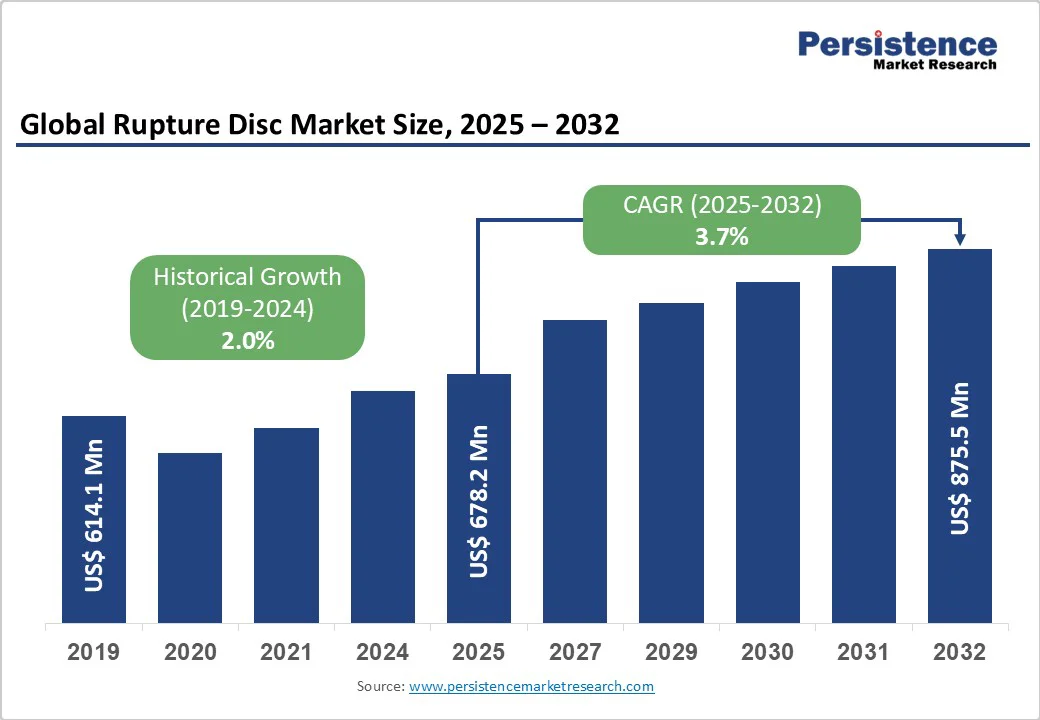

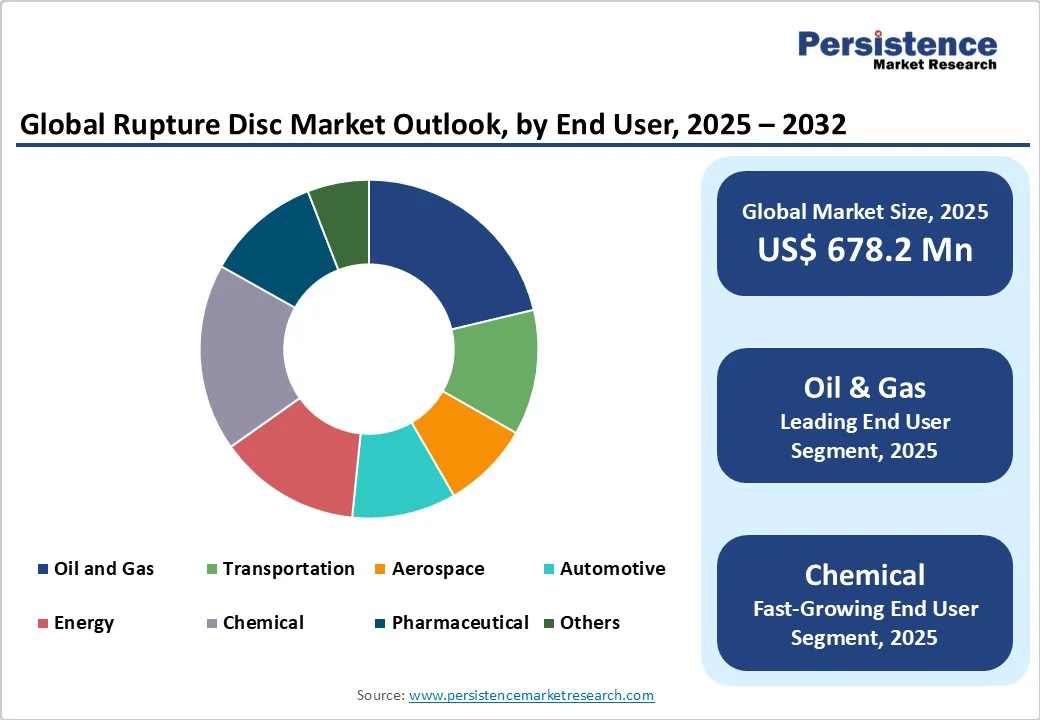

The global rupture disc market size is likely to value US$ 678.2 million in 2025 and is projected to reach US$ 875.5 million by 2032, growing at a CAGR of 3.7% between 2025 and 2032.

Rising awareness toward industrial safety and the growing adoption of high-performance rupture discs across key process industries are driving steady market expansion.

The industry’s growth is strongly supported by stringent regulatory frameworks emphasizing operational safety and the implementation of advanced industrial protection systems.

Key Industry Highlights

| Key Insights | Details |

|---|---|

| Rupture Disc Market Size (2025E) | US$ 678.2 million |

| Market Value Forecast (2032F) | US$ 875.5 million |

| Projected Growth CAGR (2025-2032) | 3.7% |

| Historical Market Growth (2019-2024) | 2.0% |

Market Dynamics Analysis

Driver - Ageing Water and Wastewater Infrastructure to Spur Market Demand for Rupture Discs

Ageing public infrastructure is a key concern for many nations. In older building infrastructure, pressure-reducing valves are also due to be replaced as these have reached the end of their life cycles. It is essential to replace these valves to mitigate deterioration and lengthen the operational lifespan of industrial infrastructure processes and ensure the highest possible standards of industrial safety and functionality.

In recent years, the public has become increasingly aware of the need for enhanced cleanliness and hygiene. This heightened awareness has led to an increased demand for sophisticated safety systems, extended service life and improved water supply and sanitation infrastructure in many countries worldwide.

Given this rising demand, governments have shifted their focus towards investing more heavily in newer technologies and infrastructures to provide citizens with access to clean water sources and better sanitation facilities.

Some of these new investments include undertaking various projects such as building new sewage treatment plants, implementing modernized rainwater harvesting systems, constructing efficient drainage networks, and providing eco-friendly wastewater treatment solutions.

Such initiatives are not only necessary to ensure that people have access to safe drinking water but also help reduce environmental pollution caused by the improper disposal of waste. These steps and investment activities are anticipated to provide the necessary push for the demand of rupture discs throughout the assessment period.

Rising Demand from Power Generation Industries Creates Market Demand

As natural gas is a clean-burning fuel, it is extensively used to generate electricity. The use of natural gas as an energy source is becoming increasingly important in the modern world. Currently, natural gas supplies 23% of the world's energy needs, making it one of the largest sources of energy globally. This percentage is only expected to increase as countries around the world continue to recognize its many advantages.

By 2040, the IEA projects that the demand for electricity will increase at a pace of 2.1% annually, which is twice as fast as the demand for primary energy. In addition, energy demand is expected to rise due to increased household incomes, electrification of transportation and domestic heating, and the rising need for air conditioning and digitally connected gadgets. Such an upgraded infrastructure for facilitating these processes is indirectly anticipated to drive the market for rupture discs.

Restraint - Replacement rate and Sensitivity of Device is Challenging

Frequent replacement requirements and operational sensitivity are emerging as significant challenges for the global rupture disc market. These devices, while highly effective for instantaneous pressure relief, are typically single-use components that demand replacement after activation or even minor installation damage. Such frequent maintenance increases operational downtime and overall lifecycle costs, particularly in high-pressure industries like oil & gas, chemical, and energy sectors.

Moreover, rupture discs are highly sensitive to temperature shifts, vibrations, and pressure surges, which can trigger premature failure or performance deviations. This sensitivity often discourages large-scale adoption where reliability and longevity are paramount, pushing industries to explore more durable, resettable alternatives, thereby restraining the market’s growth potential on a global scale.

Fluctuating Raw Material Prices and Supply Chain Vulnerabilities Pose a Major Challenge

Fluctuations in the prices of critical raw materials such as nickel, stainless steel, aluminum, and specialty alloys are emerging as a major challenge to the stability of the rupture disc market. According to the World Bank’s Commodity Markets Outlook (2024), metal prices have shown sharp volatility, with nickel prices rising by nearly 30% between 2021 and 2023 due to disruptions in key producing countries like Indonesia and Russia. Similarly, data from the U.S. Geological Survey (USGS) indicates that stainless steel input costs are heavily impacted by energy price spikes and uneven global supply recovery post-pandemic.

These unpredictable material trends significantly affect production costs and profit margins, particularly for manufacturers relying on precision-engineered metal components. In addition, supply chain vulnerabilities, including shipping delays, trade restrictions, and rising freight rates, have further constrained material availability and extended lead times.

The combination of volatile input costs and logistical uncertainties limits manufacturers’ ability to maintain consistent pricing, manage inventory efficiently, and fulfill time-sensitive industrial contracts, ultimately slowing down market growth and reducing competitiveness, especially for small and mid-tier producers operating under tight cost structures.

Opportunity - Integration of Smart Monitoring Systems Unlocks the Next Growth Wave in Rupture Disc Market

The most prominent opportunity shaping the future of the rupture disc market lies in the integration of advanced digital monitoring and smart pressure-management technologies. Governments and international bodies increasingly recognize the global manufacturing sector as a backbone of industrial growth; for instance, manufacturing accounted for approximately 17.5% of global value added in 2022. Meanwhile, adoption of advanced connectivity such as the Internet of Things (IoT) and cyber-physical systems is gaining traction: one report projects nearly 40 billion connected devices by the forecast period.

As industries increasingly move toward automation, predictive maintenance, and real-time asset monitoring, rupture discs are evolving from static safety devices into intelligent components of broader process-safety ecosystems. Incorporating pressure-sensing technology, data connectivity, and advanced analytics enables manufacturers of rupture discs to provide enhanced value by combining over-pressure protection with actionable insights.

This technological advancement aligns with the digital manufacturing agenda and opens up significant growth opportunities in sectors such as oil and gas, chemical processing, power generation, and pharmaceuticals. The shift towards "intelligent rupture disc systems" presents a major opportunity for market participants to expand into high-value segments, strengthen customer relationships, and future-proof their offerings in safety-driven, digitally enabled industrial environments.

Upcoming Mining Projects to Create Opportunities for Rupture Disc

Rupture discs have become an increasingly popular device used in the mining sector to help ensure the safety of miners. A rupture disc is designed to provide a secure pressure relief system for piping, vessels and equipment, which can be especially beneficial in areas where mining activities are dominated by hazardous materials.

Since mining projects call for a variety of equipment and safety relief devices in fluid control applications, it is anticipated that the demand for these devices will continue to grow. This is because many different types of equipment are needed when completing such projects, including valves, pumps, and other components.

Furthermore, safety relief devices are used to prevent the potential occurrence of accidents while working on such sites. As a result, manufacturers have been responding to this need by increasing production and introducing new products into their catalogs in an effort to keep up with customer requirements. It is anticipated that the expansion of mining projects in nations like Australia, Brazil, China, India, Russia, and South Africa will favourably impact the global rupture disc market.

Category-wise Insights

Application Insights

Rupture Disc in combination with Relief Valves holds a Significant Market Share in the Global Market

The rupture disc market is primarily segmented into rupture discs in combination with relief valves and standalone rupture disc systems, together forming the core of the global demand landscape. Among these, rupture discs used alongside relief valves dominate with an estimated 56.6% share, owing to their ability to deliver dual safety assurance and enhanced operational efficiency.

This combination is increasingly preferred across industries for its cost-effectiveness, temperature sensitivity, lightweight structure, and high reliability in preventing system failures or unnecessary downtime. The integrated setup provides both overpressure protection and rapid depressurization, making it highly suitable for gas as well as liquid handling applications in sectors such as oil & gas, chemical processing, power generation, and pharmaceuticals.

The demand for standalone rupture disc systems remains robust due to their instantaneous response, compact design, and maintenance-free operation, making them ideal for applications with confined installation spaces or high-frequency pressure variations.

Together, these two application categories reflect the market’s balanced reliance on comprehensive dual-protection assemblies and simplified standalone solutions, underscoring the broader industrial shift toward high-performance, regulatory-compliant, and cost-efficient pressure relief technologies across global operations.

End-user Insights

Oil & Gas Leads Market Adoption, While Chemicals Segment Registers Fastest Growth

The global rupture disc market is primarily driven by its adoption across oil & gas, chemical processing, power generation, pharmaceuticals, and food & beverage industries, each demanding high reliability in overpressure protection systems.

Among these, the oil & gas sector holds the most prominent market share, supported by extensive use in upstream extraction, refining, and pipeline transport applications where operational safety and emission control are critical. With increasing global energy consumption and aging infrastructure, operators are focusing on upgrading safety systems with high-performance rupture discs to mitigate explosion risks and ensure environmental compliance.

According to the U.S. Energy Information Administration (EIA), global oil demand is projected to exceed 103 million barrels per day by 2030, underscoring the continuous need for robust pressure management solutions in the sector.

The chemical industry is poised to register the most significant CAGR during the forecast period, driven by expanding production capacity, stricter safety mandates, and the growing integration of automated process control systems.

According to data from the OECD and UNIDO, global chemical output continues to rise, particularly in Asia and the Middle East, increasing the demand for precise, corrosion-resistant rupture discs to protect complex process lines. Collectively, these sectors reinforce the market’s evolution toward safety-driven and performance-optimized pressure relief solutions worldwide.

Region-wise Analysis

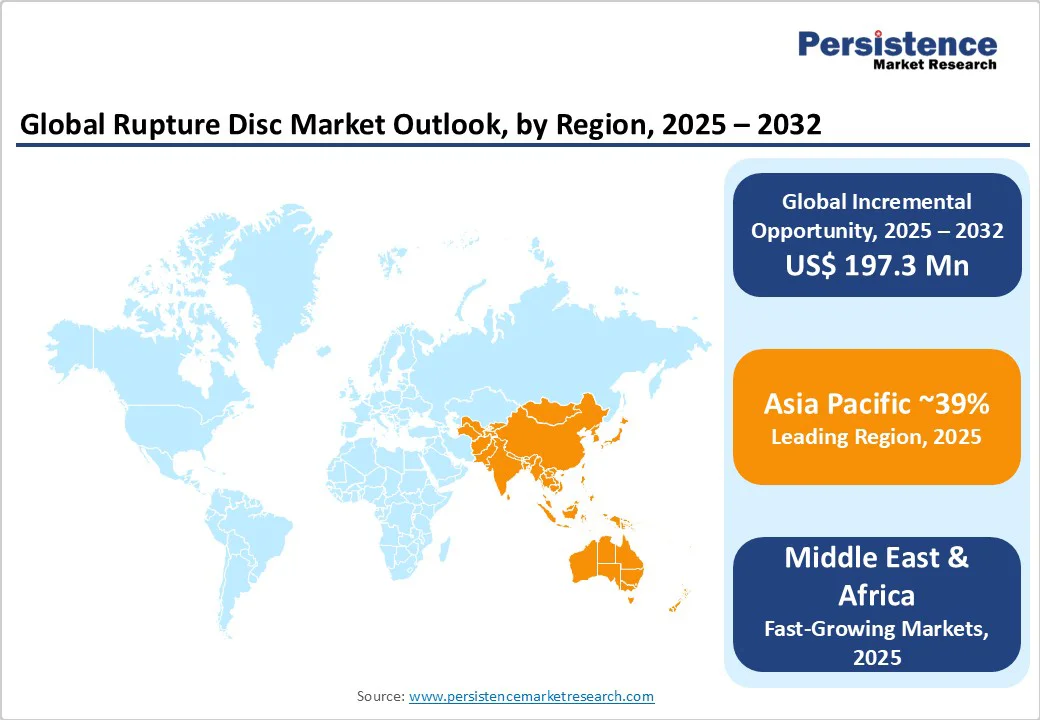

Asia Pacific to Exhibit Prominent Growth Driven by Expanding Industrial Infrastructure

Asia Pacific continues to hold a dominating presence of around 39% of share in the global rupture disc market, supported by rapid industrial development, expanding manufacturing capabilities, and growing focus on industrial safety compliance. The region’s growth is led by China, India, Japan, South Korea, and Southeast Asian economies, where rising investments in chemical processing, refining, and power generation sectors are boosting product demand.

China dominates regional consumption owing to its large-scale petrochemical expansion and strong export-oriented manufacturing base, while India is witnessing robust adoption driven by the government’s “Make in India” initiative and rapid growth in pharmaceutical and specialty chemical industries.

Japan and South Korea are advancing the use of high-performance, precision-engineered rupture discs as part of process automation and equipment safety upgrades. Meanwhile, Southeast Asia, including Indonesia, Thailand, and Malaysia, is emerging as a key contributor, supported by infrastructure development and foreign investments in manufacturing.

According to the Asian Development Bank (ADB), Asia’s industrial production is forecast to maintain growth above 4% annually through 2030, ensuring continued market momentum. Collectively, these developments position the Asia Pacific as a crucial contributor to global rupture disc demand, with expanding end-user industries and regulatory emphasis on process safety.

Europe to Maintain Steady Growth Supported by Established Industrial Base and Strong Manufacturing Ecosystem

The European continent has been an area of strong economic growth over the past several years, and certain countries have consistently maintained some of the strongest end markets in Europe. Germany is one such country with a thriving chemical and automotive industry.

France and the U.K. have one of the most established industrial sectors in the world, providing essential resources for growth across the region. For decades, these two countries have led the way in innovation and technological advances, developing new products and services for both domestic and international markets.

Additionally, other lucrative end users, including the food and beverage industry, have indicated significant demand for rupture discs and will continue to do so in the years to come. Germany is one of the top markets in the European region for rupture discs due to the presence of a large number of small and medium-sized manufacturers and their after-sales services. Germany is expected to account for about 5% of the global market value, and the U.K. is expected to achieve a CAGR of about 2.3% during the forecast period.

Middle East & Africa to Emerge as the Fastest-Growing Region with Rising Energy Investments

The Middle East & Africa (MEA) region is anticipated to register the fastest growth in the global rupture disc market with a CAGR of 4.0%, driven by escalating energy sector investments and expanding industrial capacity. In GCC nations, the use of rupture discs has increased significantly, fueled by rising oil and gas revenues, large-scale construction activities, and industrial diversification supported by sovereign wealth initiatives. Saudi Arabia, the United Arab Emirates, Kuwait, and Qatar, the core GCC states, lead the region’s demand, benefiting from strong oil and gas production coupled with downstream expansion projects.

The mining and power generation sectors across Africa are contributing to sustained market opportunities, supported by increased focus on plant safety and environmental protection. As governments across the region push for industrial modernization and process reliability, rupture disc manufacturers are witnessing growing demand from oil refineries, gas processing plants, and utility projects. With expanding manufacturing clusters and regulatory emphasis on pressure safety compliance, the MEA region is set to record a notable CAGR, establishing itself as a vital growth frontier in the global rupture disc industry.

Competitive Landscape

The global rupture disc is expected to be fairly fragmented in nature with a few players present in the market. The market participants are strategically focused on the development of new, cutting-edge, and highly effective goods along with tailored solutions to expand their client bases and increase their market shares.

To increase their market penetration, a number of unorganised firms are putting their efforts into developing items that are both personalised and affordable. Important industry participants are strategically boosting their market presence through alliances and partnerships with suppliers and dealers. Prominent companies are concentrating on significant investment in research and development activities to provide cost effective solutions.

PARKER, HANNIFIN CORP, Emerson Electric Co, Halma Plc, Mersen Group, V-TEX Corp are a few of the well-known global brands and big manufacturers who are planning to take on their own market positions and are anxious to protect their distinctive identities. The first reverse buckling rupture disc device equipped with knife blade technology was developed by BS&B®. The product was named the RB-90™.

Key Developments:

- In May 2023, Fike Corporation introduced the 1″ Axius SC bursting disc (sanitary/aseptic range) featuring a burst pressure range of 1.72 to 18.96 BARG in 316/316L stainless steel; includes a patent-pending sealing ring and fits standard ASME BPE ferrules without special hardware.

- In June 2025, Baker Hughes to acquire Continental Disc Corporation (CDC), a leading provider of rupture discs, rupture disc holders, burst disc indicators, and related pressure-management solutions, bolstering Baker Hughes’ pressure relief product portfolio in an all-cash deal of ~US$540 million.

Companies Covered in Rupture Disc Market

- Emerson Electric

- GE- Baker Hughes

- Parker Hannifin Corp

- IMI plc

- Yuanda Valve Grp

- Leser GmbH & Co KG

- Curtiss Wrieght Corp

- Mercer Valve Co. Inc

- Watts Water Technologies

- Alfa Laval AB

- CIRCOR International Inc

- Flow Safe Inc

- Mercury Manufacturing Company

- Groth Corporation

- HYDAC

Frequently Asked Questions

The global rupture disc market is likely to value at US$ 678.2 million in 2025.

The global rupture disc market is driven by rising demand from the oil and gas and power generation sectors, increasing investments in modern water and wastewater infrastructure, and a growing emphasis on industrial safety and advanced pressure control technologies.

The rupture disc market demonstrates robust growth at a 3.7% CAGR from 2025 - 2032.

Smart IoT integration enabling predictive maintenance, renewable energy infrastructure development requiring specialized valve technologies, and advanced materials for extreme applications present significant growth opportunities through 2032.

Market leaders include Emerson Electric Co, BS&B Safety Systems L.L.C, Fike Corporation, Parker Hannifin Corp, Halma Plc, Graco Inc.