- Semiconductor Materials & Components

- Rugged Embedded System Market

Rugged Embedded System Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Rugged Embedded System Market by Product Type (Single-Board Computers, Embedded Modules, Box PCs, Rack-Mount Systems, Panel PCs, Portable Systems, Others), Industry (Defense & Aerospace, Industrial & Manufacturing, Transportation, Energy & Utilities, Telecommunications, Healthcare, Others), and Regional Analysis, 2026 - 2033

Rugged Embedded System Market Size and Trend Analysis

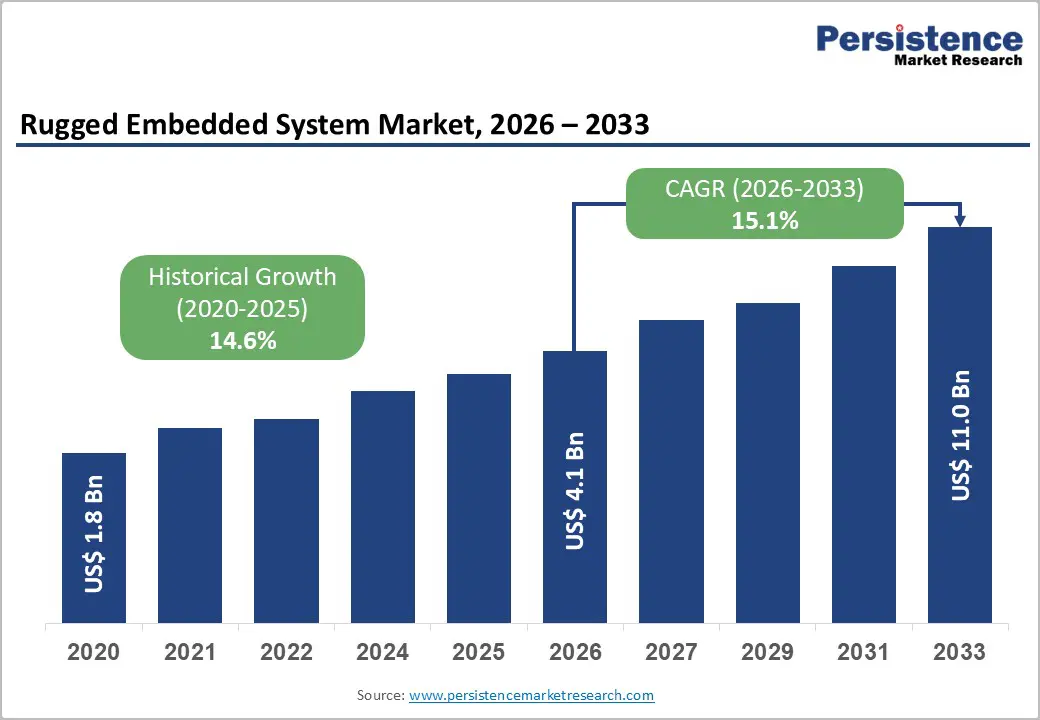

The global rugged embedded system market size is projected to be valued at US$ 4.1 billion in 2026 and is expected to reach US$ 11.0 billion by 2033, expanding at a CAGR of 15.1% during the forecast period from 2026 to 2033.

Market growth is driven by rising investments in defense and aerospace modernization, accelerating industrial automation, and the growing need for high-reliability computing in harsh environments. Defense agencies are upgrading mission-critical platforms such as UAVs, naval systems, and ground vehicles, while Industry 4.0 initiatives are boosting the adoption of rugged computing solutions across manufacturing, transportation, and energy sectors.

Key Market Highlights

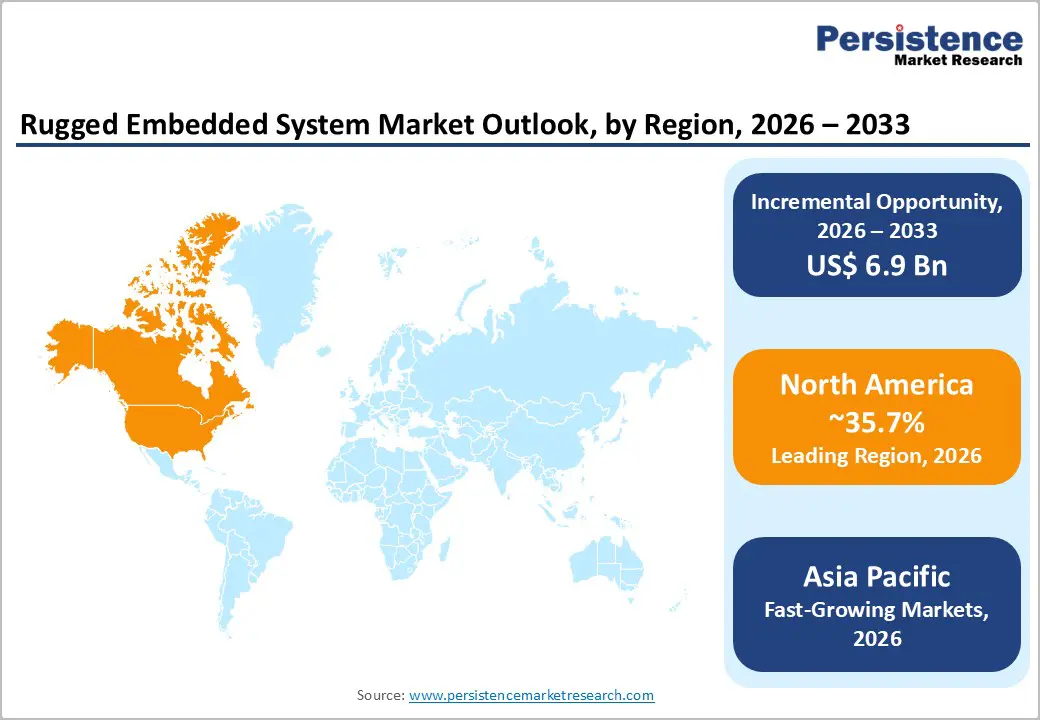

- Leading Region: North America leads with 35.7% of global revenues, driven by defense spending, aerospace, and industrial automation.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, accounting for 28.3% of revenues, driven by industrialization, manufacturing, and infrastructure expansion.

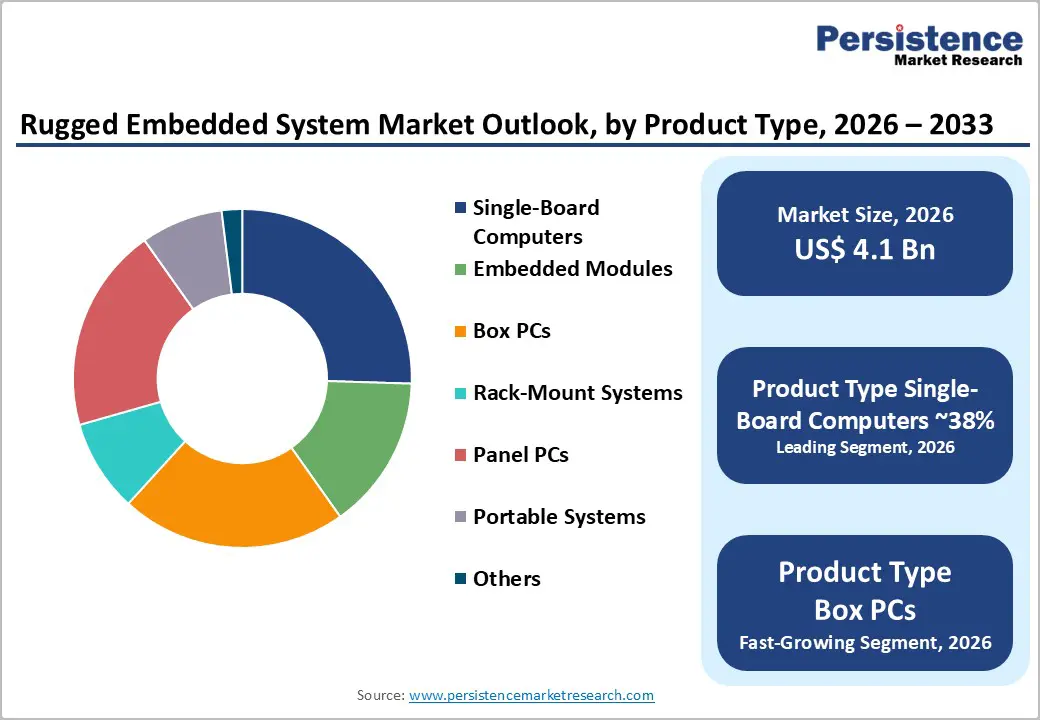

- Leading Category: Single-board computers and embedded modules hold 38% of the market, favored for modularity, ARM/x86 architectures, and robust software ecosystems.

- Fastest-Growing Region: Defense & aerospace drives 30-35% of demand, requiring reliable, certified electronics for avionics, UAVs, and mission systems.

- Key Market Opportunity: Edge computing and AI integration enable real-time analytics, predictive maintenance, and intelligent automation in the industrial and transportation sectors.

| Key Insights | Details |

|---|---|

| Rugged Embedded System Market Size (2026E) | US$ 4.1 billion |

| Market Value Forecast (2033F) | US$ 11.0 billion |

| Projected Growth CAGR (2026 - 2033) | 15.1% |

| Historical Market Growth (2020 - 2025) | 14.6% |

Market Dynamics

Drivers - Rising Defense and Aerospace Modernization Investments

Escalating defense and aerospace modernization programs are a major growth driver for rugged embedded systems, as mission-critical platforms increasingly depend on high-performance onboard computing. Defense budgets worldwide continue to prioritize next-generation capabilities such as advanced sensors, electronic warfare, secure communications, and autonomous systems, all of which require reliable embedded electronics capable of operating in extreme and unpredictable environments.

Embedded computing units deployed in radar systems, avionics suites, unmanned aerial vehicles, naval platforms, and ground vehicles must comply with stringent military and aerospace standards while delivering real-time processing. These systems are required to function under severe temperature fluctuations, shock, vibration, and electromagnetic interference, driving sustained demand for rugged single-board computers, conduction-cooled modules, and secure embedded networking solutions.

Industrial Automation and Smart Manufacturing Expansion

The rapid expansion of industrial automation and smart manufacturing is another key driver accelerating the adoption of rugged embedded systems. Manufacturing plants, process industries, and logistics facilities are increasingly integrating IoT, edge computing, and advanced control technologies to improve operational efficiency, productivity, and system visibility across production environments.

Rugged embedded computers such as box PCs, panel PCs, and rack-mounted systems are deployed close to production lines, outdoor yards, and heavy machinery, where conventional IT hardware cannot survive. Their ability to withstand dust, moisture, vibration, and electrical noise enables real-time machine monitoring, predictive maintenance, and seamless integration with SCADA and industrial control platforms, supporting higher uptime and optimized manufacturing performance.

Restraints - Thermal Management and Reliability Challenges

Thermal management is a critical restraint for rugged embedded systems as higher processing densities are integrated into compact, sealed enclosures. Advanced CPUs, GPUs, and FPGAs generate substantial heat, and systems are often required to operate in ambient temperatures exceeding +70°C in environments such as engine compartments, outdoor cabinets, and deserts. Ineffective heat dissipation can shorten component lifespan, trigger performance degradation, and cause intermittent failures that are difficult to diagnose in field deployments.

To maintain reliability under these conditions, manufacturers must adopt sophisticated thermal strategies, including conduction cooling, optimized heat spreaders, ruggedized airflow designs, and extensive environmental testing. These requirements significantly increase design complexity, validation effort, and production costs, ultimately slowing product development cycles and delaying market introduction of new rugged platforms.

High Development, Certification, and Integration Costs

High development, certification, and integration costs represent another major restraint in the rugged embedded system market, particularly for safety- and mission-critical applications. Compliance with aerospace, defense, rail, and industrial standards demands extensive design validation, documentation, and long qualification cycles, driving up non-recurring engineering expenses and extending time to commercialization.

Rugged embedded deployments often require customized hardware configurations, long-term component availability, and guaranteed software support over 10-15 years. These lifecycle commitments significantly increase supplier risk and cost compared with short-refresh commercial IT products, creating financial barriers for smaller OEMs and system integrators and limiting the pace of innovation in the market.

Market Opportunities

Edge Computing and Artificial Intelligence Integration

The integration of edge computing and artificial intelligence (AI) into rugged embedded platforms offers a significant growth opportunity, enabling real-time data analytics in remote or bandwidth-constrained environments. In industrial automation, edge AI systems support predictive maintenance, quality control, and energy optimization, with studies showing a 20-30% reduction in unplanned downtime when AI processes sensor data locally rather than relying solely on cloud computing.

Rugged edge nodes equipped with AI accelerators or GPUs can be deployed on production lines, mining vehicles, or railway tracks to perform object detection, anomaly identification, and condition monitoring directly at the source. As 5G and Industrial IoT ecosystems mature, the demand for compact, rugged systems capable of executing AI workloads at the edge while withstanding vibration, temperature extremes, and ingress hazards is expected to grow rapidly.

Telecommunications, 5G, and Critical Infrastructure Rollout

The global rollout of 5G networks and modernization of power, water, and transportation infrastructure present further opportunities for rugged embedded systems. Telecom vendors are embedding controllers into base stations, small cells, and edge data centers that must operate in towers, on rooftops, and in street cabinets, exposed to dust, moisture, and wide temperature variations. High-performance functions such as massive MIMO, ultra-low latency, and network slicing require distributed computing that is highly reliable and fault-tolerant.

Similarly, utilities are upgrading grids with intelligent electronic devices, SCADA systems, and smart meters, particularly in regions like South Asia, the Middle East, and Africa. This ongoing infrastructure transformation drives demand for rugged rack-mounted systems and embedded modules capable of secure, deterministic operation in substations, renewable energy plants, and remote pipelines, reinforcing market growth across multiple critical sectors.

Category-wise Analysis

Product Type Insights

Single-board computers (SBCs) and embedded modules dominate the rugged embedded system market, accounting for around 38% of total revenues. ARM-based SBCs lead with 40-45% value share due to their power efficiency, performance, and broad ecosystem support. Linux and other open-source operating systems run on over half of these boards, allowing customization and long-term support. SBCs and modules act as core compute units in box PCs, panel PCs, and portable devices, enabling OEMs to standardize platforms while customizing I/O and enclosures. Their modularity, scalability, and software ecosystem make them ideal for rapid deployment in industrial, defense, and transportation applications.

Rugged box PCs and panel PCs are the fastest-growing categories. These systems are increasingly used in industrial automation, smart manufacturing, and transportation. Their robust design allows operation in harsh conditions like dust, vibration, extreme temperatures, and moisture. They provide real-time processing, predictive maintenance, and connectivity to SCADA and industrial control systems, making them essential for environments where standard IT hardware fails.

Industry Insights

The defense & aerospace sector is the largest end-use segment, contributing about 30-35% of demand. Embedded systems are critical for flight control, mission management, navigation, electronic warfare, and secure communications in aircraft, UAVs, helicopters, and missile platforms. Defense modernization initiatives globally prioritize sensor fusion, network-centric operations, and high-reliability electronics that meet MIL-STD and DO-254 standards. Long product lifecycles and strict obsolescence management requirements further reinforce demand for rugged embedded solutions in this sector.

Industrial automation and transportation are the fastest-growing end-use segments. Rugged embedded systems, including box PCs, panel PCs, and portable devices, are increasingly deployed on factory floors, production lines, and transportation hubs. They enable real-time monitoring, predictive maintenance, IoT connectivity, and automation in harsh conditions such as dust, vibration, and extreme temperatures. These applications drive rapid adoption as industries modernize and adopt smart manufacturing and Industry 4.0 initiatives.

Regional Insights

North America Rugged Embedded System Market Trends

North America is the leading regional market for rugged embedded systems, accounting for approximately 35.7% of global revenues. Strong defense spending, a mature aerospace manufacturing base, and a well-established industrial automation ecosystem in the U.S. and Canada drive demand. The U.S. defense budget allocates tens of billions annually to electronic warfare, autonomous platforms, and command-and-control systems, all of which rely on rugged embedded computing. Major aerospace OEMs use certified SBCs, embedded modules, and I/O devices in avionics, engine controls, and flight test systems.

Beyond defense, industrial sectors such as automotive, oil and gas, and utilities are adopting SCADA upgrades, edge computing, and digital control systems. Compliance with UL, FCC, and aviation and rail standards favors established vendors. A strong innovation ecosystem, including leading semiconductor and industrial automation firms, further accelerates the adoption of high-performance rugged embedded systems in both brownfield and greenfield projects.

Europe Rugged Embedded System Market Trends

Europe demonstrates steady growth in rugged embedded systems, driven by advanced manufacturing, regulatory compliance, and energy transition initiatives. The region is witnessing robust adoption in smart factories, industrial IoT, and digitalized production, with directives such as the Machinery Directive and Radio Equipment Directive harmonizing safety and performance standards. Vendors such as Siemens AG and Kontron AG supply rugged PCs, HMIs, and embedded controllers for rail, energy, and factory automation.

Europe’s focus on renewable energy expansion and decarbonization further boosts demand for reliable embedded devices in wind, solar, and grid monitoring. The region is expected to grow at a CAGR of 12.3% during the forecast period, supported by strong investments in industrial digitalization, transportation safety, and smart infrastructure deployment.

Asia Pacific Rugged Embedded System Market Trends

Asia Pacific is emerging as the fastest-growing regional market, contributing roughly 28.3% of global rugged embedded system revenues. Growth is fueled by large-scale industrialization, electronics manufacturing, and infrastructure development in China, Japan, South Korea, and India. Smart manufacturing initiatives, industrial modernization programs, and the adoption of robotics are driving demand for rugged SBCs, embedded modules, and panel PCs in factory automation, machine tools, and inspection equipment.

Investments in transportation, energy, and logistics infrastructure in India and ASEAN economies further support market expansion. Governments are promoting digitalization and local development of embedded solutions, including edge computing for smart factories and smart cities. Competitive manufacturing costs and a growing base of regional suppliers reinforce Asia Pacific as a key growth engine over the forecast period.

Competitive Landscape

The rugged embedded system market is moderately concentrated, comprising a mix of large multinational corporations and specialized niche providers serving defense, industrial, and transportation sectors. Key competition revolves around product reliability, long-term availability, robust software ecosystems, and domain-specific application expertise. Market growth is supported by strong demand for mission-critical systems in aerospace, defense, and industrial automation, which require high-performance computing under extreme environmental conditions.

Companies are adopting strategies to strengthen their market position, including expanding edge AI capabilities, improving thermal and environmental performance, and forming strategic partnerships with semiconductor and software vendors. Focus is also shifting toward high-growth verticals such as smart manufacturing, electric mobility, renewable energy, and 5G infrastructure to capture emerging opportunities.

Key Market Developments

- In February 2025, Curtiss-Wright Corporation issued guidance and results indicating higher sales and robust bookings in its aerospace and defense segments, supported by increased demand for mission-critical embedded computing solutions in military flight, naval, and ground systems.

- In November 2025, AAEON Technology Inc. announced the PICO-ARU4, described as one of the first Pico-ITX boards based on Intel Core Ultra (Series 2) processors, integrating up to 32 GB LPDDR5 memory and rugged mechanical features for compact AI and edge computing applications.

- In October 2025, AAEON presented multiple edge computing platforms, including smart roadside and industrial solutions leveraging Intel technologies, highlighting the ongoing innovation in rugged, AI-ready embedded systems for transportation and smart city deployments.

Companies Covered in Rugged Embedded System Market

- Advantech Co., Ltd.

- Kontron AG

- Curtiss-Wright Corporation

- Siemens AG

- Rockwell Automation, Inc.

- Emerson Electric Co.

- ABB Ltd.

- Intel Corporation

- AAEON Technology Inc.

- Crystal Group, Inc.

- Portwell, Inc.

- Vecow Co., Ltd.

- OnLogic, Inc.

- Elma Electronic AG

- ADLINK Technology Inc.

Frequently Asked Questions

The rugged embedded system market is projected to grow from US$ 4.1 billion in 2026 to US$ 11.0 billion by 2033, at a CAGR of 15.1%, driven by defense, industrial, and telecom deployments.

Key drivers include rising defense and aerospace budgets, strong industrial automation and smart factory adoption, and growing integration of edge computing and AI in harsh environments.

Single-board computers and embedded modules, holding around 38% of total revenues, dominate the market due to modularity, software ecosystem, and use in box PCs, panel PCs, and portable systems.

North America, with 35.7% of global revenues, leads the market due to U.S. defense and aerospace spending, industrial automation, and advanced innovation ecosystems.

A major opportunity lies in rugged edge computing with AI acceleration for predictive maintenance, real-time analytics, and autonomous decision-making in industrial, energy, and transportation sectors.

Leading companies include Advantech Co., Ltd., Kontron AG, Curtiss-Wright Corporation, Siemens AG, and Rockwell Automation, Inc.