- Technology

- Quantum Computing Market

Quantum Computing Market Size, Share, and Growth Forecast 2026 - 2033

Quantum Computing Market by Components Type (Quantum Computing Devices, Quantum Computing Software and Quantum Computing Services), by Application (Simulation & Testing, Financial Modelling, Artificial Intelligence & Machine Learning, Cybersecurity & Cryptography and Others), and Industry (Healthcare & Life Sciences, Banking & Financial Services, Manufacturing, Academics & Research, Aerospace & Defence, Energy & Utilities, IT & Telecom and Others) and Regional Analysis for 2026 – 2033

Quantum Computing Market Size and Trend Analysis

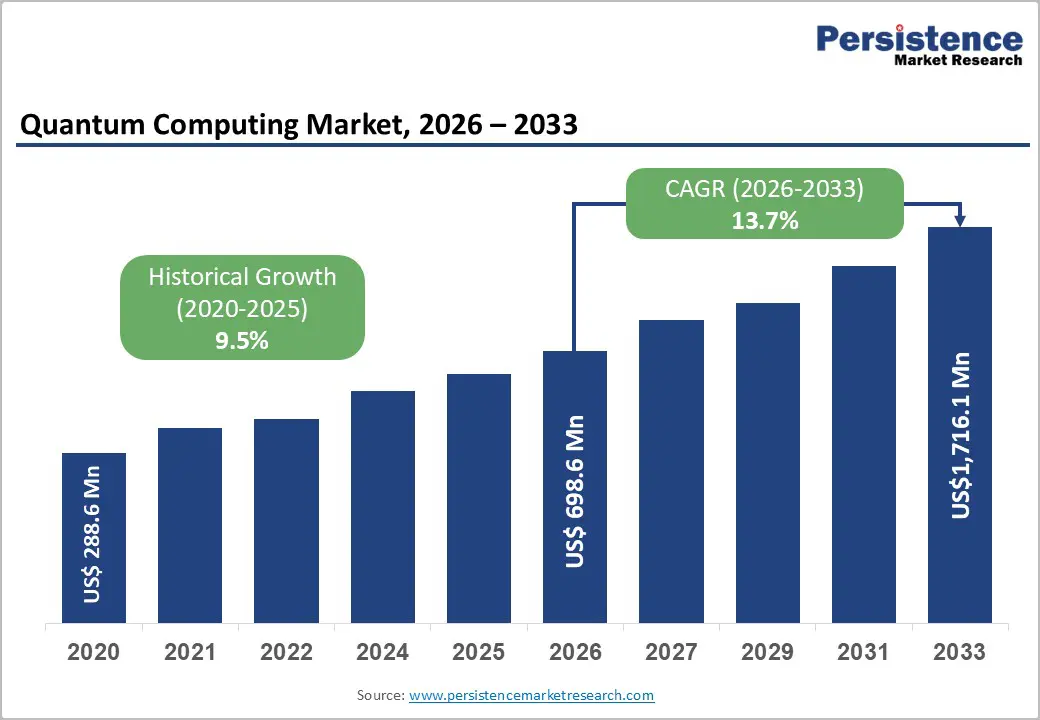

The global Quantum Computing Market size was valued at US$ 698.6 million in 2026 and is projected to reach US$ 1,716.1 million by 2033, growing at a CAGR of 13.7% between 2026 and 2033. The market is being driven by rapidly advancing quantum hardware architectures, strategic investments from major technology corporations including IBM Corporation, Microsoft Corporation, and Google, coupled with substantial government funding initiatives aimed at achieving practical quantum advantage in near-term applications.

Key Market Highlights

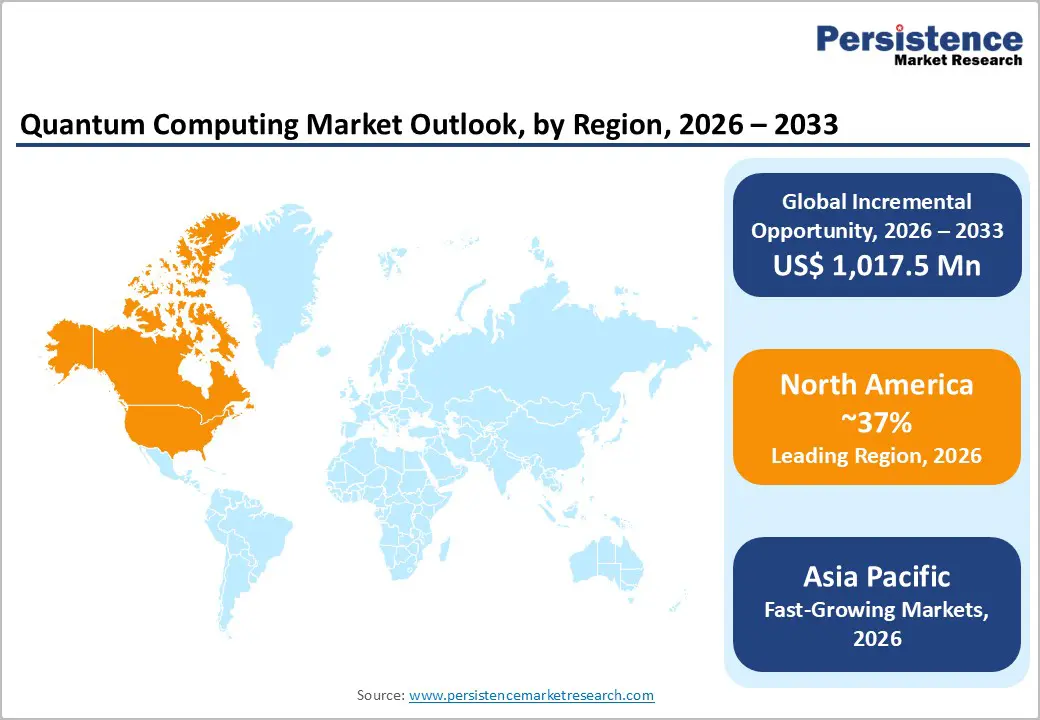

- Leading Region: North America dominates the quantum computing market with approximately 37% global share, driven by United States leadership through substantial government funding including $2.5 billion Department of Energy commitment, presence of major quantum computing companies, and advanced research ecosystem supporting quantum innovation and commercialization.

- Fastest growing region: Asia-Pacific emerges as the fastest-growing region with accelerating government investments including Japan's $7.4 billion commitment, China's 1 trillion-yuan venture fund, and Australia's $620 million PsiQuantum investment supporting quantum infrastructure development and commercialization pathways.

- Dominant segment: Quantum Computing Devices represent the dominant segment commanding approximately 64% market share, reflecting hardware's foundational role and substantial capital intensity of developing superconducting, trapped ion, neutral atom, and photonic quantum systems.

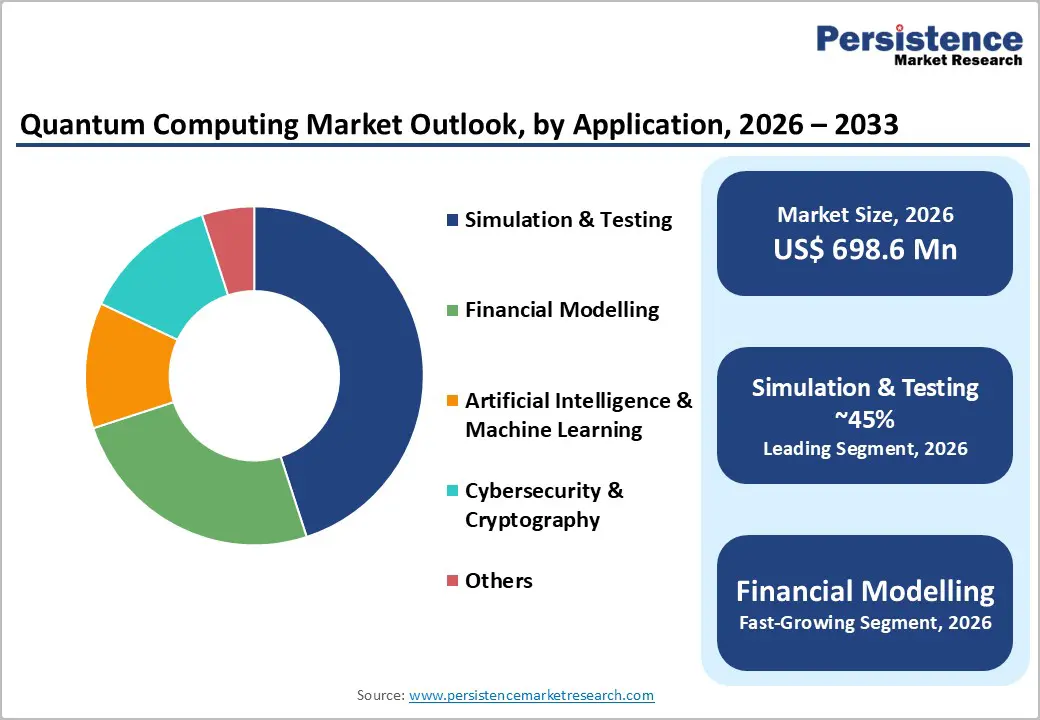

- Fastest growing segment: Artificial Intelligence & Machine Learning represents the fastest-growing application segment with projected 15% annual growth, driven by organizations recognizing quantum's transformative potential for accelerating machine learning model training and enabling previously impossible computational tasks.

- Key market opportunity: Quantum-Enhanced Artificial Intelligence Applications represent the key market opportunity, promising exponential acceleration of machine learning processes and transformation of AI capabilities across healthcare, finance, manufacturing, and logistics sectors through hybrid quantum-classical computing architectures.

| Key Insights | Details |

|---|---|

| Quantum Computing Market Size (2026E) | US$ 698.6 Mn |

| Market Value Forecast (2033F) | US$ 1,716.1Mn |

| Projected Growth (CAGR 2026 to 2033) | 13.7% |

| Historical Market Growth (CAGR 2020 to 2024) | 9.5% |

Market Dynamics

Market Growth Drivers

Accelerating Quantum Hardware Development and Cloud-Based Accessibility

The quantum computing sector is experiencing unprecedented momentum driven by significant breakthroughs in hardware development and the expansion of cloud-based quantum computing platforms. IBM Corporation released its detailed blueprint in June 2026 outlining a path toward a fault-tolerant quantum supercomputer by late 2029, while Google demonstrated substantial progress with its Willow chip achieving scalable error correction with approximately 105 qubits, solving computational problems in under five minutes that would theoretically require classical supercomputers over 10 septillion years to complete. Microsoft Azure Quantum has created a comprehensive ecosystem combining multiple quantum hardware modalities from partners including Quantinuum, IonQ, and Atom Computing, enabling researchers and enterprises to access cutting-edge quantum systems without massive capital expenditures.

Growing Quantum Applications in Artificial Intelligence, Pharmaceuticals, and Financial Services

Quantum computing's transformative potential in artificial intelligence and machine learning has become increasingly evident, with organizations recognizing quantum's capacity to dramatically accelerate machine learning processes and overcome computational limitations of classical systems. McKinsey estimates potential value creation of $200 billion to $500 billion by 2035 specifically from quantum computing applications in life sciences and drug discovery, driven by quantum's exceptional ability to perform first-principles calculations of molecular interactions. IBM and Moderna collaborated to simulate the longest mRNA sequence (60 nucleotides) ever modeled on quantum computers using 80 of 156 qubits on IBM's Heron chip, demonstrating practical near-term applications in pharmaceutical development.

Market Restraints

Technical Complexity and Error Correction Challenges

Quantum computing systems face formidable technical barriers that continue to impede large-scale commercialization and widespread adoption across industries. Qubits are inherently unstable and extraordinarily sensitive to environmental disturbances including electromagnetic interference, temperature fluctuations, and stray cosmic particles, requiring extremely cold operating environments maintained at near-absolute-zero temperatures using specialized cryogenic equipment costing millions of dollars. Error rates in quantum systems compound as qubit counts increase, with thousands of physical qubits required to create a single reliable logical qubit through redundancy and error correction protocols, creating substantial engineering and cost challenges. The lack of standardized quantum software frameworks and development tools creates fragmentation across the industry, hindering rapid application development and limiting adoption among non-specialist organizations.

High Capital Requirements and Limited Commercial Revenue Generation

Quantum computing technology requires extraordinarily expensive infrastructure investment, with specialized quantum hardware systems costing between $10 million and $100 million depending on qubit count and modality, alongside expensive cooling systems, control electronics, and supporting classical computing infrastructure. Current quantum computing startups and mature companies are generating minimal commercial revenue relative to investment levels, with most enterprises pursuing loss-making business models focused on research and development rather than profitable services. Organizations deploying quantum systems face significant opportunity costs associated with staff retraining, integration with existing IT infrastructure, and extensive testing requirements before moving to production applications. The immaturity of the quantum software ecosystem means enterprises must often develop custom quantum algorithms and applications rather than purchasing standardized solutions, dramatically increasing time-to-value and project risk for early adopters.

Market Opportunities

Quantum-Enhanced Artificial Intelligence and Machine Learning Acceleration

The convergence of quantum computing with artificial intelligence and machine learning represents one of the most compelling near-term market opportunities, as quantum systems promise exponential acceleration of training processes for advanced machine learning models. Quantum algorithms can process vast, high-dimensional datasets simultaneously through superposition principles, dramatically reducing training time for neural networks and deep learning models that currently require weeks of classical compute time. Organizations are developing hybrid quantum-classical machine learning systems where quantum processors handle computationally intensive components while classical systems manage data preparation and result integration, creating practical near-term value without requiring fully mature quantum computers. Siemens collaborated with IQM and academic partners to demonstrate Quantum Reservoir Computing applied to complex chemical reactor control, achieving accurate predictions using only a five-qubit system and 600 historical data points, illustrating quantum machine learning's immediate practical utility.

Quantum Cybersecurity Solutions and Post-Quantum Cryptography Implementation

The urgent need for quantum-resistant encryption and cybersecurity solutions is creating substantial market opportunities as organizations prepare for threats posed by future large-scale quantum computers. Quantum Key Distribution (QKD) and post-quantum cryptographic algorithms are receiving accelerated investment from governments and financial institutions preparing for the "quantum threat," with several nations including the United States, European Union, and United Kingdom advancing quantum-safe encryption standards. The healthcare sector faces vulnerability, with quantum computers potentially compromising existing encryption protecting billions of patient medical records and personal health information, driving significant adoption of quantum-resistant cybersecurity solutions. Global governments are mandating migration to quantum-safe encryption, with organizations needing to implement post-quantum cryptographic infrastructure well before large-scale quantum computers become operational, creating a multi-year implementation cycle generating substantial consulting, software development, and integration services revenue.

Category-wise Insights

Components Type Analysis

Quantum Computing Devices represent the foundational segment capturing approximately 64% of the quantum computing market, as quantum hardware forms the essential foundation for all quantum computing capabilities and applications. This segment encompasses superconducting qubit systems developed by companies including IBM, Google, and D-Wave, trapped ion architectures advanced by IonQ and Quantinuum, neutral atom systems from Atom Computing, and photonic quantum approaches from Xanadu Quantum Technologies, with each technology pursuing distinct pathways toward practical quantum advantage. The dominance of quantum computing devices reflects substantial capital intensity and technological complexity of hardware development, with IBM and Google alone investing billions annually in quantum hardware research and infrastructure. D-Wave Systems expanded its position through its $550 million acquisition of Quantum Circuits, acquiring dual-rail transmon qubit technology and advanced cryogenic packaging capabilities that strengthen its competitive position across both annealing and gate-model quantum computing architectures.

Application Analysis

Simulation & Testing emerges as the leading application segment, capturing approximately 45% of quantum computing market share, driven by quantum's exceptional capability to accurately model complex molecular and chemical systems that classical computers cannot efficiently simulate. Quantum simulation enables researchers to understand molecular interactions, predict chemical reaction outcomes, and explore material properties at the atomic level with unprecedented accuracy, directly supporting drug discovery, material science, and fundamental physics research applications. The pharmaceutical industry has embraced quantum simulation as a critical technology for accelerating drug development, with companies including Roche, AstraZeneca, Boehringer Ingelheim, and Merck collaborating with quantum computing providers to simulate protein structures, predict drug-target interactions, and assess off-target effects that would require expensive wet laboratory experiments through traditional approaches. Financial Modelling applications are experiencing accelerating adoption as financial institutions recognize quantum's capability to dramatically enhance portfolio optimization, risk assessment, and Monte Carlo simulations currently requiring massive computational resources and extended processing time.

Industry Analysis

Healthcare & Life Sciences dominates industry adoption among quantum computing end-users, commanding approximately 38-42% of market share, driven by pharmaceutical and biotechnology companies recognizing quantum's transformative potential in drug discovery and development processes. Quantum computing promises to reduce drug development timelines and costs through accurate molecular simulation, protein folding analysis, and identification of promising drug candidates before expensive clinical trials, representing potential value creation of $200-500 billion through 2035 in this sector alone.

Banking & Financial Services captures approximately 28-32% of quantum computing market share, reflecting financial institutions' focus on leveraging quantum algorithms for portfolio optimization, risk modeling, fraud detection, and algorithmic trading applications where quantum computing offers measurable computational advantages. Manufacturing represents an emerging high-growth sector for quantum computing applications, with companies exploring quantum optimization for supply chain management, production scheduling, and process control, particularly through quantum-enhanced machine learning approaches demonstrated by Siemens and university research collaborations.

Regional Insights

North America

North America maintains strong market leadership with approximately 37% of global quantum computing market share, primarily driven by United States dominance reflecting substantial government investment, presence of leading quantum computing companies, and extensive research infrastructure. The U.S. Department of Energy announced $2.5 billion in quantum funding through fiscal year 2030, including $775 million for the DOE Quantum Information Science Research Program, $875 million for National Quantum Information Science Research Centers, and $500 million for Quantum Network Infrastructure development, providing sustained resources for quantum research advancement and commercialization.

IBM Corporation, headquartered in Armonk, New York, released its industrial-scale quantum computing blueprint in June 2026, planning construction of the world's first large-scale fault-tolerant quantum computer at its newest data center in Poughkeepsie, New York, representing a substantial commitment to quantum infrastructure development in North America. Google's quantum research operations in Santa Barbara, California have pioneered breakthroughs in quantum error correction and chip manufacturing, with the company establishing its own dedicated Willow chip production facility to accelerate development cycles.

Europe

Europe is pursuing a coordinated, collaborative quantum computing strategy through its Quantum Flagship Program, allocating €1 billion over ten years combined with €400+ million in linked funding under Horizon Europe, positioning the region as a major quantum innovation hub. The European Union is deploying nine quantum systems across at least seven countries including Czechia, Germany, Spain, France, Italy, and Poland through the EuroHPC initiative, fostering equitable access to quantum computing infrastructure and supporting diverse quantum technology approaches spanning superconducting, ion-trap, and quantum annealing architectures.

Germany maintains substantial quantum computing investment through national programs and European initiatives, hosting quantum systems at Forschungszentrum Jülich including D-Wave's 5,000-qubit Advantage system, supporting research collaboration and industrial application development. Spain announced its Quantum Technologies Strategy 2026-2030 supported by €808 million in funding, establishing the nation as a regional quantum computing leader through infrastructure development and ecosystem creation.

Asia Pacific Quantum Computing Trends

Asia-Pacific is emerging as the fastest-growing quantum computing region, with China establishing a national venture capital guidance fund mobilizing 1 trillion yuan (approximately $138 billion) toward quantum technology and artificial intelligence development, supporting aggressive quantum computing capability building. China has invested approximately $15 billion (estimated) in quantum technologies according to various assessments, with the government targeting expansion of quantum communications infrastructure, development of a general quantum computer prototype, and construction of practical quantum simulators by 2030. Japan announced a landmark $7.4 billion quantum computing commitment in 2026, positioning the nation as a major quantum innovation center through aggressive funding and strategic infrastructure development. South Korea is advancing quantum capabilities through partnerships including IonQ and KiSTI finalizing plans to deploy a 100-qubit quantum system in the country, supporting semiconductor industry development and quantum applications.

Competitive Landscape Market Structure Analysis

The quantum computing market exhibits a consolidated structure dominated by large technology corporations including IBM Corporation, Microsoft Corporation, Google, and Intel Corporation, which leverage substantial capital resources, research infrastructure, and enterprise relationships to advance quantum computing across multiple technology modalities and applications. Pure-play quantum computing startups including D-Wave Systems, IonQ, Quantinuum, Atom Computing, Rigetti Computing, Xanadu Quantum Technologies, and Zapata Computing compete through specialized technological approaches, targeted application development, and cloud-based service delivery models.

Market leaders are pursuing dual-platform strategies combining multiple quantum architectures-Wave acquiring Quantum Circuits for gate-model capabilities while maintaining annealing systems, Microsoft supporting multiple hardware partners through Azure Quantum, and IBM advancing superconducting qubit leadership while exploring topological approaches.

Key Market Developments

- In January 2025, Accenture strategically invested in QuSecure, a leader in post-quantum cybersecurity, to offer comprehensive crypto agility solutions against emerging quantum risks. Together, they provide solutions that adhere to NIST's post-quantum encryption standards, crucial for protecting sensitive data like emails and e-commerce transactions.

- In November 2024, IBM announced the launch of its most advanced quantum computers, representing a significant leap forward in quantum computing technology. These new systems are engineered to deliver enhanced performance, greater stability, and improved scalability, pushing the boundaries of what's possible in the quantum realm.

Companies Covered in Quantum Computing Market

- IBM Corporation

- Microsoft Corporation

- Huawei

- Intel Corporation

- ColdQuanta

- D-Wave Systems Inc.

- Atom Computing Inc

- Xanadu Quantum Technologies Inc.

- Zapata Computing, Inc.

- Other Key Players

Frequently Asked Questions

The global Quantum Computing Market was valued at US$ 698.6 million in 2026 and is projected to reach US$ 1,716.1 million by 2033, representing a CAGR of 13.7% during the forecast period, driven by accelerating quantum hardware development, expanding cloud-based accessibility, growing applications in artificial intelligence and machine learning, and substantial government investments in quantum research infrastructure globally.

The primary demand drivers include accelerating quantum hardware development with breakthroughs in error correction demonstrated by Google's Willow chip and IBM's industrial-scale quantum blueprint, growing applications in pharmaceutical drug discovery and molecular simulation, expanding adoption of quantum algorithms in financial services.

Quantum Computing Devices represent the leading component segment, capturing approximately 64% of market share, reflecting the foundational importance of quantum hardware and substantial capital intensity of developing superconducting qubits, trapped ion systems, neutral atom architectures, and photonic quantum computing platforms across multiple technology modalities.

North America currently leads the quantum computing market with approximately 37% global market share.

Key market players include IBM Corporation, Microsoft Corporation, Google, D-Wave and Quantinuum advancing.